R1 RCM, a Two-Time Listed Healthcare IT Firm, Sells for $8.9 Billion

R1 RCM

Revenue Cycle Management Service Provider

Across the ocean, a major development has emerged in healthcare revenue cycle management, a branch of health informatics.

R1 RCM (hereinafter referred to as “R1”), a long-established player in the U.S. healthcare revenue cycle management industry, announced in early August that it had reached a definitive agreement with an acquirer to sell the company and take it private for up to $8.9 billion.. This marks another major event in the industry within a short period: unicorn company Waystar successfully completed its IPO in early June, raising nearly $1 billion, and is regarded as the largest IPO in the digital health sector in 2024.。

Why Is R1 So Popular in the Capital Markets? How Much Potential Does Revenue Cycle Management (RCM), a Sector Often Overlooked in China, Actually Hold? VCBeat Has Compiled This Analysis for Industry Reference.

According to the information released by R1, this acquisition has been quite dramatic.

Prior to the acquisition drama, R1 had two primary shareholders. As of February 23, TCP-ASC (an investment vehicle jointly held by the investment firm TowerBrook Capital Partners and the healthcare services provider Ascension) and New Mountain Capital, the two largest shareholders, collectively held 62% of the common stock, with their respective equity stakes being very close.

Just days after R1 released its impressive fiscal year 2023 annual report, New Mountain Capital publicly filed an acquisition proposal.At that time, New Mountain Capital and its affiliates held 32.4% of R1’s shares and sought to acquire the remaining outstanding shares it did not own at $13.75 per share. The total value of the offer was slightly less than $5.8 billion, representing a premium of as much as 24% over the closing price on the previous trading day (February 23).

To complete the acquisition, New Mountain Capital engaged in arduous negotiations with another major shareholder, TCP-ASC. However,No agreement was reached between the two parties. Instead, TowerBrook Capital Partners, behind TCP-ASC, quickly joined forces with relevant investment funds under Clayton, Dubilier & Rice (CD&R) to submit a competing acquisition proposal.。

TowerBrook Capital Partners and CD&R have proposed to acquire the remaining equity at a price of $14.30 per share, which is clearly more favorable than the offer made by New Mountain Capital. According to information disclosed in R1’s press release, investment vehicles controlled by TowerBrook already held a 36% stake in the company as of early August, implying an implied market capitalization for R1 of as much as $8.9 billion.

This series of news also spurred a rise in R1’s stock price. On the last trading day before the initial acquisition announcement was made public, its closing share price was $11.10,Currently, its stock price is hovering around $14, representing a nearly 30% surge from previous levels.。

Ultimately, TowerBrook Capital Partners overtook competitors to complete the acquisition. Following the completion of the transaction, R1 will be delisted from Nasdaq and become a privately held company.

Interestingly,This also marks the second time in R1’s history that it has been “acquired” and delisted.。

Founded in 2003, the company, formerly known as Accretive Health, provided the industry’s first end-to-end RCM solution.Notably, Accretive Health at the time did not merely provide consulting services or take over hospital revenue cycle management (RCM) operations. Instead, it entered into five-year partnerships with clients, after which consultants were permanently assigned to specific clients to work collaboratively with healthcare institutions. Its revenue primarily consisted of base fees, plus a percentage of all revenues generated from operational improvements and cost reductions achieved relative to the first-year baseline.

Accretive Health experienced rapid growth from 2007 to 2011, with annual revenue reaching $250 million and a year-over-year increase of more than 50%. The company went public in 2011, achieving a market capitalization as high as $2.6 billion.

However, the then-star company fell into trouble due to a series of missteps. In 2011, an employee lost a laptop containing the personal information of 23,000 patients, leading to a data breach that triggered prolonged litigation and caused core clients to abandon the company. It was not until 2013 that it reached a settlement with the government.

Subsequently,In March 2014, Accretive Health was delisted from the New York Stock Exchange and moved to over-the-counter trading due to its failure to file a financial restatement. This marked the company’s first delisting.。

untilIn June 2015, Accretive Health, following a series of adjustments, announced that it had completed the filings originally due in 2014 and resumed public trading.。

That year, Ascension, one of the most well-known healthcare groups in the United States, became a client of Accretive Health. Subsequently,Ascension, in conjunction with TowerBrook Capital Partners, issued a hostile takeover bid to acquire Accretive Health at $2.50 per share, totaling $260 million, and threatened not to renew the contract expiring in 2017 if the acquisition failed.。

Accretive Health initially rejected the acquisition offer, deeming the price too low. However, since Ascension was its largest client, accounting for nearly half of its business volume, Accretive Health ultimately had no choice but to agree to the acquisition.

Of course, the first acquisition experienced by Accretive Health also ended its long-term turmoil, allowing the business to quickly get back on track. According to forecasts at the time, Accretive Health's revenue was expected to grow at least threefold within 10 years.

This forecast was clearly conservative. Keep in mind that in fiscal year 2015, its revenue stood at $117.2 million, and the acquisition price per share was just $2.50. Today, the company’s annual revenue has surpassed $2.2 billion, with its share price reaching $14.

