Galderma's IPO: Redefining Dermatological Science as the Largest Swiss Listing Since 2017

Galderma

Developer of Dermatological Medical Solutions

On March 22, 2024, Galderma rang the opening bell for its listing on the Swiss Exchange. According to public information, Galderma’s stock opened at CHF 61.00 per share, equivalent to approximately RMB 490. The company’s total market capitalization reached CHF 14.5 billion, or about RMB 116.6 billion. This valuation surpassed that of competitors such as Shiseido, Natura & Co, and Coty.making Galderma the largest IPO on the Swiss Exchange since 2017。

Galderma’s recent listing is underpinned by its ambitious growth strategy. The company stated that it will leverage the proceeds to drive its development plans for 2024 and beyond, particularly by launching differentiated biologic products, with the aim of capturing additional growth opportunities in the market and achieving margin expansion in the medium term.

Incubated by a Tech Giant, Sales Surpass $4 Billion

The origins of Galderma can be traced back to the Owen Laboratories in the United States, which focused on dermatological research. M. Owen established the laboratory in Dallas, Texas, in 1961. Subsequently, Owen Laboratories was acquired by Alcon in 1972, and in 1977, Alcon became part of the Nestlé Group.

In 1979, with the support of François Dalle, then CEO of L'Oréal, Hans Schaefer established the International Center for Dermatological Research (CIRD) in France, aiming to extend cosmetic research into the pharmaceutical sector. In 1981, Nestlé and L'Oréal jointly invested to formally establish Galderma Laboratories, with CIRD becoming the core of Galderma’s research and development efforts.Unlike the independent growth trajectories of other beauty companies, Galderma’s development resembles the outcome of strategic positioning and cultivation by capital giants in the medical aesthetics sector.

In 1995, Galderma launched Differin, its first professional brand specifically targeting acne-prone skin. Currently, Galderma has accumulated over 40 years of research experience in the field of dermatology, with five R&D centers and 55 recent patents. Since 2019, Galderma’s R&D team has comprised more than 6,500 professionals who leverage their expertise and experience in science, clinical practice, medicine, and regulatory affairs to continuously drive the company’s efficiency and innovation.

Galderma 2023 Annual Report

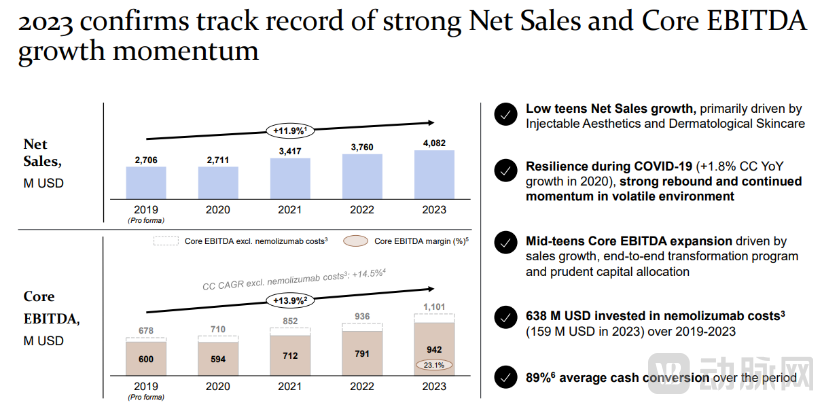

In the field of medical aesthetics, Galderma possesses significant competitive advantages.According to Galderma’s 2023 annual financial report, annual net sales surpassed the $4 billion mark for the first time, reaching $4.082 billion (approximately RMB 29.494 billion), a year-on-year increase of 8.5%.. Meanwhile, driven by double-digit growth in botulinum toxin sales, the net sales of the injectable aesthetics business increased by 6.5%. Fillers and biostimulators expanded their market share internationally and captured the number one position in the U.S. market.

As a manufacturer of hyaluronic acid fillers with triple certification from the FDA, CE, and NMPA, Galderma’s Restylane Defyne is the first and only injectable hyaluronic acid product approved in China for chin contouring.

Positioning as “Technology-Driven” Skincare, with Three Major Pipelines in Place

Backed by robust scientific research, Galderma has evolved into a dermatology brand with extensive clinical validation. Its business spans more than 90 countries and regions worldwide, with seven key markets accounting for 70% of its sales. The U.S. market stands out in particular, registering a compound annual growth rate (CAGR) of 10.1% from 2019 to 2023.

Galderma segments the dermatology market into three major areas: therapeutic dermatology, everyday skincare, and injectable aesthetics, with global market sizes reaching $53 billion, $25 billion, and $9 billion, respectively, in 2023.

Galderma’s Portfolio of Brands

In the skincare sector, Cetaphil and Alastin are two star brands within Galderma’s brand portfolio.. In 2023, Cetaphil’s sales reached approximately $1 billion, accounting for one-quarter of total sales and setting a new historical high. As the only dermatologist-recommended skincare brand included in the Physicians’ Desk Reference (PDR), Cetaphil is renowned as “scientifically formulated skincare compatible with any dermatological medication.” It offers a product range including cleansers and moisturizers that gently and comprehensively cleanse and hydrate the skin without causing irritation.

