China's $56 Billion Chemiluminescence IVD Market Sees Strong Domestic Breakthrough Amid Import Substitution

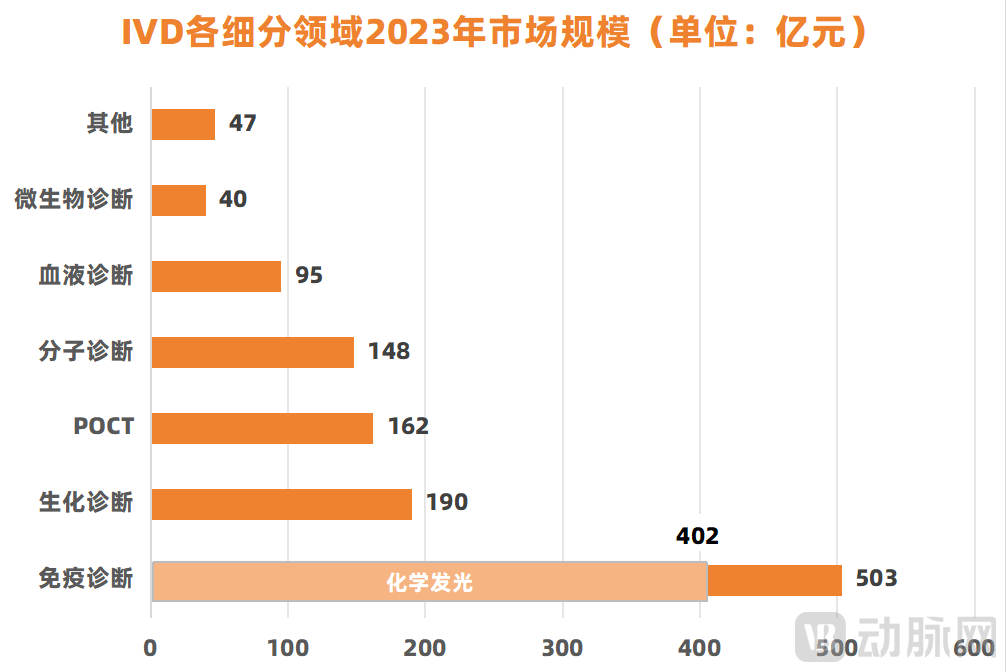

Chemiluminescence is the largest sub-sector in the IVD field and a rare blockbuster product in the medical industry, with the domestic market size exceeding RMB 40 billion in 2023.

▲Data source: Guosheng Securities, Yixiehui; Graphic by VCBeat

Yet this substantial “cake” has long been dominated by imported brands, primarily Roche, Abbott, Beckman, and Siemens, leaving domestic brands struggling to “get a slice.” Especially in tertiary hospitals, where testing requirements are more stringent and volumes are higher, this segment of the market is firmly controlled by imported brands.

“Chemiluminescence assays generally boast gross profit margins exceeding 90%. Moreover, as most chemiluminescence instruments and reagents operate within closed systems, imported brands have leveraged their first-mover advantage to secure substantial returns,” industry investor Cui Cheng (a pseudonym used at the interviewee’s request) told VCBeat.

Fortunately, in recent years, the monopoly held by imported products has begun to gradually reverse.

According to official announcements from Mindray, the company’s chemiluminescence revenue surpassed that of an imported competitor for the first time in 2023, officially securing its place among the top four players. Its strong performance has continued into the first half of this year, with chemiluminescence revenue growing by over 30%, positioning it to potentially overtake another imported brand this year. Meanwhile, other domestic brands such as YHLO, Snibe, Autobio, Maccura, and Getein are also expanding their market share. Furthermore, driven by policies such as centralized volume-based procurement, the localization rate in the chemiluminescence sector is expected to accelerate in the future.

On one hand, domestic brands are continuously advancing; on the other, market expansion is driven by increased volume from centralized procurement. Amidst the resonance of these multiple factors, the era of domestically produced chemiluminescence is arriving.

