WuXi AppTec's Earnings Dip Sparks CXO Rally, But Industry Recovery Remains Premature

WuXi AppTec

New Drug R&D and Production Service Provider

Over the past two years, the CXO sector has declined, with the stock prices of China’s top 10 companies in this field dropping by as much as 70%. At a time when market confidence is at its most fragile, WuXi AppTec, the leading domestic CXO company, released an “unexpected” semi-annual report on the evening of July 29. Although the financial data in this report may not be as impressive as in previous periods, it is particularly valuable under the current circumstances.

WuXi AppTec's Stock Price Trend Over the Past Two Days, Source: Baidu Stock Connect

On July 30, WuXi AppTec drove the entire CXO sector to open higher and continue its upward trajectory, with its shares rising more than 6% intraday to hit a one-month high. On one hand, the impact of the U.S. Biosecure Act persists, and WuXi AppTec’s interim results showed declines in both revenue and net profit. On the other hand, the secondary market’s response was unusually positive. What underlying messages are hidden in this divergence?

From Bearish to Bullish: Secondary Market Investors’ Shift in Sentiment Toward WuXi AppTec Stemmed Solely from Its Interim Report.

On July 29, WuXi AppTec released its highly anticipated 2024 interim report. In the first half of 2024, the company’s revenue reached RMB 17.24 billion, representing a year-on-year decline of approximately 8.6%. Net profit amounted to RMB 4.24 billion, down by 20%, while adjusted non-IFRS net profit attributable to shareholders of the parent company stood at RMB 4.37 billion, a decrease of 8%.

From the perspective of order changes, as of the end of June 2024, WuXi AppTec’s backlog was valued at approximately RMB 43.1 billion, representing a year-on-year increase of 33% after excluding specific commercial manufacturing projects. Among these, revenue derived from the top 20 global pharmaceutical companies amounted to approximately RMB 6.59 billion, accounting for about 25% of total revenue, with a year-on-year growth of 11.9% after excluding specific commercial manufacturing projects.

In other words, although order volume continues to grow, the incremental orders from large pharmaceutical companies are significantly lower than those from biotech firms.

