Lumenis M22 Goes Domestic: Will It Reshape China's Aesthetic Light-Based Device Market?

The trend of replacing imports with domestic products has also swept into the medical aesthetics sector.

In 2024, Lumenis’ M22 Platinum Blue IPL received NMPA approval for market launch and commenced domestic production in China in the second quarter. Additionally, Lumenis’ latest skin rejuvenation device, the Stellar M22, obtained import medical device registration in September 2024; this product is known as the eighth-generation M22.

As the originator of intense pulsed light (IPL) skin rejuvenation treatments, the M22 system has undergone multiple iterations and has consistently topped the rankings in major medical aesthetic institutions for many years, holding an absolute advantage in market share. Multinational companies such as Alma Lasers, Syneron Candela, and Jeisys also offer popular IPL devices that are widely favored by consumers in the medical aesthetics sector. (Note: IPL devices primarily refer to intense pulsed light therapy systems; some imported products integrate laser therapy, functioning as combined IPL and laser treatment devices.)

It is understood that the transition of the M22 from an imported product to a domestically manufactured one better aligns with the procurement policy requirements of public hospitals. In recent years, in addition to dermatology departments in general hospitals and specialized dermatology hospitals, some maternal and child health hospitals and primary healthcare institutions have also begun investing in intense pulsed light (IPL) skin rejuvenation projects, leading to a continuous rise in demand for related equipment.

Meanwhile,Domestic intense pulsed light (IPL) devices have developed rapidly over the past decade, with dozens of products approved for market entry. Some of these products have already established a certain industry reputation and achieved notable market scale. Will the localization of M22 production and the introduction of the latest-generation products into the Chinese market disrupt major domestic brands? Will the market dynamic, where the strong grow stronger, become further intensified? These are questions particularly worth considering for domestic companies, especially those that have received approval in recent years and are still working to establish their market presence.

Intense Pulsed Light (IPL) Therapy Device

In dermatology, intense pulsed light (IPL) devices are primarily used for the treatment of vascular disorders, pigmented lesions, hair removal, acne vulgaris, scars, and facial rejuvenation. Compared with other photoelectric aesthetic devices, IPL devices offer significant comprehensiveness in their applications.

In 1994, the first commercially available intense pulsed light (IPL) system was introduced in the United States and initially applied in the medical field; it was first introduced to the Chinese market in 1999.

With the development of China's medical aesthetics market, intense pulsed light (IPL) therapy, as an "all-rounder," has become a standard offering in nearly all medical aesthetic institutions. Photorejuvenation also enjoys high penetration and repeat purchase rates among consumers of medical aesthetic services.

According to the National Medical Products Administration (NMPA), as of September 2024, more than 10 imported intense pulsed light (IPL) therapeutic devices had been approved, including products from companies such as Lumenis, Alma Lasers, Syneron Candela, and Jeisys, primarily originating from the United States, Israel, and South Korea.

Approved Imported Intense Pulsed Light (IPL) Therapy Devices, Source: National Medical Products Administration

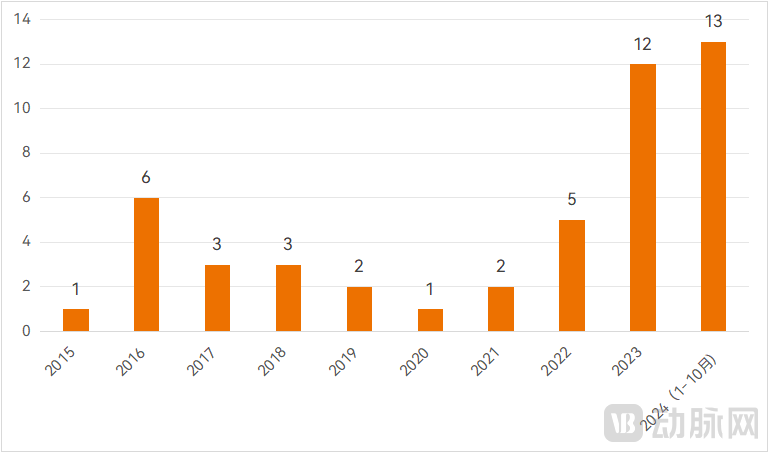

Meanwhile, domestically produced devices are catching up rapidly. Companies such as Chison Laser and Gisdi were among the earliest in China to develop intense pulsed light (IPL) therapy devices. As of October 10, 2024, more than 50 domestically manufactured IPL skin rejuvenation devices had received regulatory approval (excluding products where IPL is used solely for hair reduction, as well as home-use devices).Since 2024, 13 domestically produced intense pulsed light (IPL) therapy devices have been approved, marking the highest number in history.

