It's Raking It In: The Rise of a New Internet Healthcare Powerhouse Amid Industry Shakeout

Teladoc

Telemedicine Service Provider

Recently, publicly listed U.S. telehealth companies have released their latest semi-annual reports, with several major players showing poor performance. Teladoc, regarded as the pioneer of the telehealth industry, reported losses exceeding $800 million, and its stock price hit a near-decade low since its IPO. Another pioneer, Amwell, was forced to implement a reverse stock split to avoid delisting due to its share price falling below $1.

Not only that, the semi-annual financial reports of tech giants such as Amazon, Walgreens, and Walmart, which have all entered the internet healthcare sector in recent years, seem to signal one thing: internet healthcare is suffering massive losses.

However, this sector is not without its bright spots, as some emerging players in internet healthcare are rising rapidly. It may not be long before they supplant the “originators” and “pioneers” to become the new benchmarks for internet healthcare!

A Paradigm Shift Is Coming.

Teladoc, widely regarded as one of the pioneers of internet-based healthcare, has delivered disappointing performance over the past two years. In fiscal year 2022, the company reported a staggering net loss of $13.7 billion, primarily driven by goodwill impairment charges resulting from its acquisition of Livongo. The downward trend persisted into fiscal year 2023, with Teladoc still posting a net loss of $220 million, indicating no fundamental turnaround.

The poor performance also directly led to the voluntary resignation of the CEO who had led Teladoc to countless achievements over a 15-year period.

Although its prior performance had little direct bearing on the matter, Teladoc’s new CEO felt a chill under the scorching sun during his first fiscal quarter in office—Teladoc Reported Another $838 Million Loss in Q2; Total Loss for the First Half of Fiscal 2024 Reached $919.6 Million. In contrast, last year’s first-half loss of $134.4 million suddenly seems not at all glaring.

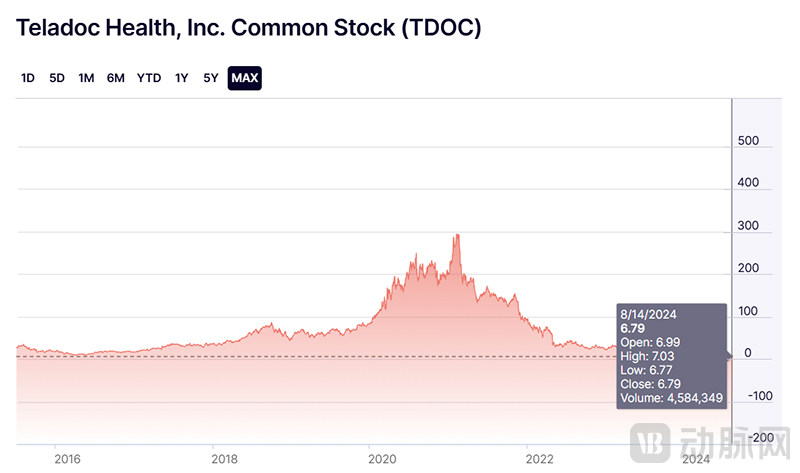

Dragged down by its performance, its stock price also fell to a historical low of $6.79 (closing price on August 14).It is worth noting that this pioneer of internet healthcare once reached a peak closing price of over $294 in 2021.Its market capitalization has evaporated by as much as 98% from its peak!Even compared to the beginning of this year, its stock price has plummeted by nearly 70%.

Teladoc’s Stock Price Hits All-Time Low (Screenshot from the Nasdaq Website)

The primary cause of the substantial loss this quarter was a $790 million goodwill impairment resulting from the underperformance of its mental health division, BetterHelp, which failed to meet committed expectations.According to the financial report, BetterHelp generated $265 million in revenue in Q2, a 9% decrease compared to Q2 of fiscal year 2023.

