Innovative Chinese Pharma Finds New Cash Flow: BD Deals Surpass $20 Billion in H1

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Recently, Hengrui Pharma released its semi-annual report: In the first half of 2024, it achieved a revenue of RMB 13.6 billion, a year-on-year increase of 21.78%; the net profit attributable to shareholders of the listed company was RMB 3.432 billion, a year-on-year increase of 48.67%.In this best-ever semi-annual report, the most discussed topic in the industry is Hengrui Pharma’s confirmation of an overseas business development (BD) revenue: in the first half of the year, Hengrui received a €160 million upfront payment from Merck for its PARP1 inhibitor, HRS-1167.。

This is merely the tip of the iceberg. In 2023, Hengrui Pharma secured five overseas licensing deals, totaling more than $4 billion. In addition to the PARP1 inhibitor HRS-1167, the portfolio included the EZH2 inhibitor SHR2554, the TSLP monoclonal antibody SHR-1905, the HER1/HER2/HER4-targeted drug pyrotinib maleate, and the Claudin-18.2 ADC SHR-A1904. Judging from the semi-annual report, business development (BD) revenue has clearly become a key driver of Hengrui’s performance growth.

In fact, Hengrui Pharma is not the only company to have successfully turned its fortunes around through business development (BD) income; Ascentage Pharma, Baili Tianheng, and Kelun-Biotech also reaped performance benefits from BD deals in the first half of the year. Taking Ascentage Pharma as an example, the company achieved revenue of RMB 824 million in the first half of 2024, a year-on-year increase of 477%, with net profit reaching RMB 163 million, marking its first return to profitability. This turnaround was largely driven by a substantial income item: on June 14, Ascentage Pharma licensed the global rights to olverembatinib, excluding the Greater China region, to Takeda, receiving an upfront payment of $100 million. Similarly, Baili Tianheng saw its first-half revenue surge 17-fold, primarily due to an $800 million upfront payment from Bristol Myers Squibb (BMS) under the collaboration agreement for BL-B01D1.

And as one substantial revenue stream after another is recorded in the semi-annual reports, an objective fact is being presented to the industry:In the Current Climate of Increasingly Difficult Monetization, Innovative Drugs Seem to Be Relying on Business Development (BD) to “Sustain Their Lifeline”。

BD: A Gold Mine Poised for Explosive Growth

It is reported that the total value of a business development (BD) deal is typically broken down into several components, including upfront payments, milestone payments, commercial milestone payments, and sales royalties. The only amount pharmaceutical companies are guaranteed to receive is the upfront payment; other payments are contingent upon subsequent R&D progress and market performance. Nevertheless, even the upfront payment represents a significant source of revenue for pharmaceutical companies.

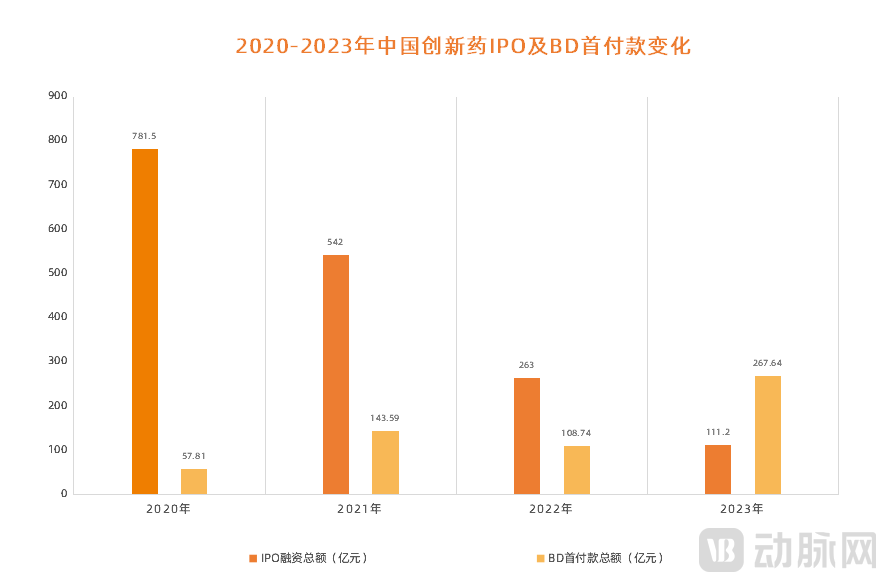

Figure 1. Changes in IPOs and Upfront Payments for Business Development Deals of Innovative Drugs in China, 2020–2023 (Data source: PharmaCube)

