Health Insurance Unicorn Yuanbao Files for Nasdaq IPO with Over $2 Billion Annual Revenue, Backed by Nearly 10 Top-Tier Investors

Five years after its establishment, Yuanbao Inc. (hereinafter referred to as “Yuanbao”) has decided to make a push for an initial public offering (IPO).

On September 17 (U.S. Eastern Time), health insurance innovator Yuanbao filed an F-1 registration statement with the U.S. Securities and Exchange Commission (SEC), planning to list on the Nasdaq under the ticker symbol “YB.” Goldman Sachs, Citigroup, CICC, and Tiger Brokers are serving as underwriters for this initial public offering (IPO).

Since its establishment in 2019, Yuanbao has been a “star enterprise,” favored by numerous investors. To date, Yuanbao has completed four rounds of financing, with well-known institutions such as Shanxing Capital, Northern Light Venture Capital, Qiming Venture Partners, SIG Asia Investments, Source Code Capital, and Kaihui Fund among its investors. Notably, Shanxing Capital, Northern Light Venture Capital, Qiming Venture Partners, and SIG have participated in multiple financing rounds of Yuanbao.

To date, Yuanbao’s product strategy has evolved into a well-defined system—centered on inclusive health insurance and short-term insurance products to target the lower-tier markets, thereby carving out a differentiated path within the broader health insurance industry:

· In terms of geographic distribution, leveraging digital advertising, Yuanbao has extended its insurance services to broader regions, including mountainous areas and villages.

· In terms of product accessibility, Yuanbao has introduced customized innovations in coverage scope and payment methods through product customization, significantly lowering the barrier for users to obtain insurance protection.

· In terms of population coverage, Yuanbao has developed tailored insurance products for specific groups that are often underserved by traditional insurance services, including the elderly, individuals with non-standard health profiles, new urban residents, and flexible workers.

▲ Yuanbao’s Revenue Performance Source: Prospectus

▲ Yuanbao’s Revenue Performance Source: Prospectus

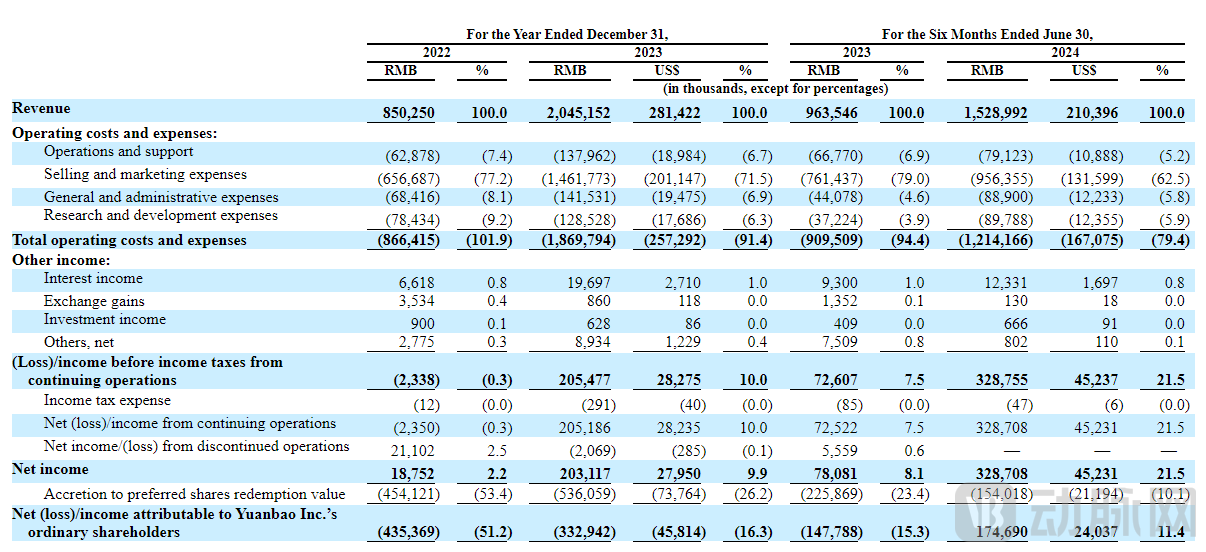

In terms of specific revenue, the prospectus shows that Yuanbao's main business revenues for 2021, 2022, and 2023 were RMB 385 million, RMB 850 million, and RMB 2.045 billion, respectively,The annual growth rates were 121% and 141%, respectively.During the same periods, Yuanbao’s net losses attributable to shareholders were RMB 1.218 billion, RMB 435 million, and RMB 333 million, respectively. In the first half of 2024, Yuanbao reported revenue of RMB 1.529 billion and net profit attributable to shareholders of RMB 174 million.

