Domestic Endoscope Market Share Surges, Fueled by CDMO Industry Support

The landscape of China’s endoscopy market is undergoing a period of transformation, with the market share of domestically produced products rising significantly. Numerous Chinese manufacturers have entered the endoscopy market; in 2022 alone, at least 48 endoscopy systems were approved in China, primarily consisting of single-use endoscopes and rigid endoscopes. New entrants have demonstrated aggressive growth. Mindray, which only recently launched its endoscopy products, surpassed Stryker to rank among the top three players with an approximate 7% market share in 2022, according to the "China Medical Device Blue Book 2023." Meanwhile, established foreign companies are facing challenges.

The significant increase in the number of participants in the endoscopy market is attributable to Contract Development and Manufacturing Organizations (CDMOs), which, as an industrial support pillar, have substantially lowered the barriers to endoscope manufacturing. Domestic and international CDMOs are now capable of providing complete endoscopic imaging system solutions, enabling Chinese companies to obtain endoscope product registration certificates in the short term through original equipment manufacturing (OEM) or module integration.

In the field of single-use endoscopes, the relatively simpler product structure compared to reusable devices, coupled with stringent cost-control requirements, has spurred substantial demand for endoscope contract manufacturing.

Amidst the dual shifts in industrial structure and market landscape, China’s endoscope CDMO supply chain is quietly emerging.

Figure 1. Recent Financing Activities of Endoscopy CDMOs

In the field of medical devices, large CDMO companies are rare. However, the endoscopy sector is an exception; Haitai XinGuang, a CDMO enterprise listed on China’s STAR Market, originates from this field.

Haitai New Optics has partnered with global giant Stryker for a decade, securing annual orders worth hundreds of millions of yuan. As Stryker rose to become the global leader in fluorescence endoscopy, Haitai New Optics served as a key upstream component supplier.

Why Can the Endoscopy Field Give Rise to Large-Scale CDMO Enterprises?

The industrial characteristics of the endoscopy sector dictate stringent requirements for precision manufacturing.Given that endoscopic systems comprise numerous highly precise components and span multiple disciplines—including optics, mechanics, electronics, and computer science—their supply chain is extensive and complex. Adopting the CDMO model allows for the delegation of technologies across different fields to specialized upstream enterprises, thereby reducing investment in basic research and development and shortening time-to-market.

For new entrants among domestic enterprises, there is a heightened demand for product and technological iteration. Consequently, their reliance on the CDMO model is more pronounced, as they seek to leverage this approach to shorten R&D cycles, enhance market responsiveness, and ultimately gain a competitive edge.

Cao Houping, founder of Weishi Optoelectronics, stated: “In the past, the global endoscopy market was dominated by Japanese companies. Their product iteration cycles were relatively slow, allowing them ample time to meticulously refine their products; consequently, they largely maintained control over their own supply chains. As new entrants and latecomers, Chinese domestic enterprises require rapid product iterations and high responsiveness in production. The innovations proposed by these companies often involve solving numerous engineering and technical challenges. The OEM/ODM model leverages specialized expertise, enabling faster conversion of design models into prototypes and subsequently achieving large-scale mass production.”

In the endoscopy sector, original equipment manufacturers (OEMs) and upstream enterprises have established a mutually beneficial partnership, rather than a mere buyer-supplier relationship.OEMs are responsible for proposing innovative design concepts, while CDMOs leverage their specialized expertise to rapidly overcome engineering challenges and achieve large-scale production. This collaborative model not only accelerates the translation of products from concept to market but also fosters innovation and efficiency improvements across the entire industry chain.

Taking the collaboration between Stryker and Haitai XinGuang as an example, in 2006, Stryker sought to replace its existing xenon light sources with LED technology. The project lasted two years but did not proceed smoothly. Consequently, Stryker searched globally for new LED solutions. Leveraging its technological expertise, Haitai XinGuang developed a proof-of-concept prototype within three months and launched its first-generation medical LED light source module, successfully securing a place on Stryker’s supplier list.

Subsequently, Stryker proposed the development of fluorescent endoscopes to reduce the failure rate of common bile duct surgeries. Haitai Optoelectronics competed with established endoscope manufacturers and ultimately took the lead in developing the fluorescent endoscope body, light source module, and compatible lenses, becoming the sole supplier of these three key components for Stryker’s fluorescent endoscopy systems.

Although some domestic companies currently purchase complete machine solutions directly, in a healthy partnership, the original equipment manufacturer (OEM) plays a leading role in product design and iteration. Meanwhile, it provides critical guidance and feedback during the product development process to ensure that the product meets market demands and maintains technological leadership.

As a domestic endoscopy company, Zhuowai Medical has adopted a strategy of full-stack independent research and development, mastering core technologies in-house before outsourcing the manufacturing of certain components. This strategic choice was driven by two main factors: first, when Zhuowai Medical entered the endoscopy industry in 2015, China’s CDMO (Contract Development and Manufacturing Organization) supply chain was still immature, and international technical collaborations were restricted; second, the company remained committed to its original mission of developing proprietary, innovative, differentiated, and high-quality products.