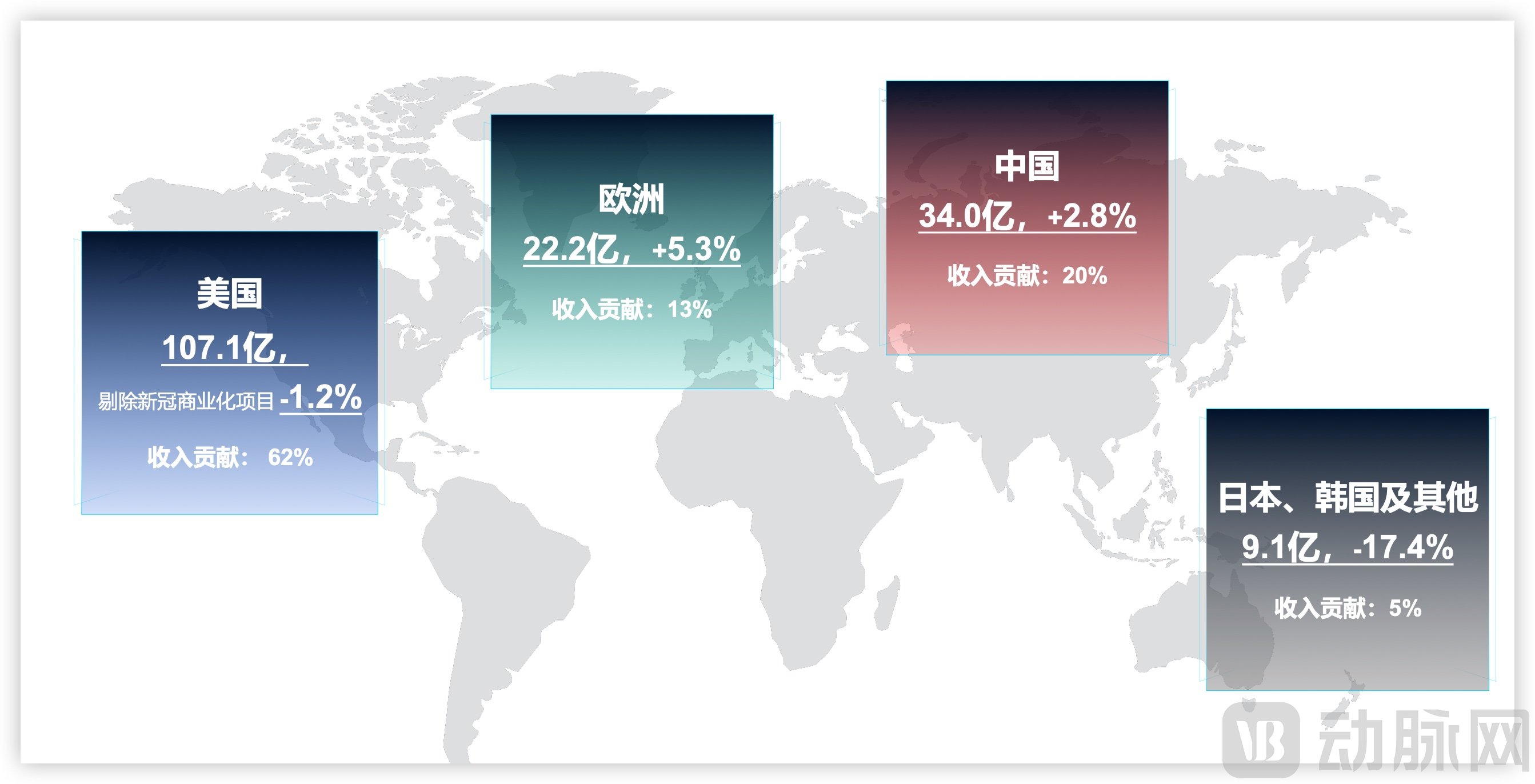

Although the sanctions turmoil over the past six months has shaken the industry, WuXi AppTec’s orders continue to grow. Revenue from China and Europe reached RMB 3.4 billion and RMB 2.22 billion, respectively, representing slight year-on-year increases of 2.8% and 5.3%. Customers in the United States remained the largest contributor to revenue, generating RMB 10.71 billion; after excluding specific commercialization projects, this figure declined slightly by 1.2% year on year, essentially remaining flat.

Revenue Performance by Region in H1 2024 (Source: Company Official Website)