Behind the Ultra-High Growth Rate: What Did Yuanbao Get Right?

“Yuanbao must find a course with deeper snow and a longer slope.”

In a previous interview with VCBeat, Li Ying, co-founder and vice president of Yuanbao, told VCBeat. According to the introduction,Nearly all of Yuanbao’s core founding team members have prior work experience at NetEase.For example, Fang Rui, founder and CEO of Yuanbao, has 17 years of work experience at NetEase. He previously served as Vice President of NetEase Group and Head of the Technology Department, founded NetEase E-commerce and NetEase Pay, and served as their CEO. Li Ying, co-founder and Vice President, formerly served as Vice President of NetEase’s E-commerce Division...

While at NetEase, Li Ying’s department identified the significant opportunities embedded in internet insurance during an exchange with an Australian insurance brokerage platform, and subsequently launched an internet insurance project in 2011. However, constrained by the immature market environment and technological limitations at the time, the project failed to achieve substantial growth.

In 2019, the founding team, deeming the timing ripe, established Yuanbao and formally entered the internet insurance sector. In June 2020, Yuanbao successfully obtained a nationwide insurance brokerage license. In October of the same year, Yuanbao completed the filing for its online insurance business.

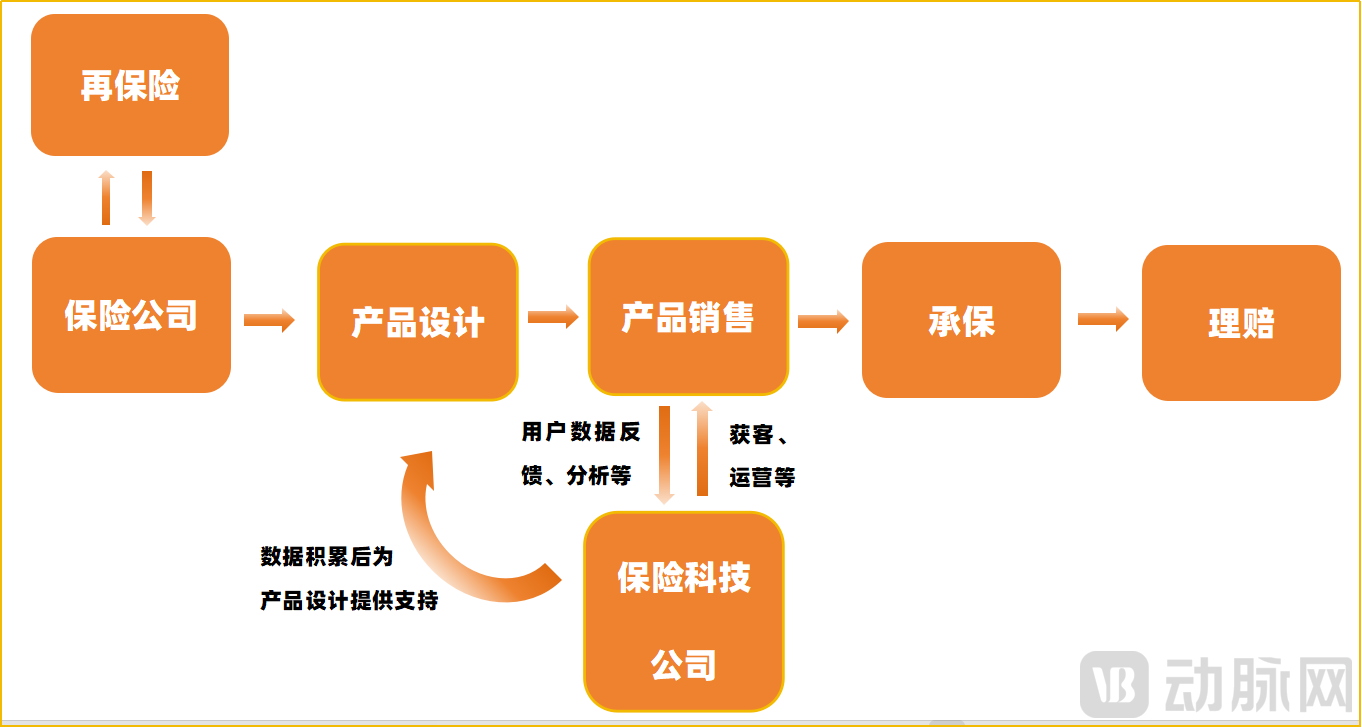

It is worth noting that the insurance industry chain encompasses multiple stages, including product design, sales, underwriting, and claims settlement. Yuanbao has entered the market as an intermediary focusing on the sales segment, positioning itself as a technology-driven online insurance distributor. Its primary business involves customizing and distributing insurance products in partnership with insurance companies, while also providing post-sales services such as claims assistance to customers.

