2024 Clinical Mass Spectrometry Industry Report: Surge in Automation Products and Accelerated Adoption of Fully Integrated Automated Systems

Clinical mass spectrometry has always been a crucial component of precision diagnostic technologies, holding a significant position. According to the newly released 17th edition of the Global IVD Industry Report by the United States, the global market size for clinical mass spectrometry was $930 million in 2024 and is projected to reach $1.435 billion by 2029. From 2024 to 2029, the clinical mass spectrometry market is expected to grow at an annual rate of 9%, making it the fastest-growing segment in the IVD field, second only to nucleic acid testing.

In recent years, nearly RMB 10 billion has been invested in the clinical mass spectrometry sector, driving unprecedented growth in niche areas such as LC-MS, nucleic acid mass spectrometry, mass spectrometry automation, and proteomics. In 2023, Roche announced its entry into the clinical mass spectrometry market, identifying it as a potential market worth CHF 2.9 billion. This move has attracted significant attention from investors and companies, injecting strong momentum into the industry.

Although there has been long-standing anticipation for mass spectrometry to make significant inroads in clinical laboratory testing, the current development of clinical mass spectrometry has not yet met expectations. Its clinical application remains constrained by numerous factors, including standards and regulations, sample pretreatment, full automation, cost, throughput, and reimbursement policies.

Based on this, VCBeat conducted a comprehensive survey of the current development of clinical mass spectrometry and authored the "2024 Clinical Mass Spectrometry Industry Research Report," aiming to present the most authentic progress in the field.

Key Insights:

China’s clinical mass spectrometry industry has entered a fast lane of development, with significant progress made in mass spectrometry-based multi-omics, domestically produced mass spectrometers, and automated mass spectrometry technologies.In 2023, new products such as ceramide mass spectrometry assays and nucleic acid mass spectrometry tests were successively approved, paving the way for clearer clinical applications of mass spectrometry-based multi-omics. Meanwhile, several domestically produced LC-MS instruments received approval from the National Medical Products Administration (NMPA), leading to a steady increase in the market share of Chinese-made mass spectrometers. Furthermore, significant breakthroughs were achieved in mass spectrometry automation: the first Class II medical device certificate for an automated sample pretreatment system was granted in China, and domestic manufacturers have officially launched fully integrated, automated mass spectrometry systems.

Vitamin testing is one of the most mature clinical mass spectrometry applications, while hormone assays are the most anticipated by clinicians.VCBeat Research Institute conducted a survey on the implementation of mass spectrometry (MS) projects in hospital clinical laboratories. The survey results indicate that MS technology has gained widespread recognition, and hospitals across various regions are actively establishing MS laboratories driven by policy incentives. Currently, vitamin testing is the most widely adopted clinical MS application in hospitals, while hormone assays are the most anticipated new projects. The two key factors for the clinical adoption of MS technology are profitability and regulatory compliance. In the short term, clinical laboratories prioritize cost reduction, improved reimbursement structures, and accelerated compliance for MS technologies, while simultaneously exploring more high-value-added applications.

Addressing the pain points of automation, domestication, and point-of-care testing within hospitals, while expanding the business footprint outside hospitals to meet the demands of new drug development and scientific research services, represents the “next chapter” for clinical mass spectrometry in China.To address the pain points of mass spectrometry applications within hospitals, companies should currently focus on domesticating instruments, automating the entire testing process, developing innovative multi-omics projects, and advancing point-of-care testing (POCT) solutions. Meanwhile, demand for mass spectrometry testing services in the out-of-hospital market is surging, allowing clinical mass spectrometry enterprises to extend their reach from in-hospital to out-of-hospital settings, thereby expanding the boundaries of mass spectrometry applications.

The following is an excerpt from the report:

Amid uncertainties such as shifts in the international environment, industries across the board are undergoing systemic transformation. In 2023, clinical mass spectrometry also experienced a series of changes. The capital market cooled down from its previous fervor, and the industry as a whole became more calm, rational, and mature. Companies have increasingly focused on strengthening their core technologies and emphasizing practical commercialization, achieving notable progress in regulatory registration, product development, and business innovation. Meanwhile, leading enterprises have further accelerated their growth.

Surge in Registration Certificates: Ceramide Testing, Nucleic Acid Mass Spectrometry, and Other New Products Approved for the First Time

As of July 31, 2024, a total of 228 domestically produced clinical mass spectrometry products, excluding quality control materials and calibrators, have received approval from the National Medical Products Administration (NMPA).

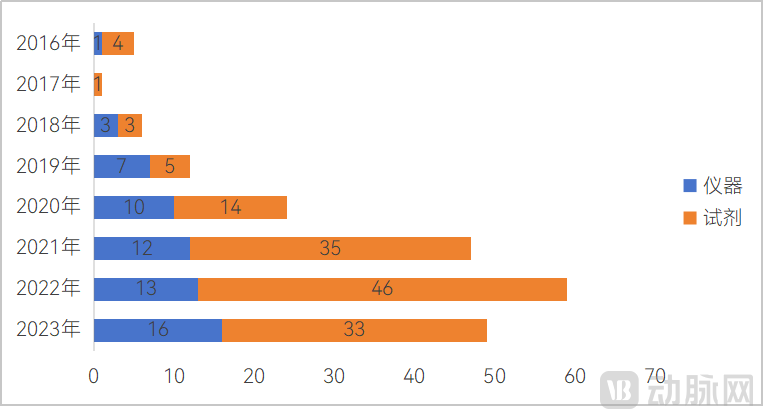

We are currently in a period of explosive growth in clinical mass spectrometry registration certificates, with the relevant review and approval systems becoming increasingly mature.From 2021 to 2023, the number of clinical mass spectrometry products receiving regulatory approval saw a significant increase compared with previous years. In 2021, a total of 47 domestically produced clinical mass spectrometry products were approved; this figure rose to 59 in 2022 and stood at 49 in 2023. From January to July 31, 2024, 25 such products received approval.

Approval Status of Domestically Produced Clinical Mass Spectrometry Products Over the Years

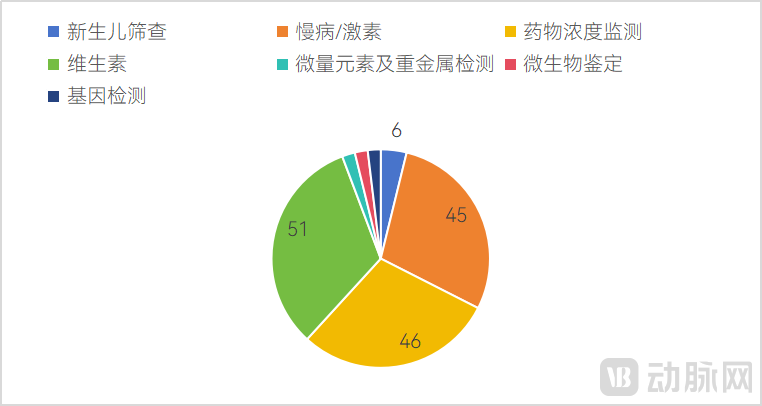

In terms of approved reagent types, as of July 31, 2024, there were 51 approved reagents for vitamin testing, 46 for therapeutic drug monitoring, and 45 for chronic diseases and hormones.

Types of Domestically Produced Clinical Mass Spectrometry Reagents Approved by the NMPA

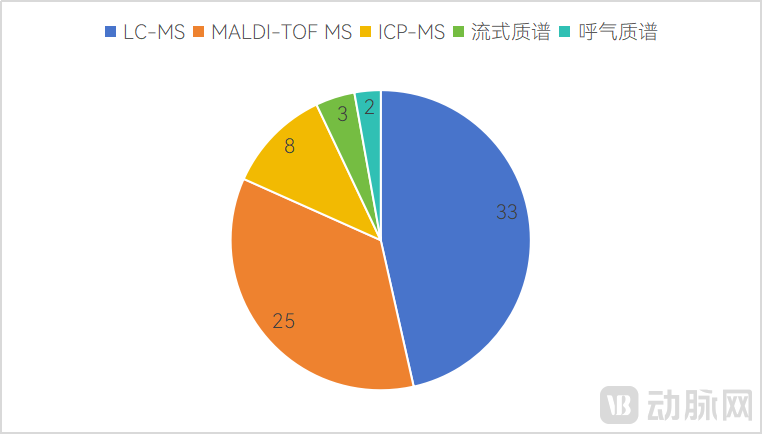

Domestic clinical mass spectrometry instruments approved in the past five years have maintained steady growth, with no signs of slowing down. The number of approvals from 2020 to 2023 was 10, 12, 13, and 16, respectively. Among the approved instruments, LC-MS systems predominated, with 33 domestically produced LC-MS devices receiving approval. This was followed by domestically produced MALDI-TOF MS systems, with 25 approvals; these are indicated for microbial detection, nucleic acid testing, and peptide analysis.

