Garbage Time or Whaling Era: Who Is Fueling Anxiety in the Healthcare Industry?

Recently, the entire healthcare industry and capital markets have been dominated by two buzzwords: “garbage time” and “the era of whale hunting.”

“Garbage time” is easy to understand; it originates from sports competitions, referring to the remaining game time when the gap between the two sides is too large to be closed. The concept of the “Whaling Era,” however, dates back to the mid-19th century, when people had to venture deeper into the Arctic Ocean in pursuit of greater returns, specifically to hunt sperm whales, which commanded higher market value.

Although the two have different definitions, when linked to the healthcare industry and capital markets, their underlying logic is consistent, namely marketThe market landscape remained unchanged for a long time, and the pendulum of the era slowed down the production of various get-rich-quick myths. In such a somewhat “boring” era, practitioners either chose to lie flat, watch from the sidelines, and wait for time to pass, or continued to compete within the existing stock market to preserve their last shred of dignity.

So, is that really the case?

In fact,Whether it is “garbage time” or the “whaling era,” what lies behind these terms is, in essence, the “anxiety” felt by practitioners regarding the current state and future development of the industry.

A top-tier investor has just confirmed this point, remarking, “Whether it’s called ‘history’s trash time’ or ‘the end of the whale-hunting era,’ it is essentially no different from the ‘winter’ that people often mention. It is merely expressed in a more sophisticated manner, but the essence remains unchanged: both refer to an industry downturn or development bottlenecks. Therefore, the widespread adoption of this concept largely stems from shared sentiment; when the overall market is underperforming, everyone experiences varying degrees of anxiety.”

At the investor level, fundraising is currently difficult, and exiting is even more challenging.Take fundraising as an example. Over the past year and a half, there has been a steady stream of news about the establishment of government-guided funds with scales of tens or even hundreds of billions of yuan across various regions. As a result, state-owned capital has become the dominant force in the entire capital market. Nearly every hotly contested medical project’s financing round features the presence of state-owned institutions. However, looking beyond the surface to the essence, this trend also indirectly indicates that market-oriented funds are dwindling, and the capital market is in urgent need of fresh sources of liquidity.

Moreover, for investors, securing funding from state-owned capital does not necessarily mean they can breathe a sigh of relief, as meeting the required performance targets is no easy feat. Generally, state-owned investors are tasked with the mission of promoting the development of the local healthcare industry. This imperative is particularly pronounced in new first-tier or second- and third-tier cities, resulting in relatively less flexibility for investors. Compounded by the dwindling number of high-quality projects and the overall sluggish performance of the secondary market, it is indeed challenging for investors to successfully fulfill their local reinvestment obligations.