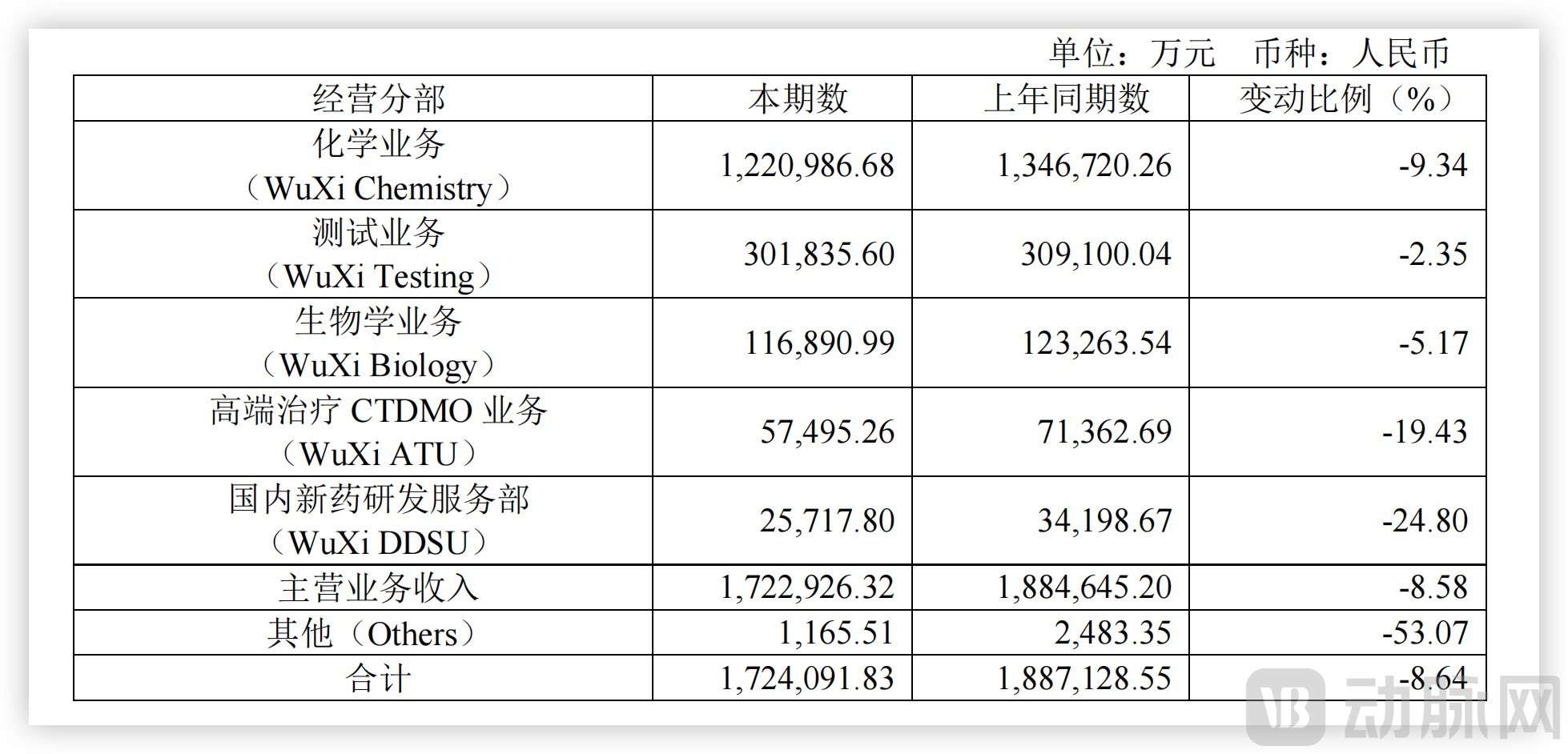

From a business line perspective, of the RMB 17.24 billion in revenue generated in the first half of the year, the Chemistry Business contributed RMB 12.21 billion, representing a year-on-year decline of 9.34%. However, excluding specific commercial manufacturing projects, revenue grew by 2.1% year-on-year. Specifically, revenue from small molecule process development and production services amounted to RMB 7.39 billion. Excluding specific commercial manufacturing projects, this segment saw a year-on-year decrease of 2.7%, following a growth of over 50% in the same period last year; nevertheless, full-year positive growth is still expected. Revenue from the Oligonucleotide and Peptide Business reached RMB 2.08 billion, marking a year-on-year increase of 57.2%.

Operating Performance of Each Business Segment, Source: Corporate Financial Reports

