China's RDC Radiopharmaceutical Story: How Many Mountains Remain to Climb?

SK Biopharmaceuticals

A biopharmaceutical company

In July 2023, South Korean biopharmaceutical company SK Biopharmaceuticals unveiled a new strategic plan, which includes building models and platforms for radiopharmaceutical therapy (RPT), with the aim of becoming one of the leading RPT companies in Asia and the United States.

Exactly one year later, SK Biopharmaceuticals entered into a collaboration with Fuliang Technology, a Chinese nuclear medicine biotech company, with a total transaction value of $571.5 million. Fuliang Technology granted SK Biopharmaceuticals exclusive global rights for the clinical development, manufacturing, and commercialization of FL-091, a radiopharmaceutical targeting neurotensin receptor 1 (NTSR1)-positive cancers. Additionally, SK Biopharmaceuticals holds right of first negotiation for other pre-selected radiopharmaceutical drug conjugate (RDC) projects from Fuliang Technology.

Since the beginning of this year, global collaborations and transactions in the radiopharmaceutical sector have been continuous, primarily characterized by acquisitions, investments, or co-development agreements between multinational corporations (MNCs) and biotechnology companies, as well as partnerships among domestic radiopharmaceutical firms. The business development deal between Fulian and SK Biopharmaceuticals marks the first license-out transaction by a Chinese radiopharmaceutical company.

2024 Transactions and Collaborations in the Radiopharmaceutical Sector, Compiled by VCBeat

Although Fuliang is a relatively young company, it has already established itself as a global enterprise. Beyond its home market in China, Fuliang has taken root in Europe—the region with the most comprehensive nuclear medicine policies and the most mature industrial chain—where it has rapidly expanded by building teams covering early-stage research, procurement, logistics, and clinical development, thereby establishing a global footprint in R&D, clinical operations, and supply chain management.

