Generative AI Breakthrough: Medical AI at a New Crossroads – Prospectus Submission

2024: A Year of Both Turbulence and Rebirth for Medical AI

Rapidly advancing large language models, powered by generative AI, are sweeping through the healthcare sector. Previous domains such as internet-based healthcare, medical imaging, and new drug development are being reshaped by the new generation of AI, unlocking unprecedented value.

However, recognizing value does not guarantee capturing it. Amid the current bleak financing landscape, companies dedicated to large language models (LLMs) can no longer afford the trial-and-error approach that was common in the deep learning era. Constrained cash flows necessitate that every enterprise thoroughly evaluate all aspects—including application scenarios, technology, risk control, and commercialization—before making decisions.

Therefore, this year’s AI report focuses on “scenarios” and “products,” aiming to provide reference recommendations for AI companies’ next steps in strategic layout, product selection, R&D, and commercialization by examining the supply-and-demand dynamics among hospitals, pharmaceutical companies, and medical device manufacturers, and analyzing real-world case studies from industry pioneers.

Deconstructing the Configuration Requirements for Medical AI: Primarily Driven by Policy and Efficiency Enhancement

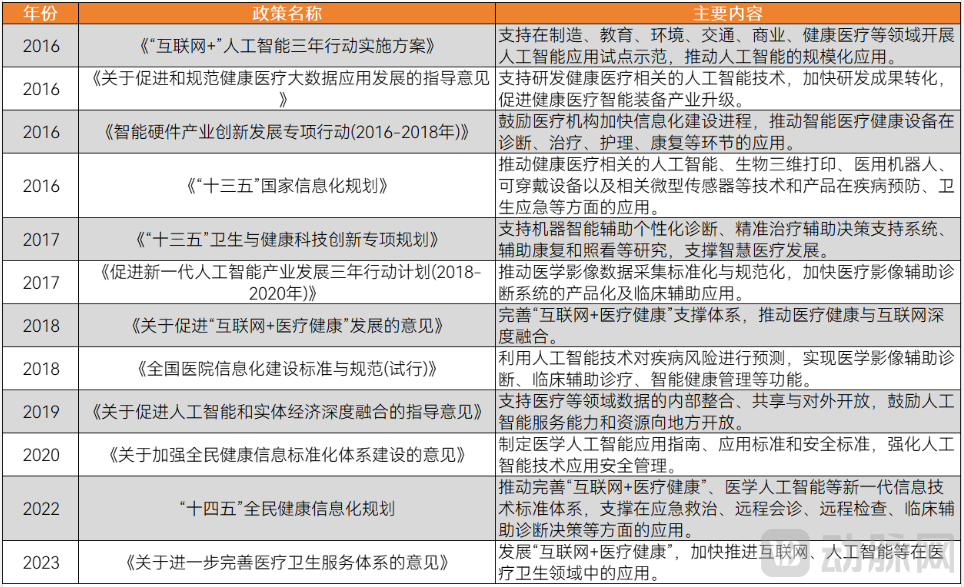

In the early stages of AI development, policy-driven initiatives played a dominant role in the implementation of medical AI. Policymakers typically formulate forward-looking and guiding policy documents based on the current state and future trends of the healthcare sector. These policy documents not only define the overall objectives and phased tasks for healthcare informatization construction but also specify key elements such as construction content, technical requirements, and implementation pathways. Therefore, for public hospitals, policy compliance is the primary consideration.

To foster a correct understanding of cutting-edge technologies among hospitals and guide the rapid development of related industries, China has been introducing policies centered on artificial intelligence (AI) since 2016. From a macro perspective, these initiatives aim to promote the application of AI in healthcare, enhance the efficiency and quality of medical services, and ultimately achieve intelligent transformation within the healthcare sector.

Core Macro Policies Driving the Development of Medical AI (Source: VCBeat)

For scenarios outside hospitals, certain sectors also require strategic early alignment with policy directions. Taking biopharmaceuticals as an example, following the “722” incident, the NMPA (then the CFDA) successively issued documents such as the Announcement on Launching Self-Inspection and Verification of Drug Clinical Trial Data and the Announcement on Adjusting the Review and Approval Process for Drug Clinical Trials. These initiatives spurred prosperity in China’s EDC and RTSM markets, enabling companies like Taimei Medical Technology to embed AI into their systems, thereby positioning themselves as key enablers of pharmaceutical enterprises’ digital transformation.