Types of Clinical Mass Spectrometry Instruments Approved by the NMPA

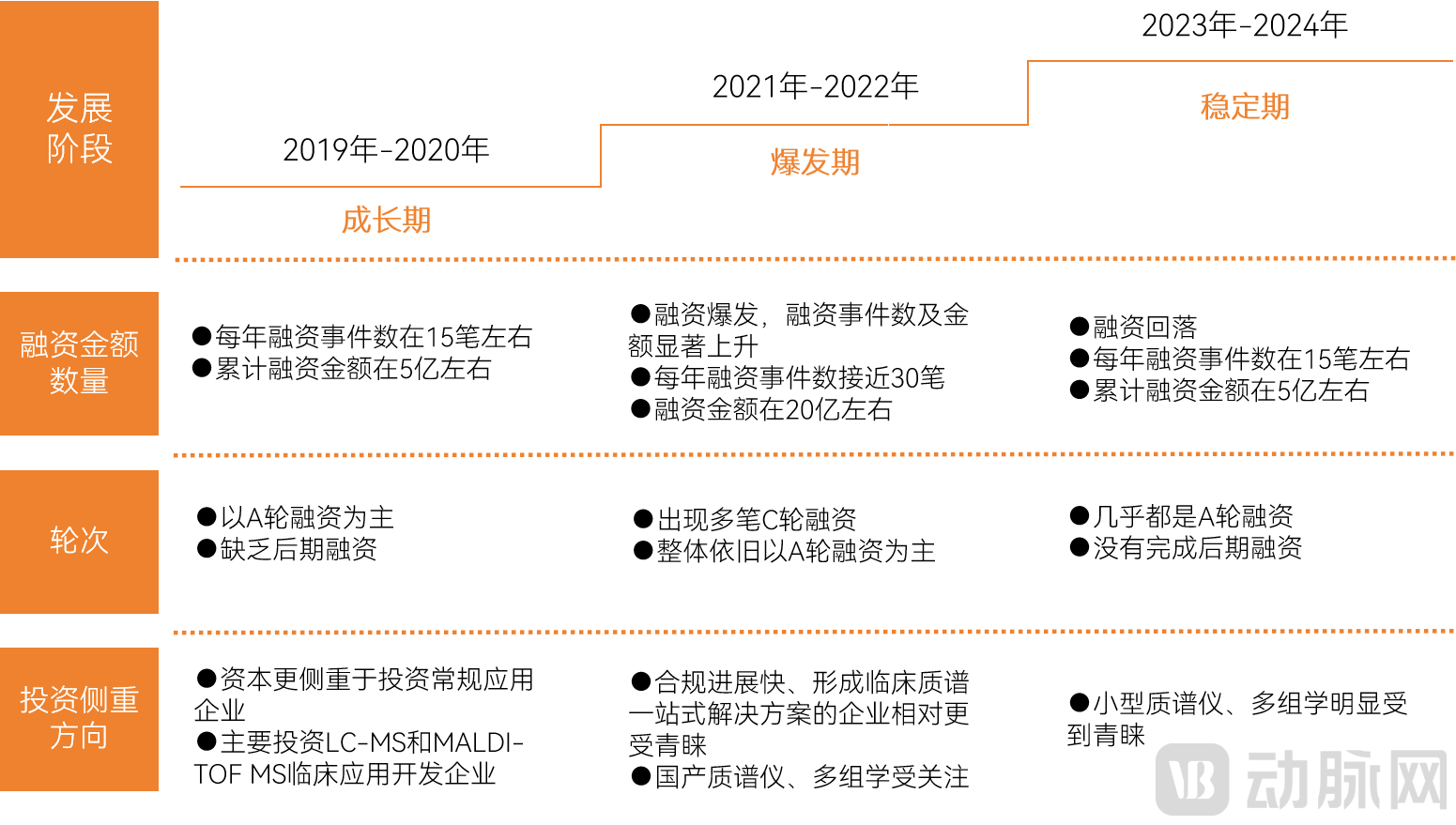

Primary Market Cools Amid Macroeconomic Headwinds; Omics and Domestically Produced Compact Mass Spectrometers Draw Attention

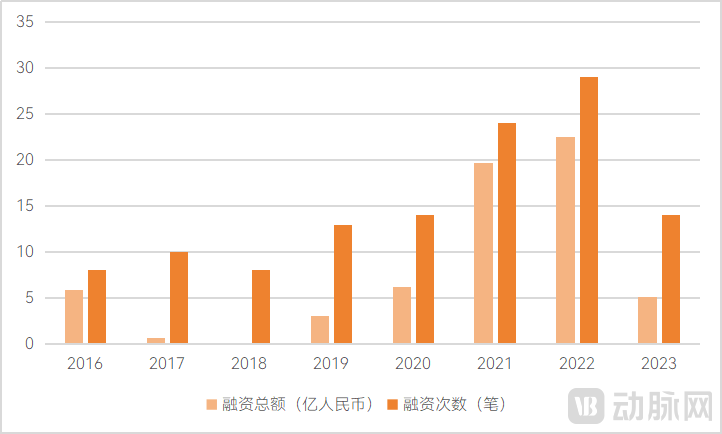

Throughout 2023, a total of 14 financing rounds were completed in China’s clinical mass spectrometry sector, with the total amount raised reaching RMB 510 million. Both the number of financing events and the total capital raised declined compared to 2022 and 2021, reflecting a contraction in large-scale financing deals, which aligns with global trends in healthcare investment and financing.

Trends in the Number and Amount of Financing Events in Clinical Mass Spectrometry Over the Years

In 2024, nine financing rounds were completed, primarily involving companies specializing in compact mass spectrometers and omics.From January to July 31, 2024, a total of nine financing rounds were completed in the clinical mass spectrometry sector, including three small-scale mass spectrometer companies—Qingpu Technology, Zhiqin Instruments, and Huayi Ningchuang—and three multi-omics companies.

In recent years, investors’ focus in the clinical mass spectrometry sector has shifted noticeably.In the early stages, capital investment primarily focused on small-molecule detection applications and microbial mass spectrometry. From 2021 to 2022, there was a surge in financing and investment in clinical mass spectrometry. Companies with rapid regulatory compliance progress attracted significant investor attention, while investment portfolios became more diversified, encompassing routine applications, innovative omics applications, domestically produced mass spectrometers, compact mass spectrometers, automated mass spectrometry systems, breath analysis mass spectrometry, and flow cytometry mass spectrometry. Since 2023, capital investment has become more prudent, with relatively greater focus on emerging technological areas such as multi-omics and compact mass spectrometers.

