Policy-Driven Industrial Transformation: Deconstructing Supply-Side Reforms in China's Healthcare and Medical Insurance System

On August 10, 2024, the 17th Health Industry Ecosystem Conference—2024 Xipu Conference grandly opened in Boao, Hainan, under the theme “Moving Forward Under Pressure: Breaking and Establishing the Path from Stock to Incremental Growth.”

That morning, Li Junguo, Vice President of Zhongkang Technology, delivered a presentation titled “Industry Transformation Driven by Policy,” providing a comprehensive, big-picture analysis of the changes brought about by the ongoing healthcare reforms in the health industry.

Li Junguo, Vice President of Zhongkang Technology, Delivers Keynote Address at the Conference

From the 14th Five-Year Plan’s new developmental positioning of the biopharmaceutical industry as a “strategic emerging industry,” to the 20th National Congress’s renewed emphasis on advancing the Healthy China initiative, and further to the Third Plenary Session of the 20th Central Committee’s clear guidance for the healthy and orderly development of the biopharmaceutical sector, a series of high-quality national policies have outlined a clear trajectory for the healthcare industry’s blueprint, driving continuous industrial progress.

Li Junguo pointed out that as China’s development enters a new stage, public demand for health has reached a historical peak; however, the growth of the medical and healthcare industry remains sluggish. The underlying reason lies in the supply-side issues within the medical and healthcare sector.

Addressing the mismatch between healthcare supply and public health needs is fundamental to building a Healthy China. The continuous evolution of healthcare reform policies is driving the industry’s transition from “quantity” to “quality.”

However, on the basis of effectively meeting demand, controlling the rapid growth of total social health expenditures is actually a global challenge in healthcare reform, and the difficulty of reducing costs and improving efficiency in the pharmaceutical and health industry is higher than that in other industries. In developed countries such as the United States and Japan, the focus of healthcare reform lies in expanding access to medical services, controlling healthcare costs, and improving medical efficiency. China’s healthcare policies center on ensuring basic coverage, strengthening primary care, and establishing robust mechanisms; nevertheless, it still faces challenges such as uneven distribution of medical resources, difficulties and high costs in accessing medical care, insufficient coverage by commercial health insurance, and inconsistent quality of medical services.

Li Junguo stated that China’s “three-medical linkage” reform has been advancing for several years. Although the pace of reform across different sectors remains uneven, its impact on the pharmaceutical and health industries is already clearly reflected in the performance of various market participants.

Meanwhile, emphasizing the public’s sense of gain and well-being has emerged as a new highlight in China’s healthcare reform efforts in recent years, encompassing measures such as expanded health insurance coverage, improved accessibility to medical care, and people-benefiting policies. If health insurance funds can provide sustained and robust support, this direction will be further strengthened.

The current achievements of healthcare reform primarily lie in the initial establishment of a tiered diagnosis and treatment system. This system serves as the key mechanism for coordinating top-down and bottom-up efforts in healthcare reform. Meanwhile, through the decentralization of medical resources, preliminary two-way referrals and sharing of medical resources have been realized between primary care institutions and large hospitals within medical consortia, gradually forming a closed loop for prescription circulation.

According to relevant data, by 2021, the rate of medical visits within county-level administrative regions in China reached 94%, representing a 9.8 percentage point increase from 2015. A total of 85.8% of county-level hospitals possessed service capabilities equivalent to secondary hospitals, while 35.1% had capabilities equivalent to tertiary hospitals. Nationwide, 1,666 urban medical groups, 4,028 county-level medical consortia, and 5,900 cross-regional specialty alliances were established. The number of two-way patient referrals across China increased from 10.58 million in 2015 to 25.075 million in 2020, with an average annual growth rate of 19.5%.

At the level of public hospitals, the fundamental orientation of public hospital reform is to uphold their public-welfare nature, while enhancing the quality and efficiency of medical services through measures such as optimizing resource allocation and controlling costs. This has made medical service innovation, artificial intelligence, patient experience, and healthcare big data the key keywords for public hospital reform in 2024.

On the other hand, the normalization and long-term persistence of anti-corruption efforts in the healthcare sector constitute an integral part of the broader, systemic anti-corruption campaign across society. In recent years, China has continuously deepened these efforts through multi-agency collaboration.

With the release of the “Opinions on Carrying Out Quality and Efficacy Consistency Evaluation for Generic Drugs” in 2016, China’s healthcare reform has also advanced alongside the initiation of consistency evaluation, promoting a “vacating the cage to change the bird” strategy in the pharmaceutical sector to reduce costs and improve efficiency.