In the field of immunodiagnostics, chemiluminescence immunoassay (CLIA) is not a novel concept: it was first developed as early as the 1970s.

However, due to the immaturity of the technology at that time, such as limitations including short light signal duration and low sensitivity, the industry did not apply CLIA to clinical testing.

Over the subsequent half-century, as scientists discovered that derivatives such as horseradish peroxidase, acridinium esters, and adamantane, along with nanoparticles, could enhance the luminescence intensity of CLIA, this method has gained increasing mainstream recognition within the industry.CLIA has gradually become the mainstream of global immunoassay diagnostic technology.Meanwhile, the range of test items is extensive, encompassing hundreds of biomarkers, including tumor markers, cardiac markers, brain injury markers, inflammation, infection, thyroid function, infectious diseases, glucose metabolism, hypertension, sex hormones, bone metabolism, and anemia.

“From the perspective of product form, chemiluminescence comprises instruments and reagents that form a closed system, with no open systems available. Most items are classified as Class III registered products, characterized by high technical thresholds, difficult market access, and significant barrier advantages,” stated Cui Cheng, an industry investor.

In terms of technical pathways, CLIA technology has undergone multiple iterations and has formed five major technical pathways: direct chemiluminescence, enzyme-catalyzed chemiluminescence, electrochemiluminescence, photo-initiated chemiluminescence, and liquid-phase chemiluminescence.

▲ Source: IVD Research Club; Chart by VCBeat

“Companies adopting both enzyme-promoted chemiluminescence and direct chemiluminescence pathways account for the largest proportion in the industry., with the combined total reaching at least 70%.” Cui Cheng, an industry investor, noted that each technological pathway has its own advantages and disadvantages, as well as its representative companies.

Specifically,Direct ChemiluminescenceThe technology employs labels such as acridinium esters and isoluminol (ABEI) to tag antigens or antibodies. During the reaction of the labeled complexes, decomposition and chemiluminescence are achieved simply by adding an oxidant to create an alkaline environment, resulting in high reaction efficiency.

On this path, both Abbott and Siemens, two imported brands, have adopted direct chemiluminescence technology using acridinium esters as labels.

Enzyme-Enhanced ChemiluminescenceThis approach utilizes the catalytic activity of labeled enzymes to induce luminescence in the luminophore (substrate). The advantage of this technical pathway is its high sensitivity, albeit with slower reaction kinetics. Currently, among imported brands, Beckman Coulter is the representative company for this pathway.

It is understood that Beckman’s microparticle enzyme immunoassay system uses AMPPD as the chemiluminescent substrate. Under the action of alkaline phosphatase (ALP), AMPPD rapidly loses its phosphate group to generate an unstable intermediate, AMPD. This intermediate undergoes intramolecular electron transfer and cleavage, yielding one molecule of adamantanone and one molecule of methyl m-oxybenzoate anion in an excited state. When the anion returns to its ground state, it emits light at 470 nm.

The detailed principles of electrochemiluminescence, photo-induced chemiluminescence, and liquid-phase chemiluminescence will not be elaborated further. Currently, the representative imported brands for these three technological pathways are Roche, Siemens, and Lumigen, respectively.

Furthermore, based on the level of automation of the instruments, chemiluminescence immunoassay can be classified into semi-automated analyzers (SA) and fully automated analyzers (AA). Among these, most semi-automated analyzers utilize microplate-based chemiluminescence, while fully automated instruments are referred to as tube-based chemiluminescence analyzers.

The “multi-pronged” technological approaches have yielded a rich array of products, thereby creating a diversified supply. Meanwhile, as Chinese residents’ awareness of disease prevention and screening rises, demand for chemiluminescence diagnostics remains robust.Efficient matching of supply and demand has driven the continuous growth of the chemiluminescence market.

According to data from Guosheng Securities, the compound annual growth rate (CAGR) of China’s chemiluminescence market has remained above 20% in recent years, despite its scale already reaching tens of billions of yuan, marking it as a high-growth niche segment.

“The market is vast, but to enter this blue ocean, the key to achieving domestic substitution lies in mastering core technologies and forging a differentiated path,” said Cui Cheng, an industry investor.