BetterHelp is an online mental health service platform acquired by Teladoc in its early stages. In January 2015, Teladoc acquired BetterHelp for $3.5 million in cash and a $1 million promissory note, and it has since grown into a major online mental health service platform.

Driven by the shortage of mental health services during the COVID-19 pandemic and its hourly rate of just tens of dollars—significantly lower than the $100–$200 per hour charged by private therapists in the U.S.—BetterHelp has experienced rapid growth.

In fiscal year 2021, BetterHelp generated $720 million in revenue, which surged by 40% to $1.013 billion in fiscal year 2022. In contrast to the sluggish growth of Teladoc’s other businesses during the same period, BetterHelp’s continued rapid expansion was once regarded as the key hope for leading Teladoc out of its predicament.

However, BetterHelp’s revenue growth slowed significantly in fiscal year 2023, increasing by only 11% year-over-year to $1.13 billion. In the first half of this year, its revenue even declined. Worse still, the average number of paying users for this segment dropped by 14% year-over-year to 407,000.

BetterHelp has long had a mixed reputation, with its efficacy drawing both praise and criticism. The platform’s primary reliance on text-based chat lacks robust evidence of effectiveness, and responses from online therapists are often delayed. Coupled with relatively low compensation, BetterHelp tends to attract less experienced therapists. These factors have increasingly fueled public skepticism about the therapeutic outcomes achieved through the platform.

Meanwhile, BetterHelp also faced data security issues, which led to a lawsuit by the FTC (U.S. Federal Trade Commission). It was not until 2023 that BetterHelp reached a settlement with the FTC, agreeing to pay $7.8 million in total to users whose health data had been allegedly shared and being prohibited from sharing user health data with third parties for advertising purposes.

BetterHelp has consistently failed to achieve a breakthrough in insurance reimbursement. During its earnings call, Teladoc executives stated that, based on insights into users who discontinued BetterHelp’s services, high out-of-pocket costs and lack of insurance coverage were among the primary reasons for churn.

Of course, a more significant reason for BetterHelp’s declining performance is its heavy reliance on advertising promotion, which has kept its marketing expenses persistently high. The recent U.S. presidential election further drove up online advertising prices, resulting in elevated customer acquisition costs. Consequently, the effectiveness of its already reduced advertising spend has diminished compared to previous periods, naturally impacting its revenue.

Amid declining performance and persistently high advertising costs this year, Teladoc’s senior management believes that BetterHelp not only faces no prospect of growth but could even see a double-digit decline in revenue if ad costs remain elevated. Due to the unpredictability of customer acquisition costs and the advertising market, Teladoc ultimately withdrew its full-year outlook for the BetterHelp business and recorded a goodwill impairment on this segment, which had been expected to generate $1 billion in revenue.

Affected by this, Teladoc’s senior management expects the year-over-year revenue growth rate for fiscal year 2024 to be below single digits. To avoid the potential risk of investor disappointment due to overly optimistic forecasts, the company has also chosen to withdraw its guidance for fiscal year 2024 and its business outlook for the next three years.

Of course,Teladoc Has Not Been Hit by Only Bad News. The Integrated Care segment, long serving as the “ballast,” saw its revenue rise 5% year over year to $377.4 million, while adjusted EBITDA surged nearly 70% to $64 million, both outperforming prior expectations.。

Teladoc has been working to integrate its internal business operations, aiming to enable customers to access a broader range of services through a one-stop solution, thereby driving an increase in average revenue per user. The performance of its Comprehensive Care segment in Q2 suggests that this strategy may be gaining traction.

Meanwhile,Its international business grew by 12%.. Therefore, Teladoc plans to make the development of its international business a key initiative to reverse its current situation, with non-English-speaking regions characterized by lower customer acquisition costs prioritized as target markets for expansion.

Furthermore,Teladoc is working to integrate BetterHelp into insurance reimbursement systems.——BetterHelp is expected to have the technical capability for insurance coverage by the end of this year, and will achieve insurance integration next year. Nevertheless, it may not be realistic to expect BetterHelp to return to its previous high growth and become the engine that drives Teladoc out of its predicament.