On one hand, the improved quality of domestically produced generic drugs and their accelerated substitution for originator products have reduced medical costs, representing the “cost reduction” aspect of healthcare reform. On the other hand, integrating the consistency evaluation with centralized drug procurement policies has driven rapid sales growth of winning brands in hospital channels and significantly enhanced procurement efficiency, thereby achieving “efficiency improvement.”

However, Li Junguo pointed out that the actual extent of advantages in medical insurance pricing resulting from the linkage between the consistency evaluation and centralized drug procurement remains to be observed.

It is worth noting that the deepening of pharmaceutical reforms has also driven a rapid elevation in R&D standards for innovative drugs. By leveraging strong policy incentives to foster substantive innovation, the bubble of high-level redundancy in the pharmaceutical and health industries has been burst.

Relevant report data shows:

○ The proportion of domestically produced new drugs approved in China increased from 4% to 48% between 2021 and 2023;

○ There was a significant increase in the number of innovative drugs approved for market launch by the NMPA from 2019 to 2023;

○ Among innovative drugs launched globally for the first time between 2019 and 2021, along with their countries of initial launch, the proportion of those first launched in China increased from 13.4% to 30%;

○ The number of overseas licensing deals for Chinese innovative drugs increased to 58 in 2023.

Li Junguo emphasized that, driven by robust supportive policies, initial achievements in innovative drug R&D have emerged, yet building a comprehensive ecosystem for innovative drugs remains a formidable and long-term task.

Healthcare insurance reform is reshaping the entire market landscape, with enhancing benefits for enrollees emerging as a key focus in the current phase. This is reflected in the orderly and progressive expansion of the national reimbursement drug list, broader coverage scope, and increased reimbursement limits, all built upon a widened insurance coverage base. Meanwhile, the healthcare security authorities are steadily strengthening and solidifying their specialized yet multi-functional management capabilities.

As of the end of 2023, the number of participants in China's basic medical insurance had reached approximately 1.334 billion, representing a 133.7% increase from 2013. The coverage rate has remained stable at over 95%, and the total number of drugs included in the catalog reached 3,088 (excluding traditional Chinese medicine decoction pieces).

Data from the National Healthcare Security Administration shows that medical insurance payments for innovative drugs have expanded rapidly, surging from nearly RMB 6 billion in 2019 to nearly RMB 50 billion in 2022, a 7.1-fold increase.

Thanks to this, drug prices have been further reduced, which is expected to alleviate the financial burden on patients by more than RMB 40 billion. The optimization of health insurance payment methods has also significantly reduced the burden on patients. In 2023, over 90% of China’s pooled regions had implemented DRG/DIP payment systems, resulting in an approximately RMB 21.5 billion reduction in out-of-pocket expenses for insured individuals compared with 2021.

Li Junguo pointed out that the leverage effect of medical insurance payment is becoming increasingly prominent, with intensified efforts in payment reform. The reform of medical insurance payment remains in a phase of continuous exploration and optimization; dynamic policy adjustments will be the norm for a certain period, and the market needs to anticipate and adapt to the resulting “period of turbulence.”

Overall, the series of supporting measures under medical insurance reform—including reforms to individual accounts, outpatient mutual aid, and pooled procurement for pharmacies—will bring greater benefits to medical institutions. The recent latest initiatives on medical insurance drug price governance have sparked heated industry discussion. In response, Li Junguo stated that drug price control is, in fact, an established function of the medical insurance authorities.

However, Li Junguo also noted that the characteristics and division of labor among different pharmaceutical distribution channels will become clearer as policies evolve and market demand diversifies. Although the pharmaceutical retail market is currently under pressure, it remains the most dynamic segment, and thus its future prospects continue to be viewed optimistically.

