How Domestic Bispecific Antibodies Are Dominating: Record-Breaking BD Deals, Head-to-Head Trial Wins, and Massive Financing

Akeso

Innovative Antibody Drug Developer

Alphamab Oncology

Developer of Antibody and Protein Macromolecule Drugs

NJCTTQ

Major Pharmaceutical R&D Company

Recently, the bispecific antibody field has been rapidly gaining momentum.

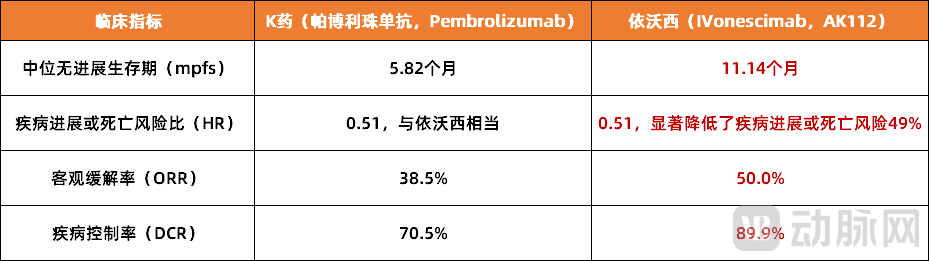

Figure 1. Clinical comparison of Ivonescimab and Keytruda in the treatment of patients with PD-L1-positive non-small cell lung cancer (Data source: public information)

Figure 1. Clinical comparison of Ivonescimab and Keytruda in the treatment of patients with PD-L1-positive non-small cell lung cancer (Data source: public information)

First, on the product front. On September 9, Akeso announced head-to-head Phase III clinical data comparing its independently developed, first-in-class PD-1/VEGF bispecific antibody ivonescimab monotherapy with pembrolizumab monotherapy (i.e., “Keytruda”) at the 2024 World Conference on Lung Cancer:Ivonescimab monotherapy demonstrated superior outcomes in median progression-free survival (mPFS), hazard ratio (HR), objective response rate (ORR), and disease control rate (DCR).It is worth noting that “K drug” (Keytruda) is one of the most effective anticancer drugs in history and currently the world’s highest-selling “blockbuster drug.” Ivonescimab’s recent success in a head-to-head trial is therefore highly significant.

Almost on the same day, Candid Therapeutics announced the completion of a $370 million financing round,This is the largest financing round in the biopharmaceutical industry to date this year., and this round of financing is also closely related to bispecific antibodies. It is reported that the launch of Candid involved the acquisition of two biotechnology companies, Vignette Bio and TRC 2004, along with their key assets. One pipeline candidate, CN106, is EMB-06, a BCMA-targeting T-cell engager (TCE) molecule licensed from WuXi Biologics’ subsidiary, Harbour Biomed (also known as Anmai Biopharma), by Vignette Bio; the other pipeline candidate, CN261, is GB261, acquired by TRC 2004 from Genor Biopharma. Both are bispecific antibody drugs.

Furthermore, positive news regarding bispecific antibodies has recently emerged from the secondary market, which had been quiet for an extended period. On September 13, Zenas BioPharma and Bicara Therapeutics simultaneously held their IPO listings on the Nasdaq. The core pipelines of both biotech companies focus on bispecific antibody drugs; Zenas possesses the bifunctional monoclonal antibody obexelimab, while Bicara holds the EGFR/TGF-β bispecific antibody BCA101.In the increasingly tense secondary market, the listing of two companies in a single day undoubtedly underscores the heated momentum in the bispecific antibody sector.。

So, what is driving the current hype around bispecific antibodies?

Who Quietly Ignited the Enthusiasm for Bispecific Antibodies?

In fact, the initial surge in bispecific antibodies occurred in 2022. That year, four bispecific antibody drugs were approved for marketing worldwide, including Roche’s blockbuster bispecific antibody Vabysmo and Akeso’s globally first-in-class PD-1/CTLA-4 bispecific antibody, Cadonilimab. Since then, major global pharmaceutical companies have increasingly invested in bispecific antibody research and development, seeking to capitalize on the “bispecific antibody boom” through collaborations or the introduction of early-stage clinical projects and high-level technology platforms.

