Future Landscape of the Prescription Drug Market Amid Evolving Market Dynamics

Driven by the normalization of centralized procurement, outpatient pooling, and the "New Three Equivalencies" policies, the landscape of the prescription drug market is undergoing gradual transformation and reshaping. What is the current state of the prescription drug market, and what are its future development directions?

At the 2024 Xipu Conference, Li Hongjian, Senior Research Director of the Commercial Data Division at Sinohealth Technology, delivered an insightful report titled “Perspectives on the Future Landscape of Prescription Drugs from Market Changes,” providing attendees with an in-depth analysis of the current state of the prescription drug market, the challenges it faces, and the opportunities for future development.

Li Hongjian, Senior Research Director of the Commercial Data Division at Sinohealth Technology

In recent years, factors such as the transformation of economic growth and the continued deepening of new healthcare reform policies have had a profound impact on the prescription drug market.

From the perspective of the external economic environment, GDP growth has moderately accelerated over the past three quarters, while the growth rate of total retail sales of consumer goods has gradually slowed. Following the initial surge in retaliatory consumption after the easing of pandemic restrictions, residents’ willingness to spend has returned to a rational level, and consumer demand has become increasingly stable.

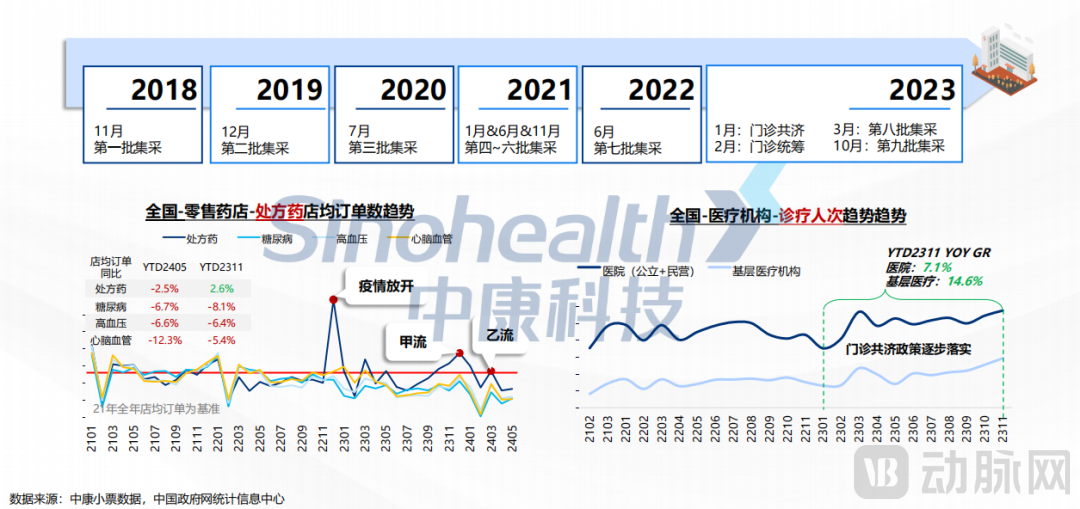

In terms of policy, the impact of normalized centralized procurement on the market for medications treating the “three highs” (hypertension, hyperglycemia, and hyperlipidemia) has stabilized. However, the implementation of the outpatient mutual aid policy has led to a resurgence in patient visits at medical institutions, resulting in a declining trend in out-of-hospital customer traffic for related “three highs” product categories.

According to data from the Statistical Information Center of the Chinese Government Website, as of November 2023, the number of patient visits at hospitals (public and private) and primary healthcare institutions increased by 7.1% and 14.6% year-on-year, respectively. During the same period, however, data from Sinopharm’s receipt-based analytics showed that the average number of orders per retail pharmacy for medications treating diabetes, hypertension, and cardiovascular and cerebrovascular diseases declined to varying extents year-on-year.

Since 2024, drug price governance has continued to deepen, leading to more standardized pharmaceutical price management in the future. Meanwhile, with the advancement of the “Internet + Healthcare” policy, online medical insurance payment has been implemented in multiple provinces and municipalities, further accelerating the reshaping of the pharmaceutical retail market landscape.

How Is the Prescription Drug Market Performing Under the Combined Influence of Multiple Factors?

In 2023, the omnichannel prescription drug sales volume exceeded RMB 12 trillion, representing a year-on-year increase of 6.7%, indicating steady growth. Among this, retail pharmacies (including O2O) accounted for 19.7% of the total market size, with a growth rate of 3.7%; the share of B2C e-commerce further increased to 2.9%, achieving a growth rate of 20.7%.

On the other hand, although the sales of prescription drugs in retail pharmacies across China have maintained year-on-year growth over the past three years, further expanding the market size, their growth rate has slowed down under the influence of policies. According to Zhongkang CMH, as of May 2024, the market size of prescription drugs in retail pharmacies nationwide reached RMB 101.3 billion, representing a 1.3% increase compared to the same period last year.