The Pioneer of Internet Healthcare Is Mired in Quagmire. Navigating Out Requires Both the New CEO’s Competence and a Bit of Luck.

Although the “pioneer” Teladoc has suffered significant losses, its revenue remains relatively stable, and its annual multi-billion-dollar scale is by no means small. In contrast, the revenue magnitude of Amwell (American Well), another publicly listed “pioneer” in internet healthcare that is frequently benchmarked against Teladoc within the industry, is not even in the same league.

In the Q2 financial report just released,Amwell reported quarterly revenue of $62.8 million, slightly lower than the $62.4 million in the same period last year, but still higher than the previous Q2 forecast ($61.1 million).. The net loss for the current quarter was $50 million, narrowing compared to Q1 (a loss of $73.4 million) and the same period last year (a loss of $93.5 million). Adjusted EBITDA loss amounted to $35 million, also lower than the previous quarter’s loss of $45.7 million.

For the entire first half of fiscal year 2024, Amwell generated $122 million in revenue, slightly below the $126 million recorded in the first half of fiscal 2023. However, its net loss for the six-month period decreased significantly to $124 million, far lower than the $492 million loss in the same period last year and also below the $134 million net loss reported in the prior-year period after excluding a $358 million goodwill impairment charge. This indicates that its cost-control strategies have begun to take effect.

After the release of the latest financial report,Amwell has raised its fiscal 2024 adjusted EBITDA guidance by $10 million, from a loss of $155–$160 million to a loss of $145–$150 million., but the projected revenue ($259–$269 million) and AMG telehealth visit volume (1.6–1.7 million) remained unchanged.

Prior to this, Amwell had just triggered a delisting warning from the U.S. Securities and Exchange Commission (SEC) because the average closing price of its common stock fell below the $1 threshold for 30 consecutive trading days.As a last resort, Amwell announced a reverse stock split in late June to bring its share price back into compliance with the $1 minimum average closing price requirement.。

A reverse stock split is a secondary market maneuver that proportionally increases the share price by consolidating existing shares into fewer shares. Similar to Amwell’s situation, avoiding delisting from exchanges is one of the most common reasons for this action. Although a reverse stock split generally does not affect a company’s market capitalization, it typically signals that the company is in distress and must address urgent financial challenges.

According to public information, Amwell’s reverse stock split ratio ranges from 1:10 to 1:20. This will significantly reduce the number of its outstanding shares to one-twentieth of the previous amount. Based on this reverse split ratio, the number of Class A common shares will decrease substantially from approximately 266 million to about 13.3 million, while the numbers of Class B and Class C common shares will be reduced proportionally to approximately 1.37 million and 280,000, respectively.

The share price increased to 20 times its pre-reverse-split level. Following the completion of the formal reverse stock split, the share price reached approximately $8, thereby meeting the minimum $1 average closing price requirement and temporarily averting the risk of delisting.

The good news is that,Amwell’s investments in technology over the past few years are gradually beginning to pay off.. In April 2021, Amwell launched the Converge telehealth platform, integrating all of Amwell’s proprietary products and third-party applications through a unified interface.

In layman's terms, this platform is more like an "app store for telemedicine," and such close collaboration can greatly enhance the user experience.

For instance, in August 2022, Amwell won the favor of CVS by helping the pharmaceutical giant build its online primary care services on the platform, with plans to integrate all service elements of the CVS ecosystem into a single platform offering a unified user experience.