Today, the FDA encourages pharmaceutical companies to adopt Digital Health Technologies (DHTs) in clinical trial sponsorship, indirectly guiding their further transformation. Taking eCOA as an example, approximately 80% of clinical studies in the United States are conducted using eCOA, with 60% in Europe following this approach, whereas fewer than 5% of sponsors in China have adopted eCOA. As expanding into European and American markets becomes an inevitable trend, FDA policies will increasingly influence Chinese pharmaceutical companies. Currently, companies such as Medidata and Veeva have integrated AI into their digital transformation solutions, preparing to meet the new demands arising from these overseas policy changes.

Unlike AI demand driven by policy, early-stage AI demand focused on efficiency improvement lacks guidance or a predefined form. It requires enterprises to independently identify genuine pain points within hospitals’ clinical, operational, and management processes, ensuring that AI-driven solutions deliver tangible benefits to the hospitals.

Among numerous scenarios, AI in medical imaging is the earliest and most intuitive example. As one of the most widely applied areas of AI, such technology assists physicians in managing high-intensity, repetitive image interpretation tasks, thereby enhancing both the quality and efficiency of radiology departments.

As AI continues to advance and gains greater acceptance among physicians, many doctors and healthcare administrators are proactively approaching AI companies with specific requirements, requesting the development of AI solutions tailored to enhance quality and efficiency.

For example. Following the introduction of Diagnosis-Related Groups (DRGs), hospitals’ profit logic shifted from scale expansion to cost control. Administrators began to place greater emphasis on refined and scientific internal management, aiming to improve operational efficiency and the quality of medical services. At this juncture, traditional healthcare IT systems could not meet the various demands posed by refined hospital management, prompting hospital administrators to turn to AI systems for support, thereby driving AI procurement primarily motivated by efficiency enhancement.

There are many such scenarios, particularly as healthcare institutions gradually meet the baseline requirements set by policies and begin to proactively seek intelligent upgrades to enhance their competitiveness. In the absence of new policy initiatives, the drive for AI adoption led by efficiency gains will gradually replace policy-driven adoption, shaping the future development trajectory of medical AI.

Driven by the dual forces of policy support and efficiency enhancement, China has fostered a large cohort of medical artificial intelligence products that have been integrated into the vast majority of healthcare scenarios.

