China's Medical Sector Opening-Up Pilot Sparks 'Catfish Effect' Amid Surge in Foreign Investment and Innovation

On September 7, the Ministry of Commerce website published the “Notice of the Ministry of Commerce, the National Health Commission, and the National Medical Products Administration on Launching Pilot Programs for Expanded Opening-up in the Healthcare Sector.” The announcement immediately drew widespread attention from the industry.

▲ Image source: Official website of the Central People's Government of the People's Republic of China

▲ Image source: Official website of the Central People's Government of the People's Republic of China

“The release of this policy has injected more 'source water' into the industry..” Dr. Zou Guowen, founding partner of Kaicheng Capital, told VCBeat that government investment, private capital investment, and foreign investment are the three major sources of investment, and this document will have a certain positive effect on strengthening foreign investment in China's healthcare sector.

Based on the specific content of the document, it primarily concerns the opening up of two major sectors: biotechnology and wholly foreign-owned hospitals.

· In the field of biotechnology, the Notice states that foreign-invested enterprises are permitted to engage in the technological development and application of human stem cell, gene diagnosis, and gene therapy technologies within the Beijing, Shanghai, and Guangdong Free Trade Zones and the Hainan Free Trade Port, for the purpose of product registration, market launch, and manufacturing. All products that have obtained marketing authorization and production approval may be used nationwide.

·Regarding wholly foreign-owned hospitals, it is proposed to permit the establishment of such facilities (excluding those specializing in Traditional Chinese Medicine and excluding acquisitions of public hospitals) in Beijing, Tianjin, Shanghai, Nanjing, Suzhou, Fuzhou, Guangzhou, Shenzhen, and across the entire island of Hainan.

Meanwhile, to ensure the effective implementation of the pilot program, the document specifically emphasizes that the commerce, health, human genetic resource management, and drug supervision departments in pilot regions must strengthen policy publicity and interpretation, proactively engage with foreign-invested enterprises expressing interest, and provide necessary support and services. Furthermore, these departments are required to enhance coordination, communication, and the establishment of information-sharing mechanisms to form a synergistic effort for the in-depth advancement of the pilot initiatives.

Undoubtedly, China’s healthcare sector is ushering in greater openness, and the industry is poised for new changes.

In the newly released documents, the provision “allowing foreign-invested enterprises to engage in the development and application of human stem cell, gene diagnosis, and gene therapy technologies within domestic free trade zones” has become the focal point of industry attention.

This is because the industry widely believes that the proactive introduction of foreign investment and advanced technologies will play a highly significant role in driving greater technological innovation and breakthroughs in China’s frontier medical technology sectors.

On the one hand, domestic innovative enterprises can learn more advanced technologies in human stem cells, genetic diagnosis, and therapy through collaboration with foreign-funded enterprises, thereby promoting medical innovation in China.

On the other hand, the entry of foreign investment can trigger a "catfish effect," compelling domestic enterprises to accelerate innovation and improve R&D efficiency, thereby countering the technological advantages and brand influence of international companies.

Performance varies slightly across specific niche segments.