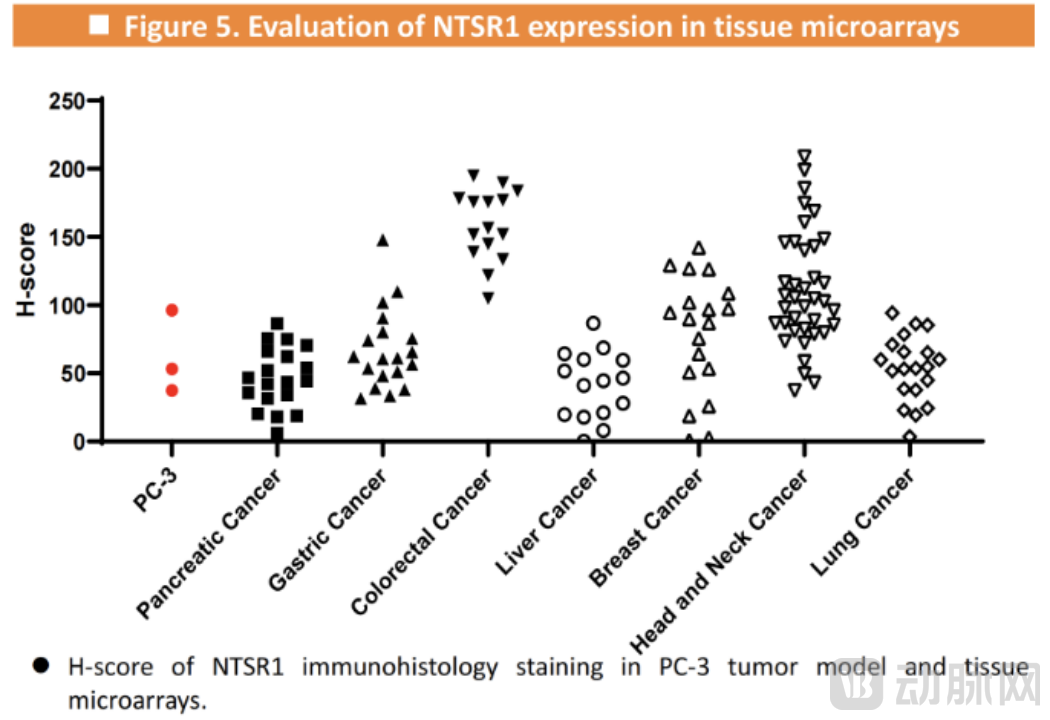

In late 2022, Fulian acquired Focus-X Therapeutics, based in New Jersey, USA, for $245 million to bolster its technological platform and product pipeline in the peptide field.Among them is a neurotensin receptor 1 (NTSR1)-targeting peptide with potential for treating pancreatic cancer—the very centerpiece of this license-out deal.NTSR1 modulates the role of the neuropeptide hormone neurotensin in the gastrointestinal system. Overexpression of NTSR1 is associated with colorectal, breast, pancreatic, and head and neck cancers, making it a promising target for diagnostic imaging and radioligand therapy.

Following the completion of the acquisition, Dr. Liu Fa, founder of Focus-X Therapeutics, became the Chief Scientific Officer of Focused Ultrasound Technology. This June, Dr. Liu2024At the SNMMI (Society of Nuclear Medicine and Molecular Imaging) Annual Meeting, positive preclinical data for NTSR1 (FL-091) were presented. This chelating radiopharmaceutical demonstrated favorable biodistribution characteristics and potent antitumor activity. Studies indicated that the NTSR1 positivity rate across different indications ranged from 10.71% to 54.29%, with the highest positivity rate observed in head and neck cancer and the highest H-score in colorectal cancer.

Source: Fulian Technology Official Website

Currently, the top three targets (PSMA, FAP, and HER2) in China’s investigational radiopharmaceutical pipeline account for a significant proportion, with indications mostly limited to prostate cancer and neuroendocrine tumors. Fulian’s FL-091 clearly possesses differentiated advantages. According to data presented by Fulian, FL-091 demonstrated significantly enhanced NTSR1 binding affinity and higher antagonistic activity compared to another NTSR1-targeted radioligand, 3BP-227 from 3B Pharmaceuticals. Therefore, it is understandable that SK Biopharmaceuticals, which aims to vigorously develop RPT, quickly took interest in this preclinical candidate.

The global expansion of ADCs in recent years has ushered in a new chapter for Chinese biotech companies. With Fuzlian’s license-out deal, the internationalization of RDCs is also becoming highly anticipated. However, the stories of RDCs and ADCs may be entirely different.

Radiopharmaceuticals: Why Go to South Korea?

SK Biopharmaceuticals’ strategic focus on RPT is well-founded. In fact, South Korea’s nuclear medicine sector has a long history; from the late 1990s to the early 2000s, the Korean government began investing in nuclear medicine infrastructure and talent development. The inclusion of PET/CT cancer diagnostics under the National Health Insurance scheme in 2005 further spurred market growth. According to data from the International Atomic Energy Agency (IAEA), South Korea had approximately 4.8 PET/CT scanners per million people in 2019. By comparison, China is projected to reach only about 2.43 units per million people by 2030.

Since the 2010s, South Korea has begun independently developing novel radiopharmaceuticals and exporting them, along with related technologies, to overseas markets, including Japan, the United States, Russia, and China. In 2018, DuChemBio, South Korea’s largest radiopharmaceutical company, signed an agreement with Dongcheng Pharmaceutical, granting the latter the rights to develop, register, manufacture, and market the licensed product “[18F]FP-CIT Injection” in China.

However, while South Korea has a long history in radiopharmaceutical development, it has long focused on diagnostic radiopharmaceuticals. Only in recent years has the country significantly increased investment in therapeutic radiopharmaceuticals and provided policy support: In 2019, the Ministry of Food and Drug Safety (MFDS) introduced an expedited approval pathway for innovative therapeutic radiopharmaceuticals, reducing the review timeline from the standard 12 months to as little as 6 months for those designated as breakthrough therapies. Meanwhile, South Korea has strengthened collaboration with agencies such as the U.S. FDA and the European EMA, recognizing the review outcomes of other major regulatory authorities under specific circumstances.

In 2020, the South Korean Ministry of Food and Drug Safety (MFDS) approved Lutathera, the first therapeutic radiopharmaceutical, which became covered by national health insurance in March 2022 for third-line treatment of adult patients with unresectable, well-differentiated, somatostatin receptor-positive advanced and/or metastatic gastroenteropancreatic neuroendocrine tumors (GI-NETs). In May 2024, the South Korean MFDS approved Pluvicto for marketing.

