Synthetic Biology in a Capital Winter: Which Companies Are Worth Investing In Amid Four Consecutive Years of Declining Investment?

In 2024, favorable policy winds for bio-manufacturing once again swept across the synthetic biology sector. From the “14th Five-Year Plan for Bioeconomy Development” to the “Implementation Opinions on Promoting Innovation and Development of Future Industries,” national and local governments have successively introduced a series of supportive policies to foster technological innovation and industrialization in synthetic biology, thereby driving the green transformation of the bioeconomy.

This has been followed by a surge in synthetic biology stocks in the secondary market, with related concept stocks experiencing significant gains. “Bio-manufacturing+” has emerged as a key sector and new business model for developing new quality productive forces. Many industry experts believe that the bioeconomy is poised to become the fourth industrial revolution, following the agricultural, industrial, and digital revolutions.

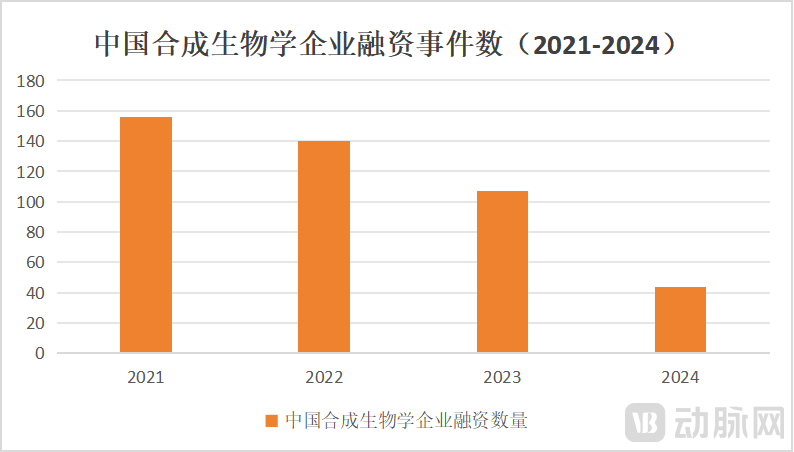

In stark contrast to the secondary market, synthetic biology has faced a “cold spell” in the primary market. According to data from VCBeat Orange and Qimingpian Pro, the number of financing deals in China’s synthetic biology sector has declined year by year since 2021, with a sharp drop in 2024.

Number of Financing Events for Chinese Synthetic Biology Companies (Data as of August 19, 2024)

Number of Financing Events for Chinese Synthetic Biology Companies (Data as of August 19, 2024)

Data sources: Qimingpian Pro, VCBeat Orange

Several investors told VCBeat, “We have reviewed numerous synthetic biology projects this year, but due to significant concerns, we have rarely made investments.”

Exceeded RMB 2 billion in the first half of 2024Over 40 casesFinancing

In 2000, with the establishment of Cathay Biotech, China’s synthetic biology industry was launched. Over the past two decades, the market size of China’s synthetic biology sector has continued to expand. According to Zhiyan Consulting, the market size of China’s synthetic biology industry was approximately USD 1.2 billion in 2023 and is projected to reach USD 4 billion by 2029, demonstrating strong development potential and growth momentum.

During this period, China’s synthetic biology sector has continuously achieved new technological breakthroughs. On one hand, technologies for gene sequencing, editing, and synthesis have undergone continuous iteration. Notable milestones include Amyris’s major breakthrough in artemisinin production in 2006 and the emergence of the groundbreaking CRISPR-Cas9 gene-editing technology in 2013, which have collectively driven a significant reduction in R&D costs for synthetic biology. On the other hand, basic research in the synthetic biology industry has advanced steadily, accompanied by a rapid increase in related patent applications. According to “Development of Synthetic Biology from the Perspective of China’s Top Ten Scientific Advances,” in 2022, China ranked second only to the United States globally in the number of published research papers on synthetic biology in biomedicine.

