Over 50 Institutions Invest More Than $2.8 Billion as Ophthalmic Innovative Drug Sector Surges

As a high-growth, high-barrier “double-high” sector, the ophthalmology industry has long been hailed as the “golden track” of the capital markets.

In recent years, driven by the accelerating pace of population aging, changes in lifestyle, and the widespread adoption of electronic devices, both the incidence of ocular diseases and the demand for pharmacological treatments have continued to rise, fueling rapid growth in the ophthalmic drug market. Meanwhile, ophthalmic diseases are highly specialized and segmented, with the pathogenic mechanisms of many eye conditions remaining poorly understood. These factors contribute to high technical barriers in ophthalmic therapeutics and pose significant challenges to the research and development of new drugs.

The iteration and development of ophthalmic drug technologies are of great significance to improving the overall level of eye health for the entire population. The research and development of novel ophthalmic drugs are dedicated to achieving longer-lasting therapeutic effects, replacing traditional medications with suboptimal efficacy, and providing innovative treatment options for ocular diseases that currently lack pharmacological interventions.

However, in China, the ophthalmic drug market started relatively late due to a lag in understanding the pathogenesis of many ophthalmic diseases and limited patient awareness and attention. Currently, the market is dominated by generic drugs and license-in products, with few independently developed innovative drugs. While generics and license-in strategies can rapidly shorten R&D cycles, accelerate market entry, and reduce development risks, they are also the root cause of drug homogenization in the market.

It can be said that the independent research and development of innovative ophthalmic drugs is a more challenging path. In light of this, we have conducted a comprehensive review of innovative ophthalmic medications. As the indications for innovative drugs continue to expand, the ophthalmic pharmaceutical market is poised for further growth. Amidst this certain market demand, who will be the first to seize the market opportunity?

12 New Drugs Approved, Financing Exceeds RMB 2 Billion: Innovative Ophthalmic Drugs Are Racing Ahead

Currently, the global ophthalmology market is characterized by steady growth and a high degree of concentration. Data shows that the global market size for innovative ophthalmic drugs was estimated at USD 3.782 billion in 2023, and is projected to grow at a compound annual growth rate (CAGR) of 8.34% from 2024 to 2030, reaching USD 6.606 billion by 2030.

In 2023, the FDA issued two relevant guidelines to guide the industry in drug quality/CMC and clinical research during ophthalmic drug development. The release of these guidelines has also led to a series of breakthrough advances in ophthalmic drugs.

In October 2023, to better guide the development of ophthalmic drugs, the FDA released a draft guidance titled “Quality Considerations for Topical Ophthalmic Drug Products.” The guidance focuses on quality considerations for ophthalmic drug products intended for topical administration to the intraocular and periocular tissues (i.e., solutions, suspensions, emulsions, gels, ointments, and creams). In February 2023, the FDA issued “Neovascular Age-Related Macular Degeneration: Developing Drugs for Treatment,” which aims to provide sponsors with recommendations on eligibility criteria, trial design considerations, and efficacy endpoints to improve the data quality of clinical trials for nAMD treatments and enhance the efficiency of drug development programs.

In 2023, the FDA approved 12 novel ophthalmic drugs for market launch. These included anti-VEGF agents, bispecific antibodies, complement inhibitors, and small-molecule drugs, with indications covering age-related macular degeneration (AMD), geographic atrophy (GA) secondary to AMD, dry eye disease, presbyopia, and mydriasis.

In 2023, the FDA approved 12 novel ophthalmic drugs

In China, innovative ophthalmic drugs have consistently remained a key focus for capital investment. Currently, 400 million patients in the country suffer from various eye diseases. With deepening population aging and changes in modern lifestyles, the burden of ophthalmic diseases in China is becoming increasingly prominent, indicating substantial growth potential in market size.