According to the data disclosed by Amwell in this quarter’s earnings conference call,Converge’s patient satisfaction rate has exceeded 90%. Meanwhile, out of the 1.5 million visits this quarter, 70% originated from the Converge platform.。

In November 2023, Amwell secured a $180 million contract from the U.S. Defense Health Agency (DHA) to deploy its Converge platform, replacing existing video solutions within the U.S. military’s healthcare system. According to projections by Amwell’s senior management, the phased implementation of this project will enableAmwell’s gross margin reached 30% in fiscal year 2024 and further improved in fiscal year 2025, with the potential to reach 50%.。

Large healthcare groups have also expressed strong recognition for the Converge platform and have begun deploying it. For instance, Capital Blue Cross migrated to the Converge platform in Q2, a move that Amwell’s senior leadership hailed as “one of the most efficient and streamlined migrations to date.”

On the other hand, Amwell’s cost reductions are also noteworthy. In 2023,Amwell Cuts Workforce by 10% to Reduce Costs, Seen as Key to Improving Financial Outlook。

As these strategies are implemented, Amwell expects its financial position to gradually improve. However, this “pioneer” of telehealth may still need more good news.

Besides Teladoc and Amwell, several other companiesMajor tech companies that rushed into the internet healthcare sector in recent years have been scaling back or even shutting down their online medical services. The trend was particularly concentrated in April: UnitedHealth announced it would close its Optum online healthcare program; a few days later, Walmart announced it would shut down Walmart Health, which included its online medical services.。

The semi-annual financial reports of the few major companies still holding on are also quite dismal. For instance, although Walgreens’ Q2 revenue increased by 6.3% year-over-year to $37.1 billion, it recorded a staggering Q2 net loss of $5.9 billion due to a $5.8 billion goodwill impairment charge stemming from the poor performance of its acquisition, VillageMD—compared with a net income of $703 million in the same period last year.

In 2021, Walgreens became a major shareholder in VillageMD for $5.2 billion; less than two years later, it was already considering the full divestiture of this business.。

Amazon’s situation is similar. In 2022, it acquired One Medical for $3.9 billion, the third-highest acquisition price in its history. Although the holding period has been short, making it difficult to divest,Amazon’s first move at the start of 2024 was to cut costs at One Medical. In addition to eliminating hundreds of jobs, Amazon set a target for One Medical to reduce its fixed operating costs from 41% of total revenue to 20% by 2028, and also plans to significantly lower the cost per patient visit from $372 in 2023 to $322 in 2024.。

Internet-based healthcare experienced unprecedented growth during the COVID-19 pandemic, far exceeding expectations. To address the shortage of offline medical services during the outbreak, the U.S. government introduced a series of measures to promote telehealth, including temporary policies allowing reimbursement for internet-based medical consultations through insurance, as well as emergency approvals for remote healthcare interventions such as digital therapeutics.

Data from the U.S. National Center for Health Statistics show that, supported by flexibilities such as Medicare’s coverage of telehealth visits, the proportion of physicians using the internet surged during this period, rising from 15.4% in 2019 to 86.5% in 2021. This optimistic outlook also drew significant attention to internet-based healthcare in the United States at the time, with related venture capital investments tripling.

However, the good times did not last long.Since 2021, the use of telemedicine in the United States has shown an overall downward trend.According to Trilliant Health’s analysis in June, quarterly telehealth visits have declined from a peak of over 60 million in 2020 to fewer than 30 million in Q3 2023.

In addition,The insurance preferential policies established to expand internet healthcare during the pandemic are set to expire at the end of this year, and it remains uncertain whether they will be extended.。

Of course,Internet Healthcare Is Not All Bad News—Some Internet Healthcare Companies Focused on Niche Segments Are Rapidly Emerging。