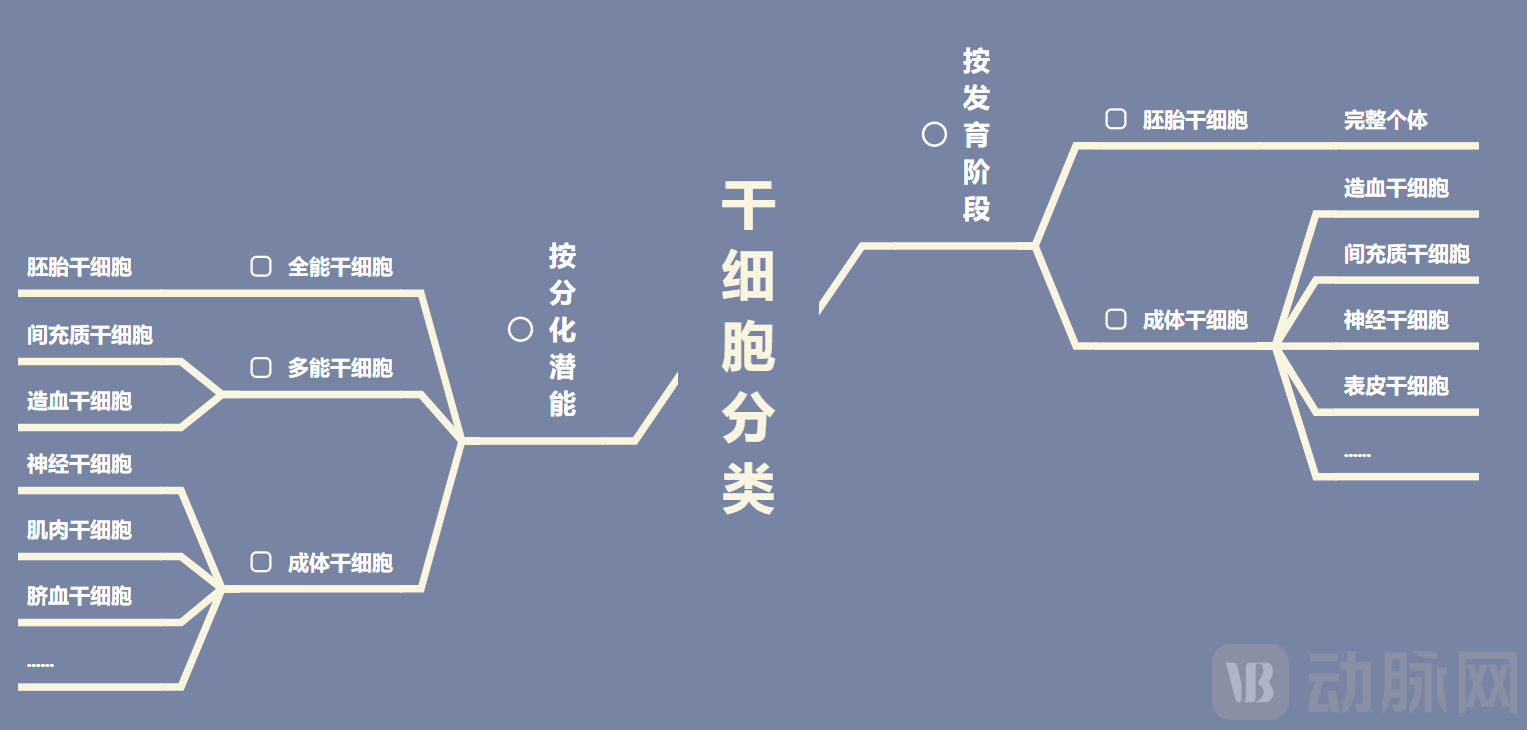

First, in the field of human stem cells, this document breaks the previous regulations that prohibited foreign investment from entering the stem cell industry, thereby providing further support for collaboration and transformation within the sector.

As a class of pluripotent cells with self-replicating capacity, stem cells can differentiate into various functional cell types under specific conditions. They are characterized by self-renewal, multilineage differentiation, responsiveness to tissue injury, and transplantability, which endow them with significant application potential in the medical field. By transplanting healthy stem cells into patients, damaged or dead cells can be repaired and replaced, thereby restoring normal physiological function.

▲Classification of Stem Cells | Graphic by VCBeat

▲Classification of Stem Cells | Graphic by VCBeat

It is precisely on this basis that the global stem cell industry is booming. According to incomplete statistics from VCBeat, more than 11 stem cell products have been approved for marketing worldwide to date. These approved products consist of hematopoietic stem cells or mesenchymal stem cells and are primarily indicated for the treatment of conditions such as thalassemia, tissue repair, and immunomodulation.

R&D Progress of Domestic Stem Cell-Related Companies Is Also Accelerating. According to data from the Qianzhan Industry Research Institute, as of December 31 last year, a total of 106 stem cell drug clinical trial applications from 56 companies (excluding subsidiaries) in China had been accepted, and 79 applications from 44 companies (excluding subsidiaries) had received implicit approval to enter clinical trials (implicit clinical trial approval).

▲ Layout of Chinese Stem Cell Enterprises in Technology and Application Fields

▲ Layout of Chinese Stem Cell Enterprises in Technology and Application Fields

Image source: Qianzhan Industry Research Institute

At the policy level, the state has successively issued a series of documents that clearly support and encourage the R&D of innovative stem cell technologies and the commercialization of related products, covering various dimensions from clinical research to industrial development. For instance, in May this year, the “Administrative Licensing Information” section on the website of the Beijing Medical Products Administration showed that Bosun Excellence, a domestic innovative enterprise, became the first company in China to obtain a stem cell drug production license. This signifies that stem cell drugs in China now meet the basic requirements for market entry.