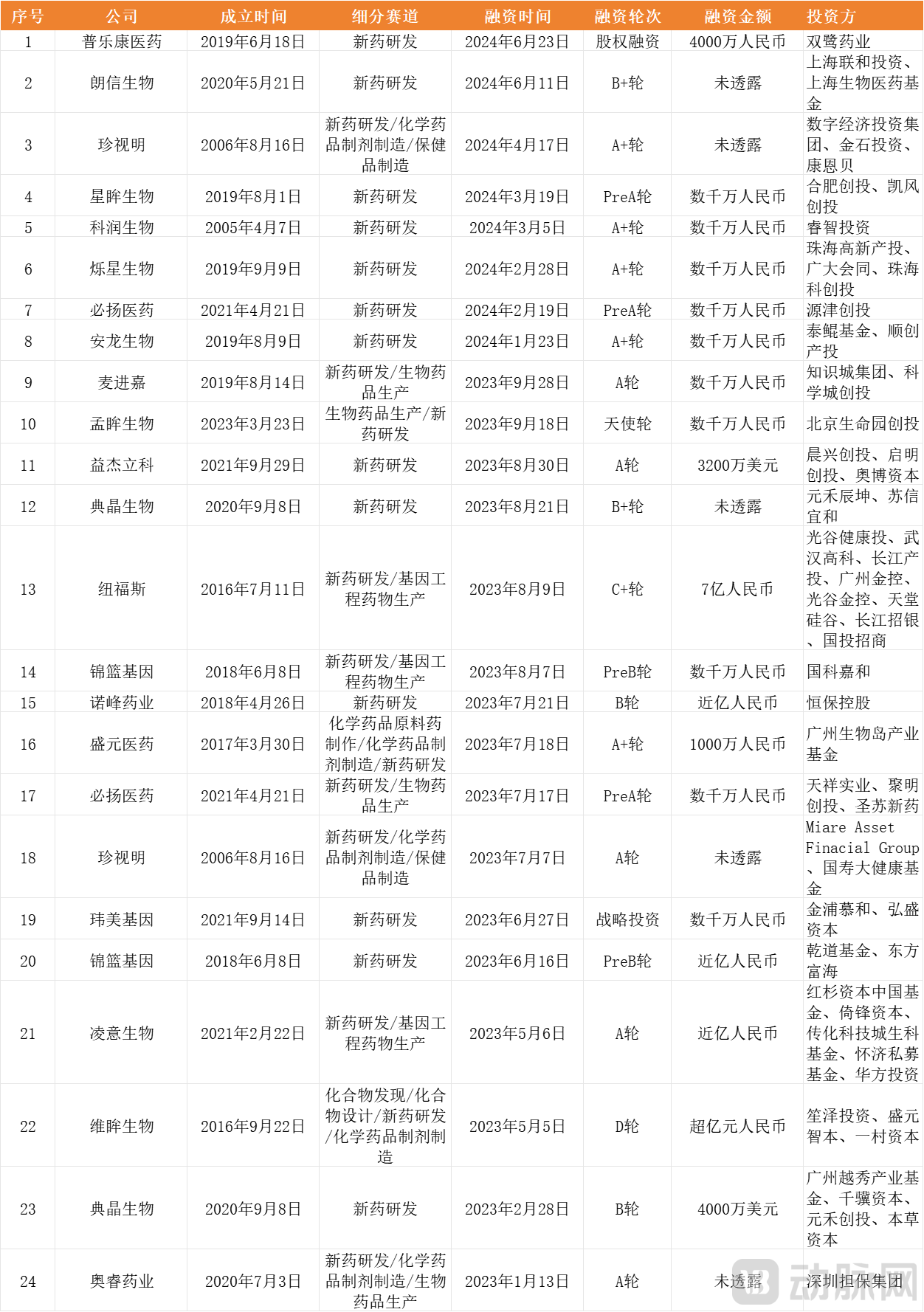

Financing Events for Innovative Ophthalmic Drugs in China from January 2023 to Present (Incomplete Statistics)

Financing Events for Innovative Ophthalmic Drugs in China from January 2023 to Present (Incomplete Statistics)

According to incomplete statistics, from 2023 to the present (with data compiled up to August 30, 2024), a total of 21 companies in China’s innovative ophthalmic drug sector have been involved in 24 financing events, with the total amount raised exceeding RMB 2 billion.

Amid robust market demand, and despite a less-than-optimistic overall investment and financing environment, numerous innovative ophthalmic pharmaceutical companies have successfully secured funding, injecting fresh capital to advance their pipeline development and future growth.

Anti-VEGF, Gene Therapy, Complement Drugs... Continuous Innovation in the Mechanisms of Ophthalmic Drugs

Currently, the market for innovative ophthalmic drugs is experiencing rapid growth, particularly in several key disease areas.

Among these, age-related macular degeneration (AMD) has become one of the areas with the greatest growth potential due to its direct association with an aging population. Diabetic macular edema (DME) has also emerged as a significant therapeutic area driven by the rising number of diabetes patients. As a leading cause of irreversible blindness worldwide, the treatment market for glaucoma is expanding alongside increasing prevalence. The incidence of dry eye disease (DED) continues to rise in the digital era, with sustained growth in demand for therapeutic drugs as eye dryness caused by prolonged use of electronic screens becomes increasingly common. Demand for myopia control medications is also on the rise, particularly in East Asia, where there is a large population of myopic patients.