Figure 1. Changes in IPOs and Upfront Payments for Business Development Deals of Innovative Drugs in China, 2020–2023 (Data source: PharmaCube)

According to statistics from PharmCube,In 2023, the total upfront payments received by Chinese innovative drug companies through business development (BD) deals reached RMB 26.764 billion, surpassing for the first time the total funds raised through initial public offerings (IPOs), and amounting to nearly twice the latter.This is undoubtedly an astonishing figure, given that the upfront payments for business development (BD) deals involving Chinese innovative drugs amounted to only RMB 5.781 billion in 2020, representing a nearly four-fold surge within just three years. Into 2024, this metric has continued its rapid ascent. According to incomplete statistics from Frost & Sullivan, there were 34 license-out transactions in China’s innovative drug sector in the first half of 2024 (H1), with the upfront payments for the top 10 deals totaling USD 720 million, already approaching the full-year levels of the previous two years.

This is attributable to the continuous surge in large-scale business development (BD) deals. In fact, four blockbuster transactions occurred within the first four days of 2024: AstraZeneca licensed AnRay Biologics’ EGFR L858R inhibitor; Ylian Therapeutics entered into a global collaboration and license agreement with Roche for the YL211 program; Galapagos signed a collaboration agreement with Qiaoji Biopharma on specific oncology targets; and Avenzo acquired the global (excluding Greater China) development and commercialization rights to AnRay Biologics’ CDK2 inhibitor, ARTS-021. Reportedly, the total value of these four BD deals exceeded $3.5 billion, with upfront payments nearing $200 million.

Since then, business development (BD) activities have surged, driving transaction values to new heights. For instance, in the aforementioned collaboration between Ascentage Pharma and Takeda, the agreement stipulates that Ascentage will receive “a $100 million option fee, up to approximately $1.2 billion in potential option and milestone payments, and double-digit royalty rates,” setting a record for the highest BD deal value for a domestically developed small-molecule oncology drug. Additionally, Merck & Co. recently announced a final agreement with Tongrun Bio for the global rights to the novel bispecific antibody CN201. The total transaction value is estimated at $1.3 billion, including an upfront payment of $700 million—the second-highest upfront payment for a Chinese innovative drug after Baili Tianheng.

According to incomplete statistics,The top 10 MNCs have already paid $7.2 billion in upfront payments for Chinese innovative drugs, with total transaction values reaching $45 billion.Although upfront payments still constitute the majority of funds received by pharmaceutical companies at this stage, subsequent payments have been gradually arriving this year. Taking Ascentage Pharma as an example, in mid-August, the company received RMB 720 million in option payments and RMB 540 million in equity investment from Takeda. In addition, companies including Kelun Pharmaceutical, Harbour BioMed, and Bio-Thera Solutions have all received milestone payments amounting to tens of millions of U.S. dollars this year.

And this is just the beginning; revenue generated from business development (BD) activities is expected to continue expanding. Taking olverembatinib as an example, as a potential “blockbuster” molecule with peak sales estimated at $1–1.5 billion, Ascentage Pharma could receive annual net royalty income of $150–225 million without deploying its own sales force, assuming a median royalty rate of 15%. Over the drug’s lifecycle, cumulative royalty payments are projected to exceed $2 billion.

Additionally, HRS-1167, a second-generation PARP inhibitor, holds significant potential as both a monotherapy and combination therapy for a broader patient population, including those with tumors previously ineligible for PARP inhibitor treatment, owing to its high selectivity and potency. Currently, no comparable products have been approved for marketing either in China or internationally, indicating substantial market potential. Under the agreement, Hengrui Pharma will receive sales royalties from Merck at a high double-digit percentage rate, amounting to hundreds of millions of euros annually.

