Two Domestic IL-17A Inhibitors Approved Simultaneously as Nine Others Reach Phase III: China's Autoimmune Drug Race Heats Up Beyond PD-1

GENRIX BIO

Developer of Novel Monoclonal Antibody Drugs

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

For years, the IL-17A target has been regarded as a blockbuster segment in autoimmune disease therapeutics; however, over the past five years, this sector has been monopolized by imported products.

Recently, the National Medical Products Administration (NMPA) of China approved the market launch of two domestically produced IL-17A monoclonal antibody drugs: secukinumab from GENRIX BIO and funakizumab from Hengrui Pharma. Both drugs are indicated for the treatment of moderate-to-severe plaque psoriasis. The simultaneous approval of these two drugs, which share the same therapeutic area, target, and indication, within a single day is set to break the monopoly held by imported drugs in the IL-17A treatment landscape.

The immunology sector is a hotbed for blockbuster drugs, with competition around identical targets never ceasing. With the approval of domestically developed new drugs and nearly ten Chinese candidates in Phase III clinical trials poised for launch, this niche market is set to witness a three-way rivalry among multinational corporations (MNCs), biotech firms, and local pharmaceutical companies.

The era of Novartis’s secukinumab dominating the psoriasis treatment landscape in China will eventually come to an end.

The core objectives of psoriasis treatment are to control symptoms and improve patients' quality of life. For patients who respond poorly to conventional therapies, targeted biologic agents have emerged as a superior option. After years of development, interleukin (IL) inhibitors have gradually replaced tumor necrosis factor-alpha (TNF-α) inhibitors as the mainstream treatment. In particular, IL-17 inhibitors have become an important therapeutic approach in clinical practice.

IL-17 inhibitors secukinumab (Novartis) and ixekizumab (Eli Lilly) achieved global sales of $4.98 billion and $2.76 billion, respectively, in 2023.

In the Chinese market, secukinumab was approved for launch in 2018 for the treatment of moderate-to-severe plaque psoriasis, psoriatic arthritis, and ankylosing spondylitis in adults. Ixekizumab followed closely, receiving approval in China in 2019. According to data from Menet, the domestic sales of these two imported drugs increased from RMB 2.08 billion and RMB 230 million in 2022 to RMB 2.75 billion and RMB 370 million in 2023, respectively.

The rapid growth of China’s psoriasis market has spurred the swift development of IL-17 monoclonal antibody drugs.

According to Frost & Sullivan, the domestic psoriasis drug market in China has witnessed rapid growth in recent years, with its size surging from $604 million in 2018 to $1.436 billion in 2022, representing a compound annual growth rate (CAGR) of 24.2%. The market is projected to continue expanding in the coming years, reaching an estimated $3.255 billion by 2025. Furthermore, the share of biosimilars in the psoriasis drug market is steadily increasing, with their proportion expected to rise from less than 30% in 2021 to over 50% by 2030.

It is precisely due to the growing market demand for this class of drugs, coupled with the untapped therapeutic potential of IL-17 inhibitors in oncology, that numerous pharmaceutical companies have flocked to enter this space.

In July this year, UCB’s bimekizumab was approved in China, becoming the world’s first dual inhibitor targeting both IL-17A and IL-17F. However, the approved indication is limited to ankylosing spondylitis, excluding psoriasis, which has been approved abroad. This was followed by the approvals of GENRIX BIO’s secukinumab-like antibody (sailiqimab) and Hengrui Pharma’s funakizumab, marking the formal entry of domestic players into the Chinese market.

Based on previous clinical data, the proportion of psoriasis patients achieving a 75% reduction in Psoriasis Area and Severity Index (PASI 75) with secukinumab reached 90.7% at Week 12, while the proportion achieving PASI 90 was 74.4%. The PASI 75/90 response rates remained stable through Week 52, with a relapse rate of only 0.4%, demonstrating the stability of long-term efficacy. Most adverse reactions were mild or moderate in severity, with the most common being upper respiratory tract infections, hyperlipidemia, and injection site reactions.

Another approved funakizumab, an IL-17A inhibitor developed by Hengrui Pharma, also demonstrated significant improvement in moderate-to-severe plaque psoriasis in its Phase 3 clinical data, with a favorable long-term safety and tolerability profile.

For the two domestically produced new drugs, regulatory approval is merely the beginning. Based on previously disclosed filing information, their market launch has been delayed relative to the original schedule. This means they must now contend with the barrier posed by competitors holding first-mover advantage, while also facing intense pressure from numerous followers close behind.

A Rush of Project Approvals May “Block Off” This Niche Sector.

Novartis’s secukinumab has demonstrated exceptional commercial performance, successfully elevating attention to the IL-17A target in the field of psoriasis and attracting numerous market participants.