▲ Position of InsurTech Companies in the Insurance Industry Chain

▲ Position of InsurTech Companies in the Insurance Industry Chain

VCBeat Graphic

In simple terms, Yuanbao’s role is to help insurance companies acquire users and assist users in finding suitable insurance products. Additionally, based on user needs, it enables insurance companies to reverse-customize personalized health insurance products.

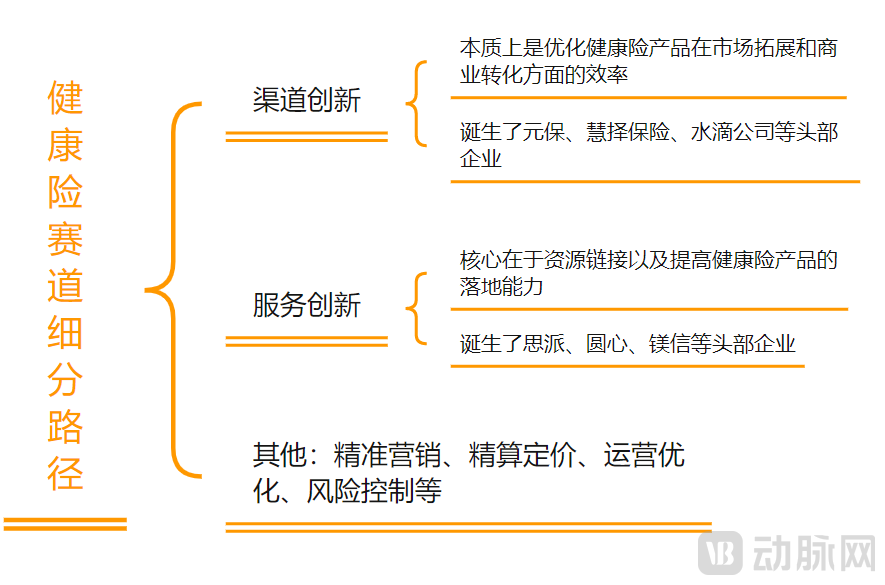

Furthermore, from a business perspective, health insurance companies can be broadly categorized into three major groups: channel innovation, service innovation, and others (including precision marketing, actuarial pricing, risk control, etc.). Yuanbao is a representative enterprise in the category of channel innovation.

However, at that time, the channel innovation sector was highly competitive, featuring numerous players such as Ant Insurance, Tencent WeSure, Shuidi, Huize Insurance, Qingsongchou, Baibaojun, Woniu Insurance, Xiaobang, Duobaoyu, and Shenlanbao. The key to success lay in establishing differentiation amidst this intense competition.

