Junshi Biosciences and Akeso’s New PCSK9 Inhibitors Approved, Challenging Foreign Dominance with Potential for Over 100% Market Growth

Junshi Biosciences

Innovative Drug Developer

Akeso

Innovative Antibody Drug Developer

On the evening of October 11, Junshi Biosciences announced that its angioreximab injection had been approved for marketing by the National Medical Products Administration. Angioreximab injection is indicated for the treatment of adult patients with primary (non-familial) hypercholesterolemia and mixed dyslipidemia.

Just before the National Day holiday, the National Medical Products Administration approved the marketing application for inuciximab, a Class 1 innovative drug independently developed by Akeso, for the treatment of primary hypercholesterolemia and mixed hyperlipidemia, as well as heterozygous familial hypercholesterolemia.

PCSK9 inhibitors have now become a powerful complement to classic statins, representing a highly promising class of therapeutics. Previously, the domestic PCSK9 landscape was dominated by imported brands such as Amgen, Sanofi, and Novartis. With the approval of products from Innovent, Akeso, and Junshi Biosciences, the market is poised for significant change.

On the other hand, although six products have already been approved for market launch in China, the market is far from saturated. PCSK9 inhibitors currently face pain points such as high costs and less patient-friendly administration routes, indicating significant potential for iteration. The entry of three domestically produced drugs may well mark the beginning of this transformative shift.

PCSK9 Inhibitors Are Emerging as a New Option for Combination Therapy, Owing to Their Significant Lipid-Lowering Efficacy and Favorable Safety Profile.

Cardiovascular diseases, primarily atherosclerotic cardiovascular disease (ASCVD), are the leading cause of death among both urban and rural residents in China, accounting for more than 40% of all deaths. It has been confirmed that low-density lipoprotein cholesterol (LDL-C) is a pathogenic risk factor for ASCVD. According to the Chinese Guidelines for Lipid Management (Primary Care Edition 2024), statins are the preferred strategy for lipid-lowering therapy in the Chinese population.

Although statins are effective and inexpensive for lipid-lowering therapy, their clinical application is significantly limited by the fact that doubling the dose of any statin yields only a 6% additional reduction in lipids. For patients with severe hyperlipidemia who fail to reach lipid targets with statin monotherapy, as well as for those who cannot tolerate even low-dose statins but still require lipid control to reduce cardiovascular risk, clinical guidelines recommend combining statins with PCSK9 inhibitors.