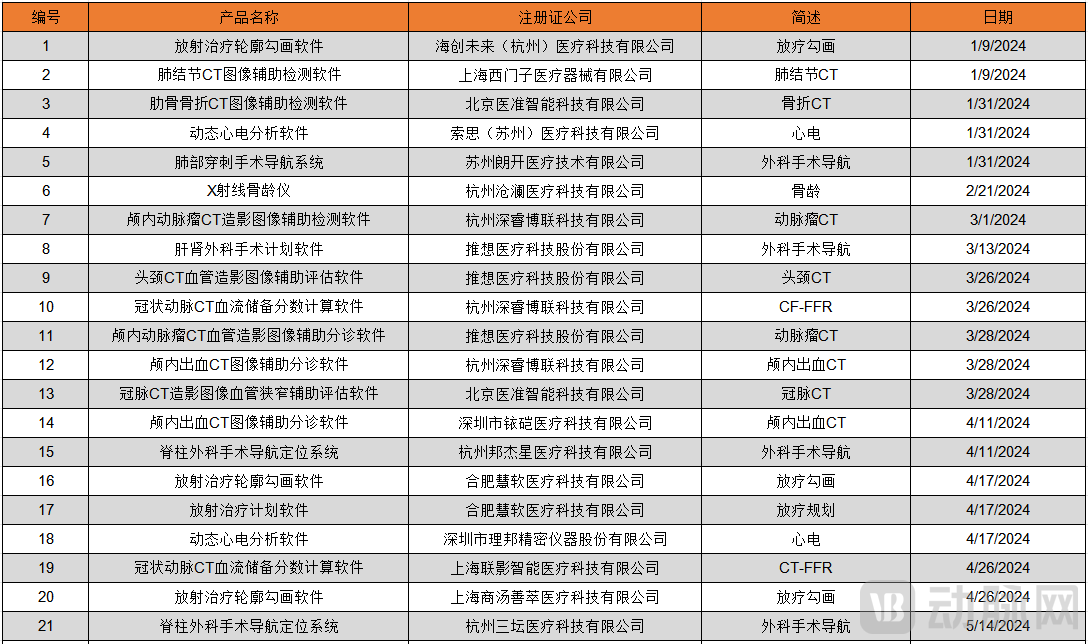

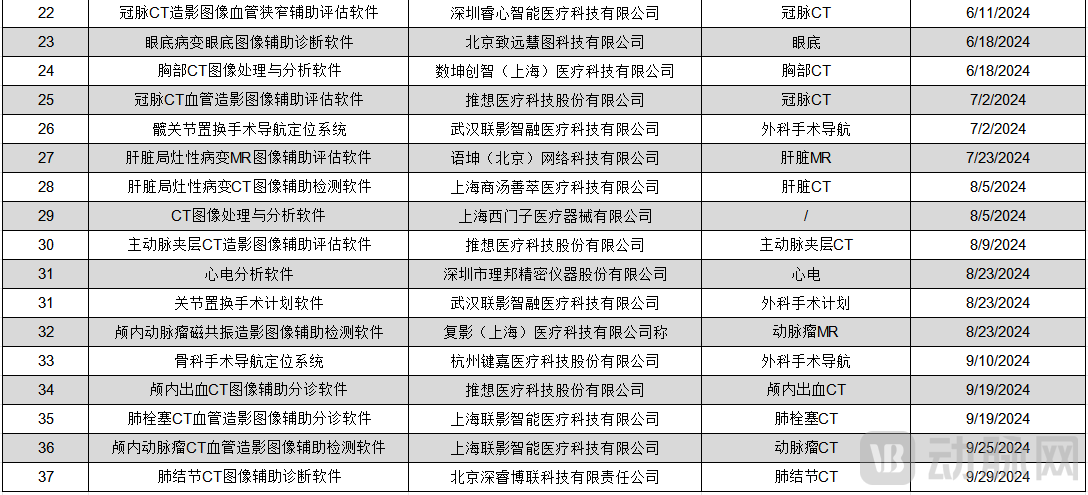

Let’s start with medical imaging. VCBeat Research Institute conducted a comprehensive review of 64 companies, including AI startups with financing records and publicly listed companies that have announced product lines, surveying a total of 436 products covering nearly all organs.

AI applications for many high-demand organs have reached a high level of maturity, enabling high-precision, multi-disease assisted diagnosis in areas such as the heart (70 conditions), bones (58 conditions), head and neck (53 conditions), and lungs (44 conditions). AI solutions for less commonly targeted organs are also under development, including the intestines (5 conditions), urinary system (4 conditions), and the entire abdomen (2 conditions). Some of these products have already obtained medical device registration certificates, allowing for a certain degree of commercialization.

Medical AI Products Granted Class III Medical Device Registration Approval from January to September 2024 (Source: Official Website of the National Medical Products Administration)

In terms of disease categories, cardiovascular and cerebrovascular diseases, bone and joint disorders, pulmonary nodules, tumors (radiotherapy), and fundus conditions are currently the most prominent, with more than 15 similar products available on the market. In contrast, fewer companies are focusing on intestinal polyps and urological-related diseases, making these niche segments relatively less popular.

The reasons behind the situation can be summarized in three points:

1. As the difficulty of obtaining standardized medical data decreases, market demand is fully driving the R&D direction of imaging AI. Lung cancer ranks first in both incidence and mortality among malignant tumors in China, with approximately 650,000 patients dying from lung cancer each year. Therefore, the strong demand within the healthcare system for cardiovascular AI and lung cancer AI is driving enterprises to conduct R&D focused on these corresponding diseases.

