State Ownership as the Endgame for Traditional Chinese Medicine Enterprises: The Case of Tian士li's Acquisition by China Resources Sanjiu

CR SANJIU

Pharmaceutical R&D, Production, Sales, and Related Health Service Provider

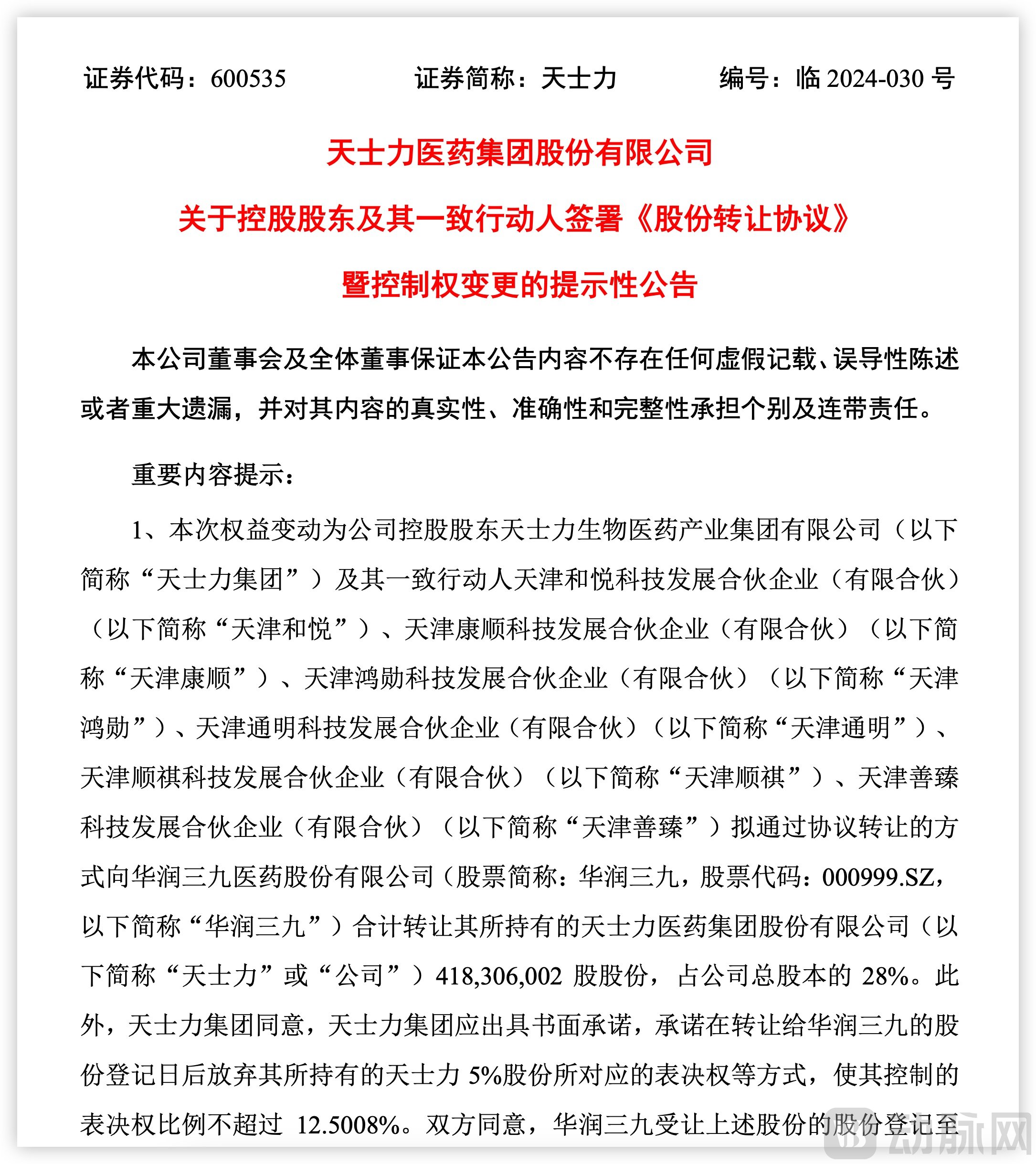

On the evening of August 4, Tasly Pharmaceutical Group Co., Ltd. (hereinafter referred to as “Tasly Pharmaceutical”) issued a major announcement, stating that its controlling shareholder, Tasly Biopharmaceutical Industry Group Co., Ltd. (hereinafter referred to as “Tasly Group”), and its parties acting in concert intend to transfer a total of 28% of their shares in Tasly Pharmaceutical to CR SANJIU Pharmaceutical Co., Ltd. (hereinafter referred to as “CR SANJIU”) through agreed transfers.

Announcement: Tasly Group and its parties acting in concert intend to transfer 418,306,002 shares of Tasly Pharmaceutical to CR SANJIU at a price of RMB 14.85 per share, with the total transaction consideration amounting to approximately RMB 6.212 billion. Upon completion of the transaction, CR SANJIU will become the controlling shareholder of Tasly Pharmaceutical, while China Resources Limited will become the new actual controller.

Tasly Pharmaceutical Releases Announcement on Equity Transfer, Source: Company Announcement

As one of the leading companies in the traditional Chinese medicine sector of China’s A-share market, Tasly Pharmaceutical’s main products include Compound Danshen Dripping Pills and Yangxue Qingnao Granules, covering multiple therapeutic areas such as cardiovascular, cerebrovascular, and nervous systems. On August 5, following the announcement, Tasly resumed trading, hitting the daily upper limit at the open and closing up 5.68%, with a market capitalization of RMB 22.23 billion. CR SANJIU rose as much as 3.73% during intraday trading before closing up 0.71%.

This change has not only drawn widespread market attention, but the replacement of the controlling shareholder also signals that Tasly Pharmaceutical’s future development strategy may undergo new adjustments, bringing both new opportunities and challenges to the company.

As the pace of state-owned capital investment accelerates, traditional Chinese medicine enterprises are reinvigorated.