Therefore, from the current perspective, BD (Business Development) revenue has not only become a crucial support for pharmaceutical companies to turn losses into profits and address funding shortages, but it will also serve as a potential driver for their future performance growth.

The Truth Behind BD: “Revenge Deals” in the Winter Chill

As a type of transaction, business development (BD) inevitably involves both buyers and sellers. In the current market, buyers are primarily multinational corporations (MNCs), while sellers are mainly domestic innovative pharmaceutical companies. From different perspectives, what subtle changes in the pharmaceutical industry can we observe?

From the perspective of buyers, namely multinational corporations (MNCs). On this matter, an industry expert remarked, “In recent years, MNCs have begun to closely monitor innovative drugs in China and have become the largest buyers,”A significant factor is the pressure on performance growth imposed by the approaching patent cliff.“...and through BD of innovative drugs in China, it can not only drive performance growth but also maintain its market position.” This clearly indicates that Chinese innovative drugs are gaining widespread recognition from multinational corporations (MNCs), with a significant enhancement in their innovation capabilities.

Specifically, take the landmark business development (BD) deal between Ascentage Pharma and Takeda as an example. It is reported that although Takeda holds ponatinib, the world’s first third-generation BCR-ABL inhibitor, its commercial performance has been lackluster due to safety concerns. Furthermore, with its patent set to expire around 2026, Takeda has gradually lost ground in its competition with Novartis’s asciminib. Consequently, Takeda quickly turned its attention to olverembatinib. This move is driven not only by the expectation that olverembatinib, scheduled for U.S. launch in 2026, will seamlessly succeed ponatinib upon patent expiration, but more importantly, by olverembatinib’s clear generational advantage over first- and second-generation BCR-ABL inhibitors. It remains effective in chronic myeloid leukemia (CML) patients who are resistant to or have failed treatments such as asciminib, while also offering a significantly improved safety profile. Following this BD transaction, Takeda is now well-positioned to compete head-on with Novartis and further solidify its dominance in the CML market.

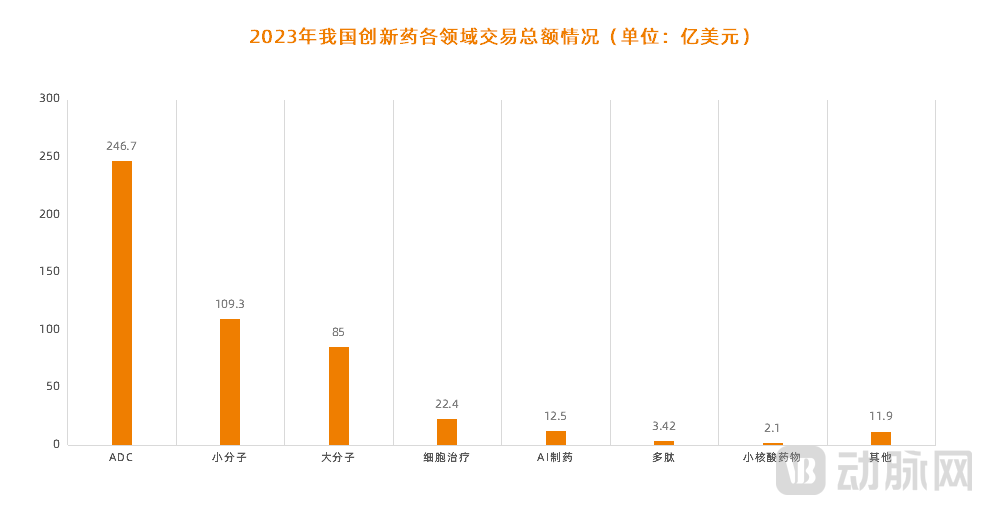

Figure 2. Total Transaction Value of Innovative Drugs Across Various Fields in China in 2023 (Data Source: “2023 BD Report on Chinese Pharmaceutical Companies”)