Accompanying breakthroughs in synthetic biology technologies and the growing number of innovative enterprises is an investment boom. Since 2015, investment in China’s synthetic biology sector has entered an acceleration phase. However, starting in 2020, the total amount of “investable capital” in the capital markets decreased, while “expected investment returns” in the biopharmaceutical sector declined. As a result, the investment community has sought to allocate limited funds to areas with greater potential.

In 2021, the field of synthetic biology witnessed a comprehensive surge in investment and financing, with total funding in the synthetic biology industry reaching RMB 2.3 billion. Simultaneously, a wave of initial public offerings (IPOs) swept through the secondary market, as industry giants Cathay Biotech and Huaheng Biotechnology successfully listed on the STAR Market. However, the “spotlight” on synthetic biology gradually dimmed thereafter. According to data from VCBeat Orange and Qimingpian Pro, the number of investment deals stood at 156, 140, and 107 in 2021, 2022, and 2023, respectively, showing a year-on-year decline.

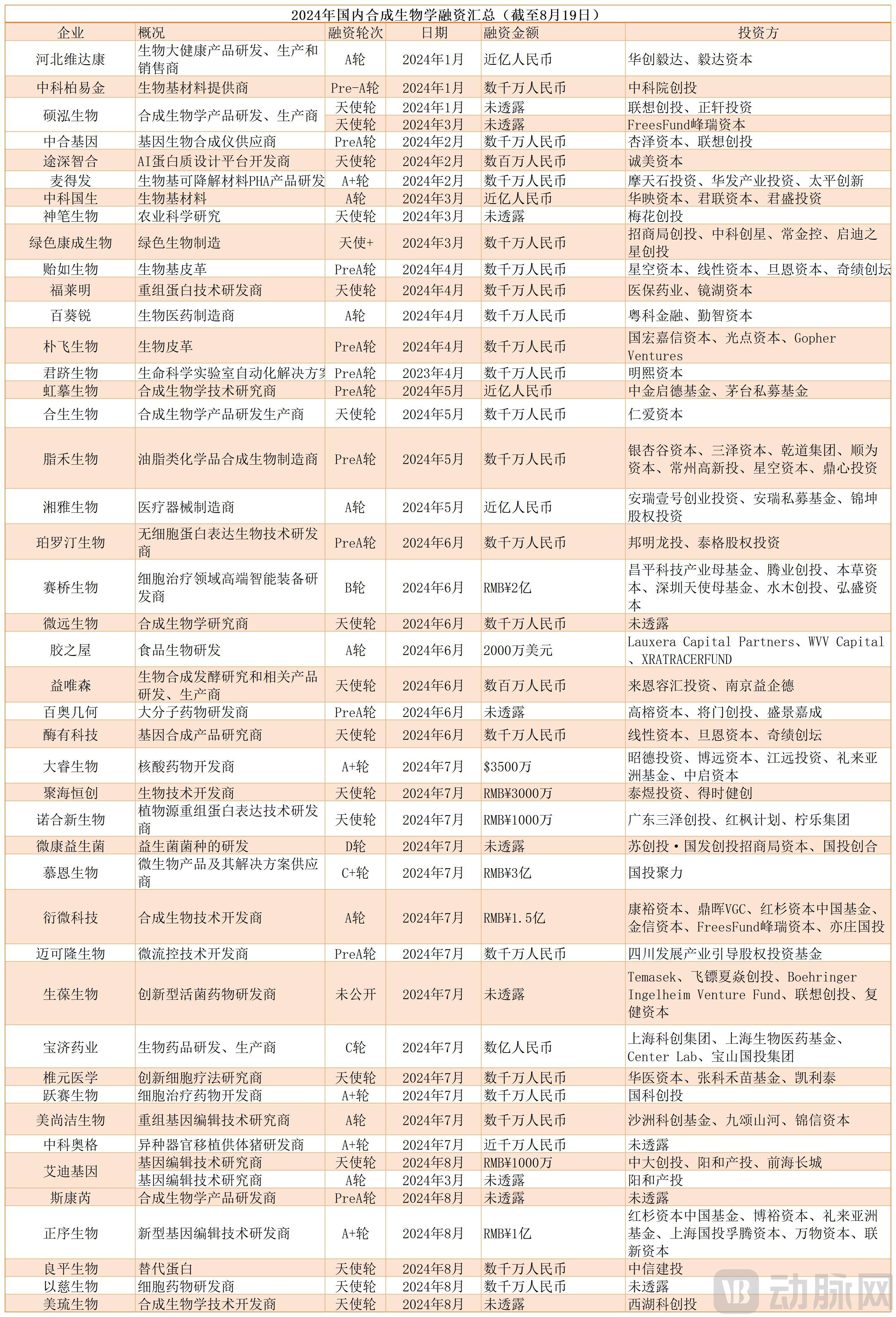

As of August 19, according to incomplete statistics from VCBeat, there were a total of 44 financing rounds in the primary market for synthetic biology in 2024.. Roughly calculated, the total financing amount has exceeded RMB 2 billion.

The following is a summary of investment and financing data:

Synthetic Biology Investment and Financing Companies in 2024 (as of August 19) | Compiled by VCBeat

Overall, the investment style in the field of synthetic biology clearly favors early-stage and small-scale ventures. Among the 44 financing rounds, only four were at Series B or later, involving Saikiao Biotechnology, Weikang Probiotics, Moonshine Biotherapeutics, and Baoji Pharmaceutical. This year, there were eight investments at the hundred-million-yuan level, with four concentrated at Series A or pre-Series A stages. These included Yanwei Technology, which raised RMB 150 million; Darui Biotechnology, which secured USD 35 million; Jiaozhiwu, which obtained USD 20 million; and Zhengxu Biology, which received RMB 100 million.

In terms of investment frequency and capital scale, there has been a slight downward trend this year. A year ago, Bluepha completed its Series B4 financing round, raising over RMB 400 million, led by Zhongping Capital with Jiangsu Huanghai Financial Holding Group (Huanghai Financial Holdings) as a co-investor. In 2023, Bluepha secured RMB 830 million in its Series B3 round. Across the entire Series B rounds, Bluepha raised a total of RMB 1.9 billion, establishing itself as one of the most prominent companies in the primary market for synthetic biology. This year, Moon Biotech secured the largest single investment; combined with its previous RMB 200 million in Series C financing, its total Series C funding has reached RMB 500 million.