Since the official launch of the three-year action plan for state-owned enterprise (SOE) reform in September 2020, central state-owned capital and local state-owned assets have gradually taken control of traditional private enterprises in the traditional Chinese medicine (TCM) industry. For instance, Kunming Pharmaceutical Group and Taiji Group have successively completed changes in their actual controllers, becoming enterprises directly under the supervision of the State-owned Assets Supervision and Administration Commission (SASAC), while Guangyuyuan and Conba have transitioned from private to state-owned ownership.

The injection of state-owned capital not only helps traditional Chinese medicine (TCM) enterprises secure policy and financial support, but also drives more significant progress in areas such as innovation-driven development and the optimization of corporate governance structures. Therefore, it is widely believed within the industry that the new round of state-owned enterprise reforms may usher in a new development cycle for the TCM sector.

Taking Kunming Pharmaceutical Group as an example, after the founding of the People's Republic of China, Yunnan Military Region Pharmaceutical Factory, the first state-owned pharmaceutical enterprise in Yunnan Province, was established. It was later transferred to local administration and renamed Kunming Pharmaceutical Factory, which is the predecessor of Kunming Pharmaceutical Group, primarily engaged in the development, production, and sales of natural plant-based medicines.

In 1995, Kunming Pharmaceutical Factory, together with several other enterprises in Kunming, jointly initiated the establishment of Kunming Pharmaceutical Co., Ltd., which was listed on the Shanghai Stock Exchange in December 2000 and renamed Kunming Pharmaceutical Group Co., Ltd. in 2015. During this period, Zhejiang Holley Group, optimistic about the development of the artemisinin industry and Kunming Pharmaceutical’s expertise in artemisinin research and development, officially became the controlling shareholder of Kunming Pharmaceutical through equity transfer in 2004.