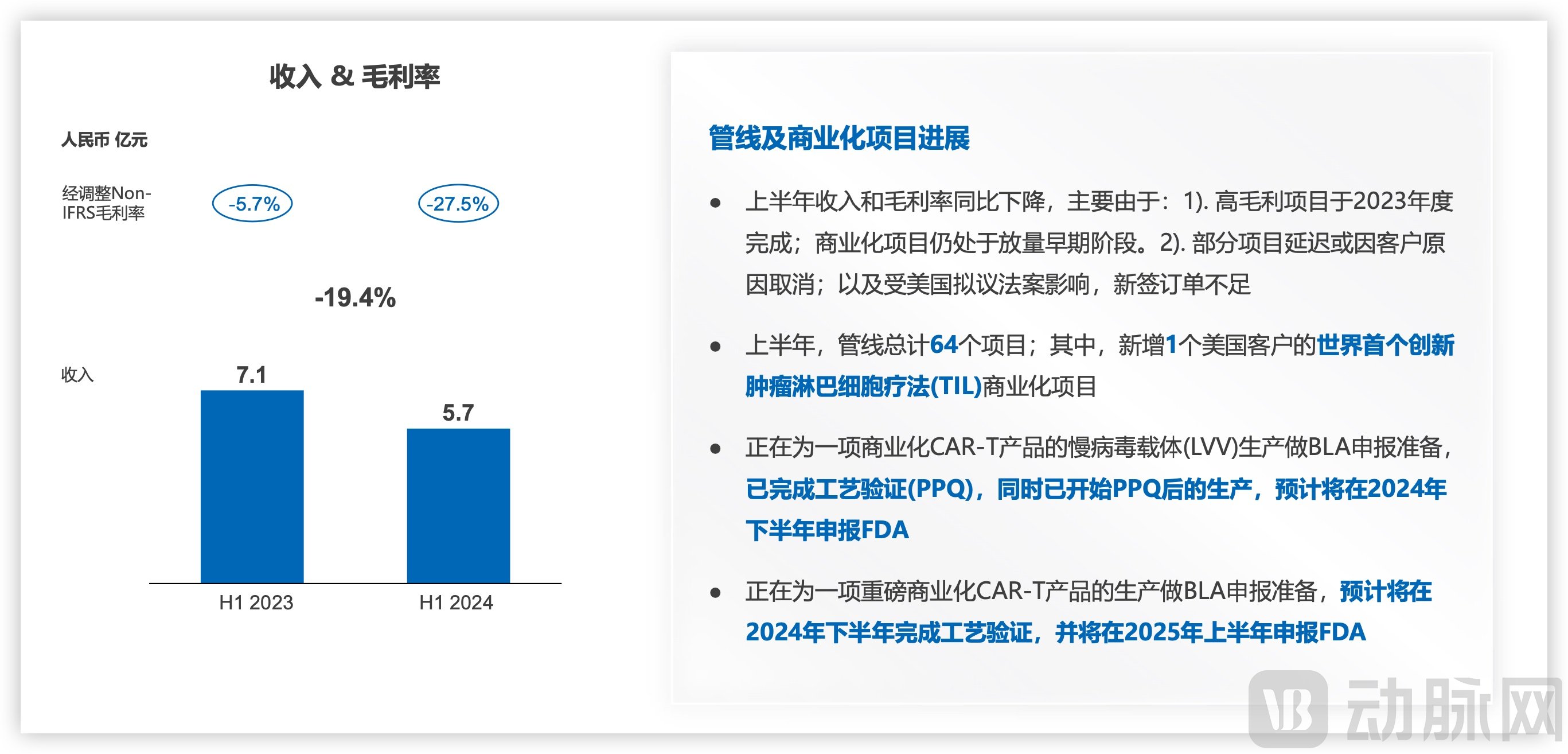

Furthermore, revenue from the high-end therapy CTDMO business amounted to RMB 575 million, a year-on-year decline of 19.43%, falling short of expectations. The financial report attributed this underperformance to the early stage of commercialized projects and the impact of proposed U.S. legislation. Revenue from the domestic new drug research and development services (DDSU) segment totaled RMB 257 million, representing a 24.8% year-on-year decrease. This further underscores that China’s innovative drug sector remains in a downturn.

In terms of gross profit margin, WuXi AppTec has basically maintained a level of 40%, representing a slight decline compared to the past. The consolidated statement of cash flows for the first half of 2024 shows that the company paid RMB 5.8 billion to employees, with net cash flow from operating activities amounting to RMB 5.0 billion, essentially flat year-on-year.

As of the end of June 2024, WuXi AppTec added more than 500 new customers, building on its existing base of over 6,000 active clients. Meanwhile, the interim report provided a full-year 2024 performance guidance of RMB 38.3 billion to RMB 40.5 billion, projecting positive growth (estimated at 2.7%–8.6%) after excluding specific commercial manufacturing projects.

Since January this year, the entire CXO industry, particularly WuXi AppTec, has been frequently disrupted by the progress of proposed U.S. legislation, raising market concerns that companies with a significant proportion of overseas revenue would suffer substantial operational impacts. According to the data disclosed in this semi-annual report, WuXi AppTec, as a leading CXO company, maintained stable operations during the first half of the year despite external environmental challenges.