Zhao Hui, Operations Director at Zhuowai Medical, stated, “Core technologies in optics, electronics, and computing must be mastered in-house before outsourcing certain components to ensure system integrity and stability. Endoscope design encompasses front-end imaging, illumination, image acquisition, and host algorithm processing. If original equipment manufacturers (OEMs) do not possess system development capabilities across this chain, it will be difficult to achieve optimal performance in terms of device compatibility and clinical application.”

CDMO companies rely on the strong brand and channel advantages of original equipment manufacturers (OEMs).The endoscopy market exhibits a high degree of dependence on brands and distribution channels, which constitute the core competitiveness that original equipment manufacturers (OEMs) have built through long-term accumulation. Leveraging their strong brand influence and extensive distribution networks, OEMs can more effectively reach numerous end-user hospitals and establish close ties with physician communities. In contrast, although Contract Development and Manufacturing Organizations (CDMOs) may engage in the end-market, they often struggle to compete with OEMs in terms of brand recognition and channel penetration.

Cao Houping, founder of Weishi Optoelectronics, stated: “The domestic substitution and globalization of endoscopes are progressing at a rapid pace. For downstream manufacturers, success depends not only on technology and product competitiveness but also heavily on sales and market channels. For upstream enterprises, the core success factors are product quality, stability, and cost control.”

The endoscopy field is characterized by stringent requirements for precision manufacturing and its multidisciplinary technological nature, creating fertile ground for the growth of CDMO companies. The brand and channel advantages of original equipment manufacturers (OEMs) provide CDMOs with stable market access. This interdependent and mutually reinforcing relationship is key to fostering large-scale CDMO enterprises in the endoscopy sector.

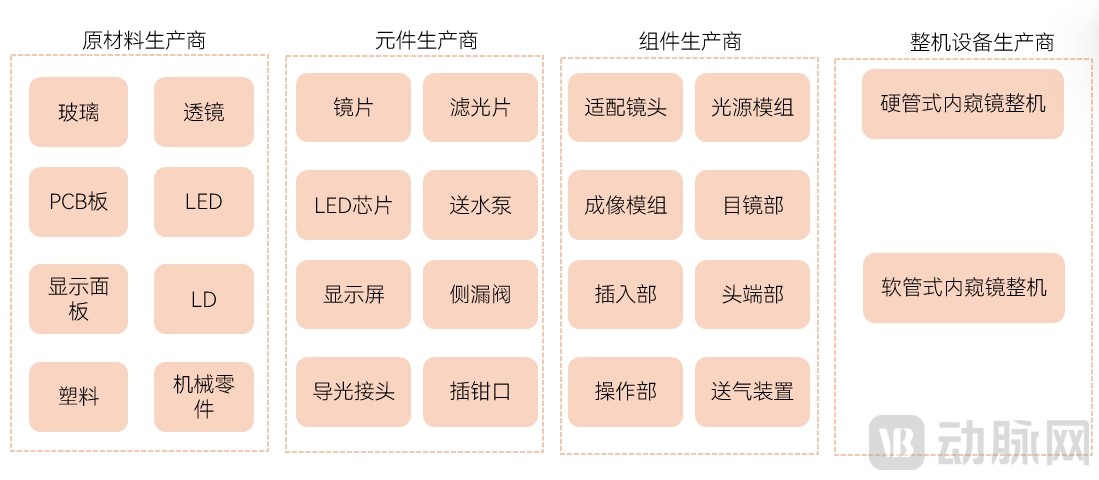

The endoscopy sector comprises numerous subfields. It can be categorized into rigid and flexible endoscopes based on application scenarios; into single-use and reusable endoscopes based on the number of uses; and into optical and electronic endoscopes based on imaging principles.

Data Source: Hanghangcha Research Center

Figure 2. Endoscope Industry Chain Map

Among the various categories, which endoscopy CDMO companies present greater market opportunities?

Driven by clinical demands for endoscopes that are simple, cost-effective, and safe, the market demand for single-use endoscopes is projected to grow significantly. Due to their lower acquisition costs and elimination of sterilization requirements, these devices are well-suited for diverse healthcare settings, including large hospitals, township hospitals, and outpatient clinics. In China, the use of single-use endoscopes in urological procedures for kidney stone surgery has become quite prevalent. In international markets, products such as single-use bronchoscopes, single-use ureteroscopes, and single-use cholangiopancreatoscopes have been widely adopted.

Moreover, the CDMO model offers greater cost advantages and achieves economies of scale in the high-volume disposable endoscope sector, enabling it to provide more cost-effective solutions to downstream original equipment manufacturers (OEMs).

Unlike the rigid and flexible endoscope markets, which were previously dominated by an oligopoly of importers, the single-use endoscope market is developing synchronously both domestically and internationally, with China’s domestic supply chain rapidly maturing.