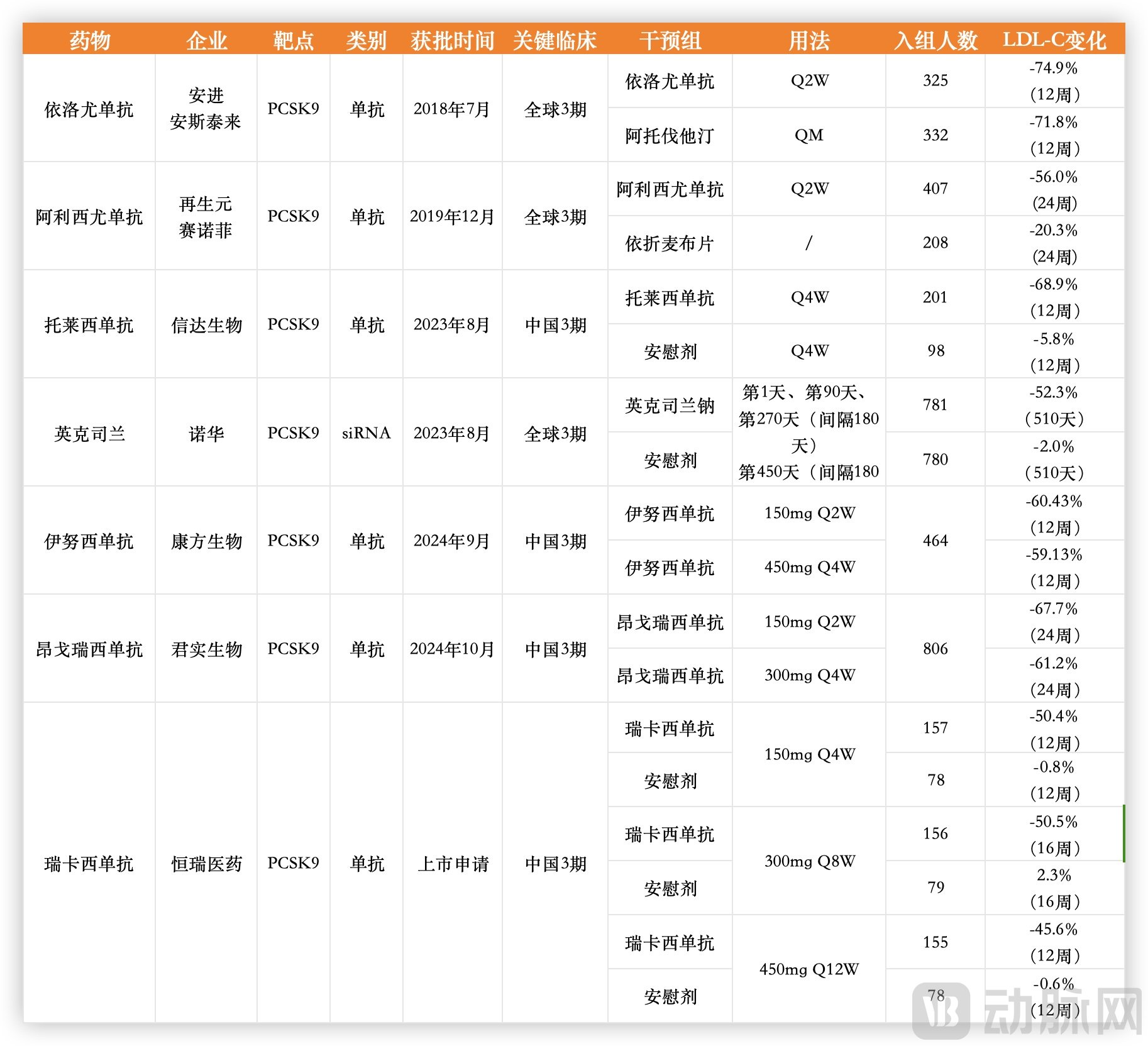

Clinical Data of Major Domestic Products (Non-Head-to-Head), Compiled from Public Information

According to clinical data, compared with statins, PCSK9 inhibitors can significantly reduce LDL-C levels by more than 50% and effectively lower the risk of cardiovascular diseases. Except for possible reactions at the injection site, the safety profile of PCSK9 inhibitors is comparable to that of the placebo group. They do not cause muscle toxicity, elevated liver enzymes, neurocognitive events, or an increased risk of new-onset diabetes, which are common side effects associated with statins, and serious adverse effects are rare. Therefore, PCSK9 inhibitors are regarded as currently the most potent, novel lipid-lowering drugs with the fewest side effects.

The emergence of PCSK9 inhibitors has also reinvigorated the field of hyperlipidemia management.

To date, six PCSK9 inhibitors have been approved for marketing in China: Amgen’s evolocumab (Repatha), Sanofi/Regeneron’s alirocumab (Praluent), Novartis’s inclisiran sodium (Leqvio), Innovent Biologics’ tolecimab, Akeso’s inucicumab, and Junshi Biosciences’ ongericimab. Additionally, Hengrui Medicine’s recaticimab is currently at the stage of filing for marketing approval.

Unlike in some previous sectors, although imported products held a first-mover advantage, it was inclusion in the national medical insurance scheme that truly drove their rapid volume growth. The subsequent approval and market launch of three domestically produced products will enable them to compete directly with imported brands in this field.