The reason why the giants have acted in this manner is largely due to their recognition of the clinical value of bispecific antibody drugs. It is reported that,Compared with monoclonal antibody ADCs, bispecific antibody ADCs are characterized by having two antigen-binding sites. By binding to both tumor cells and immune cells, they enhance tumor-killing efficacy. Furthermore, engaging two distinct cell-surface epitopes can reduce off-target side effects, while dual-target engagement blocks two different signaling pathways, thereby augmenting cytotoxicity and overcoming drug resistance.。

However, this is only one side of the story. As with most innovative drugs, commercialization remains a major hurdle on their path to development, and the industry is awaiting the “report card” for the bispecific antibody sector. Judging from this year’s annual reports, bispecific antibodies have become a key driver of performance growth, and even a turning point from loss to profit, for major pharmaceutical companies.

Figure 2. Overview of globally marketed bispecific antibody drugs (Data source: Jinduan Research Institute)

Figure 2. Overview of globally marketed bispecific antibody drugs (Data source: Jinduan Research Institute)

Take Akeso as an example. In 2023, Akeso achieved annual profitability through its bispecific antibody products. Ivonescimab (a PD-1/VEGF bispecific antibody) secured a $500 million upfront payment, while cadonilimab, the first domestically produced bispecific antibody in China, recorded sales of RMB 1.358 billion, demonstrating strong growth momentum. From an international perspective, in the first half of 2024, Roche’s two non-oncology bispecific antibodies—a FIX/FX bispecific antibody for hemophilia and a VEGF/Ang2 bispecific antibody for ophthalmic diseases—generated combined sales of $4.8 billion. This not only drove Roche’s performance growth but also significantly expanded the global market size for bispecific antibody drugs.

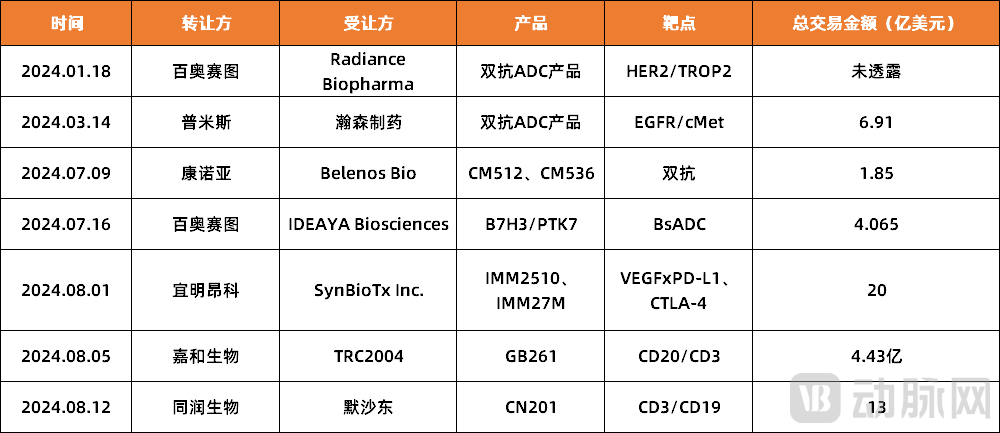

In addition, bispecific antibody (BsAb) in-licensing and out-licensing deals are booming, with many pharmaceutical companies rapidly recouping their investments. Since the beginning of this year, seven domestic pharmaceutical companies have completed licensing transactions for bispecific antibody drugs. Among them, Tongrun Bio has drawn the most attention. On August 9, Merck & Co. announced that it had reached a final agreement with Tongrun Bio to acquire CN201, a novel bispecific antibody developed by Tongrun Bio for the treatment of B-cell-related diseases, through its subsidiary. It is reported thatThe upfront payment for this deal reached as high as $700 million, marking the second-largest upfront payment ever secured in a cross-border licensing-out transaction by a Chinese biotech company., second only to the $800 million upfront payment received by Bristol Myers Squibb (BMS) for the overseas licensing of Ailicentis’s novel bispecific ADC. With this substantial income, Tongrun Bio’s cash flow has been significantly bolstered.