The second trend focuses on specific sectors; in terms of transaction volume,Bispecific antibody pipelines are increasingly poised to replace ADCs as the most closely watched frontier assets among multinational corporations (MNCs).In December 2023, BL-B01D1, an antibody-drug conjugate (ADC) developed by Baili Tianheng, was licensed out to Bristol-Myers Squibb in a deal worth up to $8.3 billion. This transaction not only set a new record for the highest upfront payment in a Chinese innovative drug license-out deal but also broke the global record for the total value of a single-agent ADC transaction. In fact, throughout 2023, license-out deals for Chinese-made ADCs emerged one after another, a trend corroborated by data: the total value of such transactions reached $24.67 billion in 2023, accounting for nearly half of the year’s overall transaction volume.

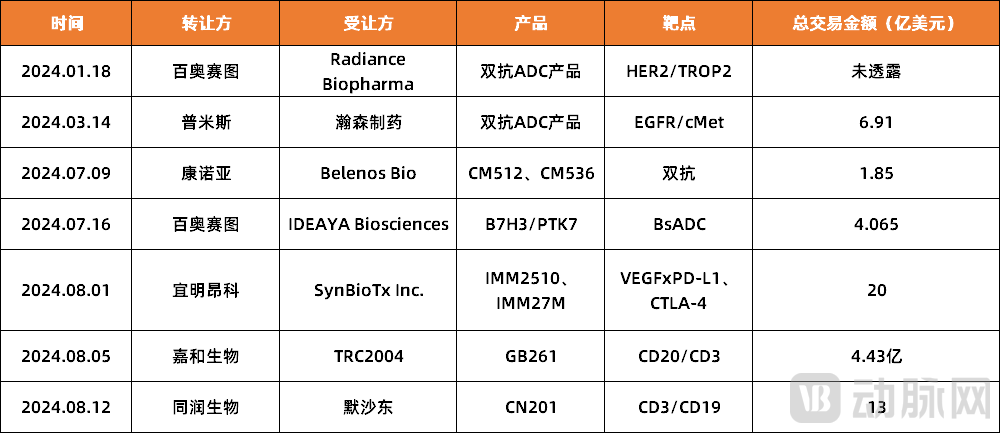

Figure 3. Overview of Business Development Deals for Bispecific Antibody Pipelines in China, 2024 (Source: Public Information)

Figure 3. Overview of Business Development Deals for Bispecific Antibody Pipelines in China, 2024 (Source: Public Information)

However, in 2024, the trend appears to have shifted. Since the beginning of this year, seven domestic pharmaceutical companies have completed licensing deals for bispecific antibody drugs. In particular, since the second half of the year, Chinese-made bispecific antibodies have seen a surge in overseas expansion. Recently, companies including Keymed Biosciences, ImmuneOnco, Genor Biopharma, and Tongrun Biopharmaceuticals have all achieved intensive international market entry, mirroring the frenzy of multinational corporations (MNCs) acquiring Chinese ADC assets over the past two years.

In this regard, an industry expert remarked, “Shifts in business development (BD) strategy are essentially no different from investment decisions: capital always flows toward the most advanced technologies and the most profitable opportunities. The fervent betting on antibody-drug conjugates (ADCs) over the past two years was driven by their significant potential in treating various types of cancer and their broad market prospects. Starting this year, greater attention is being paid to bispecific antibodies, primarily because they have been proven to not only perform exceptionally well in oncology but also hold commercialization potential in non-oncology fields.”

So, from the seller’s perspective—that is, from the standpoint of domestic innovative drug companies—what can we observe?

The first point is a shift in R&D thinking.No longer blindly pursuing “complete success,” but instead focusing more on cash flow. In this regard, the founder of a pharmaceutical company remarked, “In the current market winter, the odds of successfully bringing a drug from R&D to market, building an in-house sales team, and then competing effectively are now exceedingly slim.Therefore, as it becomes increasingly difficult to balance R&D investment with revenue, the industry is gradually embracing the “R&D–License–M&A (mergers and acquisitions)” pathway, after all, maintaining cash flow is essential for survival. Consequently, over the past one to two years, pharmaceutical companies have been aggressively recruiting business development (BD) professionals, with the clear objective of accelerating cash flow conversion.