Compared with statins, which offer high quality at an affordable price, the high cost of PCSK9 inhibitors has become a significant obstacle to their commercialization.

In terms of product development, PCSK9 inhibitors represent a rather strategic category. They are not intended to replace the dominant position of statins, but rather to address their existing limitations. The emergence of PCSK9 inhibitors has not only provided patients with more treatment options but also injected new growth momentum into the blue-ocean market of lipid-lowering therapies.

Taking Amgen’s evolocumab, the first to market, and Sanofi/Regeneron’s alirocumab as examples, both were approved in 2015, yet their sales trajectories have differed significantly. Under Amgen’s commercial execution, evolocumab surpassed the $1 billion threshold as early as 2021, becoming a blockbuster product, with its revenue soaring to $1.635 billion by 2023. In contrast, alirocumab has experienced a relatively slower revenue growth in recent years, reaching only $640 million in 2023.

In the Chinese market, these two drugs were approved for launch in 2018 and 2019, respectively. However, it was not until their inclusion in the National Reimbursement Drug List (NRDL) in 2021 that they experienced rapid volume growth and a significant surge in sales revenue.

According to data from Menet, sales of evolocumab exceeded RMB 100 million in 2021, representing a year-on-year increase of 109.70%; surpassed RMB 400 million in 2022, with a year-on-year growth of 263.91%; and reached nearly RMB 1 billion in 2023, marking a year-on-year increase of 127.22%.

Alirocumab, the second PCSK9 inhibitor launched in China, initially saw a lukewarm market response. Its sales surged only after being included in the National Reimbursement Drug List, surpassing RMB 200 million in 2022 with a year-on-year growth of 779.34%. In 2023, Alirocumab’s sales exceeded RMB 500 million, representing a 141% year-on-year increase.

Inclusion in the National Reimbursement Drug List Boosts PCSK9 Sales Volume; Data Compiled from Public Sources

In terms of the landscape of lipid-lowering drugs, statins still dominate sales in the domestic market. Although novel lipid-lowering agents, represented by PCSK9 inhibitors, are growing rapidly in China, they have not triggered a significant expansion in market demand.

“On one hand, PCSK9 inhibitors are injectables with relatively low adherence; meanwhile, statins on the market can already meet basic needs as oral formulations with better adherence, and their cost of use has become negligible after being included in the national medical insurance reimbursement list with price reductions. As a result, although PCSK9 inhibitors demonstrate excellent efficacy, they have not yet gained full market acceptance,” an industry insider told VCBeat. “The market may only fully open up when more domestic brands enter the competition and drive prices down.”

In China, the unit prices of evolocumab and alirocumab have dropped from RMB 1,298 and RMB 998 per pre-filled syringe, respectively, to RMB 283 and RMB 306 after being included in the National Reimbursement Drug List (NRDL). The annual treatment cost for both drugs is approximately RMB 7,000. Taking evolocumab as an example, after insurance reimbursement, patients’ minimum annual out-of-pocket expense is around RMB 2,000. While this cost is not exorbitant, it remains significantly higher than the monthly expense of RMB 20–30 for statins; nevertheless, the price difference, though substantial, is not prohibitive.

If the story ended here, with domestic products entering the market, leveraging differentiated advantages and reasonable pricing strategies to compete and capture a share of the market, it would be a perfect script. However, reality has not unfolded as smoothly as imagined.

In 2023, Novartis’s inclisiran and Innovent’s tolesimab were approved nearly simultaneously, further bolstering this therapeutic area.

In particular, inclisiran, despite its single-dose price of RMB 9,988 and exclusion from the national medical insurance scheme—making it a fully out-of-pocket medication—would not be expected to have strong market prospects based on historical experience. However, reality has proven surprising. According to Novartis’ Q1 2024 earnings conference call, the drug attracts more than 250 new patients daily in the Chinese market. Based on a 90-day first quarter, this translates to 22,000 newly added patients in Q1.