To some extent, the development of radiopharmaceuticals in China mirrors the situation in South Korea: there are few domestic radiopharmaceutical projects that have entered clinical trials, and these are predominantly for diagnostic purposes using molecular functional imaging, with relatively few therapeutic radiopharmaceutical projects. However, a major difference is that two key radiopharmaceuticals, Lutathera and Pluvicto, have yet to enter the Chinese market.

Another major limiting factor in China is the production of medical isotopes. As the most critical raw material for radiopharmaceuticals, these isotopes are primarily obtained through a series of radiochemical separation processes following irradiation in nuclear reactors or accelerators. In China, with the exception of small quantities of I-131 and Lu-177, the majority of medical isotopes produced via reactor irradiation rely on imports.

By comparison, the medical isotopes that South Korea can primarily produce include Tc-99m, F-18, I-131, and Lu-177. The Korea Atomic Energy Research Institute (KAERI) has also developed a Mo-99 production technology that does not rely on highly enriched uranium. This self-sufficient production capability provides significant support for the development of South Korea’s nuclear medicine industry and enhances its competitiveness in the international nuclear medicine market. Furthermore, South Korea has established cooperation agreements with countries such as the United States and Canada regarding isotope supply.

TerraPower, a U.S.-based nuclear innovation company and a key investor in SK Biopharmaceuticals, possesses the technology to produce the medical isotope Actinium-225 (Ac-225). Ac-225 is one of the most promising radionuclide precursors. With a half-life of 10 days—longer than that of Lutetium-177 (Lu-177)—and emitting alpha particles with lower penetration but higher cytotoxicity, Ac-225 offers the potential for therapies with superior efficacy and safety profiles, provided that ligand targeting is optimized. Currently, demand for Ac-225 far exceeds supply.

Therefore, South Korea’s conditions for developing radiopharmaceuticals can be described as more mature. Furthermore, the maturity and standardization of South Korea’s healthcare system are comparable to those of developed markets. In terms of regulatory classification, procedures, and requirement standards, South Korea’s medical regulatory framework is most closely aligned with those of Japan and the United States. Clinical trials conducted in South Korea also enjoy a high degree of international recognition, facilitating product entry into the broader and more financially robust European and American markets.

RDC: Is Going Global the Only Option?

Current market optimism regarding therapeutic radiopharmaceuticals and the future prospects of RDCs is primarily driven by the strong sales performance of Novartis’s two radiopharmaceuticals, Lutathera and Pluvicto. In the first half of 2024, these two agents continued to deliver incremental growth for Novartis: Pluvicto’s sales rose 45% year-over-year to $655 million, while Lutathera’s sales increased 16% year-over-year to $344 million.

However, the impressive performance of radiopharmaceuticals such as Pluvicto requires dedicated transportation and distribution networks. With a shelf life of approximately five days, any uncertainties during production and transportation pose a risk of supply disruption.

According to data from the official website of Cardinal Health, a leading representative of nuclear pharmacies in the United States, it operates more than 130 nuclear pharmacies and over 30 cyclotrons, with supply chain capabilities that enable delivery within three hours to over 95% of healthcare institutions nationwide.

Domestic nuclear pharmacies remain scarce, primarily comprising 17 facilities operated by China Isotope & Radiation Corporation, 14 by Dongcheng Pharmaceutical, and 7 by Xinke Medicine. The construction of nuclear pharmacies requires substantial capital investment, with a typical development cycle of approximately three years. The initial investment for a single facility exceeds RMB 40 million, and annual revenue of around RMB 10 million is required to reach the break-even point.

In 2022, Zhihe Biology established a Class B nuclear pharmacy in Suzhou. Obtaining the Class B qualification took a year and a half due to stringent requirements, including the need for a standalone building, prohibition of proximity to water sources, absence of residential areas nearby, and compliance with specific design and approval standards. Currently, the Class B nuclear pharmacy meets the company’s needs for R&D and partial production. However, once therapeutic drugs are approved for market launch, large-scale commercial production will require a Class A nuclear pharmacy, which entails even higher standards. It is understood that currently, only Sichuan and Zhejiang provinces in China have radioactive drug production facilities capable of meeting Class A requirements.

