Yinoi Bio Becomes the First Pharmaceutical Company to List on STAR Market in 2024

After a prolonged wait, Yinuosi Bio made its debut on the SSE STAR Market today, becoming the first pharmaceutical company to complete an initial public offering (IPO) on the board since 2024. Yinuosi’s core business involves providing outsourced non-clinical safety evaluation services for new drug development in China, ranking third in market share within this specialized sector.

With this, following the successive listings of the three major domestic laboratory mouse companies on the capital market, the top three enterprises in China’s large laboratory animal sector have also gone public, further maturing the new drug development industry chain. However, at a time when small domestic CROs are struggling to secure orders and facing idle capacity, while large CROs are experiencing successive collapses in performance, whether Yinuosi’s IPO can restore confidence in the industry remains to be seen.

Star CRO Goes Public

Founded in 2010, Yinuosi was not among the earliest participants in China’s CRO market. For a long period after its establishment, Yinuosi focused intensively on niche verticals, remaining merely one of many small yet specialized CROs in China. Its brand influence and operational scale were far inferior to those of industry leaders such as WuXi AppTec and Pharmaron, which were established earlier.

The turning point came in 2021, when the sector in which Shanghai Yinuosi Bio-Technology Co., Ltd. operates was heated up by a surge in demand for laboratory non-human primates.

Starting in the second half of 2020, the supply-demand balance for laboratory non-human primates (such as cynomolgus monkeys and rhesus macaques) tightened sharply due to the widespread development of COVID-19 vaccines and neutralizing antibodies. Public data indicate that domestic demand for laboratory monkeys reached 40,000 in 2020, with up to 6,000 used for COVID-19 vaccine and drug research and development, accounting for approximately 20% of China’s annual historical usage of laboratory monkeys. Under pandemic control measures, import channels for laboratory monkeys were temporarily closed, placing pressure on existing domestic monkey resources and driving procurement prices significantly higher. Since 2020, the purchase price of cynomolgus monkeys has risen from RMB 20,000 per animal to around RMB 70,000 per animal. By the end of the first quarter of 2022, the price of cynomolgus monkeys had further increased to approximately RMB 150,000 per animal.

In new drug development, experimental monkeys are a critical raw material for non-clinical safety evaluation.Non-clinical safety evaluation, commonly referred to as “safety assessment,” is a critical and mandatory step in the new drug development process. Only after comprehensive safety has been evaluated through a series of in vivo and in vitro animal studies can a candidate drug apply for an Investigational New Drug (IND) application to enter clinical trials, or submit a New Drug Application (NDA)/Biologics License Application (BLA) for market approval. In practice, non-clinical safety evaluation comprises a series of complex studies, which can be broadly categorized into safety pharmacology studies, single-dose toxicity studies, repeat-dose toxicity studies, reproductive toxicity studies, genotoxicity studies, carcinogenicity studies, local tolerance studies, dependence studies, immunogenicity studies, immunotoxicity studies, and toxicokinetic studies. Cynomolgus monkeys are involved in multiple toxicological and pharmacological evaluation studies within this process.

Typically, the outsourcing rate for safety assessment is very high. Regulatory authorities in various countries impose stringent requirements on drug safety studies; only results from drug safety evaluations conducted by research institutions that possess Good Laboratory Practice (GLP) certification or have passed GLP inspections are accepted and recognized. Furthermore, due to the long construction cycle for GLP laboratories, the cumbersome certification process, and the high capital expenditure required for related experimental instruments and facilities, virtually no pharmaceutical companies in China have established their own GLP laboratories. According to Patheon statistics, the outsourcing penetration rate for pharmacology and toxicology assessments reaches 70% across all stages of drug development, whereas most other stages remain below 50%.

In this context, CRO companies providing safety assessment services that directly control experimental monkey resources are overwhelmed with orders.Previously, Joinn Laboratories stated in its financial reports that possessing primate animal model resources or technology would secure market initiative and could even be monopolized as a strategic resource. CRO companies such as WuXi AppTec and Pharmaron have acquired cynomolgus monkey breeding bases to stockpile larger numbers of experimental monkeys. Consequently, non-clinical safety assessment CRO projects have become highly sought-after in the primary market, attracting significant capital inflows into this sector. Shanghai Yinuosi Bio-Technology Co., Ltd. has accordingly emerged as a new star project among CROs.