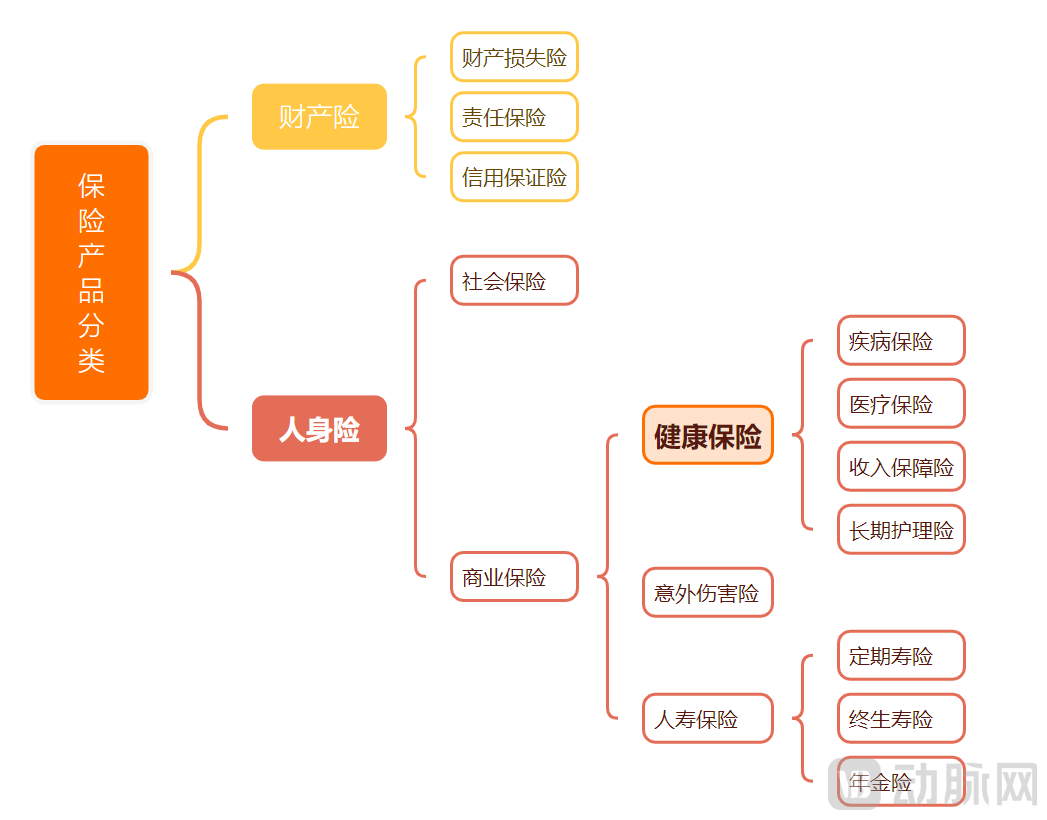

▲ Above: Classification of Insurance Types (Non-exhaustive)

Figure below: Segmentation pathways in the health insurance sector

Yuanbao has chosen to enter the niche segment of inclusive health insurance, going all-in on lower-tier markets.

In response, Yuanbao has built a diversified product matrix in the inclusive health insurance sector to meet the essential needs of the general public. For instance, in collaboration with insurance companies, Yuanbao has customized and launched a series of products, including Yuanbao Million Medical Insurance, Yuanbao Critical Illness Insurance, Yuanbao Inclusive Health Insurance, and Yuanbao Online Consultation and Medication Purchase Insurance, as well as Yuanbao National Million Medical Insurance tailored for individuals in sub-optimal health conditions, and Yuanbao Million Cancer Insurance designed for the elderly.

Additionally, to enhance the inclusiveness of its insurance products, Yuanbao has implemented comprehensive product customization innovations—such as tailoring coverage scopes and payment methods—thereby lowering the threshold for users to obtain protection.

With its unique product strategy, Yuanbao’s user base has been steadily expanding.The prospectus shows that in 2022 and 2023, Yuanbao's number of insurance consumers reached 4.6 million and 8.1 million respectively, nearly doubling.

Meanwhile, regarding claims data, Yuanbao’s recently released “2024 Semi-Annual Report on Health Insurance Claims” shows that in the first half of 2024, over 70% of Yuanbao’s claims users came from third-tier cities and below. At the same time, Yuanbao’s medical insurance covered 81% of out-of-pocket expenses (i.e., costs not covered by basic medical insurance) for users in these regions. This demonstrates that Yuanbao has achieved extensive penetration among consumers in lower-tier markets.