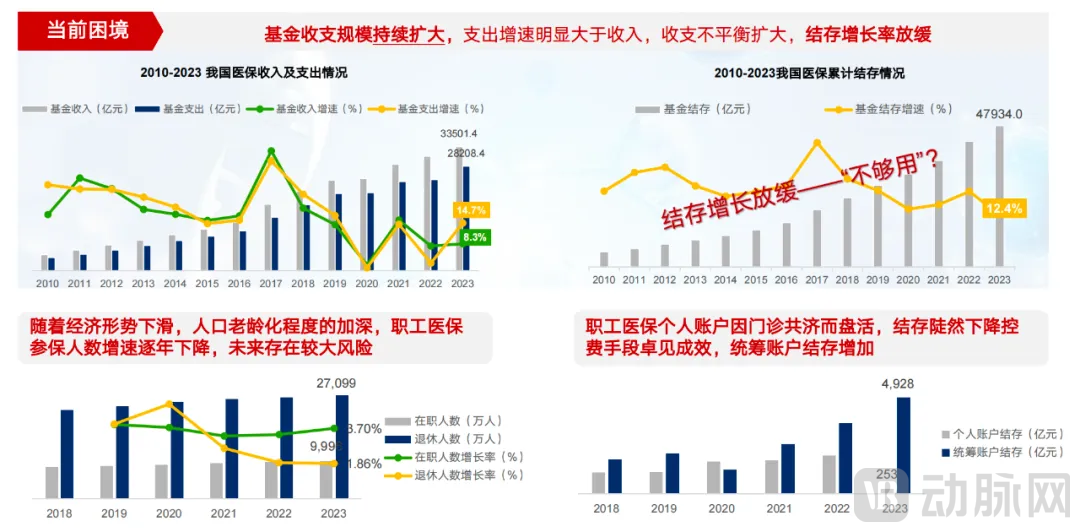

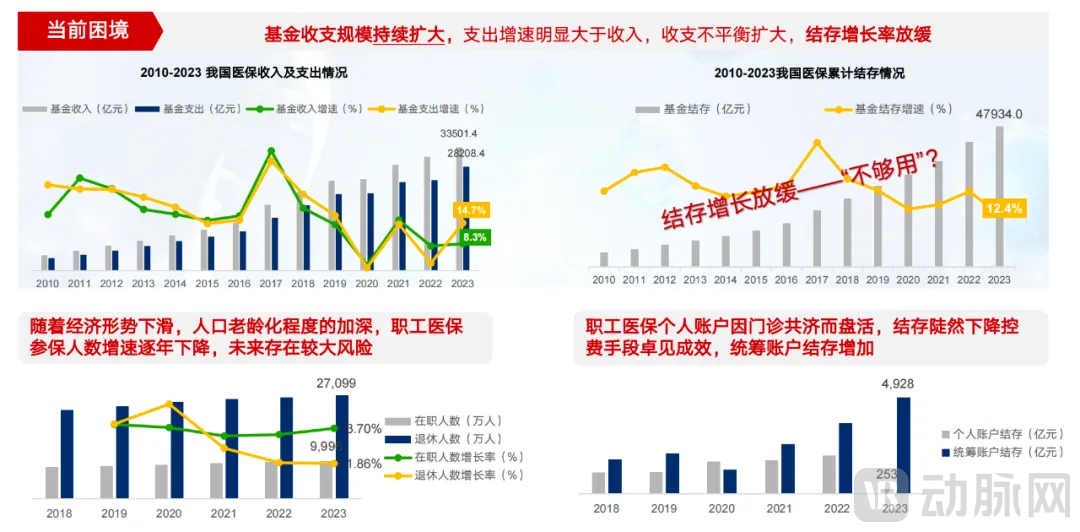

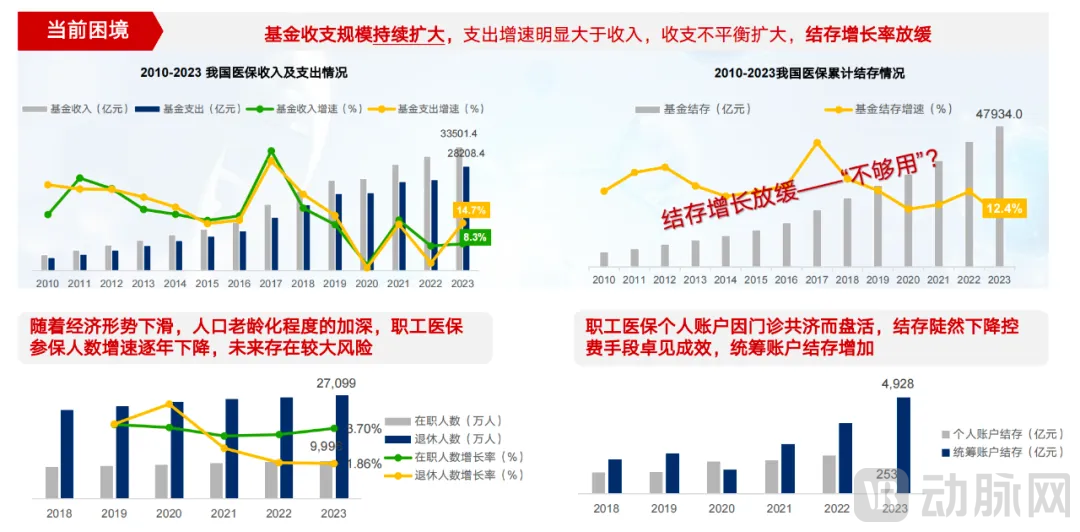

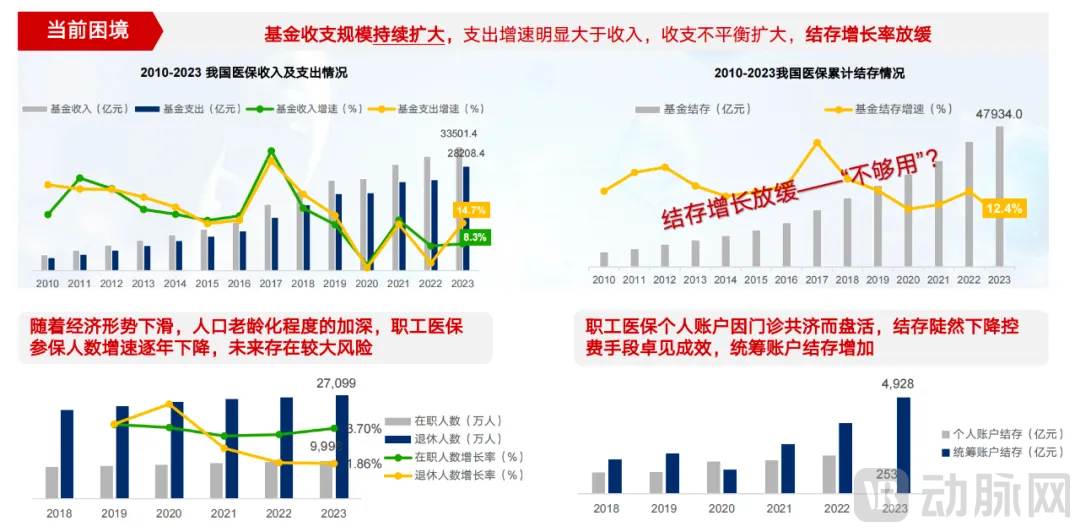

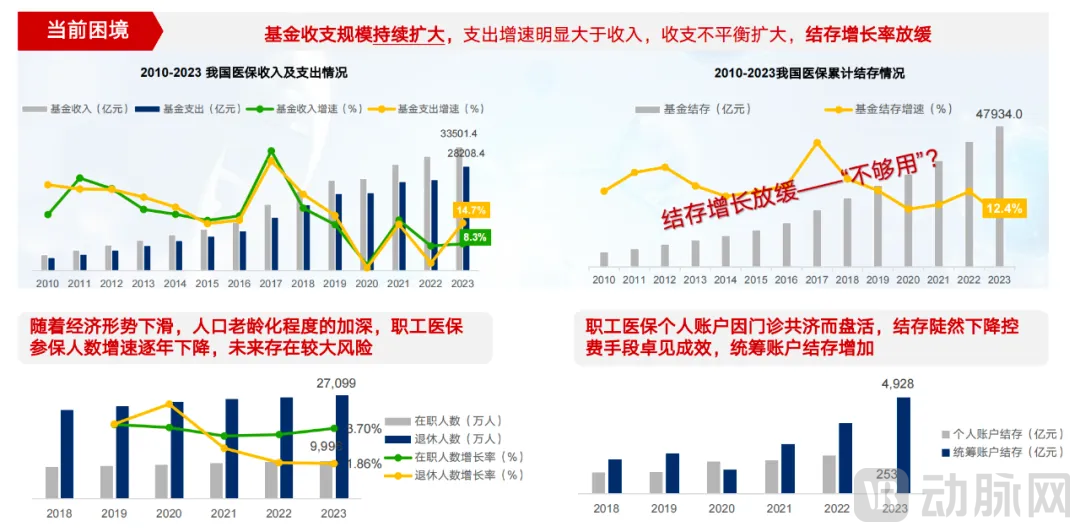

It is worth noting that, despite the current increase in medical insurance coverage on the payment side, the growth rate of the medical insurance fund’s accumulated balance is slowing down.

The underlying issue is that the growth in health insurance fund inflows is approaching its ceiling, while the financing capacity of resident basic medical insurance remains low. Against the backdrop of an aging population, the growing volume of unmet healthcare security needs will further intensify the pressure on health insurance funds.

Li Junguo stated that, as healthcare reform is a global challenge, trial and error and fluctuations are inevitable during the process. However, professionals in the medical and health industry must not harbor any wishful thinking. A clear direction, steadfast advancement, and continuous acceleration will be the inevitable trajectory of future healthcare reforms. Should economic development encounter challenges and fiscal funds become tight, the industry market must withstand the test of “stormy weather.”