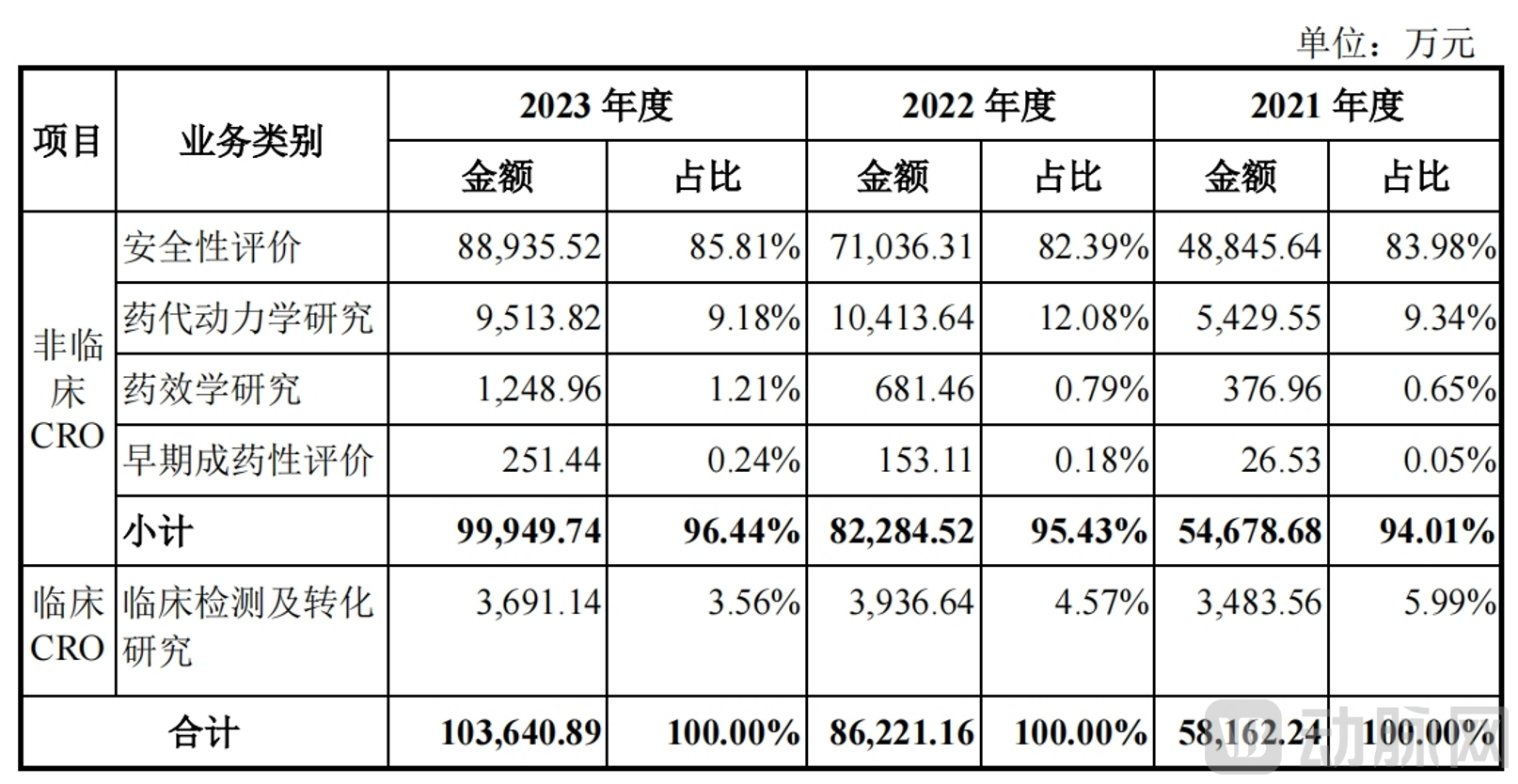

Revenue Structure of Yinuosi Data Source: Prospectus

Safety assessment services have always been the core component of Shanghai Yinuosi Bio-Technology Co., Ltd.’s business portfolio, accounting for approximately 80% of its revenue.According to the prospectus, Yinuosi is one of the earliest domestic companies to simultaneously hold NMPA GLP certification, OECD GLP certification, and pass FDA GLP inspections. It has established a key technology platform for evaluating the immunogenicity and immunotoxicity of antibody-based drugs and antibody-drug conjugates (ADCs). Information from the prospectus indicates that among domestic safety assessment CROs, Yinuosi offers the most diverse range of test types and holds the highest number of NMPA GLP certifications, giving it a competitive advantage in securing orders.