Given the high barriers to entry and substantial costs involved, RDCs are inevitably priced at a premium. Taking Pluvicto as an example, each dose is priced between $42,000 and $50,000, with a standard course of treatment consisting of six doses. Although Pluvicto is covered by Medicare and many commercial insurance plans in the United States, specific conditions and copayments may apply. For instance, under Medicare Part B, patients typically bear a 20% copayment for Pluvicto. Given the drug’s pricing, this copayment still represents a significant financial burden.

Currently, the approved indication for Pluvicto is metastatic castration-resistant prostate cancer (mCRPC) that is PSMA-positive and has progressed after treatment with androgen receptor pathway inhibitors and taxane-based chemotherapy. Treatment options for mCRPC have long been limited. In the prior Phase 3 VISION clinical trial, the median overall survival for mCRPC patients receiving Pluvicto plus standard of care was 15.3 months, compared with 11.3 months in the control group, representing a 4-month extension in median overall survival. In other words, while Pluvicto addresses certain urgent unmet clinical needs, its clinical benefit remains relatively modest.

“From the current perspective, the efficacy of RDC is not curative. In China, the upper limit of price acceptance for this type of drug is around RMB 100,000. Coupled with the limited number of hospital beds available for radionuclide therapy in the country, the market ceiling for therapeutic RDCs in China remains relatively low,” said an investor.

Globally, over 100 novel radiopharmaceutical drugs (RDCs) for diagnosis and therapy are currently in clinical trials or under regulatory review for market approval. Notably, companies such as Novartis have strategically targeted GPCR, FAP, and PSMA, as well as integrins αvβ3/β5, with indications covering breast cancer, glioblastoma multiforme, and prostate cancer, among others.

In China, diagnostic RDC pipelines still account for the majority, with only a few companies developing theranostic RDCs. It is generally believed that the market potential of RDCs lies in therapeutic radiopharmaceuticals.

In the highly sought-after global ADC sector, Chinese companies hold distinct advantages in the ADC development process. The three components of an ADC—the antibody, payload, and linker—require iterative experimentation and balancing for different tumors and tissue combinations. Chinese enterprises can fully leverage their accumulated experience and engineer dividend. What multinational corporations (MNCs) seek in terms of technology platforms, clinical data, and patience in manufacturing is precisely what Chinese companies possess and excel at.

In the field of RDC, China’s innovations remain in their early stages, whether in terms of overall infrastructure and upstream development for radiopharmaceuticals or in breakthroughs and explorations in drug development.

Therefore, it is difficult to draw a direct analogy between the global expansion of RDCs and that of ADCs. On one hand, an analysis of targets sought by multinational corporations (MNCs) reveals that therapeutic RDCs are the primary subjects of transactions; the domestic pipeline supply of RDC drugs in China is not as abundant as that of ADCs, so a surge in outbound business development (BD) deals is unlikely to occur in the short term. On the other hand, the clinical application space for therapeutic RDC drugs within China is currently limited. Unlike ADCs, the commercialization prospects for RDCs developed by Chinese biotech companies depend on overseas markets, making global expansion an inevitable path.

However, with the widespread adoption of diagnostic equipment, advancements in the production and technological capabilities of radionuclide raw materials, the issuance of technical guidelines for R&D, and regulatory policy drivers—coupled with the entry of domestic giants such as Hengrui Medicine, Novartis’s construction of a radiopharmaceutical production base in China signaling the gradual introduction of its original RDCs into the Chinese market, and the rise of emerging biotech companies like Fuliang—the Chinese radiopharmaceutical market is entering a new phase. It is at that point that the Chinese narrative of RDCs may truly begin to unfold.

References:

Three Key Considerations for Entering the Blue Ocean of Radiopharmaceuticals: Strategy, Prospects, and Barriers! - PharmaCircle

The Birth of a Blockbuster Radiopharmaceutical: Insights from the Rise of Pluvicto - Amino Observation