In early 2017, Accretive Health was renamed R1 RCM, accelerating its growth trajectory.

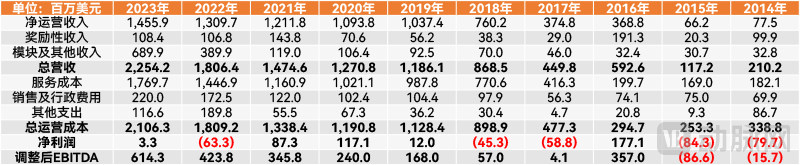

According to its annual report, R1 RCM achieved revenue of $2.3 billion in fiscal year 2023, a 24.8% increase compared to fiscal year 2022; net income reached $3.3 million, marking a significant improvement from the net loss of $63.3 million in the previous fiscal year. Adjusted EBITDA soared to $614.3 million, representing a substantial 45% surge from fiscal year 2022.

R1 Financial Report Data in Recent Years

Particularly noteworthy is that,R1 has maintained robust and stable growth, with a compound annual growth rate (CAGR) of 26.78% in revenue from 2014 to 2023.。

R1 also delivered strong performance in the first half of fiscal year 2024. Although revenue fell short of expectations due to the Change Healthcare cyberattack, its Q1 revenue still reached $604 million, a year-over-year increase of 10.7%. Q2 revenue amounted to $627.9 million, representing a 12% year-over-year growth. For the full fiscal year 2024, total revenue is projected to reach $2.6–$2.64 billion, with adjusted EBITDA expected to be in the range of $625–$650 million.

Compared with R1, Waystar—which successfully completed its IPO in June and was expected to raise up to $967.5 million, marking the largest fundraising round in digital health since 2022—pales in comparison. For the full fiscal year 2023, Waystar reported revenue of $791 million and a net loss of $51.3 million, only slightly higher than R1’s quarterly revenue.

In this light, it is perhaps not difficult to understand why R1’s two largest shareholders are willing to spend billions of dollars to vie for dominance.

RCM, or Revenue Cycle Management, is the process used by healthcare organizations to manage financial operations related to billing for medical services and collecting revenue.

In simple terms, RCM encompasses the entire workflow from initial patient scheduling and registration, through the conversion of provided care into billable codes and submission of claims to payers for reimbursement, to posting payments, managing accounts receivable, and finally generating patient statements. This process involves “appointment/pre-registration – benefit verification – clinical encounter – billing and coding – third-party follow-up – payment or denial management.”

The ideal RCM objective should enable healthcare organizations to collect the full amount due for services rendered in the shortest possible time, without any delays or errors.

It is important to note that the primary revenue source for healthcare institutions is insurance reimbursement. However, this payment process is highly complex, involving dozens of interdependent steps from the time a patient enters a healthcare facility to receive services until the post-service payment and reimbursement are completed. Within these multi-step workflows, the process of determining the amount of insurance reimbursement a healthcare institution should receive involves even millions of variables. In addition to tens of thousands of constantly changing diagnosis codes, there are unique insurance payment contracts, each with its own separate rules, processes, and reimbursement requirements.

In recent decades, the rapid expansion of the U.S. commercial insurance market and employer-sponsored benefit plans has rendered the healthcare payment system increasingly complex. Manual processing is no longer capable of tracking and managing all these variables. Coupled with ever-evolving regulatory requirements, this complexity inevitably leads to delays in reimbursement workflows and slower payment cycles for healthcare providers. Even minor oversights can result in incorrect claim submissions or denials, ultimately causing revenue loss.

Even in 2021, when Revenue Cycle Management (RCM) had already matured, approximately 17% of medical reimbursement claims in the United States were still denied upon initial submission. Once such errors or omissions occur, they can only be resolved through litigation, a process that is time-consuming, labor-intensive, and costly.

This has also become the direct reason why RCM has gained attention in the United States.

In 1996, the United States enacted the Health Insurance Portability and Accountability Act (HIPAA), which established standards for electronic data interchange in healthcare informatics and served as another key driver behind the rapid development of Revenue Cycle Management (RCM). HIPAA regulations mandate that any healthcare institution transmitting medical data must adopt standardized electronic billing practices, thereby fostering the development of standardized billing codes. This has made submitting reimbursement claims to payers easier than ever before, further enhancing the efficiency of RCM.

Subsequently, the widespread adoption of Electronic Medical Records (EMR) enabled healthcare institutions to capture patient information more accurately, thereby improving the accuracy of billing and coding. Furthermore, EMR facilitated the automation of numerous processes, enhancing the efficiency of Revenue Cycle Management (RCM) and reducing potential errors. From this point onward, RCM entered a period of rapid development.

Over the past decade or so, significant shifts have occurred across the healthcare industry, imposing specific demands on Revenue Cycle Management (RCM). For instance, billing for internet-based medical services has become a particularly challenging issue for healthcare institutions due to varying payer rules.

Furthermore, the healthcare industry is gradually shifting toward value-based care, resulting in reimbursement increasingly being tied to the quality of medical services and patient outcomes rather than solely calculated based on volume. This significant shift in reimbursement rules is also a key reason why Revenue Cycle Management (RCM) is receiving growing attention.