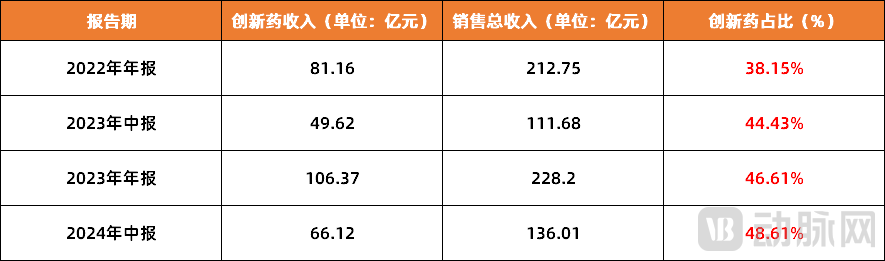

Figure 4. Revenue from Hengrui Pharma’s Innovative Drugs and Its Proportion, 2022–2024 (Source: Hengrui Pharma Annual Reports)

Figure 4. Revenue from Hengrui Pharma’s Innovative Drugs and Its Proportion, 2022–2024 (Source: Hengrui Pharma Annual Reports)

Secondly, we will discuss the transformation of pharmaceutical companies.As BD Revenue Begins to Drive Pharmaceutical Companies’ Growth, the Growing Pains of Innovation-Led Transformation Are Gradually EasingTaking Hengrui Pharma as an example, its revenue from innovative drugs reached RMB 6.612 billion in the first half of 2024. When including the EUR 160 million upfront payment from Merck for out-licensing deals that has been recognized as revenue, the proportion of Hengrui’s revenue derived from innovative drugs exceeded 50%. This indicates that Hengrui is accelerating its transition from a traditional pharmaceutical company to an innovation-driven enterprise. In fact, over the past few years, affected by the centralized volume-based procurement of generic drugs, Hengrui’s revenue and net profit attributable to shareholders declined consecutively, while its market capitalization plummeted by nearly RMB 100 billion. However, data from the first half of this year show that both revenue and profits have returned to peak levels, suggesting that Hengrui is gradually emerging from the growing pains associated with its transformation toward innovative drugs.

Of course, Hengrui Pharma is not the only company to have successfully transitioned from generic drugs to innovative medicines; Biocytogen, Kelun-Biotech, and Chia Tai Tianqing have achieved similar success. However, unlike Hengrui’s all-in strategy on innovative drugs, Biocytogen has adopted a model of “using generics to fund innovation,” Kelun-Biotech established a dedicated subsidiary for innovative drug development, and Chia Tai Tianqing has increased its investment in innovative medicines through asset acquisitions. Although their approaches differ, the current results indicate that their transformation processes are accelerating and entering a harvest period.

Finally, globalization deserves mention. As business development (BD) activities heat up, Chinese pharmaceutical companies have found new approaches to expanding overseas. In recent years, “going global” has become a keyword across the entire pharmaceutical sector, largely driven by market considerations, given that international expansion offers greater profit potential. However, for Chinese pharmaceutical companies, how to go global remains a major challenge. On one hand, there is a general lack of understanding of the global market; on the other, concerns persist about the uncertainty of performance outcomes.

From the current perspective,BD appears to be a promising strategy for global expansion.. In this regard, a senior investor remarked, “By leveraging business development (BD), domestic pharmaceutical companies can not only rapidly generate profits through the market channels of multinational corporations (MNCs), but also accelerate their understanding of overseas markets and uncover more potential opportunities. Looking further ahead,”Amidst the fierce global competition for innovative drugs, business development (BD) is undoubtedly an essential preparation for engaging in head-to-head competition with biopharma companies.”。

Take Legend Biotech as an example. In December 2017, Legend Biotech entered into an exclusive global license and collaboration agreement with Johnson & Johnson for its CAR-T product, ciltacabtagene autoleucel. Leveraging J&J’s robust R&D and commercial capabilities, ciltacabtagene autoleucel rapidly secured FDA approval and achieved $133 million in sales within its first year on the market. By 2023, annual sales of ciltacabtagene autoleucel surged to $500 million, with expectations to surpass the $1 billion mark in 2024. Bolstered by this deal, Legend Biotech not only created a market capitalization legend worth hundreds of billions of yuan but also established a firm foothold in the U.S. market, listing on the Nasdaq in 2020.

