The $10B+ Blue Ocean Market: MNCs' Nuclear Medicine Race Heats Up with New IPO Filing

Sanofi

Pharmaceutical Manufacturer

Mariana Oncology

Targeted Radiopharmaceuticals Developer

A new wave of innovation in the pharmaceutical industry, driven by “nuclear” technology, has arrived.

According to Evaluate’s forecast, annual sales of radiopharmaceutical therapies will exceed $6 billion in 2026. If diagnostic agents are included, the market size would double. Radiopharmaceuticals are rapidly becoming the new favorite of multinational corporations (MNCs) and investors.

Over the past few years, approximately 86 strategic transactions have been completed in the radiopharmaceutical sector, with the number of deals in 2022 nearly tripling compared to 2021. From a financing perspective, the number of funding events in the radiopharmaceutical field has steadily increased, and the scale of financing has also grown. For instance, the average financing amount in the first three quarters of 2023 ($51 million) was already double that of 2018 ($26 million).

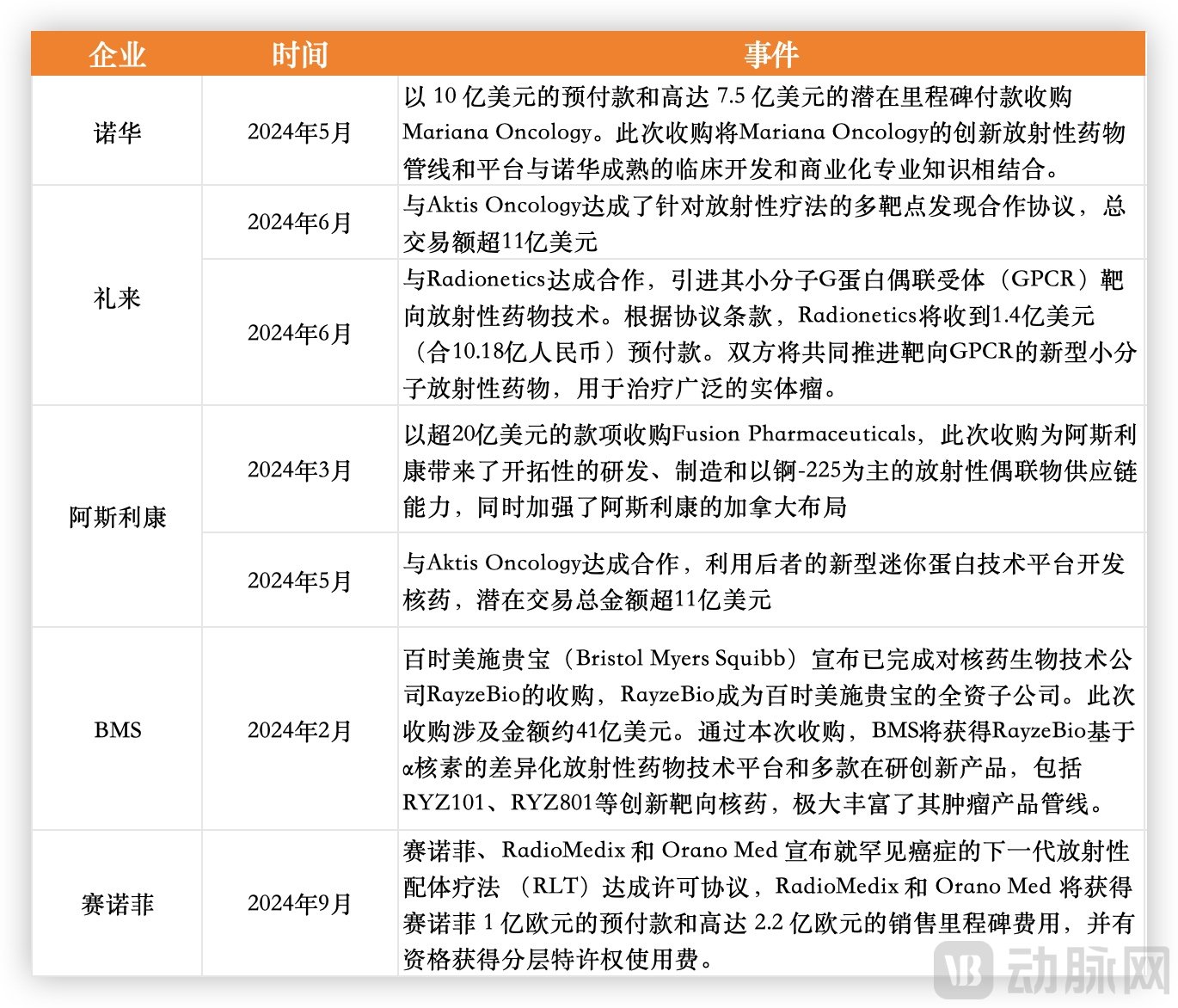

Major MNC Deals in the Radiopharmaceutical Sector This Year: Compiled from Public Information

By 2024, the radiopharmaceutical sector had not only failed to cool down but had instead intensified, becoming a fiercely contested arena for global pharmaceutical giants.

In September, Sanofi announced its entry into the “radiopharmaceutical” market with a €320 million investment, signing an exclusive licensing agreement with RadioMedix and Orano Med to jointly develop lead-based radioligand therapies (RLT) for cancer treatment.

Sanofi’s foray into the field of radiopharmaceuticals marks another strategic expansion in its pharmaceutical portfolio. With the patent for its blockbuster drug, dupilumab, set to expire in the coming years, Sanofi is urgently seeking successor products to sustain its growth.

Despite several blockbuster deals in the past two years, many multinational corporations (MNCs) have not slowed their pace in 2024; instead, they have frequently announced major transactions and actively entered the market. MNCs such as Novartis and Bayer have begun to deeply engage in the field of radiopharmaceuticals. In particular, Novartis has emerged as a leader in this sector after several years of strategic positioning.