Composition of Safety Assessment Services Across CROs Data Source: Prospectus

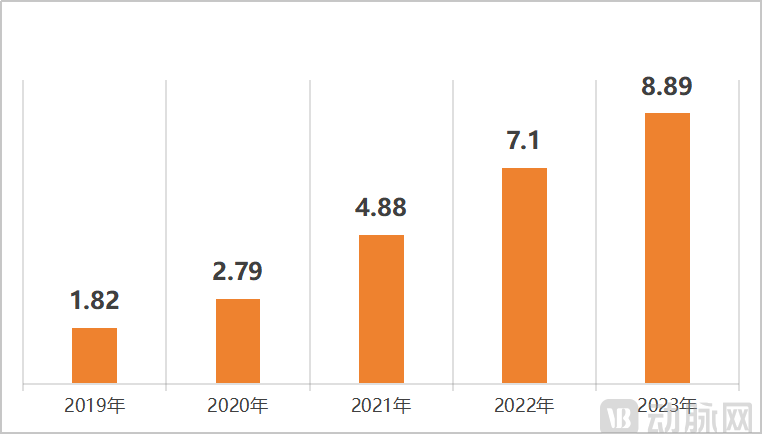

In recent years, Yinuosi’s revenue from safety assessment services has grown rapidly, increasing from RMB 182 million in 2019 to RMB 889 million in 2023, representing a nearly 400% increase. Notably, during 2021 and 2022, when the market for experimental monkeys was at its peak, this segment of Yinuosi’s business achieved growth rates exceeding 40% in both years.

2019–2023 Yinuosi Safety Assessment Business Revenue Data Source: Prospectus

In 2022, Yinuosi ranked third in China’s niche market for drug safety assessment, trailing only WuXi AppTec and Joinn Laboratories, with a market share of 6.8%. In the same year, Yinuosi submitted its IPO application to the STAR Market and became the first among its peers to list on the capital market, thereby securing the commercial gains driven by the surge in demand for laboratory monkeys. In February 2024, Tianqin Biology, another CRO company that rose to prominence amid the laboratory monkey boom, had its filing for pre-IPO tutoring accepted, further intensifying competition in this specialized sector of drug safety assessment.

Collapse of Orders and Prices

The industry's bonus period is always short-lived.