This performance not only exceeded market expectations but also surpassed Novartis’s own projections. Novartis stated that if this sales trend continues, inclisiran’s sales in China could approach RMB 3 billion, thereby reshaping market perceptions. According to Novartis’s semi-annual report, inclisiran generated revenue of USD 333 million in the first half of 2024 (1H 2024), nearly matching the full-year sales figure from the previous year. This represents a year-on-year increase of 135% and a quarter-on-quarter growth of 137%, indicating strong sales momentum.

Why Has Inclisiran, Priced at 10,000 Yuan per Injection, Gained Market Acceptance?

Comparison of Three Imported PCSK9 Inhibitors, Compiled from Public Information

On one hand, owing to its unique mechanism, inclisiran differs from monoclonal antibody drugs such as evolocumab, alirocumab, and tafolecimab, which exert their effects by blocking the binding of PCSK9 to low-density lipoprotein receptors. As a small interfering RNA (siRNA) therapeutic, inclisiran directly reduces hepatic PCSK9 production through gene silencing, thereby achieving long-term lipid-lowering effects.

Its unique mechanism of action underpins its superior long-acting profile and favorable lipid-lowering efficacy. Patients require a booster injection three months after the initial dose, followed by only two injections per year thereafter, to achieve sustained and stable control of blood lipid levels. Whether used in combination with statins or as monotherapy in patients who are completely intolerant to statins, this medication effectively improves the rate of attainment of lipid targets and provides enhanced cardiovascular protection.

On the other hand, inclisiran also demonstrates favorable tolerability and safety, with adverse reactions during treatment being infrequent and predominantly mild or self-limiting.

Furthermore, Novartis has demonstrated remarkable acumen in its pricing strategy. Although the unit price of nearly RMB 10,000 is not low, it is quite competitive when considering that inclisiran is priced at over USD 3,000 abroad (equivalent to approximately RMB 25,000), reflecting Novartis’s sincere approach to pricing.

Although the cost of RMB 30,000 in the first year and RMB 20,000 annually thereafter remains unaffordable for most patients, this market benchmark has made it relatively easier for patients who cannot effectively control their lipid levels to target ranges with tolerated statin doses, those with familial hypercholesterolemia, and a small subset of patients with complete statin intolerance to access treatment with the other two PCSK9 inhibitors at an annual out-of-pocket cost of approximately RMB 2,000.

However, Novartis’s strategy has put domestic PCSK9 inhibitors from Innovent, Akeso, and Junshi Biosciences, which were launched subsequently, in a difficult position.

The three domestically produced PCSK9 inhibitors currently on the market, along with Hengrui’s product in the pre-approval stage, are highly likely to face the same commercialization challenges seen today.

Taking Innovent’s taletectmab, the first such drug to be launched on the market, as an example, although it was approved at nearly the same time as inclisiran, its unit price of RMB 1,388 and three dosing regimens (every 2, 4, or 6 weeks) result in an annual treatment cost ranging from approximately RMB 12,000 to RMB 36,000.

This pricing strategy suggests that Innovent is emulating the approaches of evolocumab and alirocumab: launching at a price point above RMB 1,000, securing inclusion in the National Reimbursement Drug List (NRDL) through national price negotiations, and subsequently trading price reductions for volume to expand market share. In the early commercialization phase, the company aims to differentiate itself from competitors by offering more flexible dosing regimens. At the time, products from Amgen and Sanofi offered limited dosing options, while Novartis’s product was priced as high as $3,000 abroad, placing it in an entirely different competitive segment.

Novartis’s self-imposed pricing strategy has placed its market position in a difficult spot: first, the price is stuck within its own mid-range tier; second, the twice-yearly dosing regimen offers greater competitiveness.

Furthermore, in terms of the scope of indications, drugs with a first-mover advantage are more competitive. Tafolecimab has been approved for the treatment of primary hypercholesterolemia and mixed dyslipidemia, whereas evolocumab and alirocumab have both been approved in China for indications related to reducing the risk of cardiovascular events. Evolocumab is also approved for the treatment of homozygous familial hypercholesterolemia in adults and adolescents aged 12 years and older.