Shifts in Investment Hotspots for Clinical Mass Spectrometry

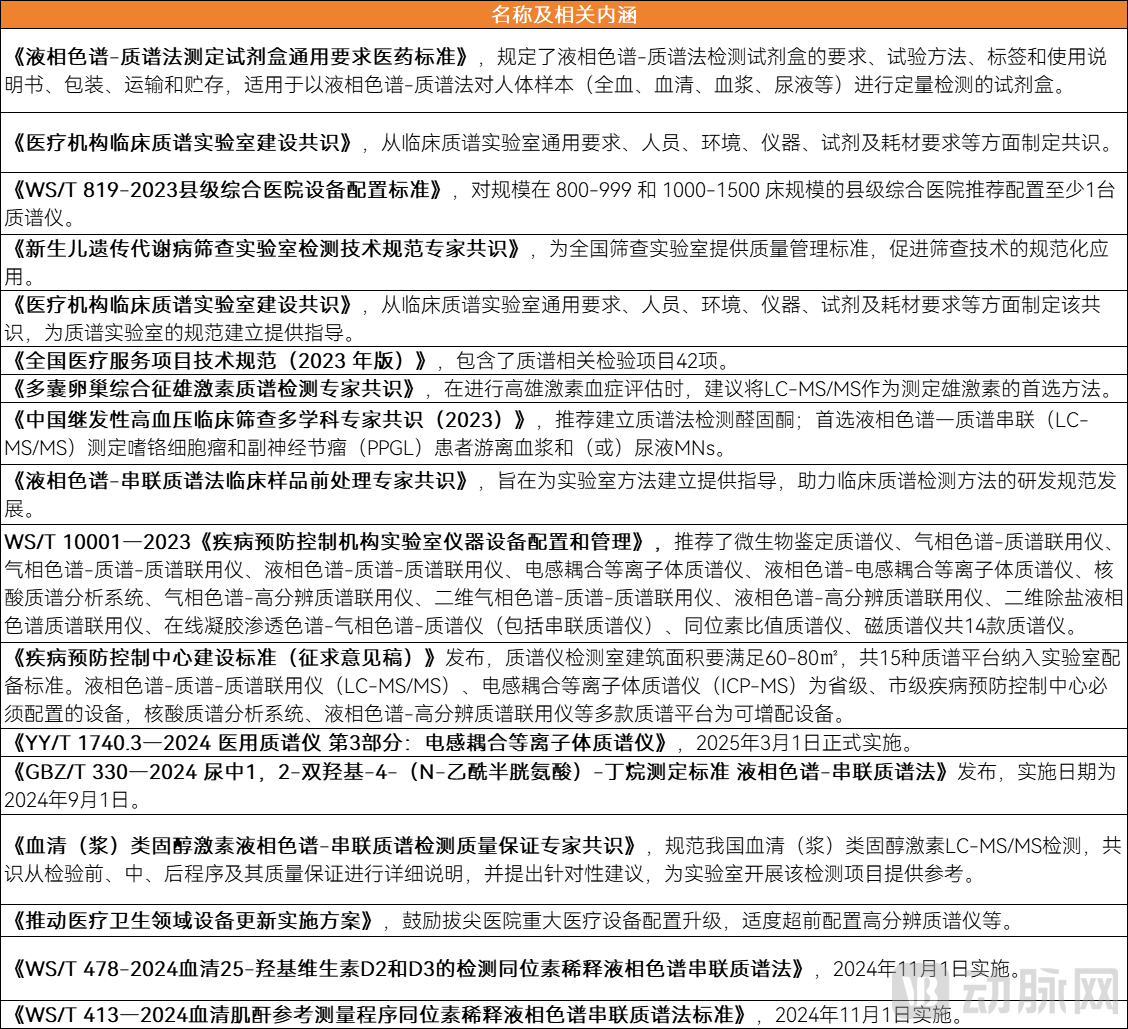

The clinical application of mass spectrometry technology is becoming increasingly in-depth. In 2023, the "Equipment Configuration Standards for County-Level General Hospitals" was released, recommending that the clinical laboratories of county-level general hospitals with 800–999 beds and 1,000–1,500 beds be equipped with one mass spectrometer. This has sparked a surge in the construction of mass spectrometry laboratories across China, with hospitals nationwide actively establishing such facilities.

Multiple Policies, Consensuses, and Standards Drive Hospitals to Accelerate the Construction of Mass Spectrometry Laboratories

What is the current status of mass spectrometry technology in clinical applications? What factors influence its clinical implementation? Amidst the surge in mass spectrometry laboratory construction, VCBeat Research Institute surveyed 37 tertiary hospitals.(Due to the limited number of surveys and coverage areas, the sample analysis results may deviate from the actual conditions of some hospitals.)

Surveys indicate that hospitals universally prioritize mass spectrometry as the preferred direction for technological upgrades in their clinical laboratories. However, current hospital mass spectrometry laboratories are typically small in scale, staffed by personnel lacking specialized expertise in mass spectrometry, and characterized by prolonged turnaround times.

Overview of Mass Spectrometry Laboratories in Participating Hospitals

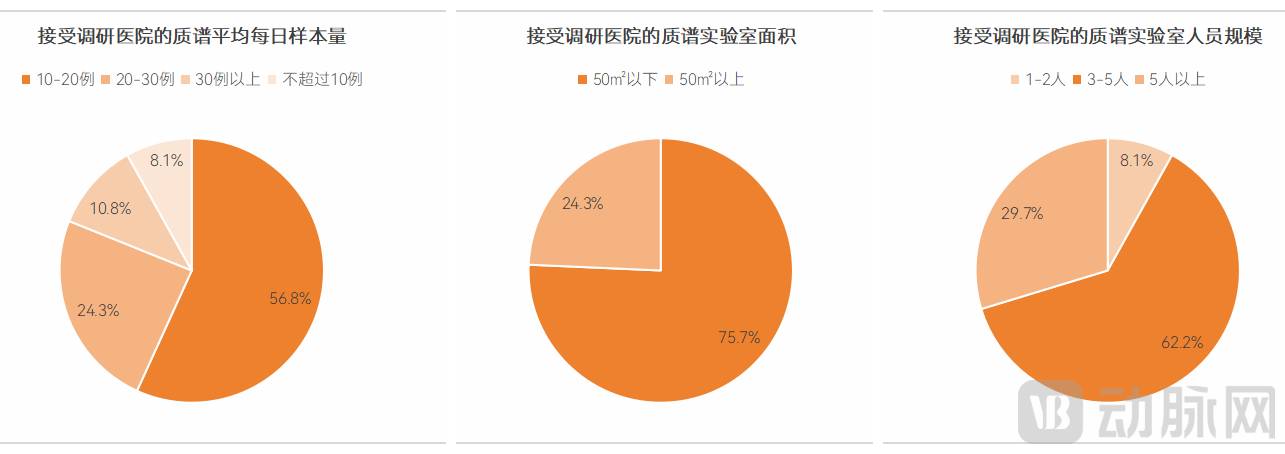

The “Consensus on the Construction of Clinical Mass Spectrometry Laboratories in Medical Institutions” states that the total area of a mass spectrometry laboratory is recommended to be no less than 50 m². Among the hospital mass spectrometry laboratories surveyed, 97.2% were retrofitted spaces; 75.7% had a floor area of less than 50 m², while 24.3% exceeded 50 m². These laboratories are generally divided into three zones: specimen preparation, instrument, and result analysis areas.

In terms of staffing, 62.2% of mass spectrometry laboratory teams consist of 3–5 members, 8.1% have two or fewer members, and 29.7% comprise more than five members. This indicates that hospital-based mass spectrometry laboratory teams are currently small in scale, with most personnel also required to perform other laboratory testing duties on a part-time basis.

Laboratory personnel generally lack specialized knowledge and practical experience in the field of mass spectrometry.According to the "Consensus on the Construction of Clinical Mass Spectrometry Laboratories in Medical Institutions," laboratory directors are required to have at least two years of experience working in a mass spectrometry laboratory. However, among the hospitals surveyed, 94.6% of mass spectrometry laboratory personnel lacked educational backgrounds and practical experience related to mass spectrometry. Instead, they primarily acquired their knowledge through three channels: training provided by manufacturers, participation in academic conferences, and organized visits to other hospitals for learning purposes.

Currently, the turnaround time for clinical mass spectrometry samples in hospitals is significantly longer than that for routine tests such as biochemistry and immunoassays.86.5% of hospitals stated that if samples could be loaded onto the mass spectrometer on the same day they were received, reports could be issued the following day. However, many laboratory personnel are responsible not only for mass spectrometry testing but also for other tasks, which often prevents timely analysis of mass spectrometry samples upon receipt; in such cases, it takes 3–5 days to issue reports. Furthermore, some hospitals currently have a low volume of mass spectrometry samples and need to batch them, conducting mass spectrometry tests 2–4 times per week in centralized runs.

Thus, the prolonged turnaround time for mass spectrometry samples is not only attributable to the cumbersome pre-treatment and analytical procedures inherent to mass spectrometry, but also significantly influenced by factors such as insufficient staffing and the need to batch samples due to low sample volume.

Currently, the volume of mass spectrometry samples in hospitals is relatively small.According to the survey, 56.8% of hospital mass spectrometry laboratories process an average of 10–20 samples per day, 24.3% process 20–30 samples per day, 8.1% process no more than 10 samples per day, and 10.8% process more than 30 samples per day.

The Complexity of LC-MS Poses Challenges for Large-Scale Clinical Application

In the past three years, the clinical adoption of LC-MS has accelerated significantly. Among the hospitals surveyed, 58.1% introduced LC-MS technology after 2022, 29.0% adopted it between 2019 and 2022, and only 12.9% had implemented LC-MS prior to 2019.

Regarding mass spectrometry instrument configuration, 30 hospitals have deployed only one LC-MS unit each. Currently, the LC-MS instruments installed in hospitals are predominantly imported brands, such as Waters and SCIEX. In contrast, testing reagents and quality control materials are mainly domestically produced, with a high level of acceptance for Chinese brands. Domestic reagents are used for vitamin testing, hormone testing, and therapeutic drug monitoring, sourced from manufacturers such as Yingsheng Biotechnology and Kaluipu. Reagents for newborn screening are supplied by Revvity, Fenghua Biotechnology, and Yingsheng Biotechnology, among others.