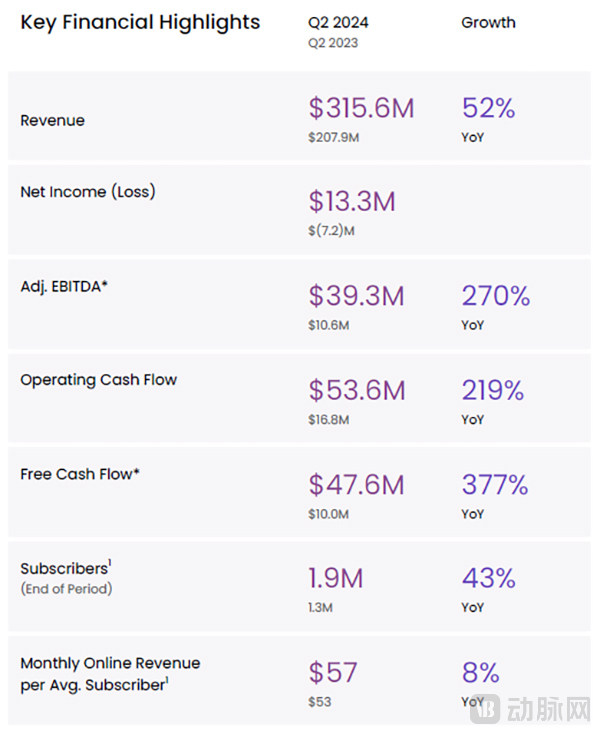

Hims & Hers has once again delivered a strong quarterly earnings report.The company reported Q2 revenue of $316 million, representing a 52% year-over-year increase from the $208 million recorded in Q2 of fiscal year 2023. Net profit reached $13.3 million, marking a significant turnaround from the net loss of $7.2 million in Q2 of fiscal year 2023.。

Its adjusted EBITDA for Q2 reached $39.3 million, with operating cash flow amounting to approximately $47.6 million, representing respective year-over-year increases of 270% and 377% compared to Q2 of fiscal year 2023—a remarkably impressive performance.。

Hims & Hers’ Q2 Earnings Report Is Quite Impressive (Screenshot from Hims & Hers’ Financial Report)

Meanwhile, as of Q2 FY2024, Hims & Hers’ subscriber base surged 43% year-over-year to 1.9 million, while the average revenue per user (ARPU) increased from $53 to $57.

Based on these positive data,Hims & Hers Raises Business Outlook Again, Lifts Full-Year 2024 Revenue Guidance to $1.37–$1.4 Billion and Adjusted EBITDA Guidance to $140–$155 Million. It is worth noting that only after the release of its Q1 financial report did Hims & Hers raise its full-year 2024 revenue guidance to $1.20–$1.23 billion and its adjusted EBITDA guidance to $120–$135 million.

In fiscal year 2023,Hims & Hers achieved revenue of up to $842 million, representing a 67% increase from the previous fiscal year’s revenue of $503 million.. This also exceeds the revenue forecast Hims & Hers provided in its fiscal 2022 annual report, when it projected 2023 revenue to be between $735 million and $755 million.

At present, Hims & Hers is poised to replicate its previous year’s success in fiscal year 2024.

What is particularly noteworthy is that, since the release of its performance forecast,The company’s actual revenue has exceeded the prior year’s forecasts for three consecutive years.. Clearly, even the company itself likely did not anticipate such rapid growth.From fiscal year 2018 to fiscal year 2023, its six-year revenue compound annual growth rate (CAGR) reached an astonishing 77.4%.。

After achieving success in the niche markets of hair loss and men’s health, Hims & Hers rapidly expanded its business model to other segments with similar characteristics, venturing into areas including women’s skincare, mental health, primary care, and obesity.

The obesity sector is a particular focus for expansion. In May, Hims & Hers announced it would add GLP-1 injectables to its weight-loss product bundle, described as containing “the same active ingredient as Novo Nordisk’s semaglutide (Ozempic and Wegovy).” However, its generic GLP-1 medication will cost only $199 per month, representing an 85% price reduction compared to Novo Nordisk’s semaglutide and Eli Lilly’s tirzepatide.