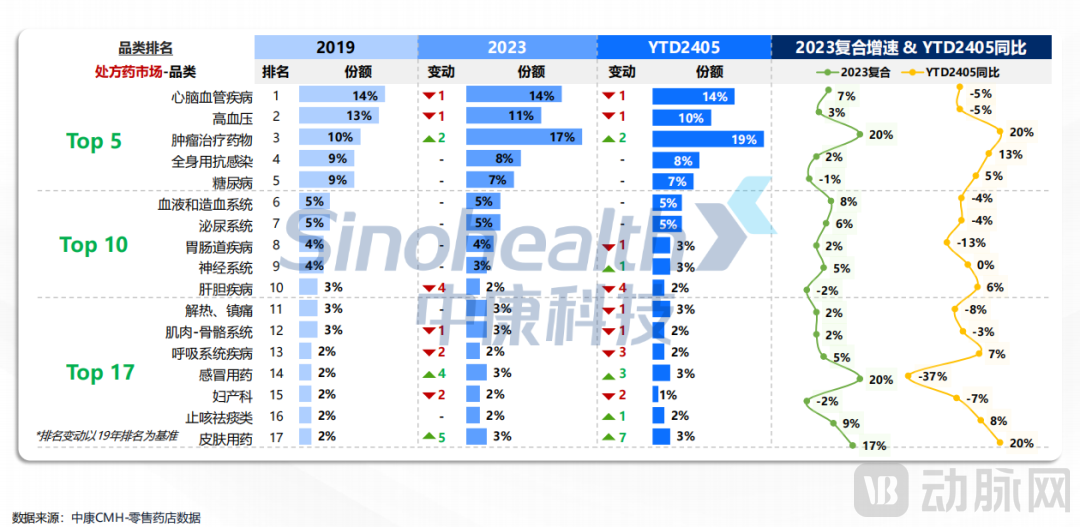

The category landscape of offline retail pharmacies is also being further reshaped by changing demand and policy drivers. A comparison of the proportion and growth rate changes of top categories before the pandemic, after the pandemic ended, and as of May 2024 reveals that, from a category perspective, oncology drugs have risen to become the leading category. Under the influence of the gradual implementation of outpatient mutual aid policies, the growth rate of medications for “three highs” (hypertension, hyperglycemia, and hyperlipidemia) has slowed, with cardiovascular and cerebrovascular disease medications and antihypertensives showing negative growth. Driven by recurring outbreaks of Influenza A, Influenza B, Mycoplasma infections, and COVID-19, related categories such as cold remedies and cough suppressants/expectorants have both increased compared to 2019 levels. Furthermore, the potential of the dermatology category in retail pharmacies continues to grow, with its ranking rising for two consecutive years.

Overall, the retail market for prescription drugs is at a stage characterized by both challenges and opportunities. For pharmaceutical companies, the key to achieving long-term development lies in how well they can navigate these changes and adjust their strategies in a timely manner.

Taking the United States as an example, offline retail pharmacies dominate the pharmaceutical market, with prescription drugs accounting for more than 80% of the market size. This indicates that, compared to developed countries, prescription drugs still have considerable growth potential in China’s retail market. The industry can conduct in-depth exploration from three dimensions: “people,” “products,” and “channels.”

People

As China’s population aging continues to deepen, the demand for medications for chronic diseases is gradually increasing. Medications for chronic conditions represent the core prescription drug purchasing need among middle-aged and elderly populations, and providing personalized chronic disease management services can effectively improve medication adherence among purchasers.