Behind Cetaphil’s commitment to “absolute safety” lies its robust capability in dermatological research. The brand has conducted more than 770 clinical trials to deepen its understanding of sensitive skin. Since entering the Chinese market in 2002, Cetaphil’s star products—including its Quadra Moisturizing Cream, cleansers, and the iconic Large Tub Body Moisturizer—have achieved monthly sales exceeding 100,000 units on its Tmall flagship store.

In addition to Cetaphil, which targets sensitive skin, Alastin, acquired by Galderma in 2022, is its second-largest skincare brand. Founded in 2015, Alastin focuses on research into post-procedural skin repair. The brand’s Chief Scientist, Alan Widgerow, is an expert in plastic surgery, facial tissue reconstruction, and wound healing, having published nearly 200 papers and two books. Under his leadership, Alastin rapidly assembled a robust team of scientists.

Compared with the skincare division, medical aesthetic injections and skin treatments are Galderma Group’s two core businesses. The cumulative growth in this segment has largely been achieved through acquisitions of independent technology and raw material companies.

Galderma’s presence in the aesthetic injectables market began in 2009, when it entered into a licensing agreement with Ipsen to secure distribution rights for Dysport (botulinum toxin type A). Dysport is indicated for the improvement of glabellar lines and has delivered over 100 million aesthetic treatments to date.

In addition to Dysport, Galderma has launched two liquid, ready-to-use botulinum toxin products: Alluzience and QM1114. Like Dysport, Alluzience is sourced from Ipsen and is the first and only liquid, ready-to-use neuromodulator in Europe. QM1114 is an independently developed product by Galderma, manufactured using a proprietary strain and advanced processes; it is a high-potency, innovative, complex-free, ready-to-use liquid botulinum toxin. Phase 3b clinical trials completed in 2023 demonstrated that QM1114 offers longer duration of effect (6 months vs. 4 months) and a faster onset of action compared to Botox, thereby providing greater convenience in use.

In the field of dermatological treatments, a key priority for Galderma is advancing the development of nemolizumab, a monoclonal antibody targeting the interleukin-31 receptor alpha (IL-31Rα). Originally developed by Chugai Pharmaceutical, a member of the Roche Group in Japan, the drug was licensed to Galderma in 2016 for development and commercialization in global markets excluding Japan and Taiwan. In 2024, Galderma announced that the U.S. Food and Drug Administration (FDA) had approved Nemluvio® (nemolizumab) for the treatment of adult patients with prurigo nodularis. The product is administered via subcutaneous injection using a pre-filled pen.

Intense Market Competition and Escalating Involution

The medical aesthetics sector is fiercely competitive, with Galderma not being the only player.

L’Oréal Group is also actively expanding into the medical aesthetics market. Its brand, SkinCeuticals, launched its first injectable product, the Platinum Research Collagen Injection, in March 2024. This product is manufactured by Jinbo Bio and contains recombinant humanized type III collagen (Type A) and 0.9% physiological saline, with a collagen concentration of 2 mg/ml. It is designed to fill the facial dermis to reduce dynamic wrinkles.

The OEM behind the product, Jinbo Bio, is the only medical aesthetics company in China to have obtained Class III medical device certification and to be listed on the Beijing Stock Exchange. In 2024, collaborations between medical aesthetics and cosmetics companies became increasingly common; for example, Lancy Co., Ltd. partnered with Haohai Biological Technology to launch hyaluronic acid products, while United Regal collaborated with Jinbo Bio to introduce New Fuyuan Collagen Skin Booster.

Prior to the collaboration between L'Oréal and Jinbo Bio, LVMH and Shiseido had already entered the medical aesthetics market. In July 2022 and September 2023, Trautec Medical secured two rounds of financing from investors including Shiseido's Ziyue Fund and L Catterton, totaling over RMB 400 million. Trautec Medical’s business spans biological raw materials, medical/cosmetic end-products, and ODM services, closely aligning with the medical aesthetics industry.

The entry of international giants marks the rise of the medical aesthetics industry, while also signaling that market competition will become increasingly intense. Compared with mature overseas medical aesthetics markets, China has a relatively low penetration rate for medical aesthetic services, but the market is in a phase of rapid growth. The "2023 Annual Insight Report on China's Medical Aesthetics Industry" projects that consumer spending in China's medical aesthetics market will grow by 20% in 2023, with the compound annual growth rate (CAGR) remaining at approximately 15% over the next four years. Despite a later start, some leading domestic enterprises are actively expanding their operations.

Among them, Imeik, Bloomage Biotech, and Haohai Biological Technology, known as the “Three Musketeers of Medical Aesthetics,” are all intensifying their investments in the collagen sector. Bloomage Biotech stated that it has seven to eight collagen products under development, has achieved the preparation of high-molecular-weight recombinant collagen, and completed the market launch of its recombinant Type III humanized collagen raw material in August. The company will promote the application of its self-produced recombinant humanized collagen raw materials in skincare products.

Haohai Biological Technology stated that it currently maintains a pipeline of multiple products under development, including smart cross-linked collagen fillers, with related R&D progress advancing in an orderly manner.

According to disclosures by Imeik, its acquired subsidiary, Harbin Peiqilong Biopharmaceutical Co., Ltd., is primarily engaged in the extraction and application of animal-derived collagen products. Possessing Class III medical device products, the company will explore additional market opportunities in the field of collagen product applications.

Amid the competition among these industry giants, China’s medical aesthetics market may gain new momentum for development. As the medical aesthetic skincare sector continues to expand, more new opportunities will likely emerge for exploration in the future.