The company expects this to generate more than $100 million in revenue by the end of fiscal year 2025. Affected by this news, Hims & Hers’ stock price surged nearly 40% at its peak on the first trading day following the announcement, closing up 27.66%.。

Amid the escalating global obesity crisis, GLP-1 drugs, with their significant weight-loss efficacy, are becoming a new “gold mine.” Having previously succeeded in this therapeutic area, Hims & Hers has once again capitalized on this lucrative opportunity, underscoring the foresight of its leadership.

Talkspace, another internet healthcare company focused on mental health, also maintained its upward momentum, achieving revenue of $46 million in Q2, a year-on-year increase of 29%., with revenue from government payers, including Medicare, surging 62% to $30 million. Starting in May 2024, Talkspace has just announced that it will provide Talkspace services to Medicare customers nationwide by the end of the year.

In addition to the increase in revenue from government payers, direct-to-enterprise revenue also grew by 20% to approximately $10 million, further validating Talkspace’s strategic decision two years ago to pivot from a D2C to a B2B model.。

Securing government reimbursement contracts is no easy feat. Given that government insurance programs must serve millions of seniors aged 65 and older enrolled in qualified Medicare plans, Talkspace has made substantial investments in its infrastructure. These efforts include expanding its network of licensed, qualified providers and building out systems to meet Medicare’s reimbursement requirements.

Prior to this, Talkspace primarily operated under a B2C model.Similar to BetterHelp, Talkspace also went through a phase of high revenue and high expenditure. After weighing the pros and cons, Talkspace abandoned this model two years ago.. Currently, in its Q2 revenue, the direct-to-consumer business continued to decline by 29%, amounting to only $6.5 million.

Driven by revenue growth, Talkspace’s net loss narrowed from $4.7 million in Q2 FY2023 to $500,000, while adjusted EBITDA turned positive at $1.2 million, an improvement from the $4 million loss recorded a year earlier. Full-year revenue is projected to range between $185 million and $195 million, with adjusted EBITDA expected to be between $4 million and $8 million.

In fiscal year 2023, Talkspace’s revenue increased by 25% year over year, reaching $150 million. If the revenue forecast for fiscal year 2024 is realized, its revenue growth rate will once again reach this level.

Although not large in scale,This digital health upstart, which went public via a SPAC in 2021, is indeed set to achieve its first profit in the company’s 12-year history in 2024. Notably, Talkspace’s leadership has expressed satisfaction with its “small but beautiful” strategy, stating that mergers and acquisitions are not necessary to drive growth.Instead, the board will implement a stock repurchase program of up to $15 million over the next two years to boost the share price.

Clearly, as traditional telehealth companies like Teladoc and Amwell decline, new entrants such as Hims & Hers and Talkspace are quietly rising by strategically selecting and focusing on promising niche markets.

Not only is internet healthcare in the United States undergoing adjustments, but China’s internet healthcare industry is facing similar changes.

Certainly, the empowering role of internet healthcare in the medical field is beyond doubt. As internet healthcare has gradually permeated the entire medical process in recent years, both patients and doctors have tangibly experienced the convenience brought by internet technology. However, it must also be acknowledged that internet healthcare still requires further technological revolution to break through the current bottlenecks. Advances in AI and digital therapeutics may well represent the future that internet healthcare needs.

Although tech giants have underperformed, some emerging and distinctive internet healthcare models are quietly taking root. Adhering to a specialized, “small but beautiful” approach may well have a promising future, representing a potential pathway for development. Given time, these “small but beautiful” entities could grow into towering trees.

How Internet Healthcare Will Evolve in the Future: Let’s Wait and See.

References:

Heather Landi,fiercehealthcare.com:How the virtual care market is shaking out in 2024 as Walmart, Optum exit the telehealth business

Caroline Catherman,Healthcare Brew:Telehealth takes a tumble, but experts say the fight isn’t over

Heather Landi,fiercehealthcare.com:Walgreens may sell entire stake in VillageMD business as it explores strategic options