Novartis has been the most active multinational corporation (MNC) in the field of radiopharmaceuticals in recent years, and its pace has not slowed down as of 2024.

In late April 2024, Novartis and PeptiDream entered into a collaboration agreement valued at approximately $2.9 billion (including a $180 million upfront payment, $2.71 billion in milestone payments, and tiered sales royalties) to jointly develop multiple macrocyclic peptide-targeted radiopharmaceutical conjugates. This marks another partnership between the two companies following their 2019 collaboration on cyclic peptide PDCs.

As a leader in radiopharmaceuticals, Novartis’s therapeutic RDC drugs are also regarded as one of the promising directions for conjugated therapeutics following ADCs, and their combination with cyclic peptides may represent another successful iteration after RDCs.

On May 2, Novartis announced the acquisition of Mariana Oncology to strengthen its portfolio in radioligand therapy. Under the terms of the agreement, Novartis will pay an upfront fee of $1 billion, with an additional $750 million payable upon the achievement of predefined milestones.

Mariana Oncology, founded in 2021, focuses on the development of targeted peptide radiopharmaceuticals. Its core asset, MC-339, is an actinium-based radioligand therapy under investigation for the treatment of small cell lung cancer, with its target undisclosed. Following this acquisition, Novartis has not only gained Mariana Oncology’s ligand discovery platform but also its radioconjugation platform, which leverages both alpha and beta radionuclides to address diverse therapeutic needs.

It is evident that Novartis’s strategic layout in radiopharmaceuticals has begun to permeate next-generation therapies. The confidence underpinning this move stems from the commercial returns generated by its radiopharmaceutical portfolio.

Novartis Acquires Radiopharmaceutical Company to Build Capabilities, Based on Public Information

In 2017, Novartis acquired Advanced Accelerator Applications (AAA) for $3.9 billion, thereby gaining Lutathera, a treatment for somatostatin receptor (SSTR)-positive gastroenteropancreatic neuroendocrine tumors (GEP-NETs).