Taletrectinib has been on the market for over a year, yet Innovent rarely mentions it in its financial reports, indirectly reflecting its sales performance. In August this year, the National Healthcare Security Administration released the preliminary review list for the 2024 National Reimbursement Drug List adjustment, which included the highly anticipated inclisiran sodium and taletrectinib.

Given the performance of inclisiran, Novartis is unlikely to have a strong willingness to significantly reduce prices for inclusion in the National Reimbursement Drug List (NRDL). Taletrectinib can leverage the window period during which two new domestically produced drugs are temporarily ineligible for national price negotiations, adopting a strategy of trading price for volume to expand its market presence.

For toripalimab, this is an opportunity to turn the tables.

The volume-expansion effect of national medical insurance inclusion is evident. After two imported PCSK9 inhibitors were included in the National Reimbursement Drug List, both ranked among the top 10 lipid-lowering drugs by sales in domestic tiered hospitals in 2023. This demonstrates that the “price-for-volume” market strategy is a viable commercial pathway in the chronic disease sector, characterized by its long growth trajectory and substantial profit potential.

For all domestically produced products, how to compete with foreign-funded products is a matter worth considering. Perhaps we can see the future changes in the track through the PCSK9 inhibitors under development.

In addition to the five marketed PCSK9 inhibitors, at least 20 other PCSK9-targeting drugs are in clinical trials; if these are merely “me-too” agents, their competitiveness will clearly be limited.

PCSK9 monoclonal antibody drugs have inherent limitations. For instance, the injectable route of administration results in lower patient compliance compared with oral formulations. Therefore, the development of long-acting agents and convenient oral medications has become a key focus for pharmaceutical companies in the next phase.

The high specificity, high potency, and long-acting properties of small nucleic acid drugs offer distinct advantages for chronic disease management. In addition to Novartis’s inclisiran, AstraZeneca’s AZD8233, an antisense oligonucleotide (ASO) targeting PCSK9, is also a small nucleic acid drug. In Phase 2b clinical trials, it reduced LDL-C levels by 73% in patients with hypercholesterolemia. Meanwhile, an oral formulation of this drug is also under investigation.

Some Investigational PCSK9 Drugs, Compiled from Publicly Available Information

Eli Lilly has taken a more aggressive approach by acquiring Verve’s PCSK9-targeted candidate therapies, VERVE-101 and VERVE-102. Among them, VERVE-101 is a single-base editor engineered based on the CRISPR system. It utilizes base editing technology to target the PCSK9 gene in the liver, permanently silencing PCSK9 expression to achieve an effect akin to “one-time treatment, lifelong lipid lowering.” Chinese companies such as Ribo Life Science, Darui Biotechnology, Jingyin Biotechnology, and Shengyin Biotechnology have also made strategic moves in this area.

In the realm of oral PCSK9 inhibitors, peptides and small-molecule drugs hold distinct advantages. For instance, Merck & Co.’s MK-0616 is a macrocyclic peptide compound capable of simultaneously disrupting the binding between low-density lipoprotein receptors and PCSK9 proteins, and it is currently in Phase 3 clinical trials. CVI-LM001, developed by China’s Synermore Biologics, is the world’s first oral small-molecule PCSK9 synthesis inhibitor to enter Phase 2 clinical studies.

The emergence of long-acting and oral PCSK9 inhibitors has addressed the limitations of PCSK9 monoclonal antibodies, while other avenues such as cell therapy, vaccines, and gene therapy represent future opportunities for iteration in this field. With three foreign-funded drugs and three already approved domestically produced PCSK9 drugs, along with subsequent products, future competition is bound to be intense. To stand out in this competitive landscape, it is essential to consider not only the efficacy of the drugs themselves but also the economic implications of lipid-lowering needs in China.