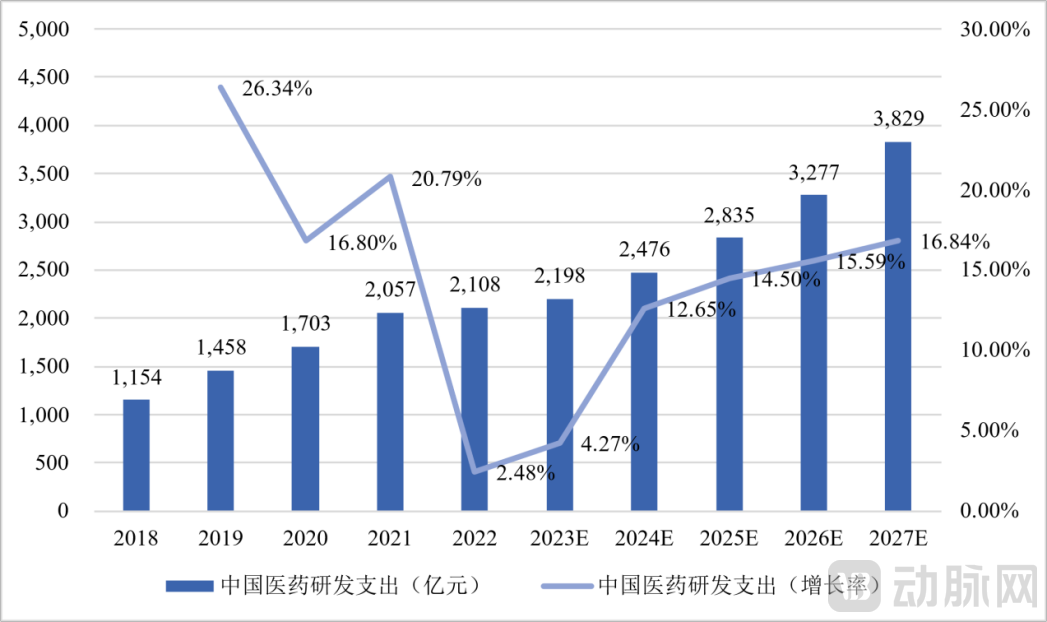

Starting in the second half of 2022, financing for innovative drugs in China slowed down, and corresponding pharmaceutical R&D expenditures shrank sharply.According to Frost & Sullivan, in 2022, the growth rate of domestic pharmaceutical R&D expenditure plummeted from the previous year’s high of 20.79% to 2.48%, nearly coming to a standstill. The direct consequence was that the number of new drug clinical trial applications accepted by the National Medical Products Administration (NMPA) experienced its first year-on-year decline since 2017, decreasing by approximately 7% compared to the prior year. As increases in pharmaceutical R&D spending and the initiation of new drug trials are the primary sources of CRO orders, the signal of market cooling quickly transmitted upstream to CROs, resulting in a sharp drop in order volumes.

Domestic Pharmaceutical R&D Expenditure Since 2018 Data Source: Frost & Sullivan

Previously, industry media described the current CRO market as being in a “halftime break.” Practitioners told the media that in the second half of 2022, one-quarter of projects were shut down within a single week. By February 2023, half of all orders had been lost. Projects still underway were largely based on contracts signed in 2020 and 2021; although clients had executed contracts for 2022 projects, nearly all of them were terminated. In earlier years, companies could still secure large deals worth tens of millions of yuan, but starting in 2023, these shrank entirely to smaller contracts in the generic drug sector valued at only a few million yuan, while rumors of layoffs spread rapidly.

Judging from the financial results announced by major domestic CROs, the industry’s contraction continues.Revenue and net profit across the industry have all experienced negative growth to varying degrees. As of press time, Joinn Laboratories has not yet released its official interim financial report for the first half of 2024; however, based on its earnings forecast, the company is set to report its first semi-annual net loss in years. In its previously announced Q1 2024 report, Joinn Laboratories recorded losses of approximately RMB 280 million in both net profit and net profit excluding non-recurring items. Nevertheless, in its interim report, Pharmaron noted that in the second quarter of 2024, alongside an initial recovery in global biopharmaceutical industry financing and investment, the volume of inquiries and visits from its global clients had begun to rebound compared to the same period in 2023, with the value of newly signed orders increasing by more than 15% year-on-year.

Performance Data of Selected Listed CROs Source: Company Financial Reports

Amid a sharp decline in demand, domestic CROs are slashing prices significantly to secure orders.Gross Margins Decline at WuXi AppTec and Pharmaron. Amid the price-cutting battle for CRO orders, Shanghai Yinuosi Bio-Technology Co., Ltd. (Yinuosi), which is preparing for its initial public offering, has undoubtedly adopted a highly aggressive stance. In its prospectus, Yinuosi stated that factors such as intensified competition in China’s CRO industry and declining prices for laboratory non-human primates since the second half of 2023 have led to a decrease in the pricing of its newly signed orders, directly resulting in an 8.11% year-on-year decline in gross margin for the first quarter of 2024. Nevertheless, Yinuosi did not relax its efforts to secure orders during this period; its revenue scale increased by 17.12% year on year, particularly with an expanded share in China’s safety assessment market, which is expected to continue growing throughout 2024. Yinuosi projects that its net profit attributable to shareholders of the parent company, after deducting non-recurring gains and losses, will decline by less than 20% in 2024 compared with 2023.