Therefore, there is no doubt that business development (BD) currently plays a crucial role in the entire pharmaceutical market, transcending economic cycles. On one hand, multinational corporations (MNCs) can leverage BD to expand their businesses and identify new growth drivers; on the other hand, domestic pharmaceutical companies can secure cash flow and accelerate their transition toward innovative drug development. As demand from both buyers and sellers intensifies, transaction activity naturally becomes more robust.

Support BD, but don't rely on BD alone

Every coin has two sides, and business development (BD) is no exception. Although BD has served as a supplementary force sustaining the continued advancement of China’s innovative drug sector during the capital winter of the past one to two years, it should still be viewed with rationality.

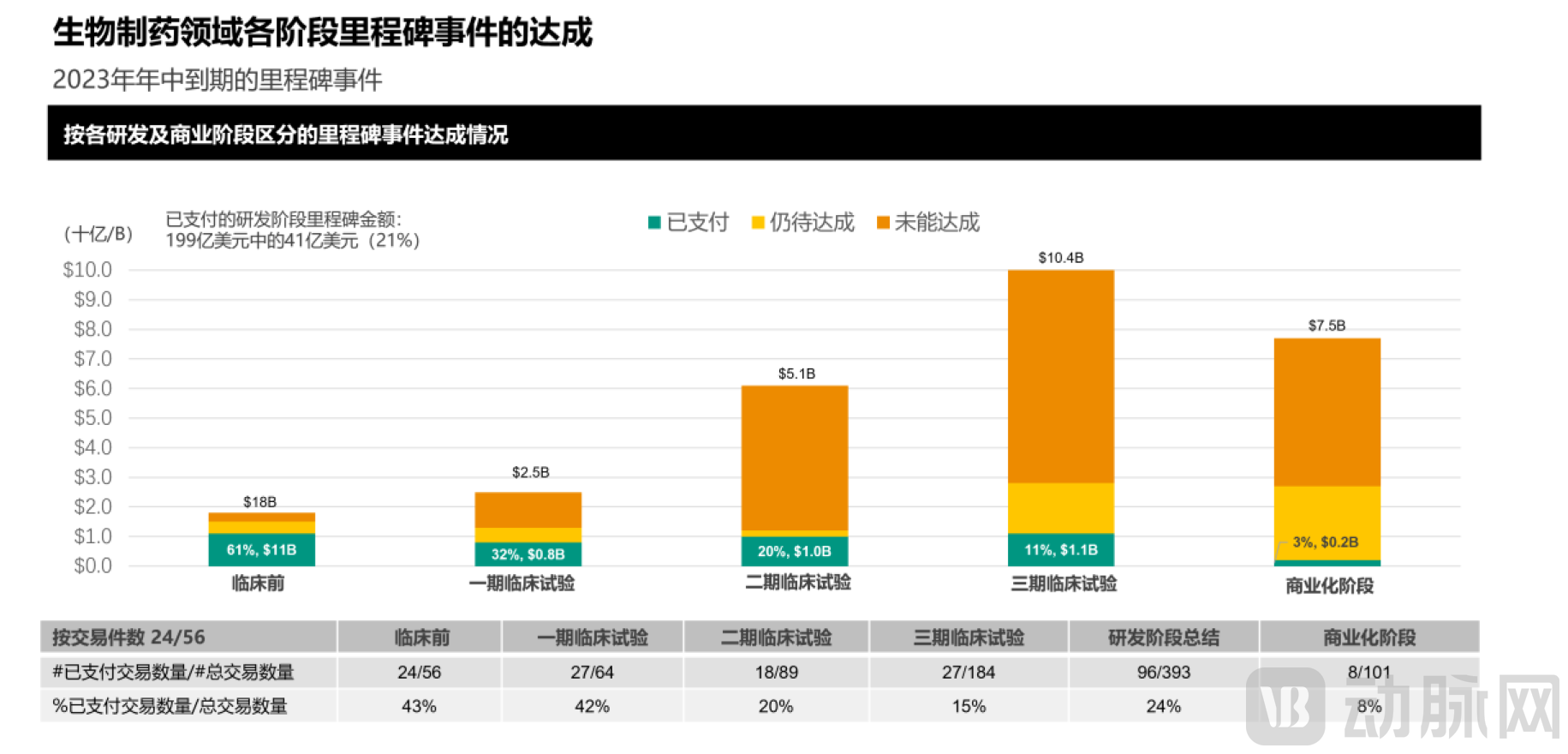

Figure 5. Statistics on the Achievement of “Milestone” Events at Various Stages in the Biopharmaceutical Sector in 2023 (Image Source: SRS ACQUIOM)

Figure 5. Statistics on the Achievement of “Milestone” Events at Various Stages in the Biopharmaceutical Sector in 2023 (Image Source: SRS ACQUIOM)

For instance, significant uncertainties currently surround the fulfillment of the most critical milestones. According to statistics from Amino Observation, in 2023, the milestone achievement rate in China’s biopharmaceutical M&A transactions was only 22%, and the amount triggered by achieved milestones was even lower, with only 3% of the total transaction value actually paid out.. In other words, even without considering the factor of “deal termination,” these massive BD deals can easily become empty promises, resulting in significant losses for pharmaceutical companies.

Next is the issue of innovative drug attrition. As business development (BD) activities gain momentum, concerns have begun to emerge at the market level thatAll the Promising Drug Candidates Have Been Snapped Up: Can China’s Innovative Drugs Still Grow Bigger and Stronger?In fact, such concerns are well-founded. On one hand, many promising candidates have indeed been acquired, with a significant number ultimately failing to reach commercialization. On