Domestic brands are rapidly catching up in the fierce competition within the chemiluminescence market.

For instance, in terms of market share, domestic brands have shown significant improvement. The results of the centralized procurement of chemiluminescence immunoassay (CLIA) reagents across 25 provinces, led by Anhui Province and implemented in December 2023, revealed that domestic manufacturers ranked high in reported volumes for multiple product categories. Based on the reported volumes, projects from Mindray Medical, Snibe Diagnostics, and Autobio Diagnostics were all included in Group A. Their respective market shares were 10.0%, 6.4%, and 4.2% for the six-item sex hormone panel, and 15.9%, 5.5%, and 22.1% for the eight-item infectious disease panel.

“Past experience indicates that centralized procurement has played a significant role in driving the volume growth of domestic brands' products.“For instance, in the fields of biochemical diagnostics, hematology diagnostics, and enzyme-linked immunosorbent assay (ELISA), domestic substitution has been largely completed thanks to centralized procurement, establishing a competitive landscape dominated by Chinese brands such as Mindray Medical, Autobio Diagnostics, Snibe Co., Ltd., and Wondfo Biotech,” Cui Cheng, an industry investor, told VCBeat. He added that the chemiluminescence sector is inevitably poised to follow the same trajectory.

The key difference is that chemiluminescence presents higher barriers to entry, giving imported brands a relative advantage. Therefore, it is unrealistic to expect centralized procurement to completely reverse the import monopoly in the short term.

Faced with the current landscape, domestic brands are accelerating their catch-up with imported competitors through a strategy of “accelerated product iteration combined with high cost-performance,” thereby positioning themselves not only to capture greater share in the Chinese market but also to compete head-to-head with international brands in overseas markets.

“In our view, there is no such thing as ‘overtaking on a bend’ in the field of medical device innovation; it is all about ‘overtaking on a straightaway.’ This is because technologies and products are developed through steady, incremental updates and iterations,” said Cui Cheng, an industry investor. “To capture market share, companies must rely on genuine technology and robust products.”

Well aware of this, domestic brands have been making concerted efforts to refine their products. Taking Mindray as an example, the company formally entered the chemiluminescence field in 2013 with the launch of its first immunoassay analyzer, the CL-2000i. In 2015, Mindray introduced the CL-1200i chemiluminescence immunoassay analyzer, capable of processing 180 tests per hour. The CL-6000i chemiluminescence immunoassay analyzer was launched in 2017, followed by the fully automated CL-6000i M2 in 2019. In 2024, Mindray unveiled the CL-2600i fully automated chemiluminescence immunoassay analyzer. This rapid pace of product iteration in the chemiluminescence segment has accelerated the growth of Mindray’s chemiluminescence business, enabling it to surpass one imported brand for the first time in 2023 and rank fourth in market share within China.