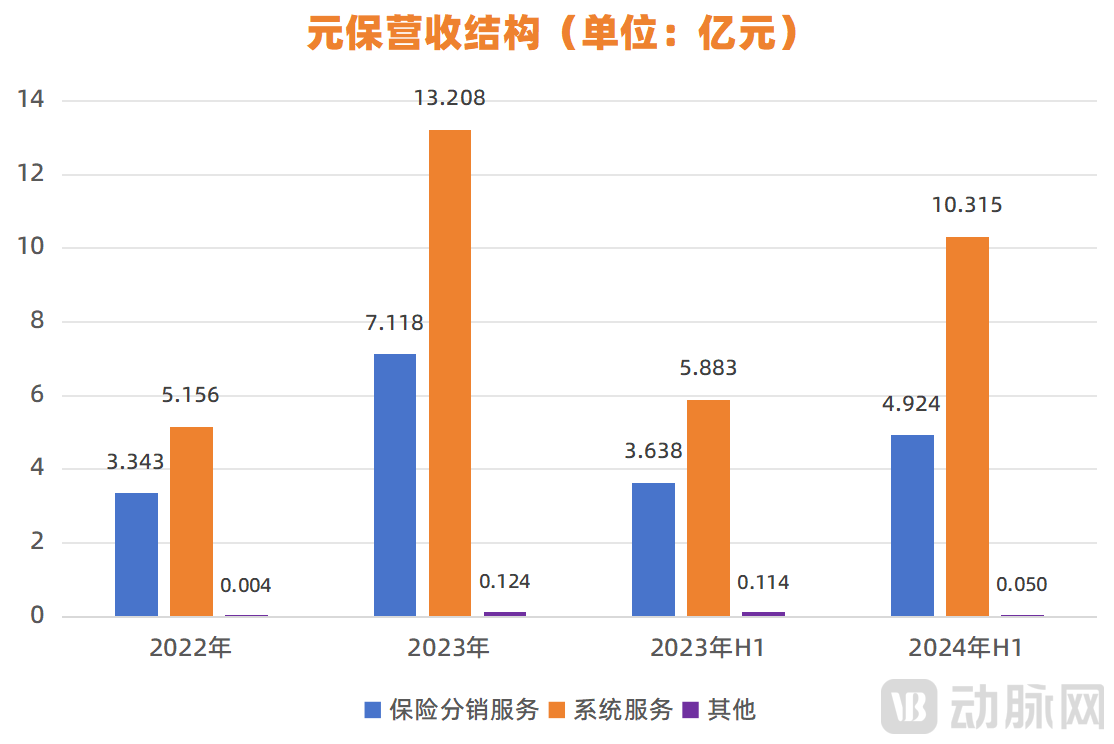

Leveraging its vast user base and consumer behavior data, Yuanbao has also been progressively providing insurers with a suite of services, including precision marketing and data analytics.At this point, insurance distribution services and system services provided to insurance companies have become the two pillars of Yuanbao’s revenue., driving its total annual revenue to achieve a year-over-year growth rate of over 120% in both 2022 and 2023.

According to the prospectus, Yuanbao’s revenue from insurance distribution services amounted to RMB 334.3 million and RMB 711.8 million in 2022 and 2023, accounting for 39.3% and 34.9% of total revenue, respectively. During the same period, revenue generated from providing system services totaled RMB 515.6 million and RMB 1.3208 billion, representing 60.6% and 64.5% of total revenue, respectively. Revenue from other services, such as assisting insurance companies in producing promotional videos for insurance products, was RMB 400,000 and RMB 12.5 million, respectively, constituting a negligible share of total revenue.