In 2022, CR SANJIU acquired a 28% stake in Kunming Pharmaceutical Group held by Holley Group for RMB 2.9 billion, making Kunming Pharmaceutical Group a listed subsidiary under CR SANJIU.

According to public information, only Kunming Pharmaceutical Group and China Resources Shenghuo currently hold production approvals for Xuesaitong Soft Capsules in China, and both companies regard Xuesaitong Soft Capsules as their core products. In June this year, Kunming Pharmaceutical Group and its controlling shareholder, CR SANJIU, simultaneously issued announcements stating that Kunming Pharmaceutical Group intends to sign an equity transfer agreement with CR SANJIU to acquire a 51% stake in China Resources Shenghuo held by CR SANJIU for RMB 1.791 billion, using its own or self-raised funds.

Upon the successful completion of the acquisition, CR SANJIU not only resolved the issue of horizontal competition between its two subsidiaries but also facilitated Kunming Pharmaceutical Group’s consolidation of the market for Xuesaitong Soft Capsules. The main active ingredient of this drug is Panax Notoginseng Saponins (PNS) extracted from Panax notoginseng. This resource integration further validates the strategic direction outlined in CR SANJIU’s initial acquisition proposal for Kunming Pharmaceutical Group, which aims to establish the latter as a leading enterprise in the Panax notoginseng industry chain and to conduct in-depth research and development centered on its core botanical resources, such as Panax notoginseng and Artemisia annua.

The logic behind CR SANJIU’s acquisition of Tasly Pharmaceutical is identical to its previous moves.

In 2023, Tasly Pharmaceutical’s R&D investment reached RMB 1.315 billion, a year-on-year increase of 29.49%, placing it among the top tier of central state-owned enterprises. The company currently has 36 drug candidates in clinical trials, with 26 of them in Phase II or Phase III. The acquisition by CR SANJIU will provide significant financial support, alleviate Tasly’s funding pressures in R&D, and help accelerate the progress of its existing projects.

As a leader in the traditional Chinese medicine (TCM) industry chain, CR SANJIU has established a presence in TCM medicinal materials, TCM formula granules, premium proprietary Chinese medicines, and the Panax notoginseng industry chain. This acquisition will help consolidate its industry-leading position and enhance core competitiveness. By fully integrating resources from both parties, it aims to strengthen, supplement, and extend the TCM industry chain, leverage R&D synergies, and boost innovation capabilities.

From a manufacturing perspective, CR SANJIU has fully demonstrated its profound expertise in automation, informatization, and digitalization through the intelligent transformation of its Guanlan base and its collaboration with Heihu Technology. Meanwhile, Tasly Pharmaceutical holds an industry-leading position in traditional Chinese medicine (TCM) dripping pill technology. The project “Creation and Application of an Intelligent Manufacturing Technology System for TCM Centered on Quality Digitalization,” led by Tasly, was awarded the Special Prize for Scientific and Technological Progress in Tianjin. Through resource integration, the two parties are poised to generate further synergies in the field of intelligent TCM manufacturing.

In recent years, traditional Chinese medicine (TCM) enterprises have leveraged state-owned capital to enter platforms directly under the supervision of the State-owned Assets Supervision and Administration Commission (SASAC). TCM companies previously held by private entities, such as Guangyuyuan and Conba, have accepted direct management by local governments following equity investments by state-owned capital. Meanwhile, Foci Pharmaceutical has achieved a transition from municipal-level to provincial-level state ownership, further enhancing its capacity for resource integration.

State-owned assets have become major players in the traditional Chinese medicine industry.