A review reveals that in the field of synthetic biology, the Sequoia-affiliated entities (including Sequoia China, Sequoia Seed Fund, etc.) lead with investments in 28 innovative companies.as the institution with the most extensive network;IDG Capital followed closely with 27 investments. However, among these firms, only Sequoia China has made moves in the synthetic biology sector this year, investing in Yanwei Technology, which focuses on lipid biosurfactants, and Zhengxu Bio, which specializes in novel gene-editing technologies.

In addition, the SDIC-affiliated funds have invested in 24 companies, including SDIC Juli, which secured the largest financing deal of the first half of the year through an exclusive RMB 300 million investment. Among investors with a strong industry-guiding focus, Temasek and Lilly Asia Ventures stood out, having invested in 25 and 18 companies, respectively.

Among the institutions active this year, industry guidance funds and university-affiliated research funds have also emerged as strong forces. The Shenzhen Angel Fund of Funds, Sichuan Development Industry Guidance Equity Investment Fund, Shanghai Science and Technology Innovation Group, and the Shanghai Biomedical Fund have all made investments this year, while university-affiliated research funds, represented by ShuiMu Ventures, are also actively expanding their portfolios.

Investment Becomes More Rational Amid the “Capital Winter”

It should be noted that the decline in synthetic biology financing is not an isolated trend. According to statistics from VCBeat, the phased downturn in global healthcare investment and financing continued in the first half of 2024, with the number of financing transactions plummeting by 21.9% compared to the same period in 2023. “Amid the capital winter, the synthetic biology sector may have been less affected than other healthcare fields,” said Gong Mo, General Manager of Linglu Capital.

During the capital downturn cycle, investment institutions have demonstrated more rational investment behavior. In the face of market uncertainty, these institutions have become more prudent in their investment decisions, placing greater emphasis on in-depth analysis of corporate fundamentals, particularly profitability, asset quality, and cash flow status. Meanwhile, investors tend to seek out companies with long-term growth potential and stable cash flows to ensure the safety and returns of their investments.