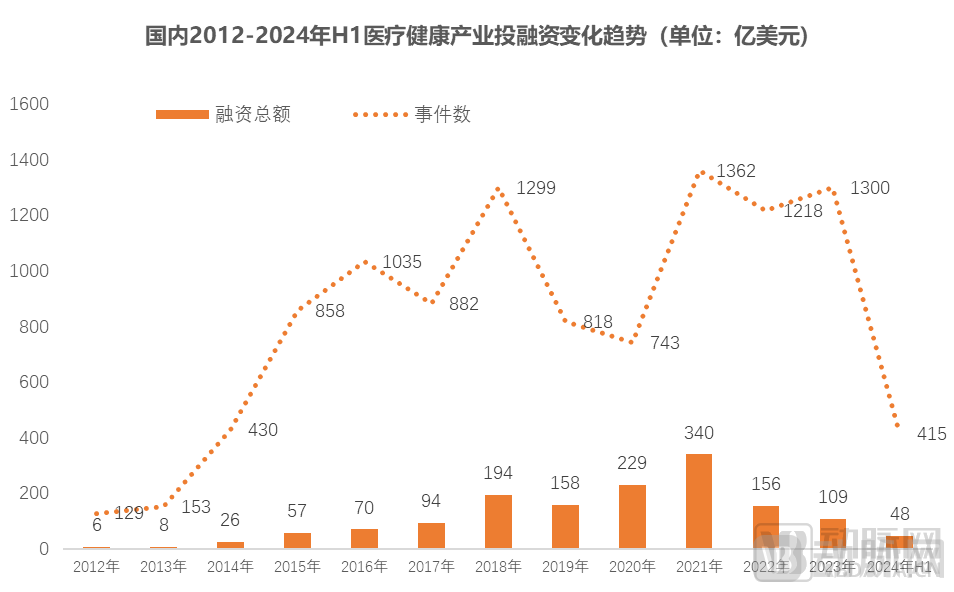

Figure 1. Trends in Investment and Financing in China’s Healthcare Industry, 2012–H1 2024 (Data Source: VCBeat)

Certainly, investors have it tough, and healthcare companies are also facing difficult times, if not even harder. First of all, for early-stage companies, fundraising has become increasingly challenging. According to incomplete statistics from the VBInsight database,In H1 2024, China’s healthcare sector completed 415 financing deals, a year-on-year decline of over 30%., the lowest in nearly a decade, meaning that many healthcare companies are unable to secure funding. Even those that have obtained financing are faring little better; due to a significant decline in overall fundraising amounts, many enterprises have had to rely on self-funding and implement across-the-board salary cuts just to barely sustain normal operations and development.

Figure 2. Twelve Healthcare Companies That Successfully Went Public in 2024 (Source: Public Information)

Compared to early-stage enterprises, mid- to late-stage healthcare companies are currently facing greater pressure. On one hand, the “investment drought for mid- to late-stage ventures” is rapidly spreading across the healthcare industry; it is reported thatIn H1 2024, there were only 70 financing rounds beyond Series C in China’s healthcare sector, with a large number of healthcare companies stuck at Series B.On the other hand, there are obstacles to going public. According to incomplete statistics,In the first half of this year, nearly 80 medical companies have failed in their IPO attempts.,Currently, only 12 companies have successfully gone public.This represents a significant departure from the boom of companies queuing for IPOs in 2021.

Of course, this is not without reason. In both the primary and secondary markets, the essential nature of the current downturn is a significant increase in barriers to entry, primarily referring toMedical enterprises must currently possess core competencies that enable stable profitability.

In this regard, a senior investor remarked, “Judging from the recent setbacks experienced by healthcare companies, commercialization capability has clearly become a key focus for regulators. The secondary market currently imposes explicit requirements on profitability and the scale of net profit. The primary market has also been affected; over the past one to two years, investors have significantly downplayed their singular pursuit of innovative technologies, instead placing greater emphasis on companies’ cash flow generation, commercialization capabilities, and timelines to profitability.”

From a market perspective, many healthcare companies are currently struggling to meet these requirements. Take the highly watched biotech sector as an example: either the market has already been dominated by multinational pharmaceutical companies, leaving little room for new players to capture a share; or the companies simply lack profitability, with their core products still in the pipeline and commercialization remaining a distant prospect. Nevertheless, the current surge in business development (BD) deals can still provide some biotech firms with much-needed cash flow, while companies in other niche segments have no choice but to persevere through the challenges.

Thus, it is not difficult to see that the survival space for the entire healthcare industry is indeed narrowing, and the anxiety among practitioners is very real. This explains their strong resonance with concepts such as “garbage time” and the “whale-hunting era.”

While the market winter is indeed a fact, many people do not agree with the notion that the healthcare industry has entered its “historical garbage time.”

In response, a partner at a certain firm remarked, “The market is indeed cyclical; after experiencing the frenzied growth of the past few years, we have truly reached a turning point,”The industry theme has also gradually shifted from past expansion-driven growth to value-driven growth.. As the market’s incremental growth shifts from quantity-driven expansion, certain enterprises or institutions will inevitably be eliminated, while others will succeed by capitalizing on the trend. Thus, this actually marks the beginning of a new strategic game; it does not mean that current efforts are futile, nor should stakeholders simply “lie flat” and wait for time to pass.”