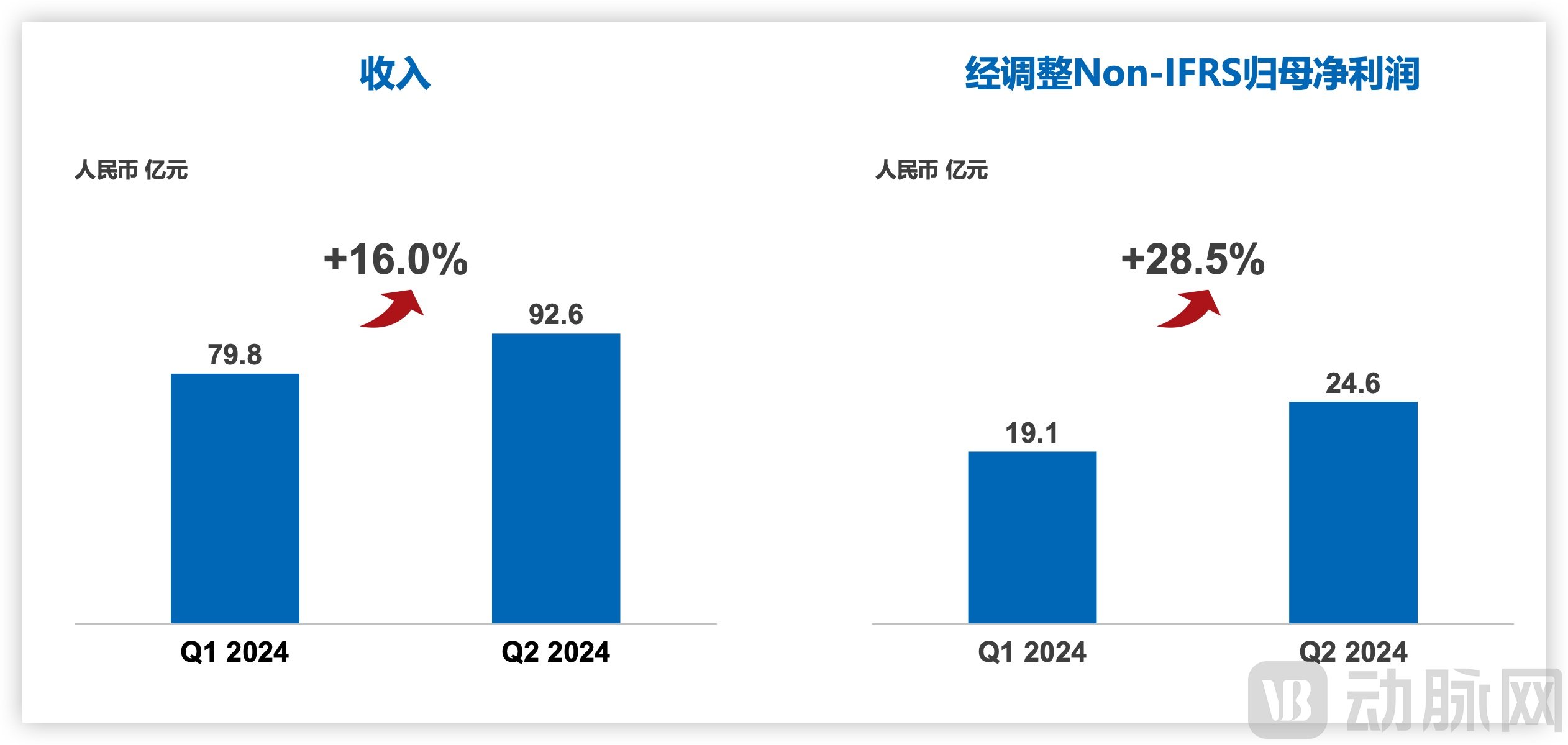

First, the month-on-month growth shows positive signals.

Although year-on-year performance was somewhat weaker, the data for 1H 2024 was lower than that for 2Q 2024, indicating that WuXi AppTec’s performance improved quarter-on-quarter, which is no small feat.

By quarter, revenue in Q1 2024 was RMB 7.982 billion, with adjusted Non-IFRS net profit attributable to shareholders of RMB 1.91 billion. In Q2 2024, revenue reached RMB 9.26 billion, a quarter-on-quarter increase of 16.0%, while adjusted net profit attributable to shareholders amounted to RMB 2.46 billion, representing a quarter-on-quarter growth of 28.5%.

Revenue Performance in the First Two Quarters of 2024, Source: Company Official Website

Although it cannot compare with the 50% growth rate in Q2 2023, double-digit growth is considered an excellent performance in the current environment. For CXO companies, year-on-year comparisons are important, but quarter-on-quarter comparisons are even more critical as they reflect continuous operational performance. It is precisely this high growth in Q2 that provides the confidence to support its revenue target of RMB 38.3 billion to RMB 40.5 billion.

Second, uncertainty in the U.S. market persists, making global expansion to diversify risk an inevitable choice.

Q2 was the primary period of contention surrounding the Biosecure Act, during which WuXi AppTec continued its efforts. According to data from a report by the Korea Biomedical Review, WuXi AppTec’s lobbying expenditures increased from $100,000 in Q4 2023 to $360,000 in Q2 2024.

Regardless of its effectiveness, lobbying is an imperative undertaking, given that revenue from U.S. clients accounts for 62.7% of total income. As the world’s most critical market, the United States commands top priority among major pharmaceutical companies. The top 20 global pharmaceutical firms contribute approximately 25% of WuXi AppTec’s revenue and have maintained double-digit growth. Currently, the stability of their “sentiment” can serve as a barometer for the legislative turmoil, directly and swiftly impacting the stability of WuXi AppTec’s performance.

In response to the turmoil that has occurred this year, WuXi AppTec devoted considerable space to providing an explanation. In summary, there are two main points: first, the Biosecure Act is still far from becoming law and currently carries significant uncertainty; second, WuXi AppTec has never transferred intellectual property or customer information to third parties.

Nevertheless, the WuXi group is also adjusting its global footprint by striving to expand markets outside the United States. For instance, this May, WuXi AppTec cut some jobs at its facility in St. Paul, Minnesota, while WuXi Biologics suspended construction of its production base in Massachusetts.

In the first half of this year, revenue from Europe reached RMB 2.22 billion, a year-on-year increase of 5.3%. Over the past year, WuXi AppTec’s revenue from European clients grew by more than 10% year on year, while WuXi Biologics’ revenue from the European market surged by over 100% year on year. The incremental growth from the European market will serve as a significant driver of WuXi’s future performance.