2. Organ-centric diagnosis has replaced disease-specific diagnosis, driving companies to adopt comprehensive strategies based on organs. In the past, the research and development and implementation of imaging AI often revolved around a specific disease. However, radiologists do not preconceive a patient’s condition when interpreting CT scans or X-rays; instead, they meticulously examine every detail in the images. This auxiliary approach limited the value of imaging AI. Today, to achieve diagnostic capabilities for a specific organ, imaging AI companies must address each prevalent disease associated with that organ individually, leading to a surge in the number of imaging AI solutions targeting these common conditions.

3. Niche disease areas, though independent, still hold potential. Fields such as pathology and electrocardiography (ECG) also face challenges of high workloads and scarce medical resources, making them prime scenarios for the deployment of medical AI. However, since these areas do not fall under medical imaging, mainstream AI companies have rarely ventured into them. Furthermore, many products in these fields require only Class II medical device certification for commercialization, resulting in relatively mild competition. Nevertheless, an increasing number of AI solutions are now obtaining Class III medical device certification. By deeply empowering these niche segments with AI, the application logic within these scenarios may be transformed in the future.

Next is medical IT. Ratings remain the primary driver for hospitals to adopt AI. Achieving an Electronic Medical Record (EMR) rating of Level 5 or higher requires hospitals to implement intelligent deployment on top of their digital infrastructure, which means they must introduce AI tools and integrate them deeply into their existing information systems.

In August 2023, Fuwai Hospital of the Chinese Academy of Medical Sciences became the first hospital in China to achieve Level 8 in the Electronic Medical Record (EMR) rating system, breaking through the previous ceiling of healthcare informatization development in the country. As of that time, a total of 312 hospitals across China had received high-level EMR ratings, including one hospital at Level 8, three at Level 7, 40 at Level 6, and 268 at Level 5.

Basic Requirements for the Graded Evaluation of Overall Application Level of Electronic Medical Record (EMR) Systems (Source: Compiled from Public Information))

More hospitals will “sprint” toward higher-level ratings for electronic medical records (EMRs) in the future. In particular, achieving Level 5—the entry point for advanced-tier certification—remains highly challenging. Over the coming years, it will become mainstream for tertiary hospitals to strive for Level 5 and aim for Level 6. This trend will create significant opportunities for artificial intelligence.

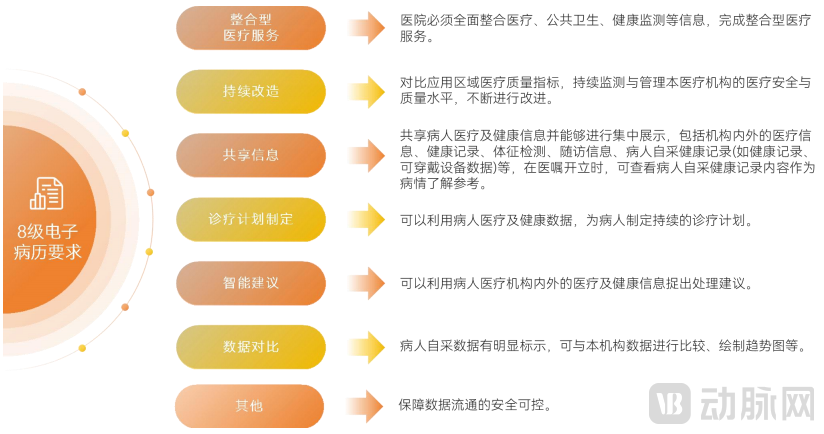

Conditions to Be Met for Level 8 Electronic Medical Records (Source: Compiled from Public Information))

Finally, let us discuss AI in pharmaceuticals. Since 2020, when AI-driven pharmaceutical ventures experienced explosive growth in the primary market, numerous startups have advanced their pipelines into clinical stages. Previously, the number of innovative drug projects led by AI that entered clinical trials was only in the single digits. This figure rapidly grew to over 100 in 2021, maintained its upward momentum to surpass 200 in 2022, and continued to rise in 2023, with the number of pipelines crossing the 300 mark.