It is evident that, bolstered by prior policy support, continuous technological breakthroughs by enterprises, and the recent liberalization of foreign investment access, China’s stem cell industry is entering a new phase of development.

Furthermore, with regard to genetic diagnosis and therapeutic technologies, the issuance of this document represents a continued follow-up on the state’s regulatory approach to foreign investment in this sector in recent years.

▲Graphic by VCBeat

▲Graphic by VCBeat

Market responses have led some observers to believe that foreign enterprises, particularly global pharmaceutical giants, are at the forefront of the gene therapy field. The implementation of new regulations will facilitate the entry of advanced international gene therapy technologies into the domestic market, especially regarding the introduction of innovative gene therapies for rare and genetic diseases, such as thalassemia, spinal muscular atrophy, and primary skeletal muscle necrosis disorders.

Furthermore, the entry of foreign-funded enterprises may drive the government to further optimize and refine regulatory policies related to gene therapy, particularly in areas such as drug approval and clinical trials.

However, an industry insider who requested anonymity also told VCBeat that, due to considerations such as biosafety security and cross-border data flows, the opening up of “the development and application of gene diagnosis and therapy technologies” will inevitably be a gradual process, with urgent need for the implementation of relevant operational details.

In the view of Dr. Zou Guowen, Founding Partner of Kaicheng Capital, the release of these documents also carries significant positive implications for market access of relevant pharmaceuticals. “Having previously worked at multinational pharmaceutical companies for nearly a decade, I was most struck by the time lag in drug launches: a medication might have been marketed abroad for many years, yet remained unavailable in China due to market access barriers.”From this perspective, the document provides global medical innovation enterprises with broader market access opportunities in China.”

Meanwhile, in accordance with the notice requirements, all products that have undergone rigorous registration, market approval, and production authorization processes may be legally used throughout China. This will significantly accelerate the translation and application of medical technological achievements, benefiting a broader patient population.

Certainly, to ensure the smooth implementation of the pilot program, the Notice further clarifies the legal and regulatory framework that foreign-invested enterprises must comply with. This includes specific requirements concerning the administration of human genetic resources, drug clinical trials (including international multi-center clinical trials), drug registration and market approval, drug manufacturing, and ethical review, while underscoring the importance of adhering to the relevant administrative procedures.

The second key point of the policy focuses on wholly foreign-owned hospitals, according to the guidelines,Proposed Permission to Establish Wholly Foreign-Owned Hospitals (Excluding Traditional Chinese Medicine Hospitals and Excluding Acquisitions of Public Hospitals) in Beijing, Tianjin, Shanghai, Nanjing, Suzhou, Fuzhou, Guangzhou, Shenzhen, and the Entire Island of Hainan. This will inevitably deliver a significant shock to the healthcare services industry, which has remained "silent" for quite some time.

In fact, healthcare service providers have faced significant challenges over the past one to two years. Taking Distinct HealthCare as an example, the company formally submitted its prospectus to the Hong Kong Stock Exchange in June this year, but there has been no further update to date. Industry insiders speculate that this is primarily due to unsatisfactory financial data. According to the prospectus, Distinct HealthCare achieved a compound annual growth rate (CAGR) of 28.64% in revenue from 2021 to 2023; however, it remains unprofitable, having incurred a net loss of RMB 817 million over the past three years. This situation will inevitably cast a shadow over its path to listing.

However, Zhuozheng Medical is not the only player trapped in the vicious cycle of “rising revenue without corresponding profit growth”; United Family Healthcare (UFH) and Amcare USA are facing similar challenges. Taking UFH as an example, although its revenue has surged in recent years, reaching approximately RMB 3.7 billion in 2023, it has yet to escape the awkward predicament of unprofitability. Amcare USA, which specializes in high-end obstetrics, gynecology, and pediatric services, has seen the contribution of its obstetrics business to overall revenue drop significantly from 80% to 30%, largely due to the persistent decline in the birth rate.

So, what exactly is holding back healthcare service providers?First and foremost, there is the bottomless pit of investment., healthcare service providers have always been a “business” characterized by heavy upfront asset investment and slow returns on investment; in particular, the need for rapid early-stage expansion to capture market share naturally results in substantial capital consumption.

Next is the intense market competition brought about by homogenization. For healthcare service providers, patient acquisition is critical, yet it remains a significant pain point. On one hand, China’s healthcare system continues to be dominated by public hospitals; on the other, these providers target middle- and high-income groups, a relatively small demographic that is difficult to reach, thereby necessitating higher customer acquisition costs. Finally, factors at the market environment level, including declining birth rates and a capital winter, will exert certain negative impacts on healthcare service providers.