Currently, four imported products have been approved in China: Novartis’s secukinumab, Eli Lilly’s ixekizumab, Kyowa Kirin’s brodalumab, and UCB’s bimekizumab. With the addition of two newly approved domestic drugs, competition has become intense. However, more than ten other companies are closely trailing behind.

Leading IL-17 Targeted Drugs Under Development in China, Compiled from Public Corporate Disclosures

Several pharmaceutical companies, including Akeso, 3SBio, Livzon Pharmaceutical, and Junshi Biosciences, have IL-17A monoclonal antibodies in Phase III clinical trials. More critically, with the patents for imported originator drugs nearing expiration, the market is also poised to face a surge of generic competitors.

Taking secukinumab as an example, its core patent in China was granted in 2012 and is set to expire in 2025, while the patent protection for ixekizumab will also expire in 2026. Currently, pharmaceutical companies such as CSPC Pharma, Bio-Thera Solutions, and BoRui Biologics have entered this space, with Bio-Thera Solutions making the most rapid progress by advancing to Phase III clinical trials.

Based on clinical data, it can be inferred that new drugs from Chinese pharmaceutical companies are generally launched approximately three years before the expiration of the originator drug’s patent, resulting in a relatively narrow window of opportunity. These companies must not only address competition from rivals with first-mover advantages but also contend with the subsequent impact of generic drugs.

“Project initiation capability is particularly critical for enterprises.” An investor told VCBeat, “In the current environment, corporate project initiation must either be fast enough to achieve First-in-Class status, or novel enough to not only address urgent clinical needs but also attract purchases from multinational corporations (MNCs). Meanwhile, market size must be guaranteed; only with a sufficiently large market can projects rapidly achieve commercial implementation through strategic business approaches, even if development is somewhat slower or competition is more intense.”

From the perspective of domestic enterprises, the rush into IL-17 development is a move born of necessity.

Biologics for psoriasis can be broadly categorized into first-generation agents, represented by TNF-α inhibitors (adalimumab) and IL-12/IL-23 inhibitors (ustekinumab), and second-generation agents, including IL-17 pathway inhibitors (secukinumab, ixekizumab, brodalumab, bimekizumab) and IL-23p19 inhibitors (guselkumab, risankizumab).

It is worth noting that in numerous previous head-to-head clinical trials, IL-17 inhibitors have demonstrated superior efficacy compared to TNF-α, IL-12/IL-23, and IL-23p19 inhibitors. Meanwhile, both IL-17A and IL-17F, members of the IL-17 cytokine family, are implicated in inflammatory processes; this allows for therapeutic strategies targeting either a single agent or both simultaneously, as well as dual-targeting approaches in combination with other cytokines. Furthermore, given IL-17’s role beyond autoimmune diseases—extending to oncology—the substantial potential for innovation has naturally attracted significant interest from pharmaceutical companies.

From a timeline perspective, with the sequential launch of second-generation drugs between 2015 and 2019, multinational corporations (MNCs) have already established proof of concept, indicating relatively low risk in drug development. Consequently, Chinese pharmaceutical companies have successively initiated their own programs. However, given that the IL-17 sector is now experiencing intense competition akin to that seen with PD-1 inhibitors, future commercialization strategies remain a challenge. Insights may be drawn from the commercialization pathway of secukinumab.