The following year, Novartis’ first RDC drug, Lutathera, received FDA approval for market launch. By 2023, the drug’s sales reached $605 million, representing a 28% year-on-year increase. In the first half of this year, Lutathera generated $344 million in revenue, reflecting a 16% growth rate.

In 2018, Novartis acquired Endocyte for $2.1 billion, thereby gaining Pluvicto, a radioligand therapy for the treatment of metastatic castration-resistant prostate cancer (mCRPC), which was approved for market launch in 2022.

In its launch year, Pluvicto generated $270 million in revenue. Sales continued to surge in 2023, reaching $980 million for the full year, a year-on-year increase of over 260%, making it the highest-selling radioligand therapy globally. In the first half of this year, Pluvicto achieved revenues of $655 million, representing a 45% growth rate, and is highly likely to surpass the $1 billion mark this year. Given this strong performance, Novartis is advancing Pluvicto into earlier lines of treatment and expanding its eligible patient population.

The commercial success of two RDC drugs has prompted Novartis to continuously invest in radiopharmaceuticals.

Having integrated the resources of two companies, Novartis has established the capability to evaluate radiopharmaceuticals and has begun acquiring product rights.

During this period, Novartis has shifted its focus to products in the early stages of research and development. This strategy not only reduces transaction amounts but also enables access to diverse radionuclides, targets, and indications. For instance, through the acquisition of rights to several products in Phase 1/2 clinical trials, Novartis has secured a portfolio of FAP-targeted therapies, effectively expanding the range of tumor types with high FAP expression.

Acquisition of Partial Product Rights from Novartis, Compiled Based on Public Information

A search of ClinicalTrials.gov identified 41 clinical trials on radiopharmaceuticals targeting fibroblast activation protein (FAP). Of these, six were sponsored by pharmaceutical companies, with three belonging to Novartis (NCT04939610, NCT05262855, and NCT05641896), targeting solid tumors, pancreatic ductal adenocarcinoma, and gastrointestinal tumors, respectively.

Novartis launched a Phase 1/2 clinical trial in July 2021 investigating the theranostic application of Ga-68 FAP-2286 and Lu-177 FAP-2286, becoming the first company globally to initiate registrational clinical trials targeting fibroblast activation protein (FAP). Other companies began their trials more than two years later than Novartis. This means that if Novartis’s FAP-targeted radiopharmaceuticals successfully reach the market sequentially over the next three years, they will not only create a new growth curve but also face no direct competition.

Subsequently, Novartis began to pursue strategic collaborative development with other companies. Particularly after 2021, Novartis has sought to leverage new platform technologies to optimize the molecular properties of the targeting moieties in radiopharmaceuticals—including low molecular weight, strong tissue penetration, high affinity, precise targeting, and prolonged in vivo retention—thereby enhancing the efficacy and safety of radiopharmaceuticals and better aligning them with clinical needs.

Furthermore, Novartis has also invested in radiopharmaceutical R&D companies; for instance, its investment in Aktis Oncology enables the deep incubation of an alpha-particle labeling technology platform.