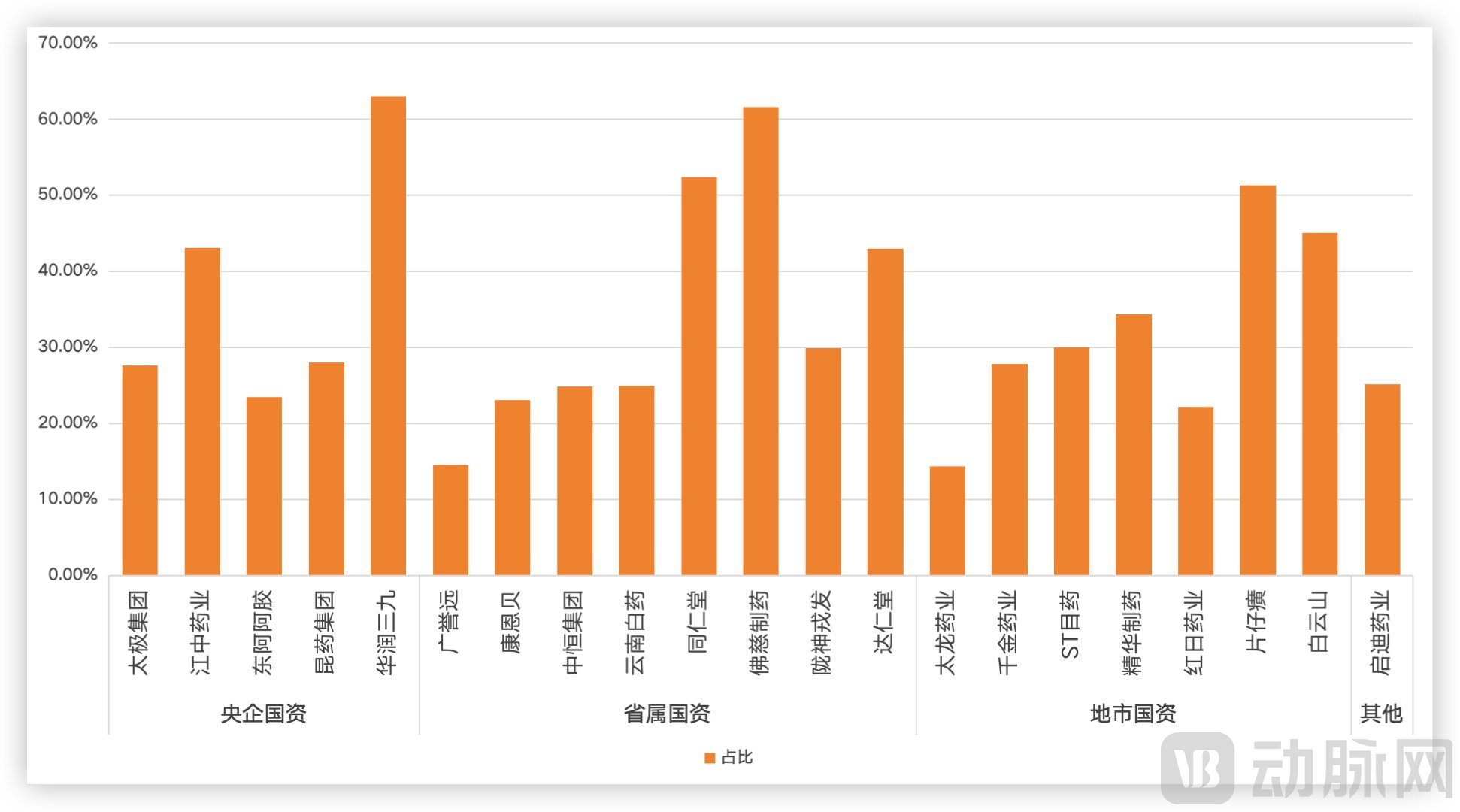

From the perspective of state-owned holding proportions in Shenwan Level 1 industries, the pharmaceutical and biological industry accounts for only 16.02%, ranking fifth from the bottom among the 31 Shenwan Level 1 industries, and is significantly lower than the average level of 27.59% across all A-share industries. In terms of the pharmaceutical industry and its Level 2 sub-industries, there are a total of 79 state-owned holding companies in the pharmaceutical industry, with the traditional Chinese medicine industry accounting for 28.77%, second only to pharmaceutical commerce, ranking second among the pharmaceutical Level 2 sub-industries.