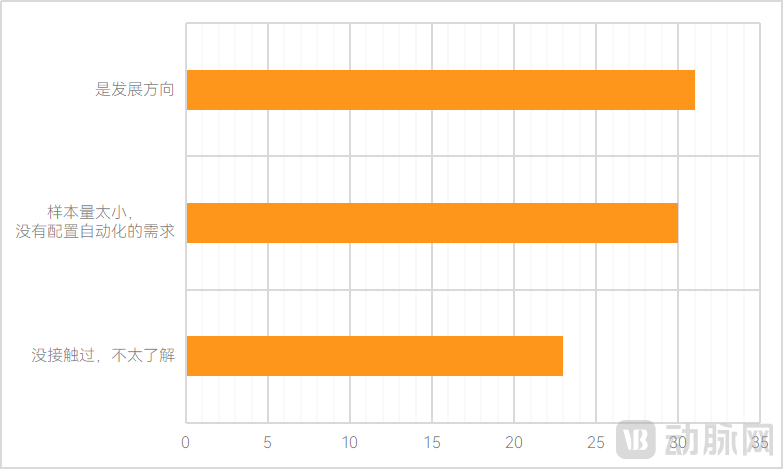

Due to limited sample sizes, the configuration rate of automated mass spectrometry pre-treatment systems is extremely low.High automation and assembly-line processing represent the prevailing trend in clinical laboratory testing. Although several manufacturers have already launched automated mass spectrometry products, their adoption rate in clinical laboratories remains extremely low. According to surveys, 96.8% of hospitals have not implemented automated systems. The primary reason is that the clinical application of mass spectrometry is still in its early stages; hospitals offer only a limited number of mass spectrometry-based tests, with daily sample volumes amounting to merely dozens. Manual operations are currently sufficient, rendering the deployment of automated systems unnecessary at this time.

However, the hospital has also clearly stated that reducing sample turnaround time and improving accuracy through mass spectrometry automation are confirmed requirements. When the daily sample volume reaches 100 to 200 cases, the hospital will consider configuring an automated pre-analytical system for mass spectrometry.

Attitudes of Surveyed Hospitals Toward Automated Mass Spectrometry Products

Vitamin Testing Is the Hottest Trend, While Hormone Panels Are Gaining Favor

A survey shows that the mass spectrometry projects currently conducted by hospitals based on the LC-MS technology platform include vitamin testing, therapeutic drug monitoring, newborn screening, and hormone testing.

Vitamin testing is currently the most popular LC-MS assay in clinical practice.Among the hospitals surveyed, 100% offered vitamin testing services. Fat-soluble vitamin tests were more widely available, with 100% of hospitals offering tests for vitamins D2 and D3, and some also providing tests for vitamins A, E, and K. In contrast, fewer hospitals offered tests for water-soluble vitamins (B-complex vitamins and vitamin C). This indicates that vitamin testing services in hospitals are quite comprehensive, with a wide variety of vitamins available for detection.

Vitamin testing is widely utilized across various clinical departments. Currently, the clinical departments with the highest demand for vitamin testing are primarily pediatrics, nutrition, and endocrinology.

In terms of pricing, tests for vitamins D2 and D3 generally cost around RMB 150, not exceeding RMB 200. Vitamin panels covering three biomarkers are priced between RMB 250 and RMB 300, while those including 5–7 biomarkers range from RMB 400 to RMB 550.

Regarding hormone testing, many hospitals have already implemented steroid hormone assays, with current demand concentrated in gynecology and endocrinology. Furthermore, when discussing the introduction of new LC-MS applications, 67.7% of hospitals expressed optimism about hormone-related tests, particularly for steroid hormones.

Currently, mass spectrometry vendors can detect more than 30 types of hormones. As the pricing structures for mass spectrometry-based hormone testing become increasingly standardized, this technology is poised to demonstrate significant application advantages in hormone analysis in the future. However, hospitals have noted that the low endogenous levels of hormones necessitate high assay sensitivity. Consequently, the operational complexity and personnel requirements for these tests far exceed those for vitamin testing and therapeutic drug monitoring, posing considerable challenges for healthcare institutions.

Analysis of the Drivers and Barriers Influencing the Release of Clinical Demand for LC-MS

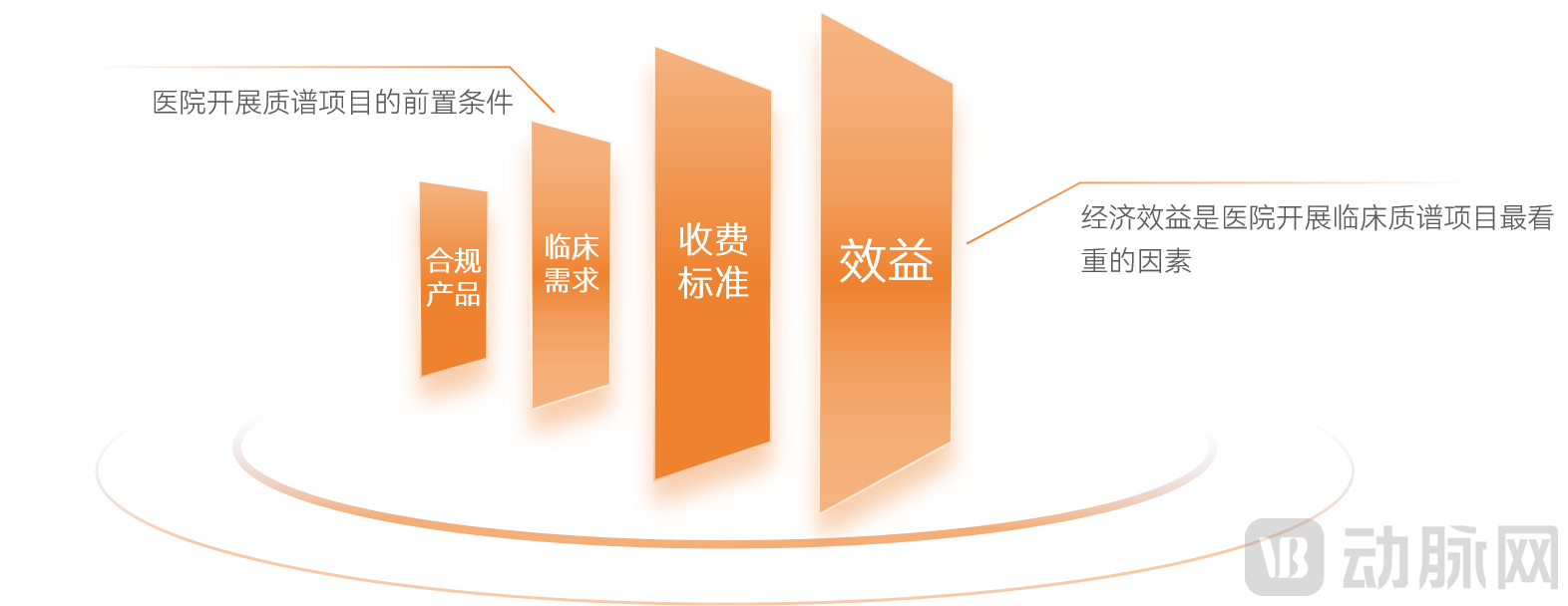

According to the survey findings, the driving factors for hospitals to adopt mass spectrometry testing are highly consistent. Economic benefit is the most valued factor for hospitals in launching clinical mass spectrometry projects, followed by pricing standards, clinical demand, and compliant products.

The Drivers Behind Hospitals’ Adoption of Mass Spectrometry Projects

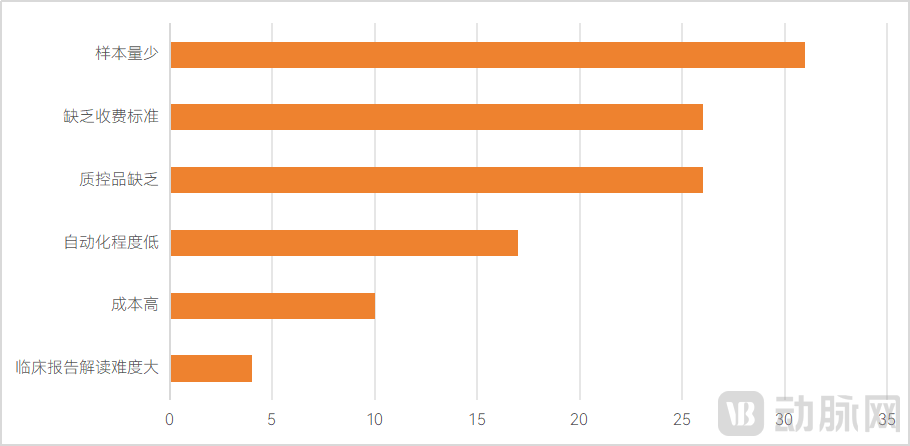

Hospitals face numerous obstacles in implementing LC-MS projects, with economic viability being the decisive factor. Profitability is primarily determined by sample volume. Hospitals have candidly acknowledged, “While mass spectrometry technology has broad applications and many departments have expressed demand, the potential sample volumes for many assays are insufficient.”