Looking back, the resurgence of bispecific antibodies this year essentially validates their business model, which is crucial in the current climate that emphasizes profitability and cash flow. So, what exactly has driven bispecific antibodies to become a viable business?

This is reflected on multiple levels. In addition to the clinical value mentioned above, it also lies in its broad range of application areas,Although bispecific antibodies are currently primarily used in oncology, their therapeutic potential is being increasingly explored in autoimmune diseases, ophthalmic disorders, hemophilia, and other indications.. Meanwhile, with continuous technological advancements and industrial scale-up, the production costs of bispecific antibody drugs are expected to gradually decrease, enabling more patients to afford these highly effective therapeutic agents and significantly improving drug accessibility.

In this regard, a professional noted, “The anti-tumor field already has many effective monoclonal antibodies and other therapeutic options. Therefore, for bispecific antibodies to stand out in the market, they must demonstrate unique advantages. In terms of actual performance, they show certain competitiveness in efficacy, safety, and cost. Furthermore, unlike monoclonal antibodies that target only a single indication, bispecific antibodies can be extended to areas such as hemophilia and ophthalmic diseases, which involve large patient populations and represent a huge market.”

Are Domestic Bispecific Antibodies “Killing It”?

From the perspective of many industry insiders,Bispecific Antibody-Drug Conjugates (ADCs) represent one of the few therapeutic areas where Chinese pharmaceutical companies can directly compete with, and even lead, their overseas counterparts.。

Figure 3. Global Bispecific Antibody ADCs in Clinical Development (16 Candidates) (Source: Insight; data as of the end of May 2024)

Figure 3. Global Bispecific Antibody ADCs in Clinical Development (16 Candidates) (Source: Insight; data as of the end of May 2024)

This is not without basis. First, in terms of absolute numbers, according to the Insight database, as of the end of May 2024,A total of 16 bispecific antibody-drug conjugates (ADCs) have entered clinical stages globally, with the majority originating from Chinese pharmaceutical companies., including Baili Tianheng, Alphamab Oncology, and Chia-Tai Tianqing. Furthermore, in the critical area of R&D, nearly half of the global bispecific antibody projects are developed by Chinese companies, with leading enterprises such as Hengrui Medicine, CSPC Pharmaceutical Group, and Hansoh Pharmaceutical making significant strategic investments.

In terms of key product efficacy, domestically produced bispecific antibodies are by no means inferior. For instance, as previously mentioned, ivonescimab monotherapy not only outperforms “Keytruda” across various metrics but also demonstrates a significant advantage. Taking median progression-free survival (mPFS) as an example, ivonescimab achieved 11.14 months, nearly five months longer than that of “Keytruda.” In response, industry insiders commented, “This is a rare and substantial breakthrough.”

Of course, Chinese-made bispecific antibodies are not solely reliant on Ivonescimab; Baili Tianheng’s BL-B01D1 is also a representative product. In December 2023, Baili Tianheng licensed BL-B01D1 to Bristol Myers Squibb (BMS) in a deal valued at up to $8.4 billion, setting a new record for the overseas licensing of Chinese-developed ADC novel drugs. BMS’s substantial investment was undoubtedly driven by the recognized value of BL-B01D1. Currently, there are seven Phase III clinical trials of BL-B01D1 underway, covering indications such as lung cancer, breast cancer, nasopharyngeal carcinoma, and esophageal squamous cell carcinoma. Additionally, 14 Phase II clinical trials are being conducted simultaneously, encompassing more than 10 tumor types. According to projections, BL-B01D1 is expected to launch in the United States in 2028, where it has the potential to become the world’s first approved bispecific antibody-drug conjugate (ADC). Its peak sales in the first year are projected to exceed RMB 6.9 billion.