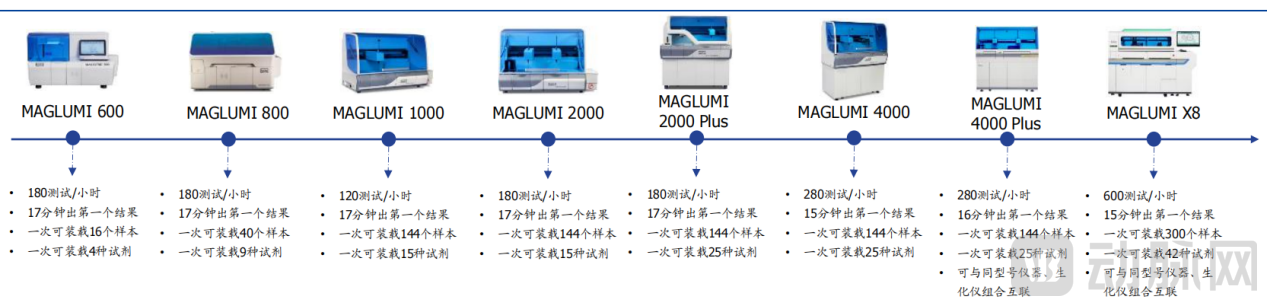

Taking the emerging industry as an example, the company has continuously innovated its chemiluminescence instruments for over a decade, progressively iterating from the MAGLUMI 600 to the MAGLUMI X8, with continuous improvements in performance and specifications. Notably, the MAGLUMI X8 is among the leading chemiluminescence immunoassay analyzers globally to achieve a breakthrough single-unit throughput of 600 tests per hour. Furthermore, the company’s higher-throughput MAGLUMI X10 chemiluminescence immunoassay analyzer was released this February, positioning it to further capture the high-end market.

▲Snibe's Chemiluminescence Immunoassay Analyzer Update Cycle

Image Source: Guosheng Securities

Currently, domestically produced instruments have reached international top-tier levels in parameters such as sample positions, reagent positions, turnaround time, and detection pathways. The gap between some of these products and imported brands is minimal, with certain individual metrics even surpassing those of imported counterparts.

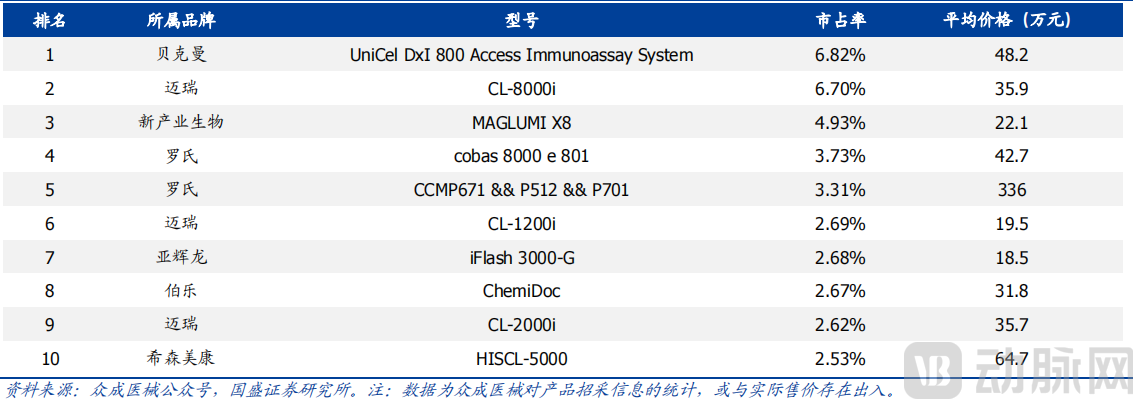

Beyond accelerating product iteration, enhancing cost-effectiveness has also become a key consideration for domestic brands.According to data from Guosheng Securities, Beckman Coulter’s UniCel DxI 800, an imported brand, ranked first in the top 10 best-selling chemiluminescence immunoassay analyzer models in China during the first half of 2024, with a market share of 6.82% and an average price of RMB 482,000. Mindray’s CL-8000i, a domestic brand, ranked second with a market share of 6.70% and an average price of RMB 359,000. Snibe’s MAGLUMI X8 ranked third, with a market share of 4.93% and an average price of RMB 221,000.

Overall comparison reveals that domestic brands such as Mindray, Snibe, and Autobio offer more competitive pricing than imported brands like Beckman and Roche, demonstrating a high cost-performance advantage.

▲Top 10 Best-Selling Chemiluminescence Instrument Models in China in the First Half of 2024

Image Source: Guosheng Securities

Of course, as imported brands continue to advance, the wave of innovation in the chemiluminescence market remains strong, so domestic brands cannot afford to relax. Recently, during surveys conducted by more than 300 institutions, Mindray stated that the company is developing next-generation high-end chemiluminescence instruments, with smooth progress. However, in this RMB 40 billion accessible domestic market, MindrayMarket share remains in the single digits, and is even negligible in overseas markets.

From this perspective, domestic brands still have a long way to go.

Despite current industry developments, the chemiluminescence sector has become an “arena” for the leading top-tier companies, with mid-tier and smaller players seeing their market shares shrink.