Barriers to the Implementation of Mass Spectrometry Projects in Hospitals

Overall,LC-MS technology offers unique advantages in clinical settings due to its precision and multi-analyte detection capabilities. There is a tangible clinical demand for mass spectrometry-based testing, indicating promising prospects.Currently, the clinical application of LC-MS is still in its very early stages. The tests offered are primarily concentrated on vitamin analysis, therapeutic drug monitoring of psychotropic medications, steroid hormone profiling, and newborn screening, indicating significant limitations in the scope of available test menus. Economic viability remains the core determinant for the implementation of clinical mass spectrometry projects. Moving forward, the large-scale adoption of mass spectrometry in clinical settings must address bottlenecks such as high costs, standardization, automation, and reimbursement pricing. These are critical issues that enterprises and regulatory bodies will need to prioritize in the future. Hospitals exhibit strong enthusiasm for implementing mass spectrometry testing; all surveyed hospitals have expressed their expectation to procure more mass spectrometers and expand the variety of mass spectrometry-based tests once issues related to reimbursement, regulatory compliance, and the availability of domestically produced instruments are resolved.

Shifting our focus from the clinical setting to the industry sector, we observe that domestic clinical mass spectrometry companies have already made strategic arrangements to address clinical challenges such as automation, localization, and standardization, achieving breakthroughs in automation, domestic production, platform development, and specialized testing items.

The Rise of Automated Pre-analytical Systems: Fully Integrated All-in-One Instruments as the Ultimate Solution

The 2023 “Expert Consensus on Clinical Sample Pretreatment by Liquid Chromatography–Tandem Mass Spectrometry” states that integrating assay panels with fully automated sample pretreatment systems will significantly enhance the level of automation in sample pretreatment. The use of automated sample pretreatment equipment can substantially reduce errors associated with manual operations, improve analytical precision, decrease the workload of technical staff, and increase overall testing efficiency. Clinical laboratories may select appropriate pretreatment equipment based on factors such as pretreatment requirements for specific assays, sample volume, and economic costs, thereby facilitating sample pretreatment through the adoption of automated pretreatment systems.

There are many sample preparation methods for mass spectrometry, and the magnetic bead-based method is the most amenable to full automation.A major advantage of magnetic bead-based methods is their operational simplicity, eliminating the need for complex procedures such as nitrogen blow-down concentration. Mass spectrometry automation instruments developed based on magnetic bead technology are more compact and have a simpler structure, enabling full automation. Therefore, the emergence of magnetic bead-based methods has significantly advanced the automation of pre-analytical processing in clinical mass spectrometry. Furthermore, magnetic bead-based methods demonstrate excellent performance in terms of reproducibility, recovery rate, and efficiency. However, as a recently developed mass spectrometry automation technology, magnetic bead-based methods still have areas requiring improvement. For instance, no related reagents have yet obtained Class II medical device certification, the stability of raw material manufacturing processes needs enhancement, and there is a lack of proven successful experience overseas. Consequently, extensive validation and optimization efforts are required for magnetic bead-based methods in the future.

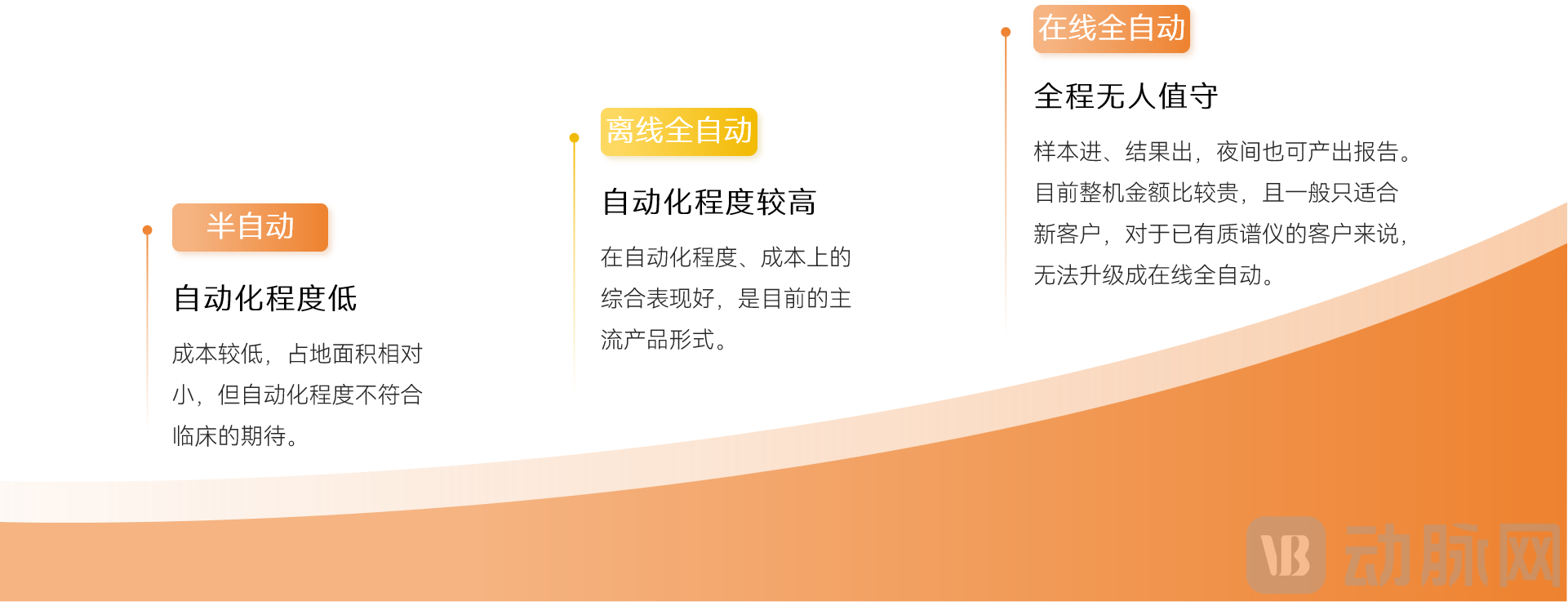

Based on the level of automation, mass spectrometry automation products can be classified into semi-automated, offline fully automated, and online fully automated systems.

Classification of Automated Mass Spectrometry Products

Semi-automationThe product, represented by liquid handling workstations, automates certain steps in the pre-processing workflow, such as pipetting, aliquoting, and reagent addition. However, some modules that are difficult to integrate still require manual operation, and the range of compatible methodologies is generally limited.Offline Automation, i.e., the automated sample pre-processing system, which achieves full automation from "sample tube input" to the stage prior to loading onto the mass spectrometer; operators only need to transfer the samples to the mass spectrometer after processing is complete;Online Fully Automated, namely the fully automated integrated mass spectrometry system, which achieves a "sample-in, result-out" workflow with unattended operation throughout. While online full automation represents the ultimate solution for mass spectrometry automation, its high cost and requirement for substantial sample volume hinder widespread adoption in the short term, making it suitable primarily for large Grade 3A hospitals.

Online, fully automated systems are widely recognized as the developmental trend in clinical mass spectrometry. However, previously available fully automated integrated mass spectrometry instruments in the industry either offered a limited menu of testable analytes or had constrained levels of automation, leaving the sector with the entrenched perception that the number of assays and the degree of automation could not be simultaneously optimized.

As Roche and BGI each disclosed the latest updates on their fully automated integrated mass spectrometry systems, this stereotype has been overturned. Based on the information currently released by both companies, VCBeat believes that their integrated systems can perform a wide range of tests and have both adopted magnetic bead-based methods with higher levels of automation, demonstrating strong technical feasibility and holding promise for accelerating the clinical adoption of integrated mass spectrometry systems.

One of the primary reasons for the limited number of participants in the fully automated mass spectrometry integrated system market is the exceptionally high technical barriers. These barriers manifest across multiple dimensions, including the interface between sample pre-treatment and the mass spectrometer, volume control, and the implementation of walk-in testing capabilities.First, the integration of the sample pretreatment module with the liquid chromatography (LC) module requires companies to have an in-depth understanding of LC-MS instruments and injection interfaces for instrument redevelopment. However, many clinical mass spectrometry companies rely on OEM-based LC-MS instruments and lack the necessary technical reserves. Second, size is a critical constraint; the pretreatment module must be compact, as excessive bulk would result in an overly large footprint when connected to the LC-MS system. Third, fully automated integrated mass spectrometry systems must enable real-time, random-access testing. If batch-processing pretreatment systems are used, there will inevitably be a mismatch between pretreatment throughput and detection speed.

Currently, there is a wide array of domestic mass spectrometry automation products, with offline automation being the predominant form. Most systems employ traditional sample preparation methods such as extraction and precipitation. The related technologies and supply chains are well-established, with fully developed modules for oscillation, incubation, pipetting, centrifugation, nitrogen evaporation, positive/negative pressure control, and magnetic separation. However, clinical feedback indicates that despite the abundance of automated solutions, it remains challenging to accurately assess whether these products truly make mass spectrometry technology more convenient, efficient, and accessible.

VCBeat Research Institute believes that assessments can be made across five dimensions: level of automation, speed, number of procedures performed, failure rate, and comprehensive cost.