As professional service providers, CROs’ ability to secure and retain contracts is heavily influenced by their brand reputation and project experience. In a market environment where even leading enterprises continue to face sustained pressure, the numerous long-tail CROs find survival increasingly difficult. How to survive during a contracting market cycle, or even achieve exponential business growth, tests the wisdom of CRO executives.

M&A: Paving the Way to a Brighter Future?

Undeniably, although the exciting upward momentum was fleeting, China’s more mature new drug R&D industry chain has solidified.

In the global pharmaceutical market, a mature industrial chain ecosystem has made significant contributions to improving the efficiency of drug development, manufacturing, and sales for pharmaceutical companies. Behind multinational pharmaceutical corporations often stand one or more powerful CROs and CDMOs, with both parties sharing the substantial commercial value generated by blockbuster drugs. Data shows that leading global CROs such as LabCorp, IQVIA, Charles River, and WuXi AppTec have average annual revenues exceeding USD 3 billion.

In China’s CRO market, even though Shanghai Yinuosi Bio-Technology Co., Ltd. has ranked among the top three in the niche segment of safety assessment, its overall market share is only slightly above 1%. For CRO companies, excellence in any single domain is insufficient to create customer stickiness. Only by offering a sufficiently long chain of outsourced services can they establish long-term, stable relationships with their client base and thereby secure continuous orders. In this sense, despite its successful listing on the STAR Market, Yinuosi still has a long way to go.

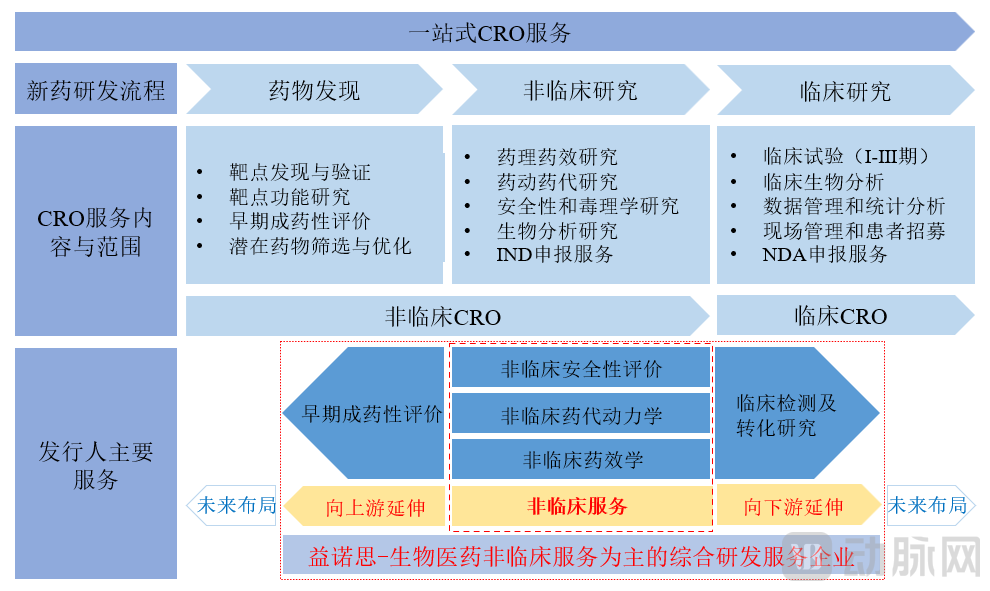

In fact, Shanghai Yinuosi Bio-Technology Co., Ltd. has been striving to extend the chain of outsourced services it offers.Around 2017, Shanghai Yinuosi Bio-Technology Co., Ltd. (Yinuosi) began to expand its service portfolio beyond safety assessment to include non-clinical pharmacokinetic and pharmacodynamic evaluations. Since then, these three services have often been complementary in the orders secured by Yinuosi. For instance, Yinuosi was previously commissioned by Baili Tianheng to conduct non-clinical pharmacokinetic studies and non-clinical safety assessments for the BL-B01D1 project. This asset became the subject of the largest transaction during the 2023 wave of cross-border business development (BD) deals for new drugs. According to incomplete statistics, Yinuosi has supported more than 20 products in their global expansion efforts, with over 90% being innovative drugs.