Amid this trend, multinational corporations (MNCs) such as AstraZeneca, Bayer, Roche, Eli Lilly, and Sanofi have successively entered the field of AI-driven drug discovery. Meanwhile, leading Chinese pharmaceutical companies, including Hengrui Medicine and CSPC Pharmaceutical Group, are actively deploying AI strategies through strategic partnerships and equity investments, seeking to leverage innovative technologies to uncover new pathways for drug research and development.

However, the pace of AI development in the pharmaceutical industry slowed significantly in 2024.

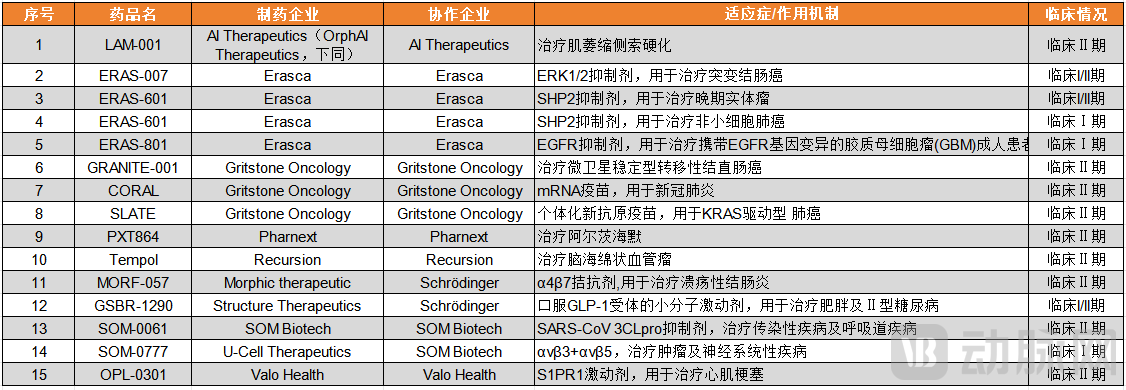

VCBeat Research Institute conducted a survey of the pipelines of 39 mainstream AI-driven pharmaceutical companies. As of October 31, 2023, these companies had a total of 95 pipelines in clinical trials. By September 1, 2024, only five pipelines had updated their latest clinical status and advanced to new stages.

Updated the clinical pipeline from October 31, 2023 to September 1, 2024

(Source: VCBeat, VBInsight)

Among the remaining pipeline assets, a total of 15 pipelines/indications have been removed from company websites or announced as discontinued. Of these, 3 were in Phase I clinical trials (accounting for 20%), 9 were in Phase II clinical trials (accounting for 60%), and 3 were in Phase I/II clinical trials (accounting for 20%).

39 Mainstream AI Pharmaceutical Companies Have Discontinued or Withdrawn Their Pipelines

39 Mainstream AI Pharmaceutical Companies Have Discontinued or Withdrawn Their Pipelines

(Source: VCBeat, VBInsight)

Meanwhile, the aforementioned companies added 16 new pipelines/indications, equaling the number of pipelines that were discontinued or withdrawn. Nearly half of these pipelines originated from AI-driven drug discovery companies with Chinese ownership, with Insilico Medicine, Eiger BioPharmaceuticals, Iceberg Biosciences, and DTI Pharma (held by XtalPi) accounting for seven of the spots.

39 Leading AI Pharmaceutical Companies Add New Pipelines/Indications

39 Leading AI Pharmaceutical Companies Add New Pipelines/Indications

(Source: VCBeat, VBInsight)

Yet, on a global scale, AI-driven drug discovery remains vibrant. Notably, NVIDIA has emerged as a key catalyst for the sector’s resurgence, making frequent and aggressive investments over the past two years. According to data from PitchBook, Crunchbase, and VBInsight, NVIDIA participated in more than 70 investment deals in 2023 and 2024 (as of September 5, 2024). All of these investments were exclusively AI-related, including stakes in at least 14 AI drug discovery companies and 8 firms in other healthcare sectors.