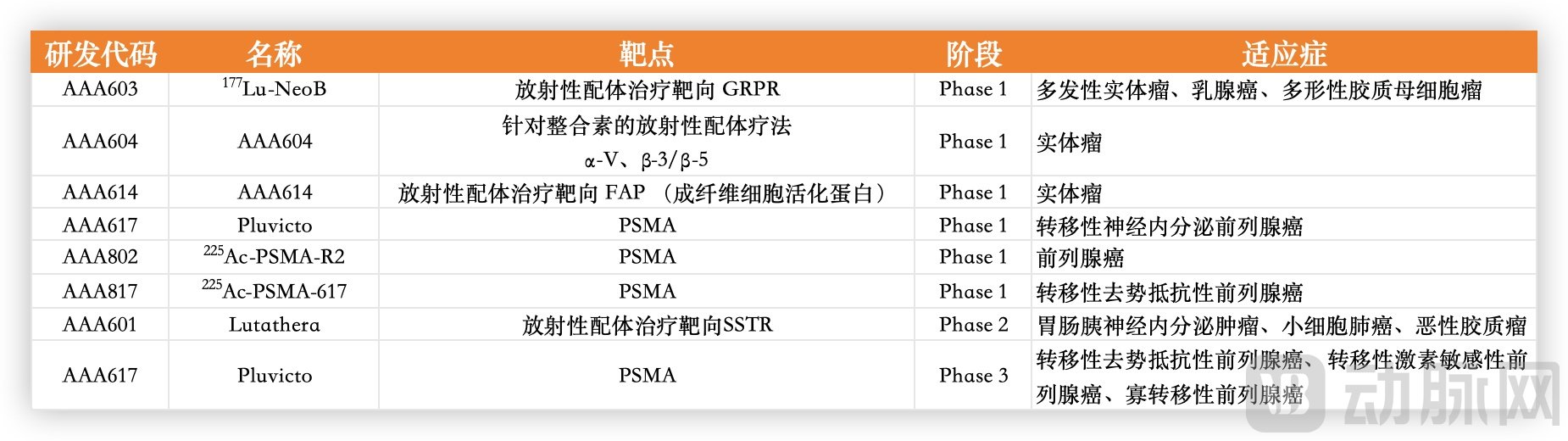

Thanks to this series of strategic moves, Novartis currently boasts a portfolio of eight radiopharmaceutical pipelines; excluding two marketed products, there are six candidates in Phase I clinical trials.

Novartis’ Radiopharmaceutical Pipeline, Data Sourced from Corporate Financial Reports

For Lutathera, which is already on the market, Novartis is expanding its indication for first-line treatment of gastroenteropancreatic neuroendocrine tumors, currently in Phase 3 clinical trials; expansions into pediatric indications, glioblastoma indications, and first-line treatment indications for extensive-stage small cell lung cancer are all in Phase 2 clinical trials.

In addition to actively expanding the indications for its marketed radiopharmaceuticals, Novartis is also developing Lu-177-labeled radioligand therapies targeting different molecules, such as gastrin-releasing peptide receptor (GRPR)-NeoB, fibroblast activation protein (FAP), and integrins αvβ3/5. These novel targets are abnormally overexpressed in various malignant tumors, including breast, prostate, pancreatic, lung, and central nervous system cancers, and are all being developed under a theranostic strategy. Notably, besides Novartis, other major multinational corporations (MNCs) and radiopharmaceutical companies are also actively laying out their pipelines for Lu-177-labeled radioligand therapies, although their targeted molecules lack significant innovation.

Summary of Clinical Trials for Novartis’s Lu-177-Labeled Novel Targeted Therapy, Sourced from ClinicalTrials.gov

Pluvicto, another marketed drug, targets PSMA. Novartis is concurrently conducting three Phase III clinical trials for prostate cancer, exploring different combination regimens and moving treatment to the first-line setting, including for oligometastatic prostate cancer. The eligible patient population is expected to continue expanding in the coming years.

The two PSMA-targeting drugs, AAA802 and AAA817, demonstrate the forward-looking nature of Novartis’s strategic layout.

Taking the two marketed RDC drugs as examples, from the perspective of drug structure, both utilize Lu-177 as their radionuclide. This isotope emits beta particles and has a half-life of approximately one week, making it suitable for eradicating small-volume tumors and metastatic lesions. With these pioneering products setting a high benchmark, RDC development has largely focused on the beta-emitting radionuclide Lu-177. However, as research deepens, pharmaceutical companies are beginning to strategize around innovative radionuclides, bringing alpha-emitting radionuclides to the forefront.

Among alpha-emitting radionuclides, Ac-225 is considered the most promising. With a half-life of 9.9 days, longer than the 6.647 days of Lu-177, it allows more ample time for production and treatment. Furthermore, due to the characteristics of the alpha particles it emits, drugs developed based on Ac-225 are theoretically expected to offer superior efficacy and safety compared to those based on Lu-177.