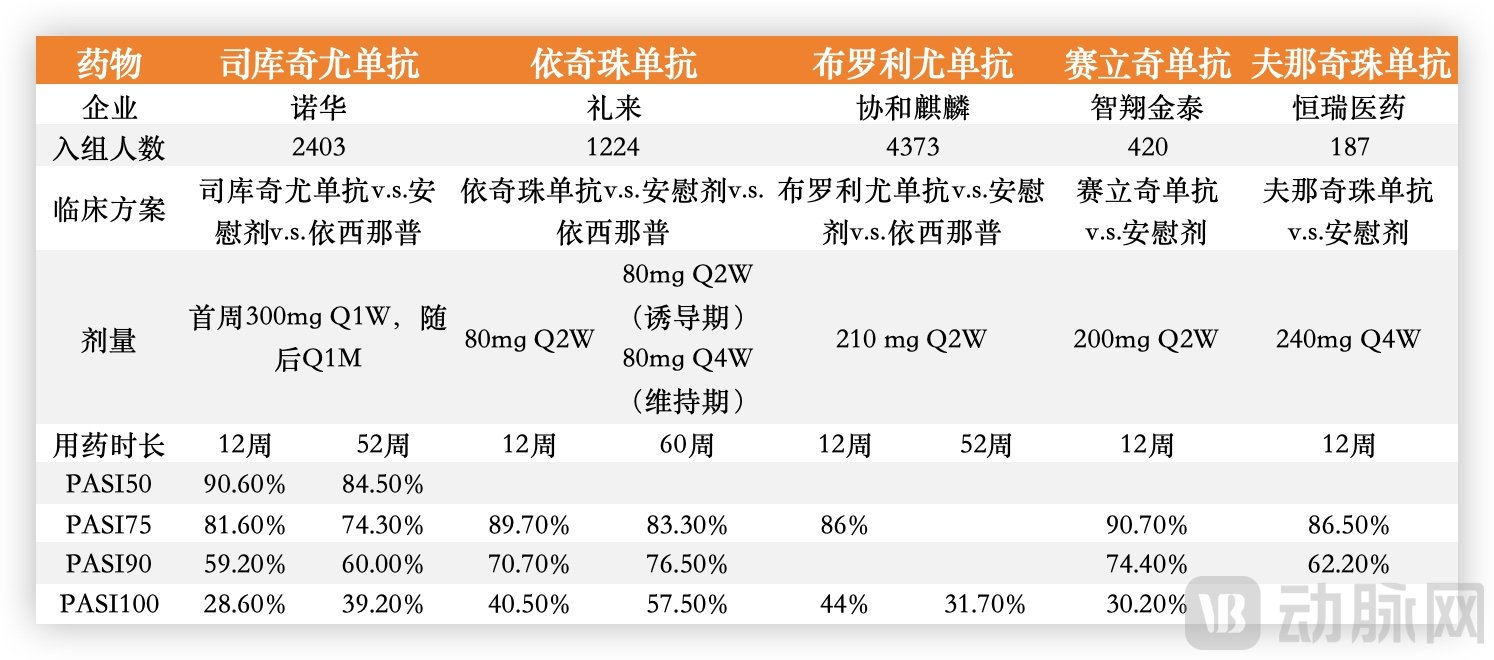

Clinical data for domestically produced IL-17A-targeted drugs are comparable to those of imported drugs, laying the foundation for competition.

Based on clinical data, after 12 weeks of treatment, the two newly approved domestic IL-17A monoclonal antibodies demonstrated efficacy comparable to that of imported drugs, and even surpassed marketed imported agents in certain disclosed metrics such as PASI75 and PASI90 (though not from head-to-head trials). However, clinical performance is only one aspect; Secukinumab’s competitive strategy must be evaluated comprehensively.

Clinical Data of IL-17 Drugs Approved in China (Non-Head-to-Head), Compiled from Public Information

Rapid onset of action is a hallmark of secukinumab. In the Phase 3 CLEAR head-to-head clinical trial comparing secukinumab with the IL-12/IL-23 inhibitor ustekinumab, the PASI 75 response rate in the secukinumab group was significantly superior to that in the ustekinumab group as early as Week 1. By Week 2, secukinumab demonstrated significantly higher PASI 90 and IGA 0/1 response rates, and by Week 4, it achieved a significantly higher PASI 100 response rate.

Therefore, even though secukinumab demonstrates inferior long-term efficacy compared with other IL-23 inhibitors, such as risankizumab and guselkumab, in head-to-head clinical trials, it still maintains sufficient competitiveness. On the other hand, Novartis has recognized the weakness of secukinumab in long-term efficacy and has adopted a strategy of expanding its indications.

Secukinumab was approved by the U.S. FDA and in Europe in January 2015 for the treatment of patients with moderate-to-severe plaque psoriasis. One year later, the U.S. FDA further approved it for ankylosing spondylitis and psoriatic arthritis. Subsequently, two additional indications—axial spondyloarthritis and hidradenitis suppurativa—were added in 2020 and 2023, respectively. Furthermore, marketing applications for three new indications—giant cell arteritis, tendinopathy, and polymyalgia rheumatica—are expected to be submitted annually after 2025.

Thanks to its comprehensive strategic layout, secukinumab achieved global sales of $261 million in the first year following its launch in 2015, subsequently maintaining rapid growth. By 2023, it generated global revenue of $4.98 billion, including $2.636 billion from the United States. Meanwhile, the commercialization of secukinumab in China has also been successful.

In 2019, Novartis announced the results of a Phase 3 clinical study involving 441 Chinese patients with moderate-to-severe plaque psoriasis treated with secukinumab. The data showed that nearly 90% of patients receiving secukinumab 300 mg achieved clear or almost clear skin within 16 weeks, with rapid symptom relief observed as early as Week 3 after treatment initiation. In terms of efficacy and safety, the outcomes were even superior to some international clinical data.

Following its market approval, Novartis did not limit its focus to first- and second-tier cities; instead, it launched the “Silver-Free in a Thousand Counties” initiative to drive market penetration into lower-tier regions. In the first half of 2023 alone, more than 300 county-level hospitals completed epidemiological surveys and were accredited as specialized psoriasis clinics, while 1,004 dermatologists in county-level areas received certification for enhanced primary care capabilities in psoriasis diagnosis and treatment. Through these efforts, Novartis also achieved significant market education. Furthermore, by leveraging medical insurance coverage and medical consortia, Novartis has continued to expand its distribution channels into lower-tier markets, thereby improving drug accessibility.