In terms of the nature of state-owned controlling shareholders, central state-owned enterprises, provincial state-owned enterprises, municipal state-owned enterprises, and other state-controlled companies account for 22.78%, 35.44%, 39.24%, and 2.53% of the pharmaceutical industry, respectively; while in the traditional Chinese medicine (TCM) industry, these figures are 23.81%, 38.10%, 33.33%, and 4.76%, respectively. This indicates that the proportion of state-owned holdings in the TCM industry is higher than the industry average, and its overall influence is correspondingly greater.

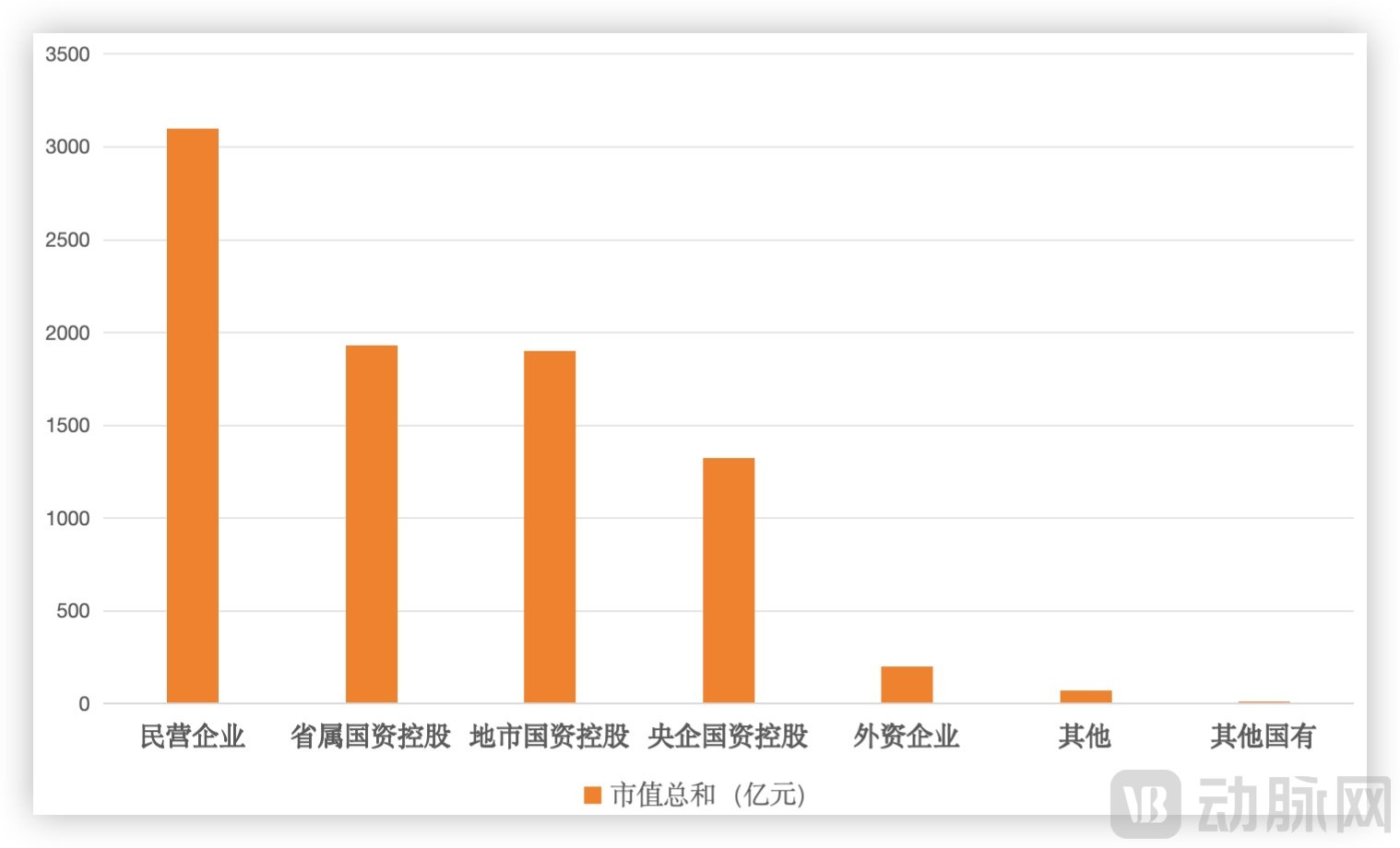

According to Choice data, based on the Shenwan Traditional Chinese Medicine (TCM) industry classification, there are currently 72 listed TCM enterprises in China. As of the end of July 2024, 21 of these companies were controlled by state-owned enterprises (SOEs), accounting for 29.17% of the total; their combined market capitalization exceeded RMB 520 billion, representing approximately 61% of the sector’s total market value. The breakdown is as follows: eight companies controlled by provincial-level state assets, with a total market capitalization of RMB 192.846 billion; seven companies controlled by prefecture- and city-level state assets, with a total market capitalization of RMB 189.887 billion; five companies controlled by central state-owned enterprises, with a total market capitalization of RMB 132.562 billion; and one other state-owned enterprise, with a market capitalization of RMB 1.2 billion.

Total Market Capitalization of Traditional Chinese Medicine Companies by Ownership Type, Data Source: Choice

Among state-controlled listed traditional Chinese medicine (TCM) companies, these enterprises are predominantly concentrated in the branded TCM and over-the-counter (OTC) segments, possessing distinct competitive advantages such as core flagship products and established distribution channels. To date, seven of the top ten TCM companies by market capitalization in China have state-owned backgrounds, while the top six—Pien Tze Huang, Yunnan Baiyao, CR SANJIU, Tong Ren Tang, Guangzhou Baiyunshan Pharmaceutical Holdings, and Dong-E-E-Jiao—are all controlled by state-owned entities.