“At its core, investment must return to the fundamentals of business,” said Chen Hang of Mingxi Capital. Over the past few years, leading synthetic biology companies in China and abroad have delivered lackluster commercial performance, which has, to some extent, influenced investors’ judgments.

In 2021, synthetic biology unicorn Zymergen filed for an initial public offering (IPO) and successfully listed on the Nasdaq in April of that year, basking in unprecedented glory. However, just three months later, due to misjudging market demand and encountering difficulties in mass production, it was revealed that its core product nearing commercialization—a bio-based polymer film called Hyaline—had failed in large-scale manufacturing. Zymergen’s after-hours trading plummeted by 78%, wiping out nearly $2.5 billion in market value. Ultimately, it was acquired by industry star Ginkgo Bioworks for $300 million, marking a regrettable exit.

How Is Biotech Giant Ginkgo Bioworks Performing Financially? According to its Q2 2024 financial report, total revenue was $56 million, a 30% year-over-year decline; revenue from its core Foundry business amounted to $27.889 million, down 18.2% year over year. The operating loss stood at $223 million, and by the end of the second quarter, Ginkgo’s cash and cash equivalents balance had dwindled to just $730 million.

Since 2023, Ginkgo Bioworks has faced severe financial challenges, with its cash and cash equivalents balance declining continuously from $1.3 billion at the end of 2022, accumulating losses reaching $5.5 billion to date. In May this year, Ginkgo received a notice of non-compliance with NYSE listing requirements, as the average closing price of its common stock fell below $1.00 per share for 30 consecutive trading days. After announcing its second-quarter 2024 earnings report on Thursday (August 8), Ginkgo Bioworks rose 3.15% in after-hours trading. As of the market close on August 19, its stock price was $0.22 per share, with a market capitalization of $467 million. This represents a decline of over 98% from its peak market value of $26 billion.

“Some synthetic biology companies show no profitability, or experience substantial revenue growth but fail to turn a profit; such business models are also problematic.”Investor Mark (a pseudonym) stated that, taking Ginkgo as an example, the core business Foundry saw zero revenue growth in 2023 and continues to decline, which has somewhat undermined investor confidence.

From the perspective of most investors, there are additional reasons behind the trend toward more rational investment. “Regardless of how one looks at it, synthetic biology is no longer an emerging concept in the market after its development in recent years, and venture capital firms may no longer be willing to pay a premium for this concept. On the other hand, competition in the synthetic biology sector has intensified in recent years. Competition for certain raw material products has become fiercer, but due to relatively low technical barriers, it is difficult to generate sufficient innovations to attract institutional investors. Moreover, institutions cannot accept financial returns that fall short of expectations as a result of shrinking profit margins caused by intense cutthroat competition,” said Chen Hang.

In the field of synthetic biology, particularly in the development of cosmetic ingredients, product homogenization has become a significant issue. Rough estimates indicate that there are currently more than 40 synthetic biology companies in China focusing on this sector, with numerous startups and publicly listed firms concentrating on popular ingredients such as squalene, ergothioneine, and ectoin. As market competition intensifies, price wars have become inevitable. Taking ergothioneine as an example, its price has plummeted from RMB 200,000 per kilogram several years ago to just tens of thousands of yuan per kilogram, posing direct challenges to companies’ implementation capabilities and market expansion efforts. In February this year, Zhongke Nuoshi, one of the early participants in this field, declared bankruptcy.

“Nevertheless, despite various concerns, most investors remain confident in the future of the synthetic biology sector. ‘Synthetic biology is not a fleeting industry. It aligns closely with China’s current strategic focus on developing new quality productive forces, and its technological innovations and iterations will have a positive impact on industrial production, agriculture, medicine, biomaterials, and other fields. Therefore, although the number of financing deals has declined in the short term, this does not signal a sustained long-term downward trend,’ said Mark.”

Investing in Synthetic Biology with a Consumer Sector Mindset?