Not just Novartis; many multinational corporations (MNCs) have made strategic moves around Ac-225.

Including Mariana Oncology, acquired by Novartis for $1.75 billion; Point Pharma, acquired by Eli Lilly for $1.4 billion; RayzeBio, acquired by BMS for $4.1 billion; and Fusion Pharmaceuticals, acquired by AstraZeneca for $2 billion, all of which have pipelines based on Ac-225. The frequent transactions also indicate that products based on Ac-225 will be a key competitive area in the future.

Given that radiopharmaceuticals are subject to strict regulation across research and development, clinical trials, manufacturing, and clinical use, Novartis’s first-mover advantage in the radiopharmaceutical sector is expected to persist for some time.

It is clearly not what other MNCs want to see Novartis dominate the field alone, as the radiopharmaceutical sector has become a fiercely contested battleground for MNCs.

The commercialization of radiopharmaceuticals faces exceptionally high barriers, including the need for a mature and comprehensive upstream and downstream supply chain, as well as substantial capital investment across multiple stages such as production and transportation. For radiopharmaceutical biotech companies, navigating this path independently is extremely challenging; selling to well-capitalized multinational corporations (MNCs) may be a more viable option. Meanwhile, entering new therapeutic areas through mergers and acquisitions or collaborations is a standard strategy for MNCs.

Take Bayer, which has also been deeply engaged in the field of radiopharmaceuticals for many years, as an example. Although Bayer’s radium-223 drug, Xofigo, was approved for marketing in 2013 for the treatment of prostate cancer, the company has since continued to strengthen its R&D capabilities and market influence in the radiopharmaceutical sector through the acquisitions of companies such as Algeta, Noria, and PSMA Therapeutics.

Through these acquisitions, Bayer not only secured exclusive rights to an actinium-225-based targeted alpha therapy directed against prostate-specific membrane antigen (PSMA), but also expanded its existing portfolio of tumor-targeted alpha therapies (TAT). Subsequently, in May 2023, Bayer entered into a strategic collaboration with Bicycle Therapeutics plc to jointly develop multiple bicyclic peptide-targeted radioligand conjugates.

Other multinational corporations (MNCs), such as AstraZeneca, Roche, and Eli Lilly, are also actively entering the radiopharmaceutical sector through equity investments and technology licensing. For instance, in October 2023, Eli Lilly announced its acquisition of POINT Biopharma, thereby securing a portfolio of late-stage clinical radiopharmaceuticals, including PNT2002 and PNT2031.

In December 2023, Bristol Myers Squibb (BMS) acquired RayzeBio, a radiopharmaceutical company founded just over three years earlier, for $4.1 billion, propelling the radiopharmaceutical market to new heights. In March 2024, AstraZeneca announced the acquisition of Fusion Pharmaceuticals, gaining access to its pipeline of actinium-based radioconjugate drugs, as well as related research and development and manufacturing facilities.

Roche and Merck & Co. have primarily adopted collaborative strategies to establish their presence in the field of radiopharmaceuticals. For instance, as early as 2021, Merck partnered with Fusion Pharmaceuticals to evaluate combination therapies involving radiopharmaceuticals and Keytruda (pembrolizumab). In March 2023, Merck further advanced its radiopharmaceutical R&D through a collaboration with Ratio Therapeutics. Roche entered the radiopharmaceutical sector by entering into a radiopharmaceutical R&D partnership worth over $1 billion with PeptiDream in September 2023.

AstraZeneca entered the radiopharmaceutical sector in March this year by acquiring Fusion Pharmaceuticals for $2.4 billion. However, as early as 2020, AstraZeneca had already partnered with Fusion to develop and commercialize next-generation alpha-particle radiopharmaceuticals and combination cancer therapies. In April 2023, Fusion announced that its Investigational New Drug (IND) application had been accepted, paving the way for joint development with AstraZeneca. Thus, the acquisition was a logical next step.