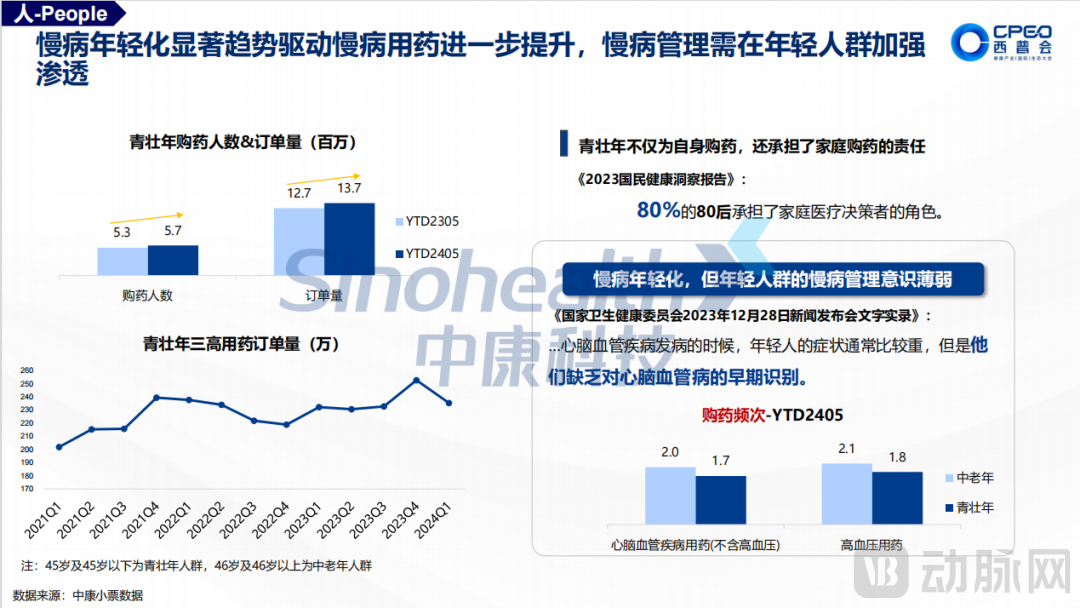

Meanwhile, the rise of the young and middle-aged demographic cannot be overlooked. Although offline pharmacies currently serve primarily customers aged 46 and above, the proportion of younger and middle-aged consumers is steadily increasing. This group possesses considerable purchasing power, contributing to higher average transaction values and gross profit margins. Furthermore, they often bear the responsibility for household medication purchases. Amidst the trend of chronic diseases affecting younger populations, this demographic will inject greater vitality into the retail prescription drug market.

Product

Channel Layout and Operational Strategies for Different Categories of Prescription Drugs Are Crucial.

Prescription-dominant categories, such as antithrombotic and antidepressant drugs, exhibit a strong reliance on in-hospital channels, with in-hospital sales accounting for over 70% of total omni-channel revenue. Patients depend on physicians’ prescriptions and medical guidance for each purchase and cannot independently continue their medication regimens. Following the implementation of volume-based procurement (VBP), the out-of-hospital market is dominated by generic drugs that won the bids, making strengthened in-hospital presence a core strategic priority.

In contrast, weak-prescription categories such as antihypertensives and lipid-lowering agents have greater opportunities in the out-of-hospital market. For these prescription drugs, the distribution channels within and outside hospitals are relatively balanced, with out-of-hospital sales accounting for 40%–60% of total omnichannel revenue.

Non-winning weakly prescribed drugs continue to maintain steady growth in the out-of-hospital market. Originator brands are strengthening their presence in this sector, leveraging brand advantages and refined operational strategies to sustain market share. Following the implementation of volume-based procurement (VBP), non-winning originator brands still have opportunities to regain lost ground in the out-of-hospital market through multi-dimensional strategic combinations.

Consumer-oriented prescription drugs, such as those for andrology and dermatology, carry greater weight in out-of-hospital channels, with sales accounting for over 60%. Patients can independently purchase or switch medications, demonstrating a high degree of purchasing autonomy. The convenience and privacy protection offered by e-commerce platforms provide strong growth momentum for these categories, while also reshaping patients’ medication-purchasing habits, with a noticeable online preference for bulk buying and stockpiling. The diversification of information sources enables consumer-focused prescription drug brands to shift from single-channel B-end promotion to direct-to-consumer (DTC) strategies for brand building and purchase conversion.

Prescription drugs can drive steady foot traffic; retail pharmacies can provide comprehensive treatment plans based on patients’ conditions, thereby increasing average transaction value and enhancing customer stickiness through cross-selling.

Category Landscape Outlook: In 2024, oncology therapeutics, systemic anti-infectives, diabetes medications, dermatological agents, and antitussive/expectorant and oral-throat preparations are expected to maintain robust growth. From a product perspective, Angong Niuhuang, azithromycin, dapagliflozin, and Suhuang Zhike still hold significant potential.

Field - Place

The pharmaceutical retail sector has entered an era of omnichannel deployment. Over the past two years, the importance of prescription drugs across various channels has continued to rise, with the O2O (Online-to-Offline) channel maintaining robust growth. According to data from Sinohealth CMH, as of May 2024, the year-on-year growth rate of prescription drug sales in the O2O channel reached 23%.

Omni-channel layout demands more refined operational management. Prescription drugs of different categories have varying advantages across channels, requiring targeted channel strategies. For instance, cardiovascular and cerebrovascular disease medications and oncology therapeutics are predominantly sold in offline pharmacies, while systemic anti-infectives and cold/fever-clearing medications are experiencing rapid growth in the O2O sector. In the refined operation of e-commerce channels, emphasis should be placed not only on product categories but also on timing, tailored to the attributes of each category.

Secondly, there are significant regional disparities in the practical implementation of outpatient pooling policies. For instance, differences between Wuhan and Dalian in terms of prescription outflow, medical insurance benefits, and regulatory intensity have directly impacted the sales and market performance of prescription drugs. Furthermore, factors such as regional variations in residents’ consumption levels and medication preferences have created distinct opportunity spaces for different brands.

Overall, offline retail pharmacies also need to adopt a “city-specific strategy” and implement refined layouts for different cities.

Although the prescription drug market currently faces challenges, forecasts indicate that it also holds immense potential and opportunities. By closely monitoring policy changes, promptly adjusting strategies, and implementing more refined management across consumer, product, and channel dimensions, companies can overcome these challenges and achieve sustainable growth.