Level of Automation: Biochemical and immunological testing has achieved a high degree of automation, enabling fully unattended operation; consequently, the clinical laboratory naturally imposes high requirements on the automation level of clinical mass spectrometry.

Speed: The clinical pursuit of high timeliness is endless, and mass spectrometry automation products need to increase processing speed as much as possible. It should be noted that improving efficiency relies not solely on automated pre-treatment; no matter how fast the pre-treatment is, if the throughput and speed of the mass spectrometer are insufficient, the overall detection efficiency cannot be improved. Therefore, enhancing the level of mass spectrometry automation requires the integration of capabilities across multiple areas, including automated pre-treatment, mass spectrometers, reagents, and software.

Number of Projects Available: The more compatible sample preparation methods a mass spectrometry automation product supports, the broader the range of assays it can perform.

Failure Rate: The failure rate significantly impacts the clinical user experience, and must be given high priority.

Comprehensive Cost: Comprehensive costs are influenced by factors such as cost, the number of feasible assays, speed, and failure rate. Furthermore, compared with methodologies like solid-phase extraction and liquid-liquid extraction, automated instruments based on magnetic bead technology offer greater simplicity and larger potential for cost reduction.

It is evident that the domestic market for automated sample preparation products for mass spectrometry has become highly diversified, and fully integrated automated mass spectrometry systems are rapidly evolving. However, as current sample volumes in hospitals remain limited, there has been no surge in demand for automation solutions. Automation is not the sole prerequisite for large-scale clinical adoption of mass spectrometry. While deploying automated products, companies must also establish a comprehensive product portfolio, diversify their offerings, enhance testing stability, and strengthen market education. Only as the clinical value of mass spectrometry becomes increasingly apparent and sample volumes continue to rise will significant demand for clinical mass spectrometry automation emerge.

Innovative Application Layout: Accelerating the Commercialization of Early Screening and Diagnosis for Major Diseases

A major advantage of mass spectrometry is its ability to detect a wide range of analytes, covering multiple application scenarios. Beyond routine applications such as vitamin testing, newborn screening, and hormone assays, some clinical mass spectrometry companies are driving the commercialization of innovative applications, including ceramide profiling and early diagnosis of Alzheimer’s disease (AD).

Routine applications are tested by cost and economies of scale, while innovative applications currently rely primarily on technological advantages and in-depth collaborations with leading large-scale hospitals. At present, there are few players deploying innovative mass spectrometry applications, resulting in limited competition and relatively high gross margins. This landscape effectively expands the development potential of clinical mass spectrometry, while companies also establish differentiated competitive advantages by providing differentiated products and services to clinical settings.

In recent years, multi-omics research encompassing proteomics, metabolomics, and lipidomics has significantly expanded the scope of mass spectrometry applications in clinical diagnostics. Internationally, Quest Diagnostics has launched multiple innovative applications based on LC-MS.

According to statistics from VCBeat, there are more innovative applications based on metabolomics in China, mainly focusing on cardiovascular disease risk prediction and cancer screening. In contrast, innovative applications based on proteomics include IGF-1 testing, indicating that the translation of emerging proteomic biomarkers into clinical diagnostic applications is very slow.

In terms of application development strategy, the prevailing approach among enterprises is as follows: First, gain a thorough understanding of the current gold standards and commonly used diagnostic techniques for disease diagnosis to identify the pain points and gaps in existing technologies. Second, assess the market size corresponding to the project. Third, pinpoint the unique application advantages of mass spectrometry technology, thereby facilitating faster commercialization of innovative applications.

Following the strategic framework of “identifying pain points, assessing market size, and leveraging the unique advantages of mass spectrometry,” notable innovative applications among domestic clinical mass spectrometry companies include ceramide CERT testing and early diagnostic prediction for acute-on-chronic liver failure (ACLF) in the field of metabolomics, as well as early detection of Alzheimer’s disease (AD) and insulin-like growth factor-1 (IGF-1) testing in the field of proteomics.

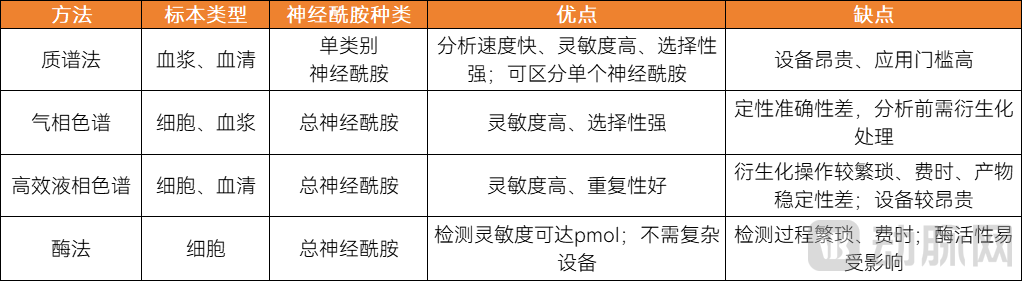

Among these, there are approximately 10 medical testing laboratories in China that offer ceramide CERT testing services based on mass spectrometry. The biomarkers detected are all ceramide (16:0), ceramide (18:0), ceramide (24:0), and ceramide (24:1). Currently, the main competitive factors among companies lie in patent layout and commercialization progress.

Ceramide Detection Methods and Their Advantages and Disadvantages

LC-MS technology has begun to be applied to the precise quantitative detection of IGF-1. Compared with immunoassays, LC-MS offers higher sensitivity, stronger specificity, better detection consistency, and the ability to detect IGF-1 sequence polymorphism information, thereby achieving precise quantitative detection of IGF-1.

Comparison of IGF-1 Detection Methods

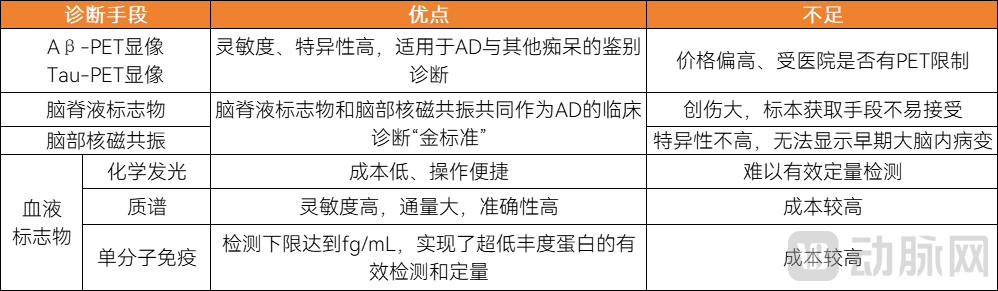

Furthermore, Alzheimer’s disease (AD) detection technologies primarily fall into three categories: chemiluminescence, mass spectrometry, and single-molecule immunoassay. Traditional chemiluminescence methods are limited by sensitivity, making effective quantitative detection challenging. In contrast, mass spectrometry and single-molecule immunoassays offer higher precision and sensitivity, generating significant expectations. Studies have also shown that mass spectrometry-based plasma assays outperform immunoassays in detecting cerebral amyloid-β (Aβ) pathology in AD patients.

Comparison of Various Diagnostic Methods for Alzheimer's Disease

Overall, the clinical mass spectrometry market has numerous innovative applications in development. For instance, metabolomics is expected to become widely adopted in tumor screening and early screening for cardiovascular diseases. Proteomics also presents significant opportunities for clinical translation, with many emerging biomarkers yet to be discovered. Currently, much of the development is based on re-engineering existing assays, such as those for IGF-1, thyroglobulin, and insulin. In the future, we can anticipate broader clinical application of novel proteomic biomarkers, positioning mass spectrometry for even more promising prospects in clinical practice.