Taking Weishi Optoelectronics as an example, the company has mastered core camera module manufacturing capabilities. In the contract manufacturing of single-use endoscopes, the camera module is the core component. Integrating optical, mechanical, electronic, and computational technologies, the camera module includes CMOS chips and accounts for the highest proportion of value. Furthermore, as single-use endoscopes feature simplified structural designs, the significance of the camera module is further accentuated, representing 50%–80% of the total component cost. As the most critical part of a single-use endoscope, it determines key image quality metrics. Weishi Optoelectronics supplies camera modules to numerous downstream enterprises in China. With the upgrading demands of downstream clients, Weishi Optoelectronics has begun offering CDMO services, providing comprehensive solutions and delivering high-quality components or complete endoscope products rapidly to companies with strong market channel access.

In addition to disposable endoscopes, contract manufacturing of rigid endoscopes also holds certain market potential. Rigid endoscopes can be categorized into optical and electronic types. Electronic endoscopes require the integration of image sensors and other modules within confined spaces, addressing challenges such as packaging size constraints, illumination areas, interference, and safety. Currently, only a few domestic companies possess the capability for module packaging and production of electronic endoscopes. The global supply chain for optical rigid endoscopes is relatively mature. An optical endoscopy system primarily consists of four major components: the optical scope, light source, camera module, and main unit. A well-established industrial chain has already formed globally for the contract manufacturing of optical endoscopy systems.

- The core technologies for optical endoscope bodies encompass optical design, machining, coating, and packaging, with a mature global supply chain already established. Major global suppliers of endoscope bodies include Karl Storz (Germany), Wolf (Germany), Schölly Fiberoptic (Germany), Zhuowai Medical, and Haitai XinGuang.

- The light source provides illumination for the endoscope. As a critical component of the complete endoscopic system, its performance metrics—such as brightness, color temperature, and color fidelity—significantly impact image quality. Fluorescence light source modules present greater challenges in excitation and manufacturing. Haitai XinGuang, a Chinese enterprise, has achieved world-leading capabilities in the production of fluorescence light source modules.

l Camera Module: Re-images the optical image formed by the endoscope tip onto the CMOS sensor of the camera handle.

l Camera Control Unit (CCU): The CCU module accounts for nearly 70% of the total cost of an endoscope, encompassing chips and algorithms. Major global manufacturers of mainstream endoscopic CCU systems include Japanese suppliers such as Ikegami, Panasonic, and Hitachi, as well as Hikvision Huiying.

Reusable flexible endoscopes have relatively low demand for CDMO services. Due to the high net value of flexible endoscopes and their limited shipment volume in reusable applications, most manufacturers opt to procure core components for in-house assembly and production, while outsourcing non-core hardware machining parts and metal machining services.

The true rise of China’s domestic endoscope industry chain depends on advancements in related materials and process technologies, as well as a robust supply chain for support.In the early stages, Japanese companies dominated the optical imaging module market. Japan and Germany possessed advanced precision optical processing and packaging technologies, making it difficult for Chinese enterprises to secure technical collaborations. Even when cooperation intentions were reached, Chinese enterprises often faced constraints from foreign suppliers in terms of response speed and level of coordination, resulting in end products that failed to meet expectations.

As a critical link in the endoscopy industry chain, in which areas should endoscopy CDMOs enhance their competitiveness?

First is the specialized capability in R&D, design, and manufacturing. Endoscope CDMOs integrate innovative R&D with supply chain management, operating in a high-barrier segment of the medical device CDMO industry that requires substantial technological accumulation and experience in the endoscopy field. Only enterprises that master core module production capabilities and can help customers achieve technical optimization and concept commercialization can sustain stable orders.

Next is cost control capability. CDMO companies need to provide cost-effective products through effective cost control to meet customers' dual demands for price and quality. Especially in the field of single-use endoscopes, there are more than 60 manufacturers in China, with fierce competition among downstream brands. This pressure is transmitted to upstream suppliers, imposing higher requirements on the cost control capabilities of CDMO companies. Previously, although some domestic CDMO companies entered the rigid endoscope field and achieved partial success, initial market feedback was poor due to excessively high mass production costs.

Ultimately, the choice of partners determines the stature of a CDMO enterprise. To integrate into the global supply chain, CDMOs must secure orders from key global players. For upstream contract development and manufacturing organizations (CDMOs), partnerships with globally leading manufacturers serve as a powerful endorsement of credibility. Such collaborations not only ensure that CDMOs adhere to the industry’s highest standards but also typically come with substantial and stable order volumes. Furthermore, these strategic partnerships significantly enhance a CDMO’s bargaining power in business negotiations with other potential partners.

As the domestic endoscopy supply chain gradually matures, competition in China’s endoscopy market is entering a new phase, with a shift in industry logic: from the previous model characterized by long timelines and substantial capital investment to one focused on enhancing product competitiveness and strategically expanding channel markets. Currently, downstream brands are experiencing rapid volume growth and high-speed development, while for upstream manufacturers, companies possessing core component capabilities are poised to emerge as leaders.

References:

On the Localization of Endoscopes — Qiushi Forest

Domestic Endoscopy Industry Accelerates Expansion; Haitai New Optics Moves Toward “Light” — Shanghai Securities News