Consolidation Surge in Consumer Healthcare: 15 Deals and Over 230 Clinics Acquired in First Half of 2024

Aier Eye Hospital

Ophthalmology Medical Chain Institution

Since 2024, Aier Eye Hospital, the leading provider of ophthalmic services, has announced three acquisitions within three months, covering a total of 106 medical institutions both domestically and internationally. These substantial transactions have become the focus of the industry. Aier Eye Hospital invests in reserve projects through merger and acquisition funds, incubates them externally, and then acquires them at an appropriate time to consolidate their performance into the listed company’s system—this expansion process has long been well-known within the industry; among the medical institutions acquired in 2024, domestic projects also followed this model, which is essentially routine practice.

However, a broad view of the consumer healthcare services sector reveals that not only Aier Eye Hospital but also numerous companies in fields such as dentistry, traditional Chinese medicine (TCM), medical aesthetics, and health checkups carried out key acquisitions in 2024. According to publicly available data, since the beginning of 2024, 15 M&A transactions in the consumer healthcare services sector have involved more than 230 medical and aesthetic institutions.

The prosperity of consumer healthcare appears to be returning.

Selected M&A Activities in Consumer Healthcare Services Since 2024; Source: Company Announcements and Public Reports

Selected M&A Activities in Consumer Healthcare Services Since 2024; Source: Company Announcements and Public Reports

Mergers and acquisitions (M&A) have become a standard pathway for healthcare service providers to expand their operational scale. As industry consolidation accelerates, healthcare services can further optimize resource allocation and enhance operational efficiency through M&A activities.

In the consumer healthcare sector, although the economic environment has had a certain impact on the overall market, mergers and acquisitions among consumer healthcare service providers have occurred frequently since 2024, with many companies undertaking pivotal acquisitions that set new records or marked their “firsts.”

Specifically regarding Aier Eye Hospital, in May 2024, the company announced plans to acquire partial equity interests in 52 medical institutions, including Chongqing Optometry and Ophthalmology and Zhoukou Aier, for a transaction amount of RMB 1.344 billion; in June, Clínica Baviera, the European division of Aier Eye Hospital, announced the acquisition of 100% equity in the UK-based Optimax Group, which operates 19 medical facilities in the United Kingdom; in July, Aier Eye Hospital issued an announcement regarding the acquisition of partial equity interests in 35 hospitals, including Humen Aier and Yuncheng Aier, for a transaction amount of RMB 898 million.

Overseas, Aier Eye Hospital is continuously expanding its presence in key countries. Previously, the Clínica Baviera medical network had covered Spain, Germany, Italy, and Austria in Europe; the acquisition of Optimax marked its formal entry into the UK market.

In China, by the end of 2023, Aier Eye Hospital had basically achieved a nationwide presence in major and medium-sized cities through self-built and acquired eye hospitals. Since 2024, among the medical institutions acquired, with the exception of Chongqing Optometry, Nanchang Hongcheng Aier, and Fuzhou Aier, the vast majority have been projects at the prefecture-level and county-level, accelerating penetration into prefecture and county markets.

Prior to 2021, Aier Eye Hospital’s individual acquisitions primarily targeted single hospitals; starting in 2021, it gradually began acquiring multiple hospitals in a single transaction, up toIn 2024, a record was set for the acquisition of 52 medical institutions in a single transaction. From 2024 to the present, Aier Eye Hospital has also reached an all-time high in terms of the number, frequency, and transaction value of its acquisitions of medical institutions.

In the dental sector, the high reliance on dentists and low dependence on equipment make standardized operations and rapid expansion challenging. However, for dental chains, increasing the number of clinics to scale up remains an inevitable path to growth and development.

In 2023, Topchoice Medical achieved a total operating revenue of RMB 2.846 billion, representing a year-on-year increase of 4.70%, while its net profit amounted to RMB 500 million, marking a year-on-year decline of 8.72%. “The development model reliant on cash burn and headcount expansion has become obsolete,” Topchoice Medical summarized in its financial report. Consequently, Topchoice Medical has now adopted a new expansion model.

In March 2024, Topchoice Medical announced the completion of its acquisition and capital increase of Loudi Stomatological Hospital Co., Ltd. (hereinafter referred to as “Loudi Stomatology”), with a total transaction amount of RMB 32.48 million, covering eight hospitals and outpatient clinics under Loudi Stomatology.

It is understood that Topchoice Medical’s previous expansion model primarily relied on building its own medical institutions, with half of its hospitals still operating at a loss in 2023. While establishing proprietary medical facilities offers numerous advantages—such as ensuring consistency with existing entities in terms of service and operational standards, corporate culture, and brand image, facilitating better integration of new businesses into the overall corporate strategy, and exerting stronger control over newly established institutions—the drawbacks are also evident: substantial capital investment, long payback periods, and the risk of failure during the incubation phase.