Yinuosi’s Business Structure Data Source: Prospectus

Since 2021, Shanghai Yinuosi Bio-Technology Co., Ltd. has accelerated its efforts to refine its business value chain, successively adding services such as early-stage druggability assessment, clinical testing, and translational research.Specifically, early-stage drug developability assessment is a research process within the early drug discovery phase of drug development. It involves conducting early pharmacodynamic studies, as well as evaluating pharmacokinetic properties and safety profiles of lead molecules, to preliminarily assess whether these active compounds possess the potential to be ultimately developed into drugs.

At this stage, Shanghai Yinuosi Bio-Technology Co., Ltd. has established platforms for early-stage in vivo and in vitro pharmacodynamics as well as early-stage pharmacokinetics research. Meanwhile, it is capable of conducting multiple rapid prediction and screening models for early toxicity, including genotoxicity prediction models, high-throughput genetic toxicity evaluation and screening models, in vitro cardiotoxicity evaluation and screening models, in vitro carcinogenicity evaluation models, and high-throughput reproductive and developmental toxicity evaluation and screening models. In addition, Yinuosi’s clinical testing and translational research services primarily involve researching and establishing analytical methodologies for test drugs and biomarkers, thereby providing analytical methods and data support for clinical pharmacokinetic, pharmacodynamic, and safety studies of innovative drug projects. From an operational perspective, the cash flow generated by these newly extended business lines has already reached a significant scale and is growing rapidly.

Regarding its future, Yinuosi stated that it aims to evolve into a high-quality, one-stop comprehensive evaluation service platform for innovative drugs, providing pharmaceutical companies with complete CRO services ranging from animal resources, druggability studies, pharmacodynamics, pharmacokinetics, and safety assessment to clinical trials and new drug registration applications. However, time is running out for Yinuosi. In the somewhat crowded CRO sector, leading enterprises have already gone further in offering one-stop services. New drug development is a complex systematic engineering project; relying entirely on in-house capabilities to overcome the service difficulties and technical barriers at each stage—drug discovery, non-clinical, and clinical—is clearly not feasible within the available timeframe. How to build sufficient outsourcing service capacity during a period of shrinking order volumes, thereby avoiding elimination by competitors, remains a common concern for many CROs.

Historically, the CRO industry has frequently experienced waves of mergers and acquisitions (M&A) following cyclical fluctuations. Through the accumulation of business capabilities and client orders, leading CRO companies have emerged during this process. Representative M&A transactions include WIL Research with Charles River Laboratories, Aptiv Solutions with ICON, Covance with LabCorp, Chiltern with LabCorp, and Quintiles with IMS Health. The most recent significant M&A activities in the CRO sector occurred in 2021, when ICON acquired PRA Health Sciences for $12 billion, and Thermo Fisher Scientific completed its acquisition of PPD. Following these consolidations, LabCorp and IQVIA have firmly established their leadership positions in the global CRO industry, with Thermo Fisher Scientific and ICON closely trailing. Global CROs have enhanced industry concentration through M&A and integration, resulting in an increasingly clear competitive landscape.

In China, leading CROs are also expanding their business chains through mergers and acquisitions. For instance, WuXi AppTec’s clinical research and SMO services, as well as its drug safety evaluation operations conducted by Suzhou WuXi AppTec New Drug Development, were both acquired through industry M&A. Joinn Laboratories has also acquired monkey breeding facilities to secure the supply of experimental monkeys required for its safety assessment services. Currently, a large number of CROs are facing idle capacity due to an inability to secure orders, resulting in tight cash flow, and the industry is quietly undergoing another round of consolidation.

For Yinuosi and many other CROs struggling to survive, strengthening competitiveness through appropriate product acquisitions, securing advantageous orders, and even winning new ones may be a viable strategy to address current challenges. If the funds raised from its IPO enable Yinuosi to pursue mergers and acquisitions, it would undoubtedly bolster confidence in the industry.

Writing Reference:

The Prospectus submitted by Yinuosi on each occasion;

WuXi AppTec, Pharmaron, and Joinn Laboratories disclose their H1 2024 financial reports or forecasts;

Deep Blue View: The Halftime Break for CROs—Left or Right?