So, how should this be understood? How exactly can one transition from expansion-driven growth to value-driven growth?

The first point is, of course, to reduce desires.Take the highly anticipated topic of public listings as an example: currently, neither healthcare companies nor investment institutions are passively waiting for IPOs; instead, they are increasingly adopting a flexible strategy of “exiting wherever feasible.”

In response, a seasoned investor stated, “From the perspective of maximizing benefits, going public is undoubtedly the ultimate goal. However, if this path proves unfeasible, persisting stubbornly will only lead to deeper predicaments.”YesFor the vast majority of healthcare companies today, maintaining a position that allows for either an IPO or, alternatively, business development (BD) partnerships or acquisition, is actually the optimal strategy.“This not only allows medical enterprises that are stuck at the listing stage to find a new path, but also enables acquiring companies to gain new leverage, further enhancing their market competitiveness.”

Data further corroborates this trend. According to a recent report from IT Juzi, mergers and acquisitions (M&A) in the healthcare sector accounted for 26.77% of the total transaction value in the first half of 2024, ranking first among all industries. Specifically, in the biotechnology and pharmaceutical sectors, there were 18 M&A deals in H1 2024, with an estimated total transaction value nearing RMB 24 billion, marking a historical high. Beyond making concessions on initial public offerings (IPOs), healthcare professionals’ willingness to settle for less is also reflected in financing amounts, pipeline portfolios, and market revenues.

Second, prioritize survival over growth.In light of this, a head of an institution remarked, “When market conditions are favorable, every sector presents opportunities. Therefore, the sole strategy for investors is to cast a wide net to identify the three to five biggest winners within each sector, as 80% to even 100% of total market returns derive from them. However, when the industry enters a downturn, fewer new winners emerge, and the market becomes a zero-sum game focused on existing stock. In such circumstances, continuing to ‘cast a wide net’ entails significantly greater risk.”

Consequently, “going global” has emerged as a keyword in the healthcare industry. Its essence is less about technological innovation and more about resource allocation, which is intrinsically linked to corporate survival. As the domestic market becomes increasingly saturated and hyper-competitive, targeting overseas markets with greater growth potential can undoubtedly provide new incremental opportunities for enterprises and institutions. However, international expansion requires caution; without sound planning and corresponding core competencies, companies risk becoming trapped due to excessive costs and resource drain.

The third point is to earn money with high certainty.Currently, the entire healthcare industry has generally low tolerance for error. This is partly because people have limited disposable income, and partly because the overall barriers to entry in the industry are rising, requiring significantly greater effort than before to achieve returns.

In this regard, a frontline investor remarked, “If we were to return to the bonus period when healthcare companies could complete two or even three rounds of financing in a single year, you could certainly spin compelling narratives, given the industry’s vast potential for imagination. However, as time progresses, the market will gradually validate many of these possibilities. At this stage, the core challenge for healthcare professionals is to make strategic choices and identify greater certainty within the industry.”

In fact, this has become a consensus. Taking healthcare companies as an example, many have temporarily shelved parts of their pipelines or paused exploration of new businesses in the past year or two, instead channeling more resources and capital into the commercial monetization of their core operations. Investment institutions are no exception. On one hand, their investment strategies have gradually shifted from prioritizing teams and technologies to focusing on commercialization capabilities and profitability levels. On the other hand, this trend is reflected in exit strategies: institutions are currently strengthening their post-investment management capabilities to empower their portfolio companies.