▲ Source: Prospectus; Graphic by VCBeat

▲ Source: Prospectus; Graphic by VCBeat

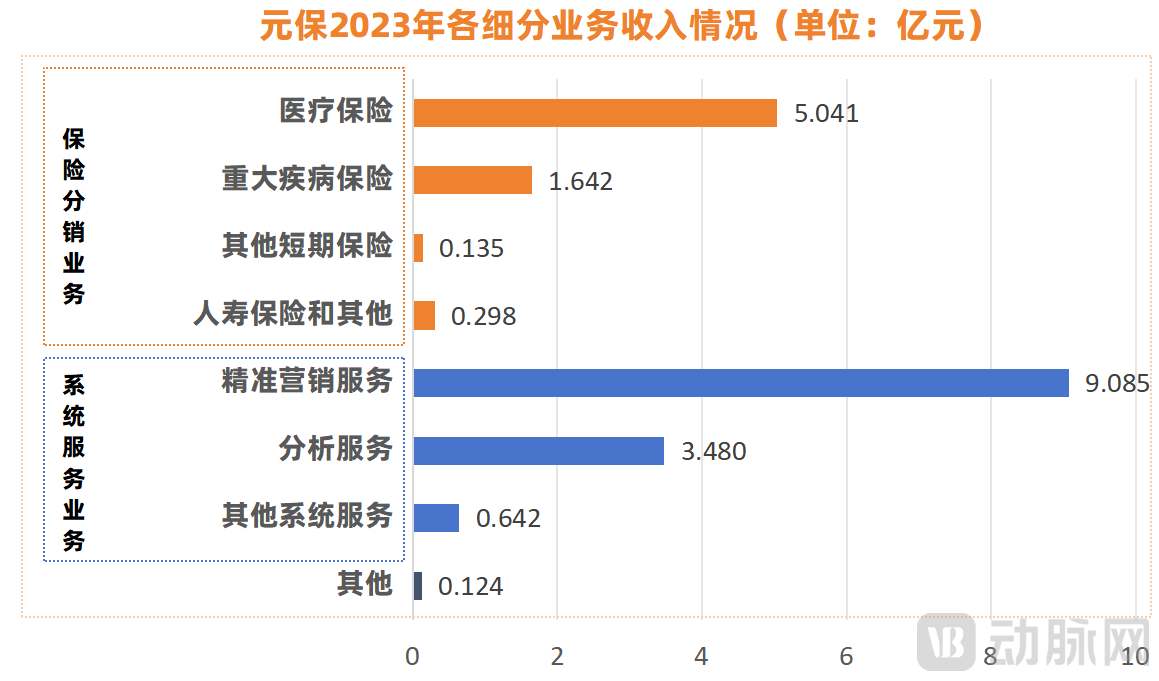

Further refining the business insights, in 2023, precision marketing services and the distribution of medical insurance ranked as the top two revenue-generating businesses, accounting for 44.4% and 24.7% of total revenue, respectively.

▲ Source: Prospectus; Graphic by VCBeat

▲ Source: Prospectus; Graphic by VCBeat

Sustained high revenue growth has steadily solidified Yuanbao’s market position. According to the latest data from Frost & Sullivan, Yuanbao has become the second-largest distributor in China’s life insurance market when measured by first-year premiums; furthermore, if affiliated insurance distributors incubated by major internet tech giants are excluded, Yuanbao is already the largest independent insurance distributor in China’s life insurance market.

Undoubtedly, the performance results have proven the success of Yuanbao’s unique product strategy of focusing on inclusive insurance and penetrating lower-tier markets. However, while choosing the right direction is crucial, the true test of a company’s operational management lies in effectively implementing its products. In this regard, what innovative attempts has Yuanbao made?

In traditional insurance distribution, reaching end users often relies heavily on a large workforce, leading to the industry-wide problem of low personnel efficiency. Since the emergence of internet insurance, acquiring users through online channels such as websites and mobile devices has become a key focus for innovative enterprises.

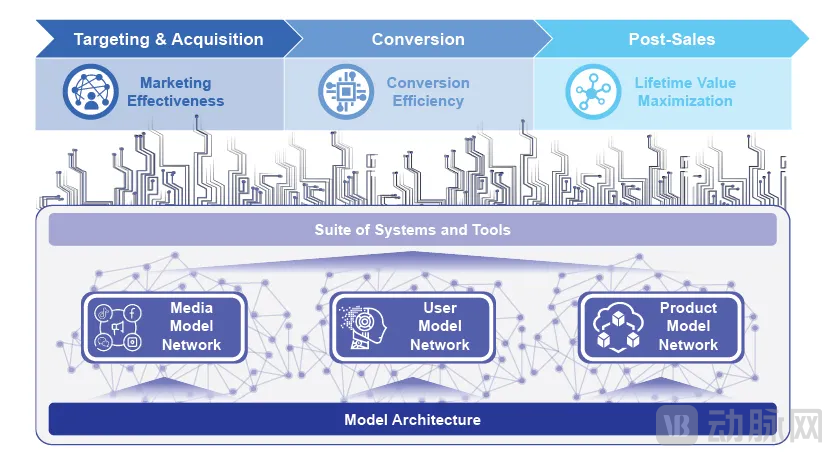

However, as more companies enter the market and online traffic becomes increasingly expensive, achieving more precise customer acquisition has become key to improving industry efficiency.Along this path, Yuanbao has adopted a strategy of integrating AI technology into every stage of insurance distribution and claims processing, transforming traditional insurance sales activities from being human-resource-driven to AI-driven, thereby enhancing the experience and efficiency of insurance sales and after-sales services such as claims handling in China.

According to the prospectus, Yuanbao has established an efficient full-lifecycle consumer service engine to provide personalized services for every insurance user, including customized product recommendations and customization, purchase, policy management, claims processing, and after-sales support.

▲ Schematic Diagram of Yuanbao’s Model Architecture Image Source: Prospectus

▲ Schematic Diagram of Yuanbao’s Model Architecture Image Source: Prospectus

Specifically, in the distribution and claims processing of insurance products, Yuanbao has leveraged AI technology and big data to develop an interconnected model network spanning user, media, and product dimensions. As of June 30, 2024, Yuanbao had developed over 700 media models, more than 3,000 user models, and nearly 700 product models.