However, according to previous research by VCBeat, most industry professionals believe that uncertainties in the industry landscape remain.

On the one hand, China’s chemiluminescence market is poised for substantial growth—according to forecasts by Huafu Securities, the market size is expected to reach RMB 70 billion by 2030.Against the backdrop of such substantial incremental growth, the chemiluminescence market is large enough to support more innovative enterprises, making a winner-takes-all outcome difficult to achieve.

On the other hand,The chemiluminescence sector is a field characterized by multidimensional competition., covering core technologies, product quality, and channel capabilities, which leaves room for innovative enterprises to achieve breakthroughs in specific areas and then seek to expand their market scale.

For instance, in terms of distribution channels, expanding into lower-tier markets has become a consensus among some companies. It is important to note that a vast number of primary healthcare institutions and some secondary hospitals in China still rely on relatively outdated methods such as enzyme-linked immunosorbent assay (ELISA) for immunoassays. This presents an opportunity for chemiluminescence immunoassay (CLIA) to largely replace ELISA and other similar technologies.

However, unlike the industry mainstream, which generally uses more expensive high-throughput equipment, the lower-tier markets are more price-sensitive, therebyCompact chemiluminescence immunoassay analyzers with comprehensive test menus and easy maintenance are in high demand.

The relevant industry background to note is that chemiluminescence immunoassay (CLIA) platforms can be categorized into high-throughput, medium-throughput, and low-throughput systems. High-throughput systems are defined as those with a capacity of over 600 tests per hour (theoretical hourly throughput), low-throughput systems generally refer to those with a capacity below 200 tests per hour, and medium-throughput systems fall between 200 and 600 tests per hour.

According to VCBeat, in the niche segment of small-scale chemiluminescence immunoassay (CLIA), besides Getein Biotech, Wondfo, and Lifotronic, which have been deeply engaged in this field, Mindray, YHLO, and Snibe have also made substantial strategic layouts.

In addition, as leading brands focus more on deploying core, high-frequency items, a large number of low-frequency testing items remain uncovered, thereby allowing some innovative companies toSeize opportunities in low-frequency services to rapidly penetrate the market through specialized offerings.

Meanwhile, creating an open industry ecosystem that fosters broad collaboration among enterprises offering reagents, instruments, technologies, and total solutions has become a trend in recent years. For instance, by introducing an innovative diagnostic model, Fapon Biotech has attempted to establish a closed-loop commercial cycle linking “scientific research – independent clinical laboratories (ICLs) – clinical practice” to accelerate the translation of scientific achievements into practical applications. It has already assisted numerous domestic in vitro diagnostics (IVD) companies in expanding their product portfolios in areas such as chemiluminescence.

More critical to the industry is the competition for production lines.What Is a Laboratory Automation Line? It refers to an IVD enterprise’s use of track systems to connect processing modules and testing systems, thereby reducing manual operations, enhancing the level of automation, and shortening sample turnaround time.

In the field of chemiluminescence, current automated laboratory workflows are predominantly closed systems, with limited interoperability between different brands.This means that once a company’s automated laboratory line is successfully procured by a hospital, it can secure 70% or even more of the hospital’s clinical laboratory testing workload.

According to National Business Daily, the current installed base of production lines in the industry stands at approximately 3,000, with a replacement cycle of about six years. This implies that the existing market generates an annual demand for 500–600 new lines. Innovative companies that capitalize on this replacement opportunity are well-positioned to gain a competitive edge in the next round of industry competition.

It is not difficult to see that, under the new landscape, domestic brands still have many opportunities. Meanwhile, innovative enterprises at the forefront of the industry have already begun to show their strength, and it is only a matter of time before they can compete on equal footing with imported brands.

References:

1: “A Pioneer in Domestic Chemiluminescence: Import Substitution and Overseas Breakthroughs Solidify Growth Foundations” — Guosheng Securities

2: “Seeing the Value of Small-Scale Chemiluminescence Amidst the Major Chemiluminescence Wave” – IVD Research Society