In addition, domestic bispecific antibodies such as Alphamab Oncology’s JSKN003, Chia-Tai Tianqing’s TQB2102, and Xuanzhu Biopharma’s KM-501 also demonstrate considerable competitiveness and are currently accelerating toward their respective milestones.

This surge in collective momentum has also caught the attention of multinational corporations (MNCs). Since the beginning of this year, MNCs have been aggressively acquiring Chinese bispecific antibody-drug conjugates (ADCs), with a noticeable increase not only in the number of transactions but also in the capital invested. According to incomplete statistics from VCBeat, by the end of August this year, upfront payments for domestically produced bispecific antibodies alone had reached $3 billion. In fact, this is just the beginning; many MNCs, including Sanofi and Bristol-Myers Squibb, have stated their intention to continue seeking more merger and acquisition opportunities in China.

Figure 4. Overview of Bispecific Antibody Pipeline BD in China in 2024 (Data Source: Public Information)

Figure 4. Overview of Bispecific Antibody Pipeline BD in China in 2024 (Data Source: Public Information)

There are certainly reasons for this, with the most critical factor being the recognition by multinational corporations (MNCs) of domestically produced bispecific antibody products. After all, in the current market environment, acquired or merged products must not only generate revenue and serve as a key growth driver for MNCs’ future development, but also help them maintain their market position—all of which requires strong product competitiveness as support.

So, what exactly are the factors driving China-made bispecific antibodies to their current global leadership position?

Through conversations with multiple professionals, VCBeat identifies two key points:The first point is based on the strong engineering capabilities of domestic pharmaceutical companies.In this regard, an executive from a pharmaceutical company stated, “Although the number of bispecific antibody-drug conjugate (BsADC) drugs currently in clinical stages globally is limited, Chinese pharmaceutical companies are leading in terms of R&D volume. This can be partly attributed to the strong engineering nature of ADC drugs, which emphasizes the organic combination of three key components—a strength that aligns well with the capabilities of Chinese pharmaceutical firms.”

The second point is the fierce, cutthroat execution capability of domestic pharmaceutical companies.In this regard, a business development executive stated, “The logic of the pharmaceutical industry is that when a major breakthrough occurs in a particular therapeutic area or a blockbuster molecule emerges, the value of that entire sector skyrockets instantly. This then attracts leading enterprises to compete for market positioning, thereby initiating competition. Bispecific antibodies are no exception. Currently, domestically produced bispecific antibodies not only exhibit diverse types and rich target combinations, but multiple products have also entered the mid-to-late stages of clinical development. The next three to five years will see a concentrated period of commercialization and returns. This progress is undoubtedly driven by the intense competition within the industry.”

Furthermore, the significant enhancement of China’s innovation capabilities in the pharmaceutical sector, coupled with the minimal gap between domestic and international development timelines in the bispecific antibody field, are key factors enabling Chinese-made bispecific antibodies to stand out.