In 2024, in addition to the Lumenis M22 transitioning from imported to domestically produced, products from several innovative enterprises received regulatory approval. For instance, Fumilei’s two intense pulsed light (IPL) therapy devices, Identical Flash and Gentle Flash, were approved consecutively; among them, Identical Flash, approved in July, was rapidly put into production after obtaining its manufacturing license. Baifu Laser’s IPL therapy device received approval, marking the starting point for the company’s expansion into the domestic market. Furthermore, Peninsula Medical’s second IPL therapy device was also recently approved.

Approval Status of Domestically Produced Intense Pulsed Light (IPL) Therapy Devices in the Past Decade, Source: National Medical Products Administration

Currently, the number of approved domestically produced intense pulsed light (IPL) treatment devices far exceeds that of imported ones; however, imported products still hold a larger market share than domestic ones, with the M22 maintaining a commanding lead in market share.

From the perspective of different types of medical institutions: Public medical institutions primarily rely on imported equipment, although the proportion of domestically produced devices is gradually increasing. According to bid award information from the China Government Procurement Network, companies such as Keying Laser, Chirpro Laser, Pumen Technology, Lifang Shengshi, Jinlaite, Guanzhou Technology, Gisdi, and Guang'an Laser have frequently appeared on the procurement lists of public medical institutions. In addition, large-scale medical aesthetic and plastic surgery hospitals mainly use imported products, while domestically produced equipment accounts for a relatively high proportion in small and medium-sized medical aesthetic institutions.

To assess the future technological and market directions of domestically produced products, it is essential to first identify the primary gaps between current domestic and imported equipment.

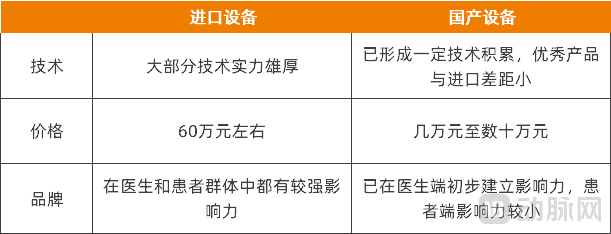

Overall Comparison Between Domestically Produced and Imported Intense Pulsed Light (IPL) Therapy Devices; Data Sources: Public Reports, VCBeat Interviews

The most fundamental dimensions for comparison are product technology and performance. “More than a decade ago, we indeed looked down on domestically produced equipment,” frankly stated Huang Xiangyu, Dean of Chongqing Haomei Xinyan Medical Aesthetics Outpatient Department, who previously served as a physician at a top-tier hospital and is now the founder of a medical aesthetics institution.The biggest problem with domestically produced equipment in the past was poor stability of output energy, which directly affected treatment efficacy.

Public information shows that domestic companies are continuously accumulating breakthroughs in the technical aspects of equipment stability.

Chirui Laser initially focused on distributing Sciton’s Profile laser and intense pulsed light (IPL) therapy systems, before gradually shifting its focus to independent research and development. Specifically, regarding IPL devices, Chirui Laser has accumulated over 20 years of technological expertise, implementing multiple upgrades and improvements to its products. These devices have demonstrated favorable therapeutic efficacy and consistent product quality stability during long-term clinical use. To date, Chirui Laser has launched two major product series: Queen and CC Light.

Among the components of intense pulsed light (IPL) therapy devices, the pulsed xenon lamp is the core component. The stability of the current supplied to the xenon lamp determines whether the pulse energy can be precisely replicated. The intensity and stability of the power output are also major technical challenges for IPL therapy devices.

Among emerging companies, Fumilei has developed a new generation of high-power constant-current xenon lamp power supplies, ensuring the intensity and stability of light output while avoiding significant pulse energy attenuation and peak light signals.

Meanwhile, domestically produced devices have also focused on improvements in independently adjustable parameters, filter configuration, and spot design to enhance the precision, refinement, and comfort of treatment.

Some Domestic Intense Pulsed Light (IPL) Therapy Devices, Source: Corporate Websites and Public Reports

Huang Xiangyu stated,With the continuous improvement of domestically produced medical devices in terms of stability and therapeutic efficacy, coupled with guidance from public hospital procurement policies, physicians’ willingness to adopt domestic products has significantly improved in recent years, including among doctors in public hospitals. “From the perspectives of therapeutic outcomes and patient comfort, high-quality domestic products no longer show significant differences compared to imported equipment.”