Third, the success or failure of emerging businesses is the lifeline for the future.

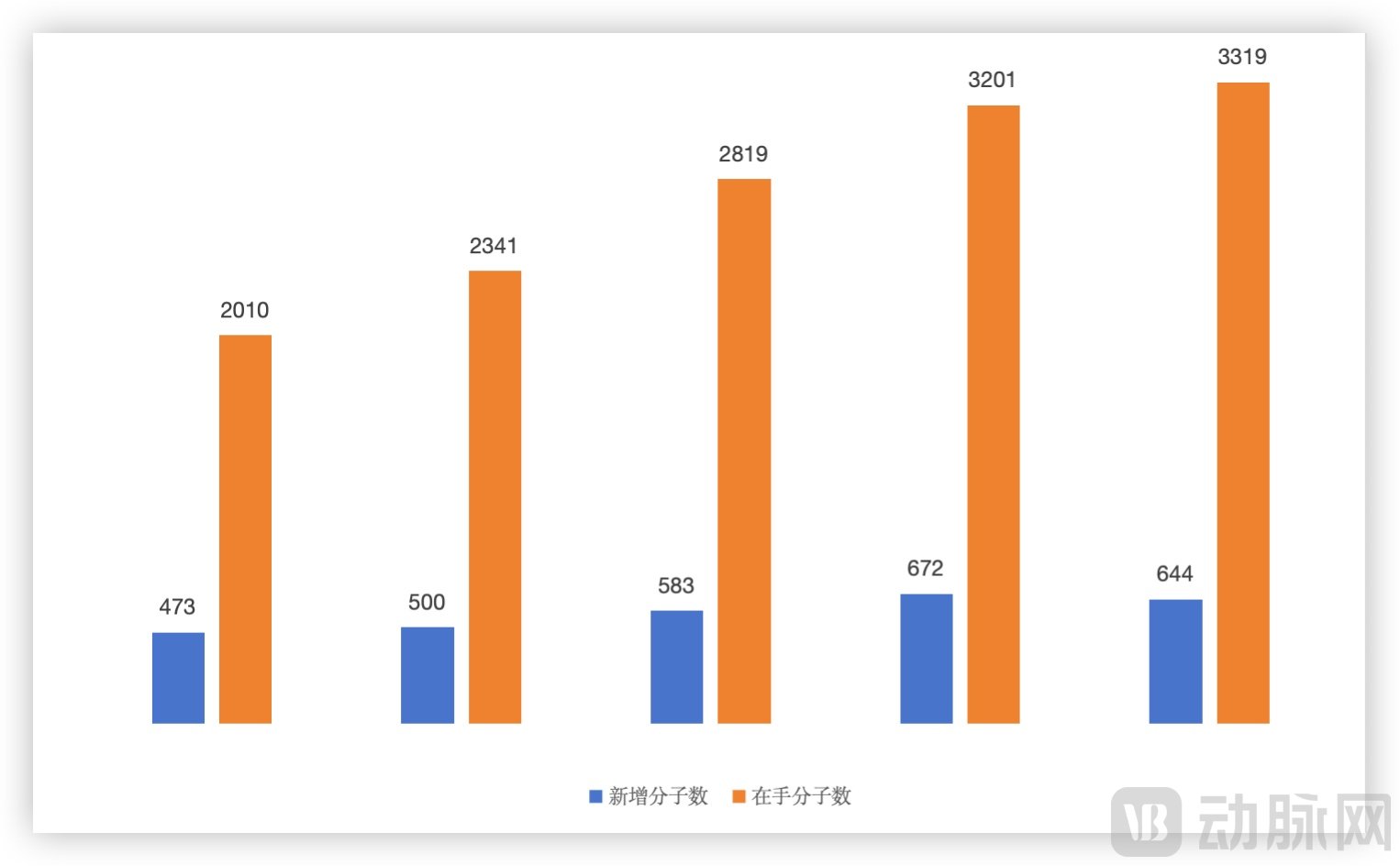

Currently, small-molecule CDMO projects account for half of WuXi AppTec’s revenue. In the first half of 2024, the company added 644 new molecules, reaching a recent high; however, the number of completed projects was also substantial, resulting in only a marginal net increase in the backlog of molecules. While WuXi AppTec’s orders were previously perceived as having long execution cycles, with an ever-growing backlog that secured future business, this dynamic has changed significantly in 2024.