Hidden “Perils” Behind the $10 Billion Market

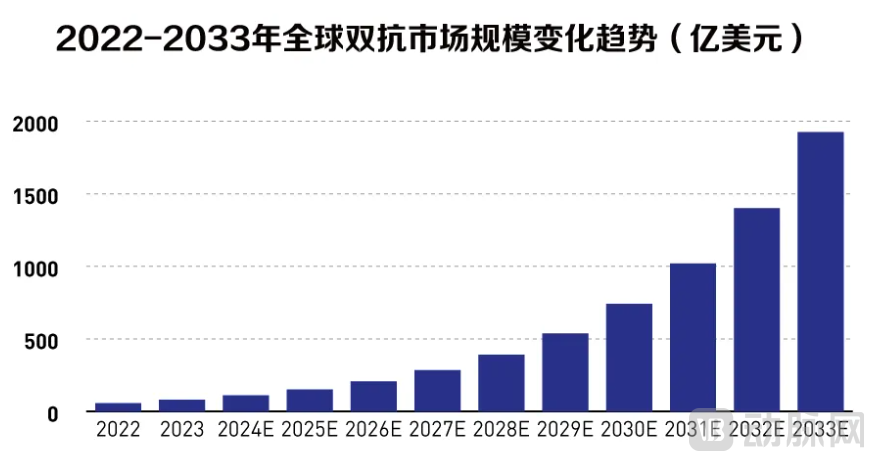

According to Frost & Sullivan’s forecasts, the growth rate of bispecific antibodies will surpass that of monoclonal antibodies in the future.By 2030, the global market size is projected to reach $80 billion, with China’s market exceeding $10 billion.Southwest Securities also expressed the same view, projecting that the market size of bispecific antibodies in China will grow from approximately USD 50 million in 2021 to USD 10.8 billion in 2030, with a compound annual growth rate (CAGR) of 81.7% from 2022 to 2030.

Figure 5. Global Bispecific Antibody Market Size, 2022–2033 (Source: Market.us data)

Figure 5. Global Bispecific Antibody Market Size, 2022–2033 (Source: Market.us data)

This is undoubtedly a market with immense potential, but it is no easy feat for domestically produced bispecific antibodies to capture significant share. They must not only navigate hyper-competition to the point of saturation in the domestic market, but also face intense rivalry directly with multinational corporations (MNCs).

Take the recently high-profile ivonescimab monotherapy as an example. Although the Phase III results are encouraging, a key metric in cancer treatment—overall survival (OS)—has not yet been disclosed. Furthermore, all patients enrolled in this clinical trial were from China, which is insufficient as credentials for breaking into the international market. According to the plan, the global Phase III head-to-head clinical trial of ivonescimab against “Keytruda” was launched in October 2023, with a four-year follow-up period. This means that the overseas clinical trial pitting ivonescimab against Keytruda will not be preliminarily completed until at least September 2027. Therefore, ivonescimab still faces significant hurdles before it can secure entry into the European and American markets.

In fact, this is merely a microcosm; for other domestically produced bispecific antibodies, the challenges to achieving a true breakthrough remain formidable.

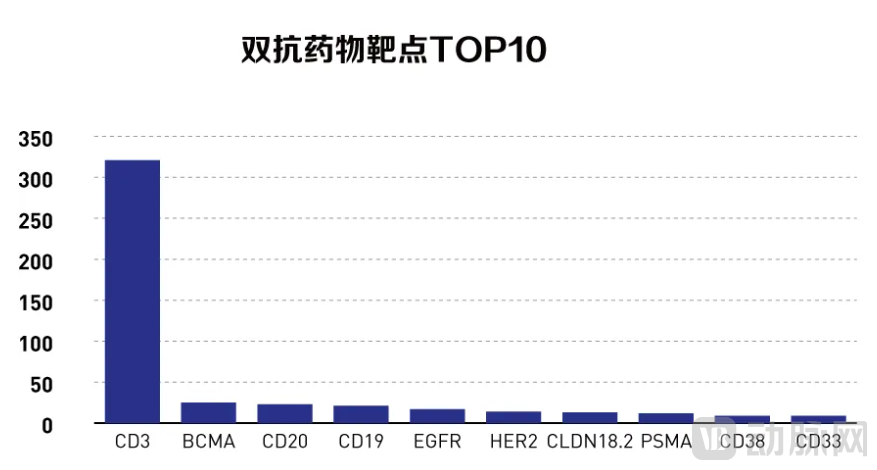

Figure 6. Top 10 Targets for Bispecific Antibody Drugs (Source: Market.us data)

Figure 6. Top 10 Targets for Bispecific Antibody Drugs (Source: Market.us data)

For instance, in the critical aspect of target selection, it is necessary to ensure that the targets exhibit both functional synergy and structural non-competitiveness; if competition exists, the two binding sites will interfere with each other, thereby compromising the mechanism of action. As of now,“CD3” has the highest utilization rate, earning it the title of the “golden target” in the bispecific antibody field.。

It is reported that the CD3 protein is one of the key molecules in the immune system, involved in activating cytotoxic T cells (CD8+ naive T cells) and T helper cells (CD4+ naive T cells), which are responsible for monitoring and defending against infections and abnormal cells in the body. The most extensively studied CD3-targeted therapies are bispecific antibodies, as CD3 bispecific antibodies can redirect CD3+ T cells to target and kill cancer cells. Among currently marketed bispecific antibody products, two-thirds target CD3, including Roche’s Glofitamab and Johnson & Johnson’s Teclistamab.