State-owned Holding Status in the A-share Traditional Chinese Medicine Industry, Data Sourced from Choice

In 2024, influenced by industry development and the broader market environment, the pharmaceutical sector exhibited an overall weak performance. As of the first half of the year, the sector declined by approximately 18.5%, underperforming the CSI 300 Index by about 21 percentage points. All six secondary sub-sectors within the pharmaceutical industry recorded declines. Among them, the Traditional Chinese Medicine (TCM) segment experienced the smallest decline, underperforming the CSI 300 Index by 12.51 percentage points but outperforming the broader Pharmaceutical and Biological Products sector by 8.15 percentage points.

From the results, it is evident that the entry of state-owned capital has become a significant driving force for the transformation of traditional Chinese medicine enterprises, bringing them greater endogenous momentum and vitality, and promoting their transition toward high-quality development.

First, the high prosperity of the traditional Chinese medicine industry is an important factor attracting state-owned capital.

From a performance perspective, the traditional Chinese medicine (TCM) sector achieved revenue of RMB 372.1 billion in 2023, a year-on-year increase of 6.4%; net profit attributable to shareholders of the parent company reached RMB 33.6 billion, up 38.6% year on year; net profit attributable to shareholders of the parent company after deducting non-recurring gains and losses amounted to RMB 29.1 billion, representing a 27.4% year-on-year growth; and the sector’s net profit margin for the full year increased by 2.1 percentage points year on year. In Q1 2024, the TCM sector recorded revenue of RMB 101.2 billion, a slight year-on-year decline of 0.7%. Although short-term performance fluctuated due to the high base effect from Q1 2023, profitability and dividend payouts remained robust.