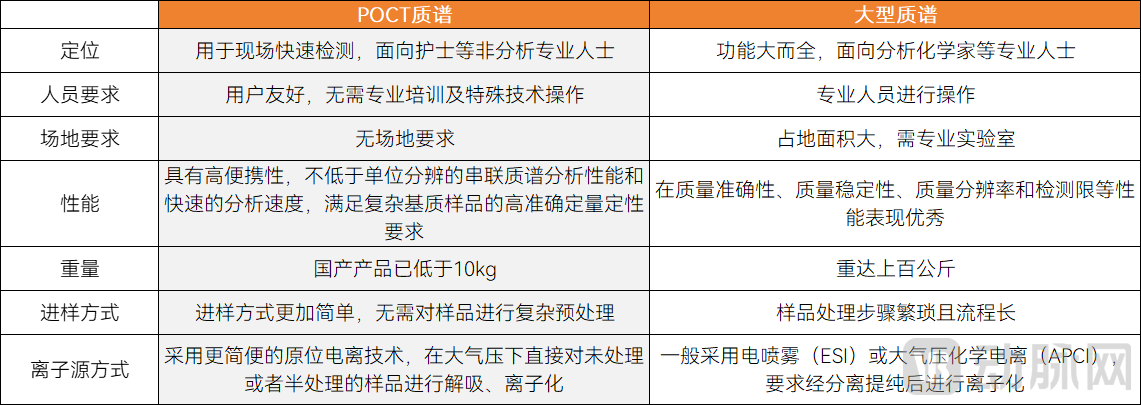

China-Made POCT Mass Spectrometry Advances Lead Globally, with Accelerating Clinical Adoption

According to clinical survey results, hospitals are acutely aware of the pain points associated with mass spectrometry technology, namely its high cost, cumbersome operation, and limited range of currently available tests. In addition to accelerating the automation and domestication of clinical mass spectrometry, VCBeat has observed that some companies are taking an alternative approach by focusing on point-of-care testing (POCT) mass spectrometers. Leveraging advantages such as compact portability, strong environmental adaptability, ease of operation, and intelligence, POCT mass spectrometers address challenges related to difficult deployment, complex professional operation and maintenance, and low levels of intelligence in traditional mass spectrometry. This facilitates the transition of specialized mass spectrometry technology from laboratory settings to rapid on-site testing scenarios.

Comparison of Differences Between POCT Mass Spectrometers and Large-Scale Mass Spectrometers

POCT mass spectrometry combines the high performance of mass spectrometry with the simplicity and rapid turnaround time of POCT products, enabling its widespread application in primary care settings.Compared with other POCT technologies, the advantages of MS-based POCT lie in not only retaining the inherent high sensitivity, high accuracy, and quantitative capabilities of mass spectrometry, but also making the entire instrument more portable and accessible. This enables rapid on-site detection and analysis of chemical substances, allows operation by non-specialists outside the laboratory, supports application in various POCT scenarios, replaces certain existing POCT tests with methodological limitations, and facilitates the development of more innovative assays.

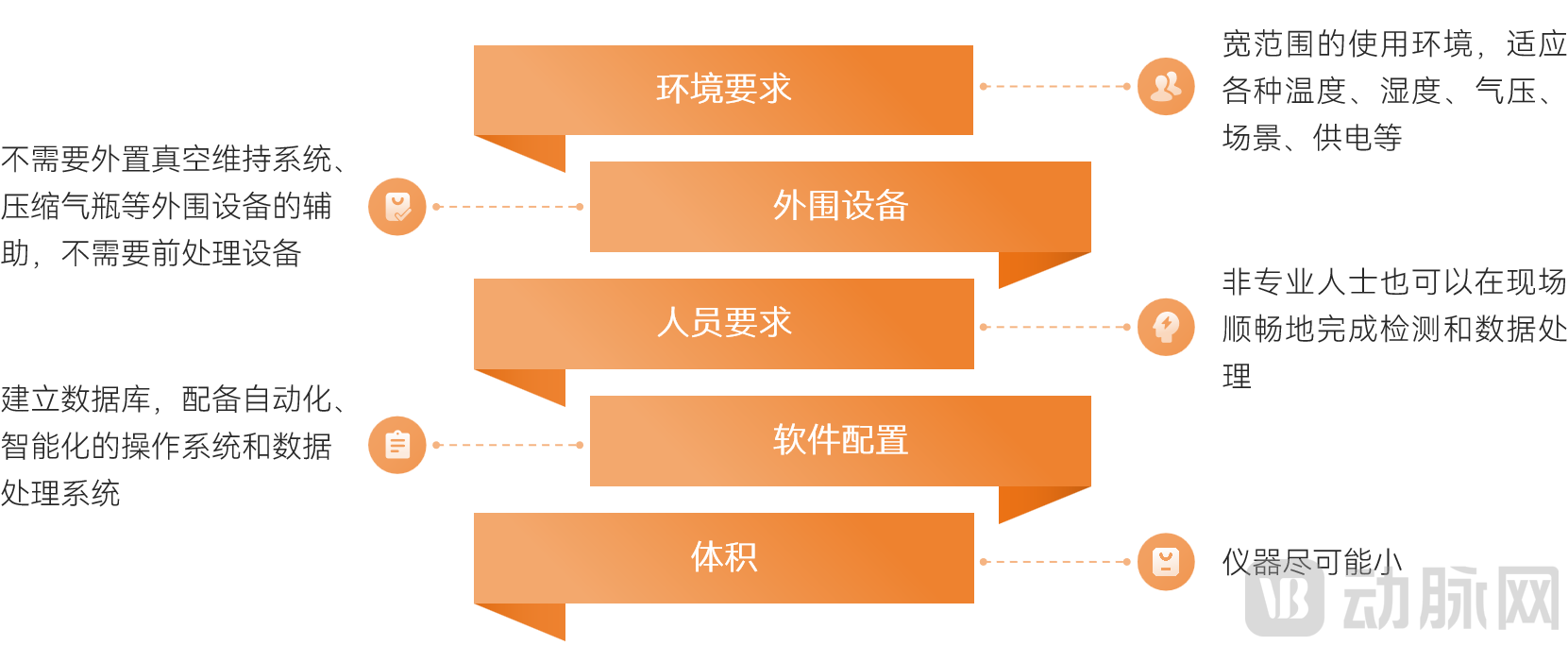

Point-of-care testing (POCT) is a key application area for compact mass spectrometers; however, not all compact mass spectrometers are suitable for POCT. Currently, several similar concepts coexist in the industry, leading to confusion between the distinct terms “compact mass spectrometry” and “POCT mass spectrometry.” Therefore, it is essential to establish an accurate definition of “POCT mass spectrometry.”

Can compact mass spectrometers, while delivering exceptionally high mass spectrometry performance, be utilized in point-of-care testing (POCT) settings? There are three primary criteria for assessment: First, POCT mass spectrometers must possess superiorEnvironmental Adaptability, adaptable to varying temperature, humidity, air pressure, scenarios, and power supply conditions, enabling use anytime and anywhere; secondlyNo Peripheral Device Assistance Required, traditional mass spectrometers require external vacuum maintenance systems, compressed gas cylinders, and other ancillary equipment. Additionally, a series of pre-processing instruments are needed for samples prior to analysis, which is time-consuming and labor-intensive, thereby significantly limiting the point-of-care testing (POCT) adaptation of mass spectrometry; furthermore,Low Requirements for Operators, non-professionals can also smoothly perform testing and data processing on-site, and instrument maintenance is very convenient.

Mass Spectrometers for POCT Testing Must Meet Multiple Stringent Requirements

Small mass spectrometers available on the market can be broadly categorized into three types: one type is compact in size but requires external gas chromatography or liquid chromatography systems, as well as gas generators and vacuum pumps; another type does not require external gas or liquid chromatography systems but still needs to be connected to gas generators and vacuum pumps; and the third type requires no peripheral equipment whatsoever, imposing virtually no requirements on the environment or operators—these instruments are known as POCT (Point-of-Care Testing) mass spectrometers. Currently,Although there are many small mass spectrometers in the industry, those capable of meeting POCT testing requirements remain scarce.

In simple terms, miniaturization is merely the first step for point-of-care testing (POCT) mass spectrometers. The key lies in enabling simple, direct, rapid, and precise analysis of complex samples, thereby achieving on-site rapid analytical capability. This primarily faces two major barriers: first, how to process complex samples quickly, conveniently, and efficiently, given that pre-treatment methods available in laboratories, such as chromatography and centrifugation, are not feasible in field settings; second, how to ensure sufficient performance during miniaturization, as the miniaturization process typically leads to a decline in analytical performance.Overall, “in situ ionization technology + DAPI + ion trap” represents an ideal technical pathway for achieving mass spectrometry-based POCT testing, effectively addressing these two core barriers.

Currently, China has developed a wide range of compact mass spectrometers for applications in environmental monitoring, public safety, aerospace, healthcare, and other fields. In the healthcare sector, most commercially available compact mass spectrometers are used for detecting volatile organic compounds (VOCs). Notable examples include Owlstone Medical, which secured $6.5 million in funding from the Bill & Melinda Gates Foundation in 2024, and NanoScent. By contrast, there are relatively few companies focused on the detection of non-volatile organic compounds.

ButIn medical settings, the demand for detecting non-volatile organic compounds far exceeds that for VOCs.From the perspective of medical applications, the use cases for volatile organic compound (VOC) detection are not as diverse as those for non-volatile organic compound detection. In the medical field, most test items—such as amino acids, organic acids, hormones, vitamins, drugs, and toxins—are non-volatile organic compounds.

There is also a significant gap in technical difficulty between VOC detection and non-volatile organic compound detection. Mass spectrometry-based VOC detection has a long history of development, with core technologies such as EI ion sources, analytical workflows, and databases already mature. In contrast, the detection of non-volatile compounds demands higher sensitivity from mass spectrometers, started later, suffers from incomplete databases, and thus involves substantially greater technical complexity.