Additionally, in the realm of antibody structure design, it is equally essential to ensure the structural stability of bispecific antibodies.. Although bispecific antibodies (bsAbs) incorporate an additional specific antigen-binding site compared to monoclonal antibodies (mAbs), thereby delivering enhanced efficacy, this also renders the design, manufacturing, and clinical development of bsAbs significantly more complex than those of mAbs, with higher technical barriers. Consequently, the design of bsAbs requires a comprehensive consideration of multiple factors, including synergistic effects, structural stability, immunogenicity, preclinical validation, dosing and administration regimens, and clinical trial design.

From the perspective of industry insiders,The most promising bispecific antibody design for achieving a win-win outcome is structurally based on the PD-1/PD-L1 axis., such as PD-1/VEGF bispecific antibodies represented by ivonescimab and PD-L1/CTLA-4 bispecific antibodies represented by cadonilimab. Taking PD-L1/CTLA-4 as an example, clinical evidence shows that PD-L1 and CTLA-4 can be co-expressed on T cells; bispecific antibodies that bind both targets simultaneously can block them concurrently, yielding potentially superior efficacy. Currently, in addition to cadonilimab, other domestic candidates in this category include KN-046 from Alphamab Oncology, QL1706 from Qilu Pharmaceutical, and SIB-003 from Baili Tianheng, among which KN-046 and QL1706 have advanced to Phase III clinical trials.

Finally, it is essential to balance market competition.According to incomplete statistics, at least 16 ADC clinical pipelines worldwide terminated their R&D in 2023, involving a total of nine pharmaceutical companies. The reasons for termination were invariably due to immature technology making drug development difficult, clinical failure, project interruption caused by broken partnerships, significant financial pressure, or strategic adjustments in response to market changes. This essentially reflects the development status of the vast majority of pipelines: pressing forward amidst uncertainty.

Bispecific antibodies are no exception. Behind the industry’s fervor, setbacks such as deal terminations and pipeline closures are simultaneously unfolding. Recently, at the 2024 ESMO Congress, Immatics presented, via an oral report, the first clinical data for IMA401, a TCR-based bispecific antibody targeting MAGEA4/8 that had been licensed to Bristol Myers Squibb (BMS). The results indicated that IMA401 was well tolerated, and its antitumor activity as monotherapy was preliminarily confirmed by durable objective responses and disease control. However, Immatics also regretfully announced that BMS had elected to terminate the license agreement. The collaboration between the two companies began in 2021, and the $150 million upfront payment previously made by BMS will not be refunded.

In addition, companies such as Harbour BioMed, Kelun-Biotech, and BeiGene have also experienced license terminations or product returns. In fact, as more multinational corporations (MNCs) enter the market and leading domestic pharmaceutical companies increase their investments, industry competition will intensify. This dynamic will naturally generate numerous opportunities while simultaneously triggering a rigorous process of survival of the fittest. Therefore, amidst the heightened market activity, there is an even greater need for rational perspectives, with closer attention paid to market shifts and the intrinsic value of the products themselves.

1. “Domestic Bispecific Antibody ADCs Are ‘Killing It’” — Insight Database;

2. “Bispecific Antibodies, You’re Truly on Fire!” — Huihui Yaoka;

3. “Interview with Zhu Guidong | 8,000-Word In-Depth Article: The ‘15 Soul-Searching Questions’ on Bispecific Antibodies” — PharmCube Pro.