According to the report by Fortune Market Insights,At the end of 2022, the global market size for healthcare revenue cycle management (RCM) software was approximately $64.13 billion, with a projected compound annual growth rate (CAGR) of 10.7% from 2023 to 2030.。

Since getting back on track in 2018, R1 has embarked on multiple acquisitions, gradually emerging as a leader in the field.

In 2018, R1 acquired Intermedix Corporation, another player in the RCM space, for $460 million. In 2020, R1 acquired EHR vendor SCI Solutions for $190 million and Cerner’s RCM business for $30 million. In 2021, R1 acquired VisitPay, a digital payment solutions provider, for $300 million.

These successful acquisitions spurred R1 to pursue further large-scale deals, culminating in the 2022 acquisition of Cloudmed for up to $4.1 billion. Renowned for its intelligent healthcare big data analytics, Cloudmed helped clients recover over $1.5 billion in bad debt in 2021 and delivered an average return on investment (ROI) of 3–5 times for its customers.

What makes this even more intriguing is that it was precisely this acquisition that turned Cloudmed’s behind-the-scenes investor, New Mountain Capital, into a shareholder of R1, thereby triggering the aforementioned takeover battle.

At the end of 2023, R1 made another move, acquiring the RCM company Acclara for $675 million, further expanding its share in the RCM business.

According to the annual report, as of the end of 2023, R1’s platform possessed the architecture and capability to process demographic, clinical, and financial data for over 550 million patient visits annually. It served more than 3,700 healthcare organizations across the United States, including 93 of the top 100 medical groups. Additionally, it provided services to over 30,000 physicians. Statistics indicate that the net patient revenue covered by its business exceeded $1 trillion.

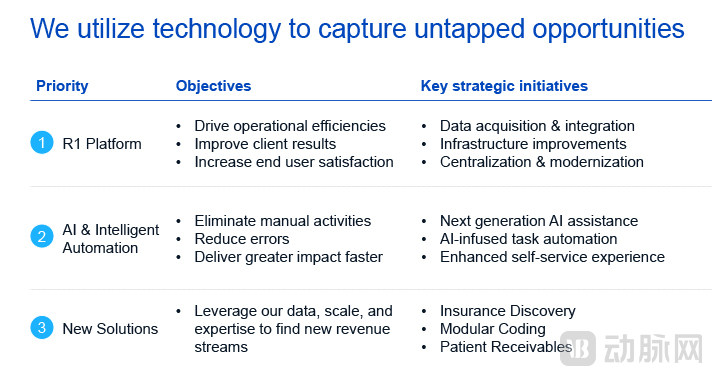

R1’s senior leadership attributes its business success to its mastery of technology.

R1’s Three Main Technical Pathways (Screenshot from R1 Presentation Materials)

The existing R1 platform features modularity and centralization. By leveraging generative AI, intelligent automation, and deep data analytics to process data from payers, EHR vendors, and financial institutions, it has enhanced operational efficiency, improved patient outcomes, and increased user satisfaction.

AI-based automation technology introduces next-generation generative AI capabilities, significantly reducing manual intervention, thereby lowering error rates and enhancing processing speed.

Furthermore, R1 is developing future solutions with the aim of introducing new capabilities such as insurance discovery, modular coding, and patient affordability, thereby exploring new business directions beyond its existing business model.

From R1’s acquisition to Waystar’s IPO, it is evident that the Revenue Cycle Management (RCM) sector plays a critical role in the U.S. healthcare system and is currently experiencing a new wave of momentum. Although this field has limited applicability in China due to differences in national conditions and healthcare systems, the technological innovations and process optimizations pioneered by leading RCM companies still offer valuable insights for the financial management and payment management branches of healthcare informatics. Meanwhile, with the ongoing reform of China’s medical insurance payment market, the introduction of RCM models in the future remains a distinct possibility.

On the other hand,The Once-Frozen Global Digital Health Capital Market Is Gradually Recovering—According to a report by Rock Health, U.S. digital health startups raised $5.7 billion in the first half of this year, slightly lower than the $6.1 billion raised in the first half of 2023. However, the number of financing deals reached 266, significantly higher than the 244 recorded in the same period of 2023, with the majority (84%) being early-stage rounds. In addition, the IPO market has also seen a long-awaited thaw. These developments indicate that the digital health sector is gradually recovering.。

VCBeat will continue to closely monitor the recovery of both RCM and digital health. Through peaks and troughs, we remain steadfastly by the side of entrepreneurs, providing valuable insights for the industry. Best of luck to all.

References:

Dave Muoio,fiercehealthcare.com:Revenue cycle management vendor R1 RCM receives $5.8B buyout offer from shareholder New Mountain Capital

Heather Landi,fiercehealthcare.com:TowerBrook, CD&R take health tech company R1 RCM private in $8.9B deal

Adriana Krasniansky、Mihir Somaiya、Sari Kaganoff,Rock Health:H1 2024 digital health funding: Resilience leads to brilliance

Andrew Walker,Harvard Business School Digital Initiative:Accretive Health: Revolutionizing the Revenue Cycle