the other hand, pharmaceutical companies are becoming increasingly reliant on business development (BD) activities; currently, they are not only licensing out drug rights but even engaging in outright acquisitions of entire companies. This trend will inevitably lead to a certain degree of loss of innovative drugs from China.

The final issue to address is that of profit maximization. In this regard, a senior investor stated, “For some domestic pharmaceutical companies,BD is, in essence, a financing strategy adopted out of necessity; as IPO channels gradually narrow, companies must seize the cash flow from business development deals to ensure their survival.Therefore, in many cases, it does not fall under the conventional business development (BD) model aimed at maximizing self-interest.” This has long been validated in the U.S. biopharmaceutical industry. Although the sector as a whole has formed a “three-wheel drive” financing model comprising primary market fundraising, initial public offerings (IPOs), and BD transactions, actual development shows that IPOs and subsequent secondary market refinancing are essential for sustaining the growth of biotech companies and even enabling their evolution into biopharma enterprises.

Therefore, from an integrated perspective, the current BD boom has indeed alleviated the financial pressure on pharmaceutical companies. However, the urgent "overheating" may easily lead to bubbles and even the unfortunate misallocation of resources. Thus, business development for innovative drugs in China should return to the right track as soon as possible, truly becoming a mature asset allocation practice within the market environment.Let BD focus on BD, and let R&D continue with R&D.。

1. “Go Global or Get Out? Business Development Deals for Innovative Drugs Going Overseas Accounted for About 80% in the First Half of the Year” — Cailian Press;

2. “China’s Promising Innovative Drug Candidates Are Being Snapped Up” — The Economic Observer;

3. “The Era of Universal Business Development for Innovative Drugs: Annual Salaries of 2–3 Million Yuan, Headhunting Firm Bosses Enter the Fray to Poach Talent, and CEOs Lead Recruitment Efforts Personally” — DeepBlue View.