Amidst their strong performance, traditional Chinese medicine enterprises also face underlying concerns.

For traditional Chinese medicine (TCM) enterprises, identifying new growth curves beyond their core products is no easy task. Whether through developing new products or making external investments, they often fall into a trap where increased investment fails to drive corresponding revenue growth, ultimately resulting in an overly concentrated business structure. Take Conba as an example: its former core product, Salvia Miltiorrhiza and Ligustrazine Hydrochloride Injection, was included in the key monitoring drug list and affected by adjustments to the National Reimbursement Drug List, leading to a decline in revenue. Unable to identify new business growth drivers, the company ultimately resorted to introducing state-owned capital as a lifeline.

Following the entry of state-owned capital, Conba began to adjust its business structure and optimize its assets, successively divesting low-efficiency and non-performing assets to focus on its core business. In 2023, Conba achieved operating revenue of RMB 6.733 billion, a year-on-year increase of 12.2%; the net profit attributable to shareholders of the listed company was RMB 592 million, a year-on-year increase of 65.19%.

Overall, the entry of state-owned capital into traditional Chinese medicine (TCM) enterprises brings not only financial and policy support but also improved management mechanisms. Through various state-owned enterprise reform measures—including equity structure adjustment, enhancement of performance assessment and incentive mechanisms, optimization of corporate governance, asset integration, optimization of asset structure, and divestiture of non-core businesses to focus on core operations—TCM enterprises with state-owned backgrounds are poised to achieve performance improvements through a combination of external expansion and organic growth, thereby promoting high-quality development in the TCM industry by enhancing quality and efficiency.

Secondly, the stable operational characteristics and proactive dividend policies of traditional Chinese medicine (TCM) enterprises are highly favored by state-owned capital.

Compared with chemical drugs or biologics, many traditional Chinese medicine (TCM) companies generate dual revenue streams from both pharmaceuticals and consumer goods. A typical example is Yunnan Baiyao, where the revenues from its pharmaceutical and toothpaste segments are nearly identical, each exceeding RMB 6 billion. Coupled with businesses such as herbal material sales and pharmaceutical distribution, the company’s total revenue in 2023 reached RMB 39.111 billion, representing a year-on-year increase of 7.19%; net profit amounted to RMB 4.094 billion, a year-on-year increase of 36.41%.

Meanwhile, Yunnan Baiyao ranked second among A-share healthcare companies in dividend payouts, with a distribution of RMB 3.706 billion, trailing only Mindray Medical. Notably, since its listing in 1993, Yunnan Baiyao has paid dividends every year, with cumulative cash dividends exceeding RMB 24 billion by 2023.