Obviously,Topchoice Medical Seeks to Mitigate Risks by Shifting Its Expansion Model. The 2024 acquisition of Loudi Stomatological Hospital marks the first implementation of Topchoice Medical’s M&A and franchising strategy, signaling that its future external expansion will transition from relying solely on organic growth to prioritizing mergers, acquisitions, and franchising.

Over the past two years, the wave of Chinese pharmaceutical and medical device products going global has continued to surge,The trend of global expansion has also reached the healthcare services sector; previously, companies such as Aier Eye Hospital and Jinxin Fertility had already established overseas operations in fields like ophthalmology and assisted reproduction, and now traditional Chinese medicine (TCM) has also joined the wave of going global.

Since 2024, Gushengtang has acquired multiple medical institutions, including Beijing Yayuncun Traditional Chinese Medicine Hospital, Changshu Nanshan Tang, Ningbo Yinzhou Guyuan Tang, Ningbo Yinzhou Mingyi Tang, and Ningbo Yinzhou Zhanhai Guyuan Tang. Notably, Gushengtang signed an agreement to acquire 100% equity of Baozhongtang Singapore, marking its first step toward internationalization.

As planned, Gushengtang will continue to expand its presence in Singapore and other overseas markets through strategic investments, mergers, and acquisitions, extending its “medical services first, pharmaceuticals second” model deeper into international territories.

External medical aid featuring TCM techniques, overseas Chinese practitioners providing TCM services, and foreigners studying TCM have all deepened the overseas market’s understanding of Traditional Chinese Medicine (TCM). With the application of digital technologies, the standardization of TCM has improved, allowing it to be organically integrated with evidence-based medicine. This integration will enable TCM to gain greater recognition in overseas markets and unlock larger market opportunities.

In the maternal and child health sector, influenced by the declining fertility rate, investment, financing, and M&A transactions have remained sluggish over the past two years. The number of obstetrics hospitals and obstetrics and gynecology departments in both private and public general hospitals is decreasing.

In early 2024, Weienno announced the acquisition of Beijing Future Children's Hospital, marking its first hospital acquisition and one of the few transactions in the women’s and children’s healthcare sector over the past two years. Furthermore,Historically, acquisitions in the maternal and child health sector have mostly involved well-funded chain clinics or large hospitals backed by industrial conglomerates acquiring smaller clinics. In contrast, Weienno’s acquisition of a hospital as a chain clinic operator constitutes a “reverse” acquisition.

Whether it is ophthalmology acquisitions setting record highs, dental chain expansions pioneering new models, traditional Chinese medicine enterprises embarking on global expansion through acquisitions, or “reverse” acquisitions in the women’s and children’s healthcare sector,All signs indicate that 2024 was a pivotal year for consumer healthcare services. After enduring significant challenges from the external environment in previous years, companies are leveraging this turning point to embark on new journeys as medical services return to normalcy.

M&A activity in the consumer healthcare sector remained robust in 2024, driven by a confluence of factors.