“After years of observing the synthetic biology sector, innovation capability and market competitiveness have likely become the primary considerations for stakeholders,” said Chen Hang. “In previous years, when the financing environment was favorable, many founders with academic or research backgrounds found it relatively easy to secure funding, partly because their companies had not yet reached the commercialization stage. However, as many companies’ commercial performance has fallen short of expectations, investors are now questioning whether they should continue to pay a premium for technological potential.”

Judging from the financing activities of synthetic biology companies this year, in addition to product-oriented and platform-oriented firms, tool-oriented companies have emerged frequently, with at least 13 such enterprises securing funding. This is precisely the sector that Chen Hang views optimistically: “Driven by technological innovation and market demand, I believe China’s synthetic biology tools and services sector will reach an inflection point. Currently, some companies have begun to specialize in providing synthetic biology tools and services. Although constraints such as confidentiality and cost remain, drawing on overseas development trajectories, I believe that a subset of these enterprises can achieve early breakthroughs.”

Mark also sees greater promise in synthetic biology companies operating at the tools layer. “We are more inclined to focus on the upstream tools segment, including areas such as DNA synthesis, sequencing, and editing. First, this layer offers concrete metrics—such as accuracy and cost—to assess performance, and there are many overseas counterparts for benchmarking. Second, upstream companies can serve a broader client base that may extend beyond the field of synthetic biology, offering a sufficiently large market opportunity. Furthermore, the barriers to entry at the tools layer are relatively higher; currently, only a handful of companies in China have established a presence, so the sector has not yet reached a stage of intense competition.”

“Advances in the tooling layer of synthetic biology will drive iterative innovation in downstream products, further reducing the cost of biomanufacturing. This also highlights the immense potential for the industrialization of synthetic biology and its disruptive impact on traditional industries,” said Chen Hang.

Gong Mo, who also holds the identity of an individual investor, believes that “it is inappropriate to invest in synthetic biology using the logic applied to pharmaceutical investments; rather, it is more suitable to apply consumer-sector investment logic.” Many end products of synthetic biology will ultimately target the consumer market. If one relies solely on pharmaceutical investment logic, there may be an excessive focus on technical details and the R&D process, while overlooking key factors such as market demand, business models, and consumer acceptance. “Therefore, in the current synthetic biology sector, strong market development capabilities are the most valued core factor.”

Regarding future investment and financing trends in synthetic biology, multiple investors highlighted a notable shift in interviews: beyond financial investments, there is a clear trend toward targeted industrial investments. Examples include Junji Biology, which received investment this year from Mingxi Capital (jointly established by Mingde Biological and Legend Capital), and Hongmo Biology, which saw increased investment from the Moutai Fund.

Hongmu Bio was jointly incubated by Mengniu and Yikolai Bio in 2022, primarily engaged in the research, development, and sales of products for nutritional health, with its core product being HMOs (human milk oligosaccharides). Internationally, HMOs have been widely applied in infant formula, dietary supplements, functional foods, and other sectors, whereas the domestic market is only just beginning to develop. Currently, there are very few companies in China capable of industrial-scale HMO production, including Hongmu Bio, Yixi Bio, Henglu Bio, and Zeno Tech. Among listed companies, Guangji Pharmaceutical, Cabio Biotech, and Langkun Environment are also laying out their product pipelines.

In recent years, the Chinese government has continuously strengthened its policy support for synthetic biology. Multiple regions, including Shanghai, Shenzhen, and Changzhou, have successively introduced policies to support the field. In addition to providing financial and technical support, these policies have clearly defined the industrial layout and development direction for synthetic biology.

No matter how the technological waves of synthetic biology in China surge, or how the heat of the capital market rises and falls, VCBeat will remain committed to closely following these developments, jointly anticipating the arrival of the “Bio-manufacturing Revolution.”

Reference Article:

Synthetic Biology: A Sunrise Industry Leading the “Third Biological Science Revolution.” China Science and Technology Information Magazine

“Amid the ‘Capital Winter,’ Which Institutions Are Still Investing in Synthetic Biology Companies?” by Dr. Fang