Small-Molecule CDMO Business Performance in Recent Years, Data Sourced from Corporate Financial Reports

In Q1 2024, WuXi AppTec added 337 new molecules, with the cumulative total increasing by 85. In Q2, it added 307 new molecules, while the cumulative total rose by only 33. This indicates that WuXi AppTec is aggressively securing small and medium-sized projects to safeguard its performance. Although maintaining order volume can stabilize current operations, it is crucial for future growth to identify new business lines that can serve as new revenue drivers.

In the first half of this year, WuXi AppTec’s TIDES business (primarily oligonucleotides and peptides) generated revenue of RMB 2.08 billion, representing a year-on-year increase of 57.2%. As of the end of June 2024, the backlog of orders for the TIDES business rose by 147% year on year. The number of clients served by TIDES’ research and development and manufacturing services reached 151, a 25% year-on-year increase, while the number of molecules served totaled 288, up 39% year on year.

In January this year, the total volume of peptide solid-phase synthesis reactors increased to 32,000 L. With the continued strong global demand for GLP-1 drugs and the expiration of the domestic patent for semaglutide in 2026, the industry’s demand for raw peptide production will remain robust, allowing WuXi AppTec to benefit from this favorable trend for some time.

ATU’s Business Expansion Falls Short of Expectations, Image Source: Company Official Website

However, the expansion of other emerging businesses has not been as smooth. The interim report shows that the high-end therapy CTDMO business, such as CGT, generated only RMB 570 million in revenue, falling short of expectations.

This is a dangerous signal. Recall that during the turmoil at the beginning of the year, the CEO of Ginkgo, a company dedicated to cell programming technology, stated that emerging drugs and therapies such as CGT represent the future industries that the United States should focus on, while legacy sectors like traditional chemical pharmaceuticals are obsolete and do not warrant particular attention.

It is certain that the crackdown on China’s CXO industry will not abate, particularly as the struggle for dominance in emerging business segments remains intense. Chinese CXO companies, represented by WuXi AppTec, must make full preparations for fierce competition.

The prosperity of a single company is hard to sustain, while the collective well-being of the industry endures. Throughout 2023, more than 20 of the 28 CXO companies listed on China’s A-share market experienced share price declines, with an average drop exceeding 30%. If only one company reports decent financial performance, it clearly does not reflect the overall condition of the industry.

Pharmaron Releases H1 2024 Earnings Forecast: Revenue Expected at RMB 5.471–5.640 Billion, Down ~0%–3% YoY; Net Profit Attributable to Shareholders Projected at RMB 1.055–1.143 Billion, Up 34%–45% YoYPharmaron announced its interim performance forecast for the first half of 2024, projecting operating revenue of RMB 5.471 billion to RMB 5.640 billion, representing a year-on-year decrease of approximately 0% to 3%. The net profit attributable to shareholders of the listed company is expected to range from RMB 1.055 billion to RMB 1.143 billion, marking a year-on-year increase of 34% to 45%. Pharmaron explicitly stated that global customer inquiries and visits have rebounded compared to the same period in 2023, with the value of newly signed orders increasing by more than 15% year on year.

Notably, Pharmaron’s revenue decreased by 1.95% year-over-year in Q1 2024, but rebounded in Q2 2024 with both quarter-over-quarter growth from Q1 and a slight year-over-year increase compared to Q2 2023. By segment, laboratory services revenue reached a record high in Q2 2024, driven by new orders; CMC (small-molecule CDMO) service revenue also increased quarter-over-quarter from Q1, with more projects expected to be delivered and revenue recognized in the second half of 2024.

Asymchem’s earnings forecast indicates that its operating revenue for the first half of the year reached RMB 2.660–2.740 billion, a year-on-year decrease of 40.72%–42.45%; net profit was RMB 480–550 million, down 67.39%–71.54% year on year; and net profit excluding non-recurring items is estimated at RMB 430–480 million, representing a year-on-year decline of 69.38%–72.57%.

Joinn Laboratories Issues 2024 Half-Year Performance Forecast: Revenue Ranges from RMB 720 Million to RMB 973 Million, Down Approximately 3.8%–28.9% Year-on-Year; Net Loss of RMB 136 Million to RMB 184 Million; Non-GAAP Net Loss in the Range of RMB 163 Million to RMB 221 Million

As can be seen, although WuXi AppTec released a fairly acceptable financial report, the revenues of domestic CXO companies as a whole showed a downward trend (for those that did not announce their H1 2024 performance, Q1 2024 figures were used). On the other hand, the net profits after deducting non-recurring gains and losses for various enterprises were also unsatisfactory. Apart from a slight decline at WuXi AppTec, many other companies experienced significant drops.