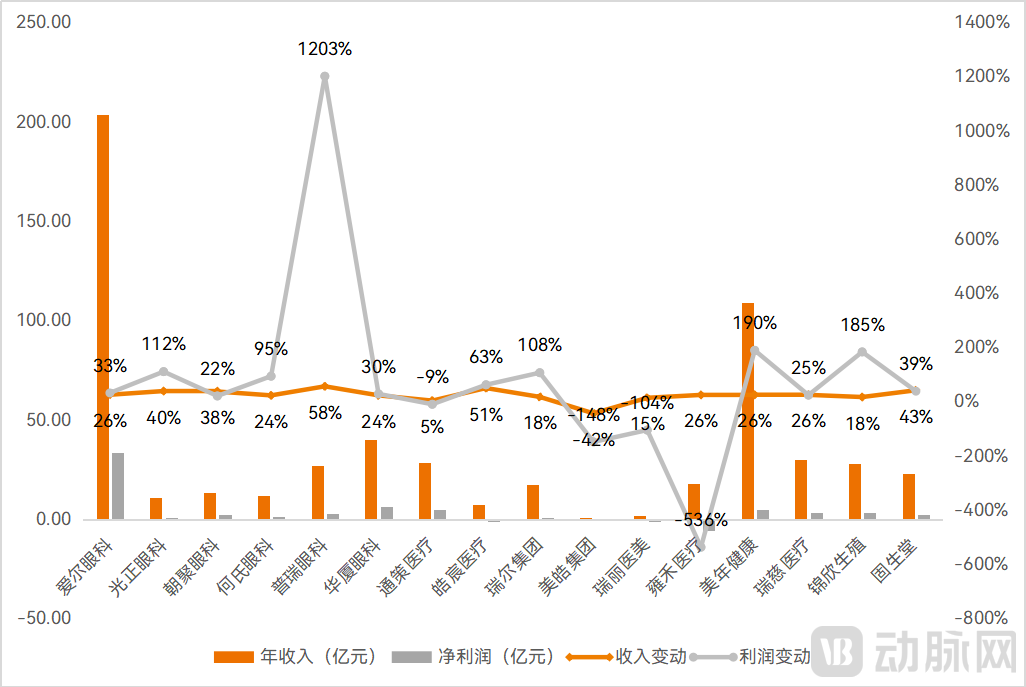

First, the gradual improvement in business operations has brought more ample funding.Financial reports from various companies show that, based on 2023 data, all enterprises except for a very few in the dental and medical aesthetics sectors achieved substantial growth in revenue and profits.

Annual Revenue and Profit of Selected Listed Companies in the Consumer Healthcare Services Sector (Arrail Group’s data is for the fiscal year ended March 2024; all other companies’ data is for the 2023 fiscal year)

Annual Revenue and Profit of Selected Listed Companies in the Consumer Healthcare Services Sector (Arrail Group’s data is for the fiscal year ended March 2024; all other companies’ data is for the 2023 fiscal year)

Data source: Corporate financial reports

Meanwhile, as economic cycles shift and the investment and financing landscape evolves, the healthcare services sector is entering a period of consolidation.A cohort of healthcare institutions, despite possessing superior technical expertise and service capabilities, are compelled to pursue mergers and acquisitions (M&A) amid current pressures from investor exits, financing constraints, and operational challenges. With valuations across the healthcare sector undergoing a broad correction—including healthcare services—this period presents a strategic window for acquirers to expand through M&A.

The slowdown in IPOs has also spurred increased M&A activity in the healthcare services sector.Since 2023, the landscape for initial public offerings (IPOs) in the healthcare and medical sector has been less than optimistic. Nevertheless, numerous healthcare service providers have remained active in this space, with consumer-oriented medical services consistently present. For companies striving to go public, acquiring institutions that already generate revenue or are profitable can directly drive performance growth, while the acquired parties can facilitate a smooth exit for their investors.

Prior to submitting its prospectus in June 2024, Distinct HealthCare acquired a 51.04% equity stake in Wuhan Shenlong Tianxia, which operates one secondary hospital and two clinics. Public records indicate that Wuhan Shenlong Tianxia reported revenue of RMB 26.7086 million and net profit of RMB 484,800 for the period ended March 2024. In its prospectus, Distinct HealthCare disclosed that it will continue to seek opportunities to acquire well-performing, mature medical service institutions in first-tier and new first-tier cities.

Tongrentang Medical and Elderly Care also pursued consecutive acquisitions during its IPO sprint. According to the prospectus, in January 2024, Tongrentang Medical and Elderly Care acquired a 70% equity stake in Shanghai Chengzhitang to strengthen its business presence in the Yangtze River Delta region. In June, the company signed an agreement to acquire a 60% equity stake in Shanghai Zhonghetang.

Healthcare service providers in certain specialized fields are undergoing transformation, expanding their specialties and service offerings through acquisitions, with women’s and children’s health being a typical example.

For example, Weier Nuo’s acquisition of Future Children’s Hospital signifies the company’s transition from specialized outpatient clinics to a comprehensive hospital model. Following the acquisition, it will develop along the lines of “strong specialties, limited general services.”

In July 2024, Lianchi Hospital, part of the Obstetrics and Gynecology Medical Group, issued an announcement stating its intention to acquire 100% equity interest in Hefei Xinhai Obstetrics and Gynecology Hospital for RMB 70 million. Prior to this acquisition, Lianchi Hospital already operated three hospitals, providing services in obstetrics, gynecology, pediatrics, orthopedics, health check-ups, and vaccination. This acquisition expands Lianchi Hospital’s service portfolio to include reproductive medicine and postpartum care centers. According to the hospital’s announcement, this move is aimed at optimizing the company’s strategic layout and cultivating new profit growth points.

Amcare, which was previously acquired by ByteDance, is also undergoing a gradual transformation. In 2024, Amcare disclosed that after 18 years of development, it has completed its transition from a specialized women’s and children’s healthcare provider to a more comprehensive medical platform, establishing a diversified presence across multiple disciplines, including oncology, assisted reproduction, orthopedics/sports medicine, obstetrics and gynecology, pediatrics, medical aesthetics, internal medicine, ophthalmology, otolaryngology, dentistry, and dermatology. In the fourth quarter of 2024, a large tertiary hospital under Amcare will also commence operations. Notably, Amcare had previously acquired Beijing Baodao Maternity Hospital to obtain the license for in vitro fertilization (IVF) services.