In terms of pricing, secukinumab was launched in China in April 2019 at a price of RMB 2,998 per pre-filled syringe. In 2020, it was included in the National Reimbursement Drug List (NRDL), with its price reduced from RMB 2,998 to RMB 1,188 per pre-filled syringe. In 2023, secukinumab was renewed for NRDL coverage at a further reduced price of RMB 870 per pre-filled syringe. Based on this pricing, the estimated annual treatment cost for secukinumab is approximately RMB 35,640 during the induction phase and RMB 28,512 during the maintenance phase. To improve drug accessibility, Novartis partnered with Gaoji Medical to launch the “Supporting You All the Way” patient assistance program, under which eligible patients can receive rebates on part of their medication costs.

It is precisely by leveraging a multi-dimensional combination of strategies across project initiation, clinical strategy, indication expansion, and commercialization that secukinumab has achieved sustained and rapid growth in its sales volume in China.

Following in the Footsteps of Secukinumab: The Choice of Domestic Biosimilars.

Taking domestically approved and investigational drugs as examples, their development directions can be assessed based on currently ongoing clinical trials. It is evident that, in addition to psoriasis, the primary indications under development are ankylosing spondylitis, axial spondyloarthritis, Crohn's disease, and lupus nephritis.

Selected Domestic IL-17 Clinical Trials: Data Sourced from ClinicalTrials.gov and the Center for Drug Evaluation (CDE)

Domestic IL-17 inhibitors have made significant efforts to achieve differentiation. Secukinumab by GENRIX BIO adopts a fully human IgG4 antibody, offering higher affinity and stronger activity. Funakizumab, approved at the same time, has expanded its indications beyond psoriasis to include psoriatic arthritis, lupus nephritis, Graves' ophthalmopathy, and axial spondyloarthritis.

Notably, axial spondyloarthritis (axSpA), a therapeutic area targeted by multiple pharmaceutical companies, is primarily categorized into ankylosing spondylitis (AS) and non-radiographic axial spondyloarthritis (nr-axSpA). According to a domestic epidemiological survey, the current prevalence of axSpA among adults in China is approximately 0.507%, with an estimated patient population of around 6 million. However, this niche segment will also face competition from TNF-α inhibitors and their biosimilars.

Furthermore, as the first domestically produced dual IL-17A/F inhibitor, LZM012, developed by Livzon Pharmaceutical Group and Xinkanghe Biopharma, is undergoing a Phase 3 head-to-head clinical trial against secukinumab for the treatment of psoriasis. The primary endpoint is the proportion of subjects achieving a 100% improvement in the Psoriasis Area and Severity Index (PASI 100 response rate) at Week 12. According to information published on the website of the Center for Drug Evaluation, enrollment for this study has been fully completed.

From a developmental perspective, improving patient adherence is a key focus in the treatment of psoriasis, and related biologics have been continuously optimizing their dosing regimens in recent years. Taking secukinumab as an example, it was initially approved in China as a pre-filled syringe and later upgraded to the Autoinjector Pen, which features a hidden needle design aimed at reducing patients’ anxiety about injections. The emergence of injection pens aligns with the current trend toward more convenient drug administration, reduces the need for fine motor skills, and provides patients with a superior treatment experience.

Selected Oral Formulations Under Investigation, Compiled from Public Information

On the other hand, many pharmaceutical companies have recognized that injections are inherently less convenient than oral administration, prompting them to develop oral formulations. For instance, Eli Lilly’s DC-806 and DC-853 are oral drugs targeting IL-17A, currently in Phase II and Phase I clinical trials, respectively. Chengdu HitGen in China has also made strategic moves in this area. It is not only the IL family; small-molecule targeted therapies, including those against TYK2 and PDE4, are also focusing on the oral psoriasis market and are at advanced stages of development. In the future, IL-17 biologics will face competition from these agents.

Overall, the domestic autoimmune market, represented by IL-17 inhibitors, is on the verge of intense competition. However, participants’ performance has yet to win market favor; the recent approvals of GENRIX BIO and Hengrui Pharma failed to generate significant ripples in the secondary market. On one hand, the success of secukinumab demonstrates that promoting psoriasis drugs requires robust channel capabilities. On the other hand, the influx of domestic competitors has made it difficult for the market to determine which players possess genuine clinical efficacy, channel advantages, flexible pricing strategies, and strong commercialization capabilities.

The fierce nature of future market competition is beyond doubt; we await to see who can stand out by relying on their comprehensive capabilities in such an environment.