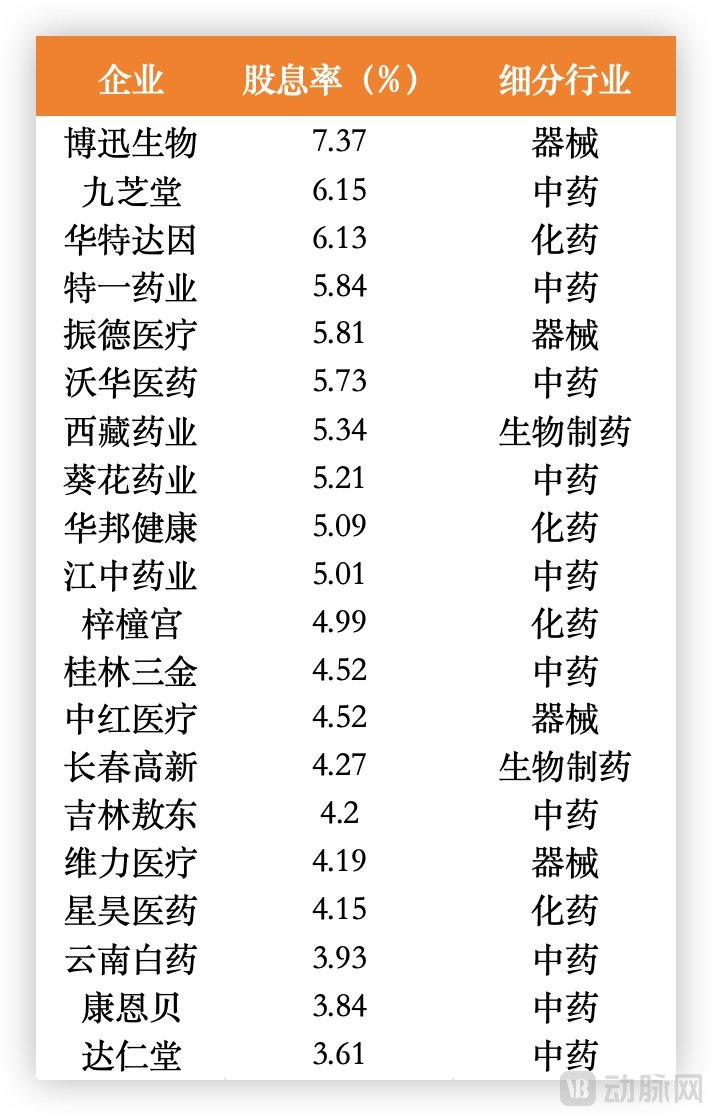

Top 20 A-Share Healthcare Companies by Dividend Yield in 2023, Data Source: Choice

From a sector-specific perspective, the traditional Chinese medicine (TCM) industry is also the most generous in terms of dividend payouts. Using the dividend yield—the ratio of dividends per share to stock price—as the benchmark, and taking bank wealth management products with an expected annualized return of 3.5% as a reference, only about 20 healthcare companies can outperform this threshold. Among these, 10 are TCM companies, accounting for half of the total.

Most of these traditional Chinese medicine (TCM) enterprises have their own core products, such as Liuwei Dihuang Wan, Jianwei Xiaoshi Tablets, and Baiyao. On the one hand, most of these drugs are over-the-counter (OTC) medications that can be purchased directly without a doctor’s prescription; their primary sales channels include retail pharmacies, private clinics, and online e-commerce platforms.

On the other hand, these blockbuster traditional Chinese medicine (TCM) products typically feature high entry barriers, such as national protected variety status, confidential formulas, time-honored brand recognition, and patents. Coupled with their strong brand influence, they face limited competition throughout their long product life cycles, resulting in low operational volatility.

Low R&D expenses, high revenue, and generous dividends align with the current preferences of the capital market.

Finally, the traditional Chinese medicine industry is undergoing a development cycle, with substantial internal demand for consolidation.

In recent years, the Chinese government has intensively rolled out a series of policies targeting the traditional Chinese medicine (TCM) industry and its upstream and downstream supply chains. These initiatives have granted TCM enterprises greater market opportunities and room for development, making M&A transactions centered on resource integration the new normal in industry growth. For instance, Beilu Pharmaceutical, an A-share listed company, announced its plan to invest RMB 202 million to acquire an 80% equity stake in Tianyuan Pharmaceutical. Xincheng Capital announced the completion of its acquisition of Guilong Pharmaceutical, a TCM company specializing in throat health. In addition to listed companies, some local state-owned assets entities have also begun to frequently engage in M&A and consolidation of unlisted TCM enterprises. For example, in the second half of 2023, Zhiguang Chenji, a century-old time-honored TCM brand, underwent a change in equity structure, with its actual controller becoming the State-owned Assets Supervision and Administration Commission of Shanxi Province.

In the current macroeconomic environment, state-owned capital is becoming a critical variable driving transformation in traditional Chinese medicine (TCM) enterprises. The relationship between TCM companies and state-owned investors is one of mutual attraction, with each party fulfilling the other’s strategic needs. In the near future, such industry consolidation is likely to become the norm.