In recent years, although resident consumption has been constrained to some extent by objective environmental factors, health awareness among residents has strengthened, leading to a corresponding increase in related expenditures. According to data from the National Bureau of Statistics of China, in 2023, the per capita expenditure on medical and healthcare services for residents nationwide reached RMB 2,460, representing a year-on-year increase of 16%. This accounted for 9.2% of total per capita consumer spending, marking the first time in the past five years that this figure has exceeded 9%.

As is well known, population aging, as a deterministic trend, will create enormous market opportunities for the healthcare sector. For consumer healthcare, the opportunities brought by aging have already arrived and will become even more pronounced.

According to BCG’s “China Consumer Healthcare Market Outlook 2024,” the post-1960s generation, with greater financial strength and higher education levels, is entering a wave of retirement, driving robust demand for healthcare services.

Currently, the demand for consumer healthcare services related to aging has become significantly evident in areas such as health check-ups and traditional Chinese medicine.

Meinian Onehealth disclosed in its financial report that since 2023, demand for health check-ups among both groups and individuals has continued to rise. There has been sustained growth in diverse and personalized demands for healthcare services from government and enterprise clients, mainstream working professionals, high-income individuals, the elderly population, and patients with chronic diseases.

Traditional Chinese medicine (TCM) demonstrates significant advantages in managing geriatric and chronic diseases. The Notice on Comprehensively Strengthening Health Services for the Elderly, jointly issued by the National Health Commission, the China National Committee on Aging, and the National Administration of Traditional Chinese Medicine, proposes strengthening TCM health services for the elderly, aiming to achieve a TCM health management rate of over 75% among individuals aged 65 and above by 2025. In the future, TCM will continue to meet the diverse health needs of the elderly population.

The emergence of new technologies and products in consumer healthcare will provide users with more choices and stimulate greater demand.

In the fields of ophthalmology and dentistry, the market for pediatric myopia prevention and control as well as early orthodontic intervention is experiencing growth. Notably, new products are emerging that offer greater wearing comfort, more effective myopia progression delay, and enhanced cost-effectiveness. Early orthodontic products now feature richer functionalities, providing comprehensive intervention for symptoms associated with malocclusion. These products place greater emphasis on monitoring the dynamic development of children’s oral and maxillofacial structures and even incorporate additional oral healthcare benefits.

In the field of medical aesthetics, the penetration rate of non-surgical, minimally invasive services—whether energy-based device treatments or injectable procedures—is increasing. In particular, the rise of regenerative aesthetic medicine offers more natural and longer-lasting outcomes compared to traditional dermal fillers. Meanwhile, the efficacy and safety profiles of regenerative aesthetic products continue to be iteratively improved, providing a broader and superior range of options for anti-aging treatments.

Furthermore, the target demographic for consumer healthcare will expand from individuals to families.

Despite the overall downward trend in fertility rates, the proportion of families with two or three children has increased.According to the "Statistical Bulletin on the Development of China's Health and Healthcare Services in 2022," the number of births in 2022 was 9.56 million, with second children accounting for 38.9% and third or higher-order children accounting for 15.0%; in other words,These families consist of at least four or five members. Building a consumer healthcare service model centered on the family unit means expanding the user base at a lower cost.

New Century Healthcare has adopted a pediatric family physician membership model. By the end of 2023, it had cumulatively served nearly 480,000 families with women and children. In 2024, the company will drive upgrades to its customer management system and enhance the experience of its membership service products, continuously increasing the number of member households and the service reach rate.

Distinct HealthCare has also established departments of pediatrics, dentistry, ophthalmology, dermatology, otolaryngology and surgery, gynecology, and internal medicine within its medical institutions. By building a family-centered care model and fostering close collaboration among specialists across these disciplines, Distinct HealthCare addresses the diverse healthcare needs of patients and their entire families, continuously improves patient satisfaction, and creates opportunities for cross-departmental referrals.

By providing consumer healthcare services to families, demand can be transformed from single-occasion, low-frequency interactions into multi-person, higher-frequency engagements. This allows medical institutions to increase service volume while maintaining high average revenue per user. Meanwhile, collaboration and referrals among various specialties facilitate more efficient allocation of medical resources.

Although the consumer healthcare sector is currently showing a trend of returning prosperity, it is essential to control the pace of expansion to prevent integration difficulties arising from fundamental divergences in values and other core areas during acquisitions. There have been numerous precedents where large-scale acquisitions by healthcare service providers resulted in significant operational mismatches and failures.

Overall, despite the pressures of the economic environment, consumer healthcare services remain highly resilient, driven by heightened health awareness across all age groups and demographic segments; the key lies in taking steady, pragmatic steps forward.