Furthermore, the market for treating ocular inflammation and infections is similarly driven by population aging and lifestyle changes, with rising incidence rates fueling demand for novel therapeutic approaches.

Given the numerous and complex subtypes of ophthalmic diseases, innovative drug research in the field of ophthalmology is dedicated to achieving innovation through multiple mechanisms of action, with the aim of providing patients with more effective and better-tolerated treatment options.

Notably, anti-vascular endothelial growth factor (VEGF) agents have achieved significant progress in treating neovascular ocular diseases by inhibiting abnormal blood vessel growth to improve vision. Complement C5 inhibitors, such as Lzervay, provide new therapeutic options for fundus diseases like geographic atrophy (GA) by reducing complement system activity. Bispecific antibodies, such as faricimab, offer more effective treatments for patients with retinal vascular diseases by simultaneously targeting the VEGF and Ang-2 pathways, among other advancements.

In the treatment of hereditary ophthalmic diseases, gene therapy is demonstrating significant potential by replacing or repairing defective genes to treat conditions such as Leber hereditary optic neuropathy and retinitis pigmentosa.

Low-concentration atropine has been proven to effectively slow the progression of myopia, offering a new strategy for myopia control. Meanwhile, in the treatment of open-angle glaucoma, novel agents such as VVN539 lower intraocular pressure through a dual-target mechanism, providing patients with new therapeutic options.

Anti-VEGF Drugs: Four Products Launched in China, with Substantial Revenue from Marketed Products

Common neovascular ocular diseases primarily include wet age-related macular degeneration (wet-AMD), diabetic retinopathy (DR), diabetic macular edema (DME), and retinal vein occlusion (RVO). As anti-VEGF agents can effectively inhibit the formation of new blood vessels and promote the regression of existing ones, they have become the mainstay of treatment for fundus vascular diseases.

Anti-VEGF agents have revolutionized the field of ophthalmic therapy, exerting their therapeutic effects through multiple mechanisms to treat various fundus diseases. First, these drugs inhibit VEGF activity, thereby preventing pathological angiogenesis, which is crucial for managing conditions such as wet age-related macular degeneration (AMD) and diabetic macular edema (DME). Second, by reducing vascular permeability, they minimize the leakage of plasma proteins and fluid from blood vessels into the retina, effectively alleviating macular edema. Furthermore, anti-VEGF agents promote the regression of existing abnormal blood vessels, further improving the pathological state of the retina.

In terms of improving vision, anti-VEGF drugs help delay disease progression and, in some cases, even improve visual acuity through the aforementioned mechanisms of action. With advancing research, next-generation bispecific antibody therapies that simultaneously target VEGF-A and Ang-2 are providing more comprehensive therapeutic benefits. Meanwhile, the development of oral anti-VEGF agents is underway, which will significantly enhance patient adherence and quality of life.

Although anti-VEGF drugs have achieved significant clinical efficacy, challenges remain, such as the need for frequent injections, potential systemic side effects, and non-response to treatment. To overcome these limitations, scientists are continuously exploring new drug formulations and delivery methods, aiming to provide more effective and safer therapeutic options for patients with ocular diseases.

Currently, five ophthalmic anti-VEGF drugs—ranibizumab, aflibercept, conbercept, brolucizumab, and faricimab—have been approved for marketing worldwide.Among them, ranibizumab, conbercept, aflibercept, and faricimab have been approved for marketing in China.

Anti-VEGF Drugs Approved in China

Ranibizumab, jointly developed by Roche and Novartis, was the first to receive approval, gaining FDA marketing authorization in 2006. As the first anti-VEGF ophthalmic biologic, its significant efficacy propelled anti-VEGF drugs to prominence in the field of ophthalmic therapy. The product entered the Chinese market in 2011. Leveraging its first-mover advantage, ranibizumab’s sales climbed steadily, peaking in 2014 at over $4.3 billion.

Aflibercept is the world’s first fully humanized fusion protein, jointly developed by Regeneron and Bayer. Although it entered the market approximately five years later than ranibizumab, Aflibercept rapidly established a dominant global position in the treatment of age-related macular degeneration (AMD) thanks to its superior therapeutic efficacy and affordable pricing. In its first year on the market, Aflibercept achieved sales of $838 million; by 2022, its sales reached $9.647 billion, making it the highest-selling anti-VEGF ophthalmic drug worldwide.