From a pricing perspective, imported products generally cost around RMB 600,000, whereas domestically produced products range from tens of thousands to several hundred thousand yuan, with mainstream models priced between approximately RMB 100,000 and RMB 300,000.Accordingly, the prices of core consumables for domestically produced equipment, such as handpieces and filters, as well as subsequent maintenance services, are also lower than those of imported products. Therefore,Domestically produced products generally offer a higher cost-performance ratio.

Furthermore, most imported devices have gained significant influence among physicians due to their superior performance; with continuous public education and marketing efforts by medical aesthetic institutions, internet-based medical aesthetic platforms, and social media platforms, these devices have also achieved widespread recognition among patients.

A cohort of domestic enterprises that were among the first to invest in the research and development of intense pulsed light (IPL) therapy devices has established a strong reputation among physicians through sustained technological accumulation and market expansion. However, there remains a significant gap between domestically produced and imported brands in terms of patient influence.

In short, domestically produced medical devices have made continuous progress in technical functionality in recent years and are gaining increasing market recognition.

Based on the above comparison, what should be the next steps for domestically produced equipment? How can they maximize their strengths and minimize their weaknesses?

The most fundamental aspect, of course, is to achieve continuous breakthroughs at the R&D and manufacturing levels, thereby meeting clinical needs with superior product performance.

“To this day, the M22 still represents the pinnacle of intense pulsed light (IPL) therapy devices,” candidly stated Xia Yuqing, founder of Fumilei. Although some voices in the market claim that their products have surpassed the M22 or even rendered its technology obsolete, there is currently no literature or data to support these assertions. “Domestic devices must first be pragmatic, letting actual equipment parameters, treatment cases, and evidence of safety and efficacy speak for themselves.”To match leading imported products, domestically produced devices still need to address issues such as optical waveform output, energy stability, and spot uniformity, while also prioritizing ease of use for physicians.”

Meanwhile, in Xia Yuqing’s view,Greater opportunities for domestically produced devices in the future still lie with small and medium-sized medical aesthetic institutions, particularly those founded by physicians.“Young doctors launching startups to establish ‘small yet beautiful’ clinics, adopting a physician-led decision-making model and relying on word-of-mouth for client acquisition, will become one of the trends in aesthetic medical services.”

In many medical aesthetic institutions, services are predominantly driven by “patient decision-making.” For most minimally invasive aesthetic procedures, including intense pulsed light (IPL) skin rejuvenation, patients play a decisive role in selecting treatment options; consequently, physicians have relatively limited decision-making authority in this process.

Internet-based medical aesthetics platforms and social media platforms have experienced rapid growth in recent years. These platforms, along with medical aesthetics institutions, have extensively educated patients on the technologies, materials, and functionalities of medical aesthetic devices, while also conducting related marketing campaigns. On internet platforms, medical aesthetics institutions are typically required to list the brand and model of the equipment used for each displayed treatment item, and even specify the operating mode and number of shots corresponding to a given price point. For injectable treatments, the brand must be indicated, along with the dosage or quantity administered at the corresponding price level.

This has played a significant role in promoting the standardization and transparency of the medical aesthetics services market, enabling patients to access intuitive information about treatment procedures. However, a consequent issue is that most patients possess only a superficial understanding of products and technical principles. Influenced by a plethora of complex marketing messages, they are prone to self-diagnosis and directly selecting specific treatments. Driven by sales targets, consultants at medical aesthetics institutions can significantly influence patient decisions, thereby undermining physicians’ decision-making authority. As a result, user choices guided by equipment or material brands may not necessarily correspond to treatments that are appropriately indicated for their conditions.

Xia Yuqing believes that,In the physician-led decision-making model, greater emphasis is placed on outcome delivery and the equipment efficacy required to achieve expected results, as well as on clinical case evidence for the devices, while brand preference plays a lesser role.

Huang Xiangyu also stated that while the equipment itself is certainly important, what matters more is how physicians utilize it.“Take intense pulsed light (IPL) skin rejuvenation as an example: devices from each brand are equipped with multiple filters. It is not the case that money is well spent only when all filters are used in a so-called ‘full-mode’ treatment; rather, the most appropriate device and treatment protocol should be selected based on the patient’s specific skin concerns.”

So, why must domestically produced equipment target small and medium-sized medical aesthetic institutions founded by physicians as an entry point in order to foster the formation of physician-led decision-making models?

This involves another broader context: in large medical aesthetic institutions, intense pulsed light (IPL) skin rejuvenation often serves as a customer acquisition tool. These institutions attract consumers with low prices and then pursue upselling, particularly leveraging the brand influence of imported devices to draw in customers at competitive price points.