Leveraging these model networks, Yuanbao is able to operate across a wide range of scenarios—from initial user targeting and acquisition, through sales conversion, to after-sales service—while continuously optimizing the service journey for each potential consumer.

So, how exactly is it implemented?

In this regard,The prospectus presents a case study.: First, after selecting an inclusive insurance product, Yuanbao establishes partnerships with popular social media platforms to identify potential internet users who match the product’s profile by filtering through user tags such as occupation type, age range, and consumption preferences. Once Mr. X is identified as a target user, content models engage his interest with tailored content and present advertisements for the inclusive insurance product. If Mr. X shows interest, he is directed to Yuanbao’s self-operated platform for more information. During the conversion process, user models and product models provide precise product recommendations tailored to the user segment to which Mr. X belongs.

Once Mr. X purchases the relevant products, Yuanbao will cultivate a long-term service relationship with him and respond promptly during the claims process. Furthermore, throughout the course of ongoing services, Yuanbao will recommend policies tailored to Mr. X’s specific circumstances and needs, including child protection, critical illness insurance, and long-term care insurance, thereby achieving sustained operational effectiveness.

Data shows that Yuanbao's user stickiness continues to strengthen.In 2022 and 2023, Yuanbao’s active user retention rates were 11.3% and 27.6%, respectively, indicating that while maintaining rapid business growth, Yuanbao was also able to extend the duration of engagement with its existing active users.

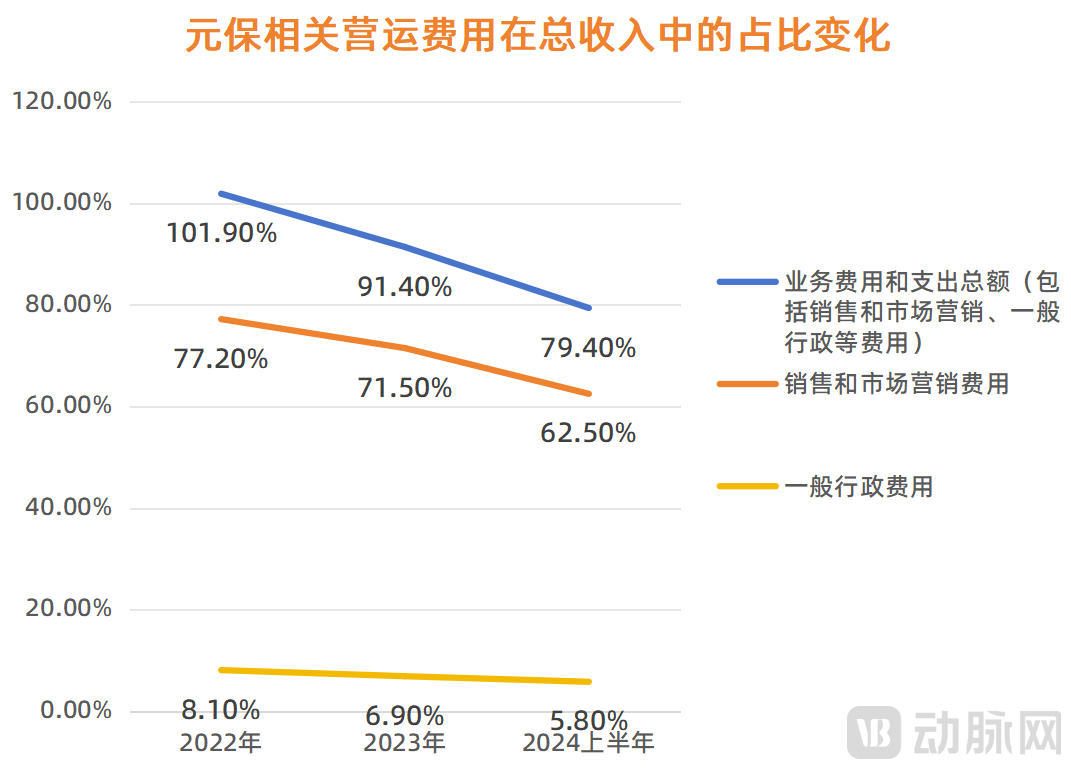

Reflected in financial performance, this translates into continuously optimized profitability. Data shows that Yuanbao’s operating costs and expenses as a percentage of total revenue have decreased from 101.9% in 2022 to 91.4% in 2023, and further declined to 79.4% in the first half of 2024, indicating the company’s sustained improvement in operational efficiency.