Therefore, there has been limited progress in China regarding the detection of non-volatile organic compounds using point-of-care testing (POCT) mass spectrometers. According to statistics from VCBeat, Qingpu Technology has made relevant strategic deployments, focusing on market segments that leverage the timeliness advantages of POCT mass spectrometry, address strong clinical needs, and currently remain underserved, such as intraoperative and intensive care unit (ICU) therapeutic drug monitoring, as well as intraoperative tumor diagnosis.

From Self-Developed Instruments to a Complete Industrial Chain: Accelerating the Localization of LC-MS in China

Domestic mass spectrometers hold advantages in production costs, demand responsiveness, and customized services, enabling the provision of more cost-effective products that meet the needs of medical institutions at various levels. The pressing challenge of limited economic benefits in clinical mass spectrometry must be addressed by resolving the issue of domesticating mass spectrometer technology; therefore, the localization of mass spectrometer manufacturing is imminent.

Imported mass spectrometry manufacturers have not deployed reagents, failing to establish a complete clinical mass spectrometry product portfolio, which creates opportunities for accelerating the localization of instruments.Currently, in the clinical sector, Chinese clinical mass spectrometry companies have captured a significant market share by relying on OEM instruments and self-developed reagents. This has fostered high acceptance of domestic clinical mass spectrometry brands among healthcare providers, thereby facilitating the subsequent entry of domestically produced mass spectrometers into the clinical market.

Currently, enterprises involved in the development of domestically produced mass spectrometers fall into two categories.One category is life science instrumentation companies., these companies have been quite active in the R&D of domestically produced mass spectrometers, but they lack a deep understanding of reagent varieties and clinical needs.Another category comprises clinical mass spectrometry companies., such enterprises are well-versed in clinical needs and possess strong application development capabilities, but lack sufficient hardware development expertise. They can develop “small yet sophisticated” instruments tailored to clinical demands, thereby establishing differentiated competition against imported instruments.

The development of clinical mass spectrometers requires not only equipment development capabilities but also extensive clinical experience, including familiarity with physicians’ testing habits, pain points, and reporting requirements, to ensure that domestically produced mass spectrometers meet clinical needs. Therefore, companies possessing both hardware development strength and clinical insights hold a unique advantage in the development of clinical mass spectrometers. It is anticipated that more clinical mass spectrometry companies with reagent development capabilities and clinical service expertise will extend their operations into the instrument sector to develop domestically produced clinical mass spectrometers.

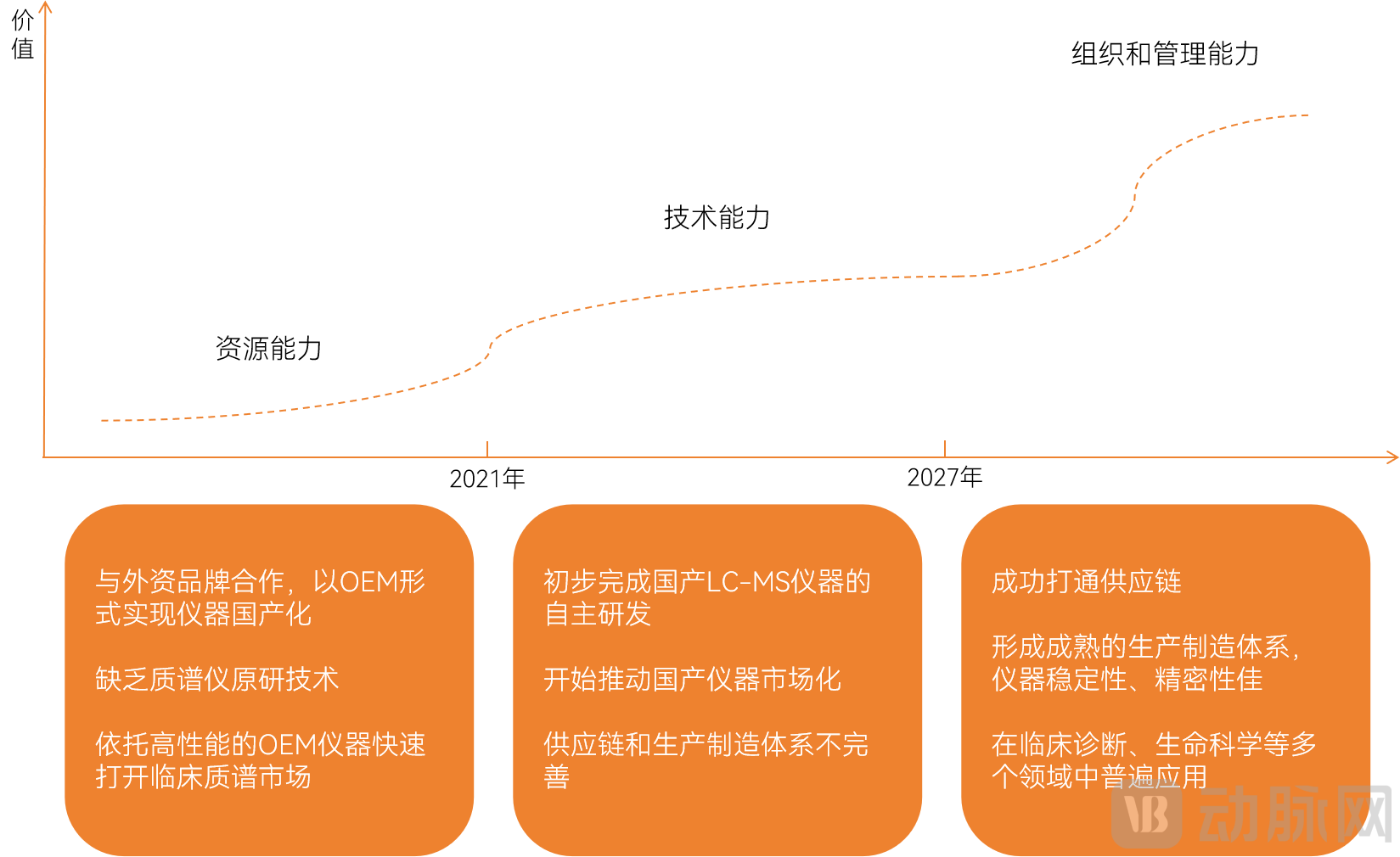

The localization process of LC-MS mass spectrometers can be divided into three stages.Phase I: Collaborating with foreign brands through OEM/ODM models for private-label product registration; currently, most enterprises are at this stage;Phase II: A small number of enterprises have independently developed LC-MS instruments and obtained registration certificates, such as Anyipu, Puju Medical, and Jingke Biology; however, the related supply chain and manufacturing systems are not yet mature, and there is no established clinical application.Phase III: Chinese-made mass spectrometers are being deployed on a large scale in clinical settings, with mature supply chain and manufacturing systems.

Progress in the Localization of LC-MS Instruments

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1: Quantifying Industry Changes in 2023: Clinical Mass Spectrometry Enters a Period of Steady Development

1.1 Surge in Registration Certificates: First-Time Approvals for New Products Including Ceramide Testing and Nucleic Acid Mass Spectrometry

1.2 Macro Cooling in the Primary Market: Omics and Domestically Produced Compact Mass Spectrometers Gain Attention

1.3 Continuous Breakthroughs in Automation: Fully Automated Mass Spectrometry Integrated Systems Gain Attention

1.4 The Trend of Domestic Substitution Continues, Achieving a “Zero” Breakthrough in High-Resolution Mass Spectrometers

Chapter 2 Clinical Survey: Vitamin Testing Is Widely Conducted, with Profitability Being the Dominant Factor Influencing the Adoption of Mass Spectrometry Projects

2.1 The Complexity of LC-MS Poses Challenges for Large-Scale Clinical Application

2.2 Microbial Mass Spectrometry and ICP-MS: Simpler and More User-Friendly

Chapter 3: Automation, Localization, and Miniaturization—A Multi-Pronged Approach to Addressing Pain Points Within Hospitals

3.1 The Prevalence of Automated Pre-analytical Systems: Fully Integrated All-in-One Analyzers as the Ultimate Solution

3.2 Innovation Application Layout: Accelerating the Commercialization of Early Screening and Diagnosis for Major Diseases

3.3 Chinese-made POCT Mass Spectrometry Leads Globally, with Accelerating Clinical Application

3.4 From Self-Developed Instruments to a Complete Industrial Chain: Accelerating the Localization of LC-MS in China

3.5 Clinical Demand, Healthcare Reform, and Corporate Development Needs Drive Companies to Optimize Platform Layout

Chapter 4: Deploying Scientific Research Services and New Drug Development to Break the Boundaries of Clinical Mass Spectrometry Applications

Chapter 5 Corporate Case Studies

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please proactively request the document.