Figure 4. R&D Investment of China’s Top 10 Pharmaceutical Companies in 2023 (Source: Annual Reports)

The final point is to be bold yet meticulous, always striving for original innovation.Despite the current capital winter and the varying degrees of survival pressure faced by healthcare companies, the exploration of innovation has not ceased. Data from the 2023 annual reports and the Q1 2024 quarterly reports indicate a significant overall increase in R&D investment among China’s top 10 pharmaceutical companies. Notably, BeiGene has cumulatively invested nearly RMB 50 billion in R&D over the past five years.

Furthermore, in the primary market, although the overall financing volume has decreased significantly, the proportion of financing for innovative medical projects has increased notably, with a primary focus on frontier fields such as precision instruments, antibody-drug conjugates (ADCs), radiopharmaceuticals, medical robots, and cell and gene therapy.

In fact, a focus on innovation can be viewed as healthcare professionals’ pursuit of sustained, long-term stable returns, given that only “genuine innovation” is likely to stand out in the current landscape. Specifically, innovation has first received strong policy support; second, numerous research institutions and platforms have begun to participate, significantly enhancing overall innovative capacity; and finally, in terms of market competition, with the surge in overseas expansion and business development (BD) transactions, China’s innovative medical products have reached a stage where they must compete head-on with top-tier global products.

In this regard, the founder of a pharmaceutical company remarked, “The era of undifferentiated ‘me-too’ drugs is quietly passing. The main theme of the future pharmaceutical industry will gradually shift toward ‘best-in-class,’ and even ‘first-in-class.’ This implies higher investment and greater risk, making it all the more essential for healthcare professionals to remain rational and allocate capital and efforts to R&D pipelines with greater certainty.”

Therefore, from a holistic perspective, the healthcare industry is currently prioritizing the realization of value over short-lived "get-rich-quick" growth narratives. In other words, healthcare professionals are becoming more pragmatic and grounded.

If we must invoke the concept of “garbage time,” when did the healthcare industry’s previous “garbage time” occur? Through interviews, many industry professionals generally agree that it was around 2015.

That year, the pharmaceutical sector experienced a massive valuation bubble, leading to the withdrawal of numerous clinical trial applications, while the CSI Pharmaceutical Index plummeted by nearly 44% over seven months. It was not until three years later, in 2018, when centralized volume-based procurement for generic drugs was launched, that China’s innovative drug industry finally saw its first wave of explosive growth.

So, what exactly happened in between?

On July 22, 2015, the China Food and Drug Administration (CFDA) issued the “Announcement on Launching Self-Inspection and Verification of Clinical Trial Data for Drugs,” which was hailed as imposing “the strictest data verification requirements in history.”From this moment on, Chinese pharmaceutical companies are officially transitioning from an era of generic drugs characterized by inconsistent quality and high profit margins to a new era of innovative drugs that offer superior quality and high cost-effectiveness.

Consequently, a cohort of young professionals with global perspectives and deep expertise in the intricacies of new drug development emerged on the historical stage, founding pharmaceutical companies such as CStone Pharmaceuticals, InnoCare Pharma, Antengene Corporation, Harbour BioMed, and WuXi Juno Therapeutics, all of which were established during this period. Furthermore, industrial parks represented by BioBAY began to strengthen their focus on innovative drugs by introducing specialized capital.

Thus, it is not difficult to see that the core of “garbage time” still lies in the shift of industry standards—this was true in 2015, and it remains so today. Therefore, to navigate this period smoothly or achieve further development, healthcare professionals need to remain rational, closely observe the genuine changes within the industry, and align themselves as closely as possible with new industry objectives by leveraging their own strengths. This has always been the “law of survival” in the healthcare sector.

References:

1. “The End of the Whaling Era and the Dawn of a New One” — LatePost;

2. “M&A Transactions by Chinese Enterprises in H1 2024: Total Deal Value Approaches RMB 200 Billion, Up 22% Quarter-on-Quarter” — IT Juzi;

3. “There Is No Garbage Time in Biomedicine” – VCBeat;

4. “Memories of the Year of the Ox: No Tears for China’s Innovative Drugs” — Fengshuo Venture Capital