Conbercept is a fusion protein independently developed by the Chinese pharmaceutical company Kanghong Pharmaceutical, combining an anti-VEGF receptor with the Fc fragment of human immunoglobulin. As the first domestically produced VEGF monoclonal antibody in China, it broke the monopoly of high-priced imported drugs on the Chinese ophthalmology market and became one of the landmark products of innovative drugs in China at that time.

Unlike ranibizumab, conbercept’s active protein is a next-generation anti-VEGF fusion protein that is 100% humanized in structure. It effectively binds to multiple targets associated with pathological neovascularization, including VEGF-A, VEGF-B, and PlGF, offering superior therapeutic efficacy, fewer injections, and better medication adherence. Since its approval in China in 2013, conbercept has rapidly achieved sales growth by leveraging its first-mover advantage and cost-effectiveness. In 2023, conbercept generated revenue of RMB 1.936 billion, a year-on-year increase of 41.73%, accounting for as high as 48.93% of total revenue.

Brolucizumab is a humanized single-chain antibody fragment (scFv) developed by Novartis, with a molecular weight of 26 kDa. It features a small size, strong tissue penetration, potent inhibition of VEGF-A isoforms, and high affinity. This product is the first anti-VEGF drug approved for dosing every three months and received FDA approval for market launch in October 2019. According to EvaluatePharma forecasts, its global sales are expected to reach $1.32 billion by 2024.

Roche’s faricimab is the first approved bispecific antibody for ophthalmic diseases, targeting both VEGF-A and Ang-2. This dual-pathway mechanism of action enables faricimab to not only inhibit neovascularization but also enhance vascular stability in the treatment of fundus diseases, thereby improving therapeutic efficacy.

In China, the vast market potential has prompted domestic companies to target this promising sector. Among Chinese pharmaceutical firms, Qilu Pharmaceutical is a key player in this niche. In April 2022, Qilu Pharmaceutical submitted a marketing application for QL1207, a biosimilar of aflibercept; in January 2023, its marketing application for QL1205, a biosimilar of ranibizumab, was accepted for review.

In addition, Boan Biologics’ LY09004 and Mabwell’s 9MW0813, both aflibercept biosimilars, have also entered Phase III clinical trials. Once approved for marketing, the domestic ophthalmic anti-VEGF biologic sector will enter a phase of intense competition between innovative drugs and biosimilars, with market rivalry gradually intensifying.

In the arena of innovative anti-VEGF therapeutics, China’s market remains a blue ocean; therefore, the pace of drug development, along with innovation and differentiation, will be key to standing out in the future.

Gene Therapy: The Golden Track of Ophthalmic AAV Gene Therapy, with Over 20 Companies in China Laying Out Their Strategies

Gene therapy is an ideal candidate for the treatment of ophthalmic diseases, demonstrating significant advantages in ocular therapeutics. On one hand, the eye is an immune-privileged site; the blood–ocular barrier keeps it relatively isolated from the systemic immune system, thereby reducing the risk of immune responses triggered by treatment. On the other hand, since many ocular disorders result from defects in single or multiple genes, and mutations underlying numerous hereditary eye diseases have been precisely identified, gene therapy has a wide array of potential targets for development. Gene therapy aims to achieve long-term therapeutic effects through a one-time intervention, alleviating the burden of chronic medication on patients.

Beyond its advantages, gene therapy also faces challenges in ophthalmic treatment, including issues related to gene delivery efficiency, long-term safety, manufacturing costs, regulation, and ethics. With deepening scientific research and continuous technological advancements, these challenges are expected to be gradually overcome, enabling gene therapy to play a greater role in the future of ophthalmic care.

Currently, there are 137 gene therapy drugs in the research and development stage worldwide. Most of the gene therapies in clinical development focus on the most common hereditary eye diseases, such as retinitis pigmentosa, choroideremia, Leber hereditary optic neuropathy, Leber congenital amaurosis (LCA), color blindness, and X-linked retinoschisis (XLRS).

In December 2017, Luxturna, the world’s first ophthalmic gene therapy, was approved for marketing in the United States, sparking a surge of interest in ophthalmic gene therapies. Compared with other organs, the eye is smaller in volume, requiring only low drug doses to achieve therapeutic effects. Moreover, due to advantages such as immune privilege and low systemic risk, it has become a key area where pharmaceutical companies are prioritizing their strategic investments.