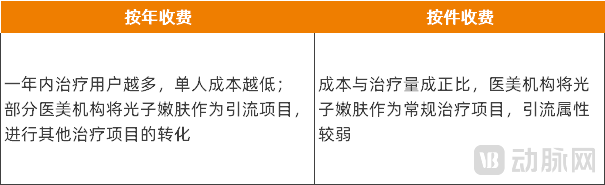

The treatment handpiece equipped with a pulsed xenon lamp (i.e., the component of the device that contacts the treatment area) is a high-value consumable accessory for intense pulsed light (IPL) therapy devices. The pulsed xenon lamp typically has a service life of 100,000 flashes (note: this refers to a total of 100,000 flashes; a single treatment session usually requires approximately 100–200 flashes). After this point, energy output begins to attenuate, necessitating replacement of the handpiece to ensure therapeutic efficacy. The price of an imported device’s handpiece is approximately RMB 100,000. Some manufacturers have introduced an annual subscription model for handpieces. Under this model, the more patients treated by a medical institution within a year, the lower the per-patient cost becomes, allowing it to be used as a low-priced customer acquisition offering. For large medical aesthetic institutions, which offer a wide range of other treatment services, there is greater potential for conversion following initial customer acquisition.

Fee Structure for Handpiece Replacement of Intense Pulsed Light (IPL) Therapy Devices

For small and medium-sized medical aesthetic institutions, the annual volume of patients undergoing intense pulsed light (IPL) skin rejuvenation treatments is limited, making an annual subscription model impractical. Even if such a model is adopted to attract a large user base with low pricing, the potential for conversion remains constrained due to the institutions’ limited scale, ultimately adversely affecting overall business operations.

Thus,Small and medium-sized medical aesthetic institutions will prioritize the therapeutic efficacy of intense pulsed light (IPL) skin rejuvenation treatments over their customer-acquisition potential; therefore, a product’s strong influence among end users is not a primary criterion for these institutions when procuring equipment.

As a core distributor for Pumen Technology’s medical aesthetics product line, Zheng Xiangqiang, General Manager of Baifumei Medical Technology, told VCBeat that most small and medium-sized medical aesthetic institutions are highly cautious about fixed investments in equipment. Adding new services or purchasing new devices requires careful consideration. Their primary concern is whether new projects funded by limited resources can be successfully launched, and how well patients will accept them, given the intense market competition and declining profitability across the industry. “Even equipment costing over 100,000 yuan represents a significant sum for them. When planning equipment purchases, they often worry about low patient volume and the failure to establish the new service.”

From this perspective, what medical aesthetic institutions need is not just equipment, but also comprehensive support. Zheng Xiangqiang stated that entry barriers could be lowered in the early stages by collaborating with these institutions on projects through a “guided sales” model. During this process, operational assistance would be provided to the institutions. Once the projects are running smoothly, the institutions would then proceed with the purchase, with early-stage operational revenue offsetting the equipment costs.

Huang Xiangyu believes that, in light of national policies, more medical aesthetic devices may shift from imports to domestic production in the future.Among these device categories, with the exception of intense pulsed light (IPL), high-quality domestic products and companies have emerged in the fields of Q-switched lasers, carbon dioxide (CO2) lasers, and gold microneedling. Domestic ultrasonic lifting devices have also risen to prominence unexpectedly. As long as domestically produced equipment offers high quality, it can gain market acceptance even at higher price points. This enables companies to invest more funds into research and development, thereby establishing a virtuous cycle for the industry as a whole.”

From his perspective, when viewed from the standpoint of clinical use, products from different brands within the same treatment category each possess unique characteristics and functional emphases, making it difficult to claim that one device can completely replace another. “In practice, we may even employ two devices from different brands for a single treatment modality, targeting specific skin concerns to achieve complementary advantages.”

Overall, domestically produced medical aesthetic devices need to continuously achieve breakthroughs in underlying technologies within their respective fields and establish differentiated therapeutic functionalities; meanwhile, they must also help physicians and medical aesthetic institutions further enhance treatment efficacy.In the future, rather than merely achieving domestic substitution for medical aesthetic devices, the focus should be on cultivating core competitiveness through technological and service-based competition with imported products.

Special thanks to Huang Xiangyu, Director of Chongqing Haomei Xinyan Medical Aesthetics Clinic; Xia Yuqing, Founder of Fumailai; and Zheng Xiangqiang, General Manager of Baifumei Medical Technology, for their strong support of this article.