From AstraZeneca’s perspective, Fusion is also highly valuable. First, it possesses an alpha-nuclide platform and a relatively advanced product pipeline. Although Fusion’s 225Ac-PSMA is not among the most advanced in terms of development progress, it remains within the first tier. Second, Fusion features a specialized linker design platform that can reduce the circulation of unbound drug molecules in the body, thereby enhancing safety. Leveraging this platform, Fusion can continuously generate combination molecules such as FPI-2068 using validated precursors, providing a distinct advantage in the validation of clinical candidates. Finally, there is its Ac-225 production and CMC (Chemistry, Manufacturing, and Controls) capabilities.

Completing the build-out of supply chain and production-distribution capabilities through mergers and acquisitions has become a standard playbook for multinational corporations (MNCs) entering the market. Indeed, the inherent characteristics of radiopharmaceuticals make acquisition by MNCs one of the optimal exit strategies for radiopharmaceutical biotech companies, given the substantial challenges associated with their commercialization.

Even Novartis has encountered challenges in the commercialization of radiopharmaceuticals.

The China Isotope and Radiation Association projects that the domestic radiopharmaceutical market will reach RMB 9.3 billion in 2025 and further expand to RMB 26 billion by 2030. Faced with such a promising market, Novartis is certainly not going to sit on the sidelines.

According to information on the CDE website, Novartis has been preparing for the launch of radiopharmaceutical R&D in China since 2000. Clinical trial applications indicate that its R&D strategy in the Chinese market continues to focus on integrated theranostics, indication expansion, and earlier intervention in treatment.

Notably, Novartis initially introduced only Ga-68-labeled radiodiagnostic agents and Lu-177-labeled radiotherapeutic agents for clinical development in China. It was not until 2023, driven by a global synchronized development strategy, that Novartis introduced NeoB, an integrated theranostic agent.

Not only in the clinical arena, but Novartis has also made extensive preparations to support the approval and launch of Pluvicto in China.

Given that Pluvicto has a shelf life of only five days from the time of factory packaging (compared to just three days for Lutathera), establishing local manufacturing facilities in target markets has become an imperative. To this end, Novartis has invested in building a new radiopharmaceutical production base in China to ensure supply coverage for China and surrounding regions. The facility is located in the Nuclear Technology Application (Isotope) Industrial Park in Haiyan County, Jiaxing City, Zhejiang Province. With total investment expected to exceed RMB 600 million, the plant is scheduled to commence operations by the end of 2026.

Furthermore, Novartis China will establish a new Radioligand Therapy team, building upon its existing breast cancer, hematology oncology, and lung cancer and solid tumor pipeline teams, to accelerate the introduction of innovative radioligand products in China and ensure timely access for Chinese patients.

Novartis’ CEO explicitly affirmed the value of radiopharmaceuticals and the company’s long-term commitment to this sector at JPM 2024, expressing confidence that revenue from radiopharmaceuticals will increase substantially in the coming years and account for a significant proportion of its total annual revenue.

As an increasing number of multinational corporations (MNCs) enter the field, the development of radiopharmaceuticals will accelerate further, driving innovation in oncology within the pharmaceutical industry. With more pharmaceutical companies joining the race, the radiopharmaceutical sector is experiencing unprecedented prosperity. In the future, as more radiopharmaceuticals reach the market and the industrial chain becomes more comprehensive, radiopharmaceuticals are poised to become a mainstream next-generation therapy for cancer. Who will cross the finish line first depends not only on respective R&D capabilities and commercialization strategies but also on who can better address clinical needs and prioritize patient benefits.

References:

《nature》The radiopharmaceutical renaissance: radiating hope in cancer therapy doi.org/10.1038/d43747-024-00014-w

National Nuclear Safety Administration: “2030 → RMB 26 Billion! The Domestic Market Size of Radiopharmaceuticals Continues to Expand”