Currently, more than 20 companies in China are focusing on AAV gene therapy for ophthalmic indications, with many investigational new drugs already entering clinical trials, bringing new hope for the treatment of inherited eye diseases. Numerous innovative pharmaceutical companies are actively deploying in this field, including Nuofus Biologics, Langxin Biologics, Jiayin Biologics, Tianze Yuntai, Kanghong Pharmaceutical, Zhongyin Technology, Huida Genomics, Anlong Biologics, Jinweike, Bendao Gene, Jintian Biopharma, Fangtuo Biologics, Dingxin Genomics, Lingyi Biologics, Extreme Vision Biopharma, Xingmou Biologics, Mujing Biologics, Niulunjie Biologics, Lingnuo Pharmaceuticals, Aiweiluxin, Nanjing BestBio, Ruifeng Biologics, and Yinnowellcon. Many of their investigational drugs have already entered clinical trials.

Neurophth Biotech is a leading domestic enterprise in the field of ophthalmic gene therapy. Its core pipeline candidate, NFS-01, is designed to treat Leber Hereditary Optic Neuropathy (LHON) caused by ND4 mutations. In January 2022, NFS-01 received FDA Investigational New Drug (IND) clearance, becoming the first domestically developed ophthalmic gene therapy to obtain FDA approval for clinical trials. Currently, Neurophth Biotech has established a portfolio of 13 pipeline candidates, covering four major therapeutic areas: hereditary optic neuropathies, optic nerve injury disorders, hereditary optic atrophy, and vascular retinopathies.

Complement Therapeutics: The Cornerstone of Dry AMD Treatment—Can They Spark the Next Wave of Hype?

In the past two years, clinical development of complement therapeutics has continued to make positive progress, with some patients with rare diseases already deriving substantial benefit. Beyond rare diseases, the development and application of complement therapeutics in common conditions such as ophthalmic diseases are becoming increasingly active.

In the development of innovative ophthalmic drugs, the mechanism of action of complement therapeutics primarily involves modulating the activity of the complement system to mitigate complement-mediated inflammatory responses and pathological processes. The complement system is a component of the human immune system and participates in the onset and progression of various diseases, including ophthalmic conditions such as age-related macular degeneration (AMD). In the pathogenesis of AMD, abnormal activation of the complement system is considered a significant factor; it can cause cellular damage through the formation of the membrane attack complex (MAC) and exacerbate disease progression by promoting inflammatory responses.

Complement-targeting drugs inhibit excessive activation of the complement system by targeting specific components, such as C3, C5, or complement regulatory proteins. For example, IBI302 (Efdamrofusp Alfa) is a dual-targeting agent against VEGF and the complement system, capable of simultaneously inhibiting VEGF-mediated signaling pathways and mitigating complement activation-mediated inflammatory responses. The N-terminus of IBI302 binds to the VEGF family, blocking VEGF-mediated signaling pathways, thereby inhibiting angiogenesis, improving vascular permeability, and reducing vascular leakage. The C-terminus specifically binds to C3b and C4b, inhibiting the activation of both the classical and alternative complement pathways. This dual-targeting mechanism aims to provide more comprehensive therapeutic effects, improve visual acuity, reduce retinal edema, and potentially ameliorate macular atrophy and fibrosis.

In addition, the development of complement therapeutics encompasses other strategies, such as the biologic agent GEM103, a complement factor H-based therapy that functions by restoring proper regulation of the alternative pathway in the eyes of patients with age-related macular degeneration (AMD). Another example is avacincaptad pegol (ACP), a biologic agent targeting complement factor C5. As a potent and specific inhibitor of C5, it prevents C5 cleavage, thereby slowing the progression of AMD.

Currently, several complement-targeting drugs have been approved in the field of innovative ophthalmic drug development, including Eculizumab, Ravulizumab, Aflibercept, Avacincaptad Pegol (ACP), and IBI302 (Efdamrofusp Alfa). The approval of these agents has introduced new therapeutic options for ocular diseases, demonstrating significant efficacy particularly in complement-mediated conditions.

Currently, anti-VEGF agents remain the cornerstone of treatment for choroidal neovascular diseases, including wet age-related macular degeneration (wAMD), achieving visual improvement in the majority of patients and enabling effective control and management of retinal conditions that were previously nearly untreatable.