▲ Source: Prospectus; Graphic by VCBeat

▲ Source: Prospectus; Graphic by VCBeat

Thanks to the concurrent implementation of the aforementioned measures, Yuanbao has successfully achieved profitability. The prospectus shows that Yuanbao’s net profit attributable to shareholders in the first half of 2024 reached RMB 174.6 million.

As a sector once heavily favored by capital, the health insurance industry was once scorching hot.

Data from the VCBeat database shows that from January 2020 to June 2021 alone, there were over 35 primary market financing events in China’s health insurance sector, with total funding exceeding RMB 10 billion. Major players such as Sequoia Capital, Hillhouse Capital, Tencent, and Ant Group frequently appeared on the list of investors.

However, starting in October 2021, the rapid growth momentum of the health insurance industry cooled down quickly due to the introduction of a series of stringent regulatory policies, including the new regulations on internet-based personal insurance, as well as the gradual disappearance of internet dividends. Many once-popular companies have since shifted their business focus. To this day, the health insurance industry has not regained its former fervor.

In this regard, one prevailing view in the market holds that there are significant differences between China’s commercial health insurance sector and its U.S. counterpart; therefore, it is unreasonable to forecast the development of China’s health insurance industry by drawing parallels with the U.S. market:

· First, under China’s broad national health insurance coverage, commercial health insurance is not a necessity compared to the U.S. market, resulting in low user reliance on health insurance products;

· Second, Chinese consumers have insufficient awareness of health insurance, resulting in prohibitively high user education costs. Consequently, demand for health insurance in China remains questionable, and the overall market size is very limited.

This perspective actually highlights some of the pain points in certain industries, but it is important to recognize thatThe Development of China's Health Insurance Industry Is Closely Linked to the Direction of Healthcare Reform—Since the initiation of drug R&D reforms in 2014, the comprehensive elimination of drug markups in public hospitals in 2017, and the establishment of the National Healthcare Security Administration in 2018 to consolidate multi-party medical security responsibilities, the new healthcare reform centered on the “tri-medical linkage” (coordinated reform of medical care, health insurance, and pharmaceuticals) has been progressively advanced over the past decade, entering a phase of deep-water challenges. In February 2020, the State Council issued the Opinions on Deepening the Reform of the Medical Security System, further clarifying the need to accelerate the development of a multi-tiered medical security system and promote reforms in payment methods as well as supply-side reforms in pharmaceutical and medical services.

Since the beginning of this year, policy support has remained robust. In June, the National Financial Regulatory Administration issued the “Guiding Opinions on Promoting the High-Quality Development of Inclusive Insurance,” calling for the advancement of high-quality development in inclusive insurance. In September, the State Council released the “Several Opinions on Strengthening Supervision, Preventing Risks, and Promoting the High-Quality Development of the Insurance Industry,” reiterating the need to enhance the insurance industry’s capacity to serve public welfare and social security. This initiative primarily encompasses four key areas: diversifying forms of catastrophe insurance coverage, actively developing the third pillar of pension insurance, improving the service and protection levels of health insurance, and strengthening the inclusive insurance system.

More importantly, from the user’s perspective, health insurance can, to some extent, alleviate supply-side contradictions. The value of health insurance lies in its ability to manage uncertain future medical expenses through affordable, upfront payments. After all, although most diseases are currently covered by national basic medical insurance and drug prices have shown a significant downward trend under the centralized procurement policy, individuals’ out-of-pocket medical burdens remain substantial.

Therefore, from both the policy and consumer perspectives, demand for health insurance is genuine and robust, serving as a key pillar supporting its emergence as a trillion-yuan blue-ocean market.Given the enormous scale of this market, it can accommodate not only listed companies such as Huize Insurance and Shuidi, as well as several firms like Yuanbao that are racing toward an initial public offering (IPO), but also give rise to many more enterprises with valuations reaching tens of billions, or even hundreds of billions.

Certainly. In this process, industry participants should actively promote the continuous transition of healthcare services toward value-based care. Guided by the principles of value-based care, they should deeply engage in the “tri-medical linkage” (coordinated reform of medical services, health insurance, and pharmaceuticals) by expanding funding sources, providing insurance coverage, integrating service delivery, and strengthening industrial consolidation. In doing so, they will serve as a catalyst for deepening healthcare reform and, while mitigating risks associated with medical costs, help drive the transformation of the healthcare model from a disease-centered approach to a health-centered one.

Only after gaining a profound understanding of this point can innovative healthcare payment models truly hold practical value and significance.