The release of the “Wholly Foreign-Owned Hospital” policy may change this situation.For example, it will promote business cooperation at relevant levels., which will bring new opportunities to healthcare service providers.In June this year, Mayo Clinic established its first office in China at Shanghai United Family Hospital. The two parties will engage in long-term cooperation in areas such as joint treatment programs, international academic exchanges, and clinical training. In terms of mergers and acquisitions (M&A), activity among healthcare service providers has remained robust in recent years. A total of 45 M&A transactions occurred in the fourth quarter of 2023, and this number is expected to continue growing with increased involvement from foreign investors.

In addition to fostering collaboration, another positive development is the acceleration of market consolidation through survival of the fittest, thereby driving institutions to expedite their transformation and upgrading.In this regard, a senior industry expert remarked, “What foreign-funded hospitals actually bring are advanced management models, technologies, and equipment. Particularly in areas such as personalized medicine, complex surgeries, and the treatment of rare diseases, their high-quality services and international standards are more likely to attract high-income patient groups. This will naturally exert competitive pressure on existing medical institutions, prompting them to improve service quality and management standards. Those that fail to keep up will gradually be eliminated by the market.” Therefore, in a sense, this represents a critical process for clearing out industry bubbles.

Overall, allowing foreign investors to establish wholly-owned hospitals has effectively injected more capital and innovative elements into the industry, while simultaneously intensifying market competition. These forces will ultimately converge to stir up the stagnant waters of the healthcare services sector, bringing about significant new changes.

As the healthcare industry becomes increasingly globalized, this latest liberalization is bound to yield numerous beneficial outcomes. In fact, the development of China’s healthcare sector has long relied on foreign investment, ranging from the early establishment of multinational corporations in the country to the current multi-dimensional collaborations in commercial and R&D arenas, all of which are closely tied to foreign capital.

However, even so,Regarding the newly released policy on easing restrictions, we must still maintain a rational perspective, as the immediate challenges remain equally present.

For instance, the complexities at the regulatory and compliance levels.As is well known, the healthcare sector pertains to human life and health, and is therefore subject to extremely stringent regulatory requirements. Taking human stem cells, a key focus of this discussion, as an example, their use involves human genetic data. If foreign investment is to be permitted in this area, more detailed policy documents must be issued to clarify specifics such as market entry thresholds and qualification reviews for foreign investors. However, current policies have not yet elaborated on these aspects, merely stating that “the specific conditions, requirements, and procedures for establishing wholly foreign-owned hospitals will be announced separately.” Nevertheless, it is predictable that these restrictions will be very strict, posing significant challenges from policy formulation to implementation.

Furthermore, how can market competition be positively guided?As previously mentioned, the involvement of foreign capital will drive innovation in human stem cell, gene diagnosis, and therapy technologies in China, while significantly enhancing the quality of medical services and promoting the transformation and upgrading of the healthcare service industry. This will impose considerable competitive pressure on domestic companies; therefore, it is crucial to ensure that this pressure translates into healthy competition.

Meanwhile,In practice, the arrival of foreign-funded hospitals may intensify the mobility of medical talent., as some outstanding physicians and specialists will gradually leave public hospitals to work at foreign-funded hospitals due to the attractive compensation packages. This may lead to a shortage of talent resources in domestic public hospitals, especially in regions with already low levels of medical care, where the situation will be more severe. As the volume of such mobility increases, China’s medical innovation process, centered on public hospitals, will be affected, thereby impacting the development of China’s healthcare enterprises.

Finally, there are the challenges of cultural integration and localization.In recent years, multinational corporations (MNCs) have been accelerating their “localization in China” strategies. A typical example is AstraZeneca, which has been progressively integrating its core capabilities and resources deeply into China’s healthcare system, achieving notable progress to date. The current policy follows a similar logic: wholly foreign-owned hospitals must localize their operations to address the distinctive characteristics and demands of the Chinese healthcare market. This requires foreign enterprises to make corresponding adjustments in talent recruitment, service workflows, marketing strategies, and other areas—a process that will take time.

Nevertheless, it is certain that the promulgation of this policy demonstrates the nation’s determination to expand openness in the healthcare sector. As foreign capital continues to flow in and technological innovation persists, China’s market will see a growing number of R&D centers, production bases, and medical institutions established by foreign enterprises, all of which will inject new vitality and momentum into the country’s healthcare industry.