In contrast, the dry AMD market, which accounts for more than 80% of all AMD cases, remains largely untapped, with no effective therapeutic or preventive drugs currently available. As the cornerstone of current dry AMD treatment strategies, complement inhibitors are poised to access a market four to five times larger than that of wet AMD (wAMD) upon successful clinical validation. Will complement therapies ignite the next wave of innovation following the anti-VEGF era? The future holds great promise.

Rapid Progress of Biosimilars in China, While Innovative Drug Development Still Faces Challenges

In recent years, China has made rapid progress in the research and development of ophthalmic biosimilars, particularly in the field of anti-VEGF drugs. Several biosimilars have already been approved for marketing in China, such as QL1205, a ranibizumab biosimilar developed by Qilu Pharmaceutical. In addition, companies like Innovent Biologics and Kelun Pharmaceutical are actively expanding their presence in the ophthalmic therapeutics sector, with multiple Class 1 innovative drugs and first-to-market generics currently under development.

Despite progress in biosimilars, there remains a certain gap between China and the United States in the research and development of innovative ophthalmic drugs, and the landscape for new ophthalmic drug development is distinctly different.

According to previous research by VCBeat, the U.S. ophthalmic drug market has an early start. After a series of mergers and acquisitions, R&D companies in this field have become more focused and concentrated among leading players. Whether it involves small molecules, large molecules, or gene therapies, they are largely dominated by major corporations such as Novartis, Roche, and Bausch + Lomb.

China presents a different landscape. In recent years, with the influx of capital and the return of outstanding scientists to launch startups, Chinese ophthalmic innovative drug companies have emerged in large numbers. Patent technologies are fragmented across various small firms, with high-quality enterprises present in each niche segment—such as Rayming Pharma and Weimu Biopharma in the small-molecule sector, and Innovent Biologics and Kanghong Pharmaceutical in the large-molecule sector. In other words, China has not yet produced a truly leading innovator in the ophthalmic drug industry.

Meanwhile, as China’s ophthalmic innovative drug sector is still in its nascent stage, certain challenges are inevitable. First, at the capital level, R&D funding for domestic ophthalmic innovative drugs primarily comes from investment institutions, which tend to be more risk-averse. This has resulted in most currently pipeline ophthalmic innovative drugs being “de-risked” assets, predominantly based on external licensing-in rather than independent innovation, with very few truly first-in-class drugs being developed. While this strategy may yield short-term achievements, it fails to address fundamental technical issues in the long run, making it imperative to strengthen independent innovation efforts.

Secondly, at the regulatory approval level, the National Medical Products Administration (NMPA) of China is still in the process of gradually improving regulations for the ophthalmic innovative drug sector, making the approval communication process a significant factor constraining R&D speed. Currently, the United States has a mature regulatory framework for ophthalmic innovative drugs, whereas the NMPA lacks experience in approving such drugs for conditions like wet age-related macular degeneration and dry eye disease, resulting in slower approval speeds. This poses challenges to companies' R&D progress and market access.

Furthermore, in more cutting-edge fields such as cell and gene therapy, the lack of relevant domestic products has resulted in unclear regulatory and approval laws and regulations in the current market, posing certain challenges to pioneering enterprises.

Finally, from a corporate perspective, the number of participants in the ophthalmic drug sector is increasing. Companies must identify precise positioning and areas of expertise, while selecting appropriate disease indications, commercial operational models, and R&D and regulatory strategies. Furthermore, regarding corporate strategy, external in-licensing serves merely as a supplementary approach; the most critical factor remains internal R&D capability. Greater confidence and patience are required for first-in-class drugs, which carry higher R&D risks, to foster independent innovative R&D and attract more outstanding scientists to the field of innovative ophthalmic drug development.

In the future, as China cultivates more innovative talent in ophthalmology and the industry becomes increasingly standardized, the gap between China and the United States in the research and development of innovative ophthalmic drugs will continue to narrow. A diverse array of drugs, mechanisms, and therapies will continually emerge, fostering a vibrant landscape across specialized segments and ultimately establishing a robust ecosystem for innovative ophthalmic drug development. We look forward to witnessing this progress.

References:

The Power of “Visibility”: Analysis of a Billion-Dollar Ophthalmology Pipeline Candidate—Asymchem

Capital Influx, Heated Sector: How to Build a Healthy Ecosystem for Ophthalmic New Drug R&D? — VCBeat

In 2023, the FDA Approved These 12 Novel Ophthalmic Drugs for Dry Eye Disease, Presbyopia, Mydriasis, and More—Eye Care Insight