The CXO sector is inherently cyclical. From 2020 to 2022, the industry experienced explosive performance growth driven by large pandemic-related orders. Subsequently, from 2023 to 2024, a significant decline in such major orders led to sluggish performance growth. This year, controversy surrounding proposed legislation has further amplified industry risks. The 2024 performance results also indicate that the period of high-speed growth for China’s CXO industry has ended, and further differentiation will become the new norm.

The underlying development logic of the CXO industry remains unchanged, but the competitive landscape has shifted.

The Rise of CXOs: An Inevitable Trend in the Biopharmaceutical IndustryUnder the cost pressure where developing a single innovative drug often requires $1 billion and ten years, contract research, development, and manufacturing organizations (CXOs) that help pharmaceutical companies reduce costs, improve efficiency, and accelerate timelines have entered a period of rapid growth. Today, to cope with the Inflation Reduction Act (IRA), nearly all large pharmaceutical companies are making concerted efforts to control costs, exercising extreme caution in all expenditures, from pipeline optimization to supplier selection.

Under such circumstances, CXO companies are facing immense pressure for survival. Since 2023, well-known companies including New Vision, Lonza, and Thermo Fisher Scientific have undergone varying degrees of contraction and adjustment, such as layoffs and plant closures. For instance, Evonik, the German chemical and pharmaceutical CXO giant, continued to experience year-on-year declines in revenue and profit in Q1 of this year following a significant drop in 2023, and it will continue to lay off employees to cope with cost pressures.

For Chinese CXO companies, having gone through the previous growth cycle, they have made significant progress in cost control, engineer dividend, industrial chain support, organizational structure, and fulfillment capabilities, fully reflecting the advantages of domestic manufacturing. External suppression does not align with the objective laws of industrial development, and a hard decoupling is unlikely to occur in the near term. Moreover, it is difficult for major pharmaceutical companies to find partners as stable and reliable as Chinese CXOs.

But this does not mean they are not preparing a Plan B. In fact, multinational pharmaceutical companies have already taken action in the past two years.

For instance, Novo Nordisk acquired Catalent, the leading CGT CDMO company, for $16.5 billion, while other multinational CXO firms have entered a fierce competition for orders.

Global CDMO giant Lonza announced its first-half financial results, with sales of CHF 3.1 billion, in line with its 2024 sales expectations. Meanwhile, Samsung Biologics, benefiting from the strong performance of its subsidiary Samsung Bioepis, saw its quarterly revenue surpass the KRW 1 trillion mark for the first time, reaching KRW 1.16 trillion (approximately USD 839 million), representing a year-on-year increase of 34% and a quarter-on-quarter growth of 22%.

Notably, Samsung Biologics has established partnerships with 16 of the top 20 global pharmaceutical companies, including a $1 billion production deal with a U.S. pharmaceutical company that extends through 2030. Meanwhile, its ADC manufacturing facilities are expected to be completed by the end of this year.

It is foreseeable that the era when multinational pharmaceutical companies blindly entrusted orders to Chinese CXOs, adhering to the principle of “not putting all eggs in one basket,” has come to an end. Currently, the business volume of domestic pharmaceutical companies is insufficient to absorb the production capacity of CXOs. Proactively expanding into overseas markets, building a diversified layout, and deeply binding with customers have become the choice for many enterprises.

In May this year, Asymchem acquired a Pfizer facility in the UK, completing the layout of its first R&D and production base in Europe. Building on this foundation, Asymchem will continue to plan for emerging fields such as peptides, nucleic acids, and enzyme technologies, while continuously expanding and strengthening its R&D capabilities and production base construction in Europe. In the first half of 2024 (2024H1), Asymchem’s newly signed orders increased by 20% year-on-year, with a significant quarter-on-quarter growth in Q2 compared to Q1, mainly driven by new orders from customers in the European and American markets.

In addition to the European market, domestic CXO companies are also expanding into the Asian market through acquisitions or self-built facilities.

In January this year, Clinipace acquired CSI, a regional CRO headquartered in Singapore; in March, WuXi Biologics announced the groundbreaking of its integrated CRDMO center in Singapore; and in July, Tigermed announced the completion of its acquisition of the Japanese CRO company Medical Edge.

It is an indisputable fact that the global biopharmaceutical industry is in a downturn, and for CXO companies, the era of rapid growth is already in the past. Looking back, the CXO sector evolved from chemical synthesis outsourcing to generic drugs, biologics CDMO, small-molecule CDMO, and now ADCs. WuXi AppTec has steadily enhanced its resilience and vitality, managing to stabilize its performance in the face of suppression—a feat that is no easy task. For other CXO companies, learning to be resilient is key to waiting out the current slump until the next wave of opportunity arises.