AI Drug Discovery Companies Invested in by NVIDIA (2023–August 2024)

(Source: Pitchbook, Crunchbase, VBInsight)

Furthermore, collaboration deals between multinational corporations (MNCs) and AI-driven drug discovery companies or other AI-enabled pharmaceutical enterprises have seen significant growth in the past two years. According to J.P. Morgan data, the share of upfront payments in biopharmaceutical transactions has been on a downward trend since 2020, with the upfront payment ratio dropping to just 6% in the first half of 2024. Given the high-risk, capital-intensive nature of drug development, smaller upfront payments undoubtedly reduce the economic risks associated with these transactions, reflecting MNCs’ increasingly cautious approach to business development (BD) deals. In this context, the greater allocation of MNC capital toward the AI healthcare sector serves as a “vote with their feet,” affirming the value of AI-powered drug discovery.

Just as deep learning once surged in popularity, emerging large language models are rapidly sweeping through the healthcare industry at a visibly accelerated pace. In less than two years, the number of healthcare-specific vertical models on the market has exceeded one hundred, with many leading hospitals proactively deploying related platforms and spontaneously embarking on explorations into the next generation of artificial intelligence.

However, for tech-driven healthcare to gain a firm foothold in the medical field, it requires not only substantial technological innovation but also products that are highly adapted to specific clinical scenarios and seamlessly integrated into existing healthcare workflows. In other words, the trial and refinement of large language models have only just begun.

Driven by capital support and market demand, large medical models have developed rapidly. In less than two years, the number of specialized vertical medical models released on the market has exceeded 100. According to incomplete statistics from VCBeat, 39 newly released large medical models were collected as of September 10, 2024.

According to the nine major application domains for large models classified in VCBeat’s “2023 Medical Artificial Intelligence Report,” nearly 30% of large models are applicable to scenarios spanning two or more categories. Among these, “clinical decision support,” “quality control,” and “patient services” remain the most concentrated subfields for large model deployment, followed by “traditional Chinese medicine” and “new drug R&D.” In contrast, large models in the fields of “scientific research” and “treatment plan generation” are relatively scarce, and no new large models have been released for “public health” applications to date.

Although the number of applications has reached a significant scale, the scenarios involved remain fragmented and unsystematic, with insufficient depth. Consequently, the total addressable market that enterprises can reach through these applications is limited, which is not yet sufficient to demonstrate that large language models have achieved viable commercialization. Therefore, to drive large-scale commercial adoption of large models, enterprises must still address the following challenges.

I. Infrastructure Development Issues. At present, the vast majority of hospitals that have successfully implemented large language models are top-tier Grade A tertiary hospitals, which possess the financial resources and conditions necessary for deployment. In contrast, lower-ranked hospitals and even primary healthcare institutions remain significantly distant from adopting such technologies.

Currently, the existing resource infrastructure in most hospitals is primarily oriented toward general-purpose computing using CPUs, with very few hospitals possessing GPU resources dedicated to graphics processing and parallel computing. Due to the lack of deployment environments for large language models (LLMs), hospitals need to procure GPUs alongside their applications to operate LLM-based solutions, while also ensuring sufficient storage capacity and high-speed network connectivity to guarantee the stable operation of these models.

For most hospitals, this represents a significant cost. Based on an estimate of one RTX 4090 GPU per general department, equipping a hospital campus with the necessary computing power would require an investment in the millions of yuan for chip configuration. Although leading hospitals have shown great enthusiasm for deploying large language models and are willing to pursue on-premises deployment, many other hospitals remain deterred by the substantial expense.

II. Data Integration Challenges. Due to the complexity of hospital information systems, which involve numerous platforms and vendors, integrating data across the entire patient lifecycle presents significant challenges. For many medical large language model (LLM) companies, it is imperative to further enhance the models’ capabilities in processing multimodal data.

In an ideal scenario, multimodal large language models should not merely classify various types of medical data; they should also extract key insights from each modality and provide comprehensive recommendations.

III. Limitations in ApplicationCurrently, intelligent applications built on large language models (LLMs) have not transcended the scope of traditional healthcare IT applications. They resemble an enhanced version of internet-based healthcare services—valuable, yet not irreplaceable. In the future, enterprises need to develop “killer apps” tailored to hospital needs, thereby stimulating hospitals’ demand for LLM adoption and ultimately achieving large-scale implementation of these models.

The above is an excerpt from the main content of the report. Scan the QR code to download the full report for free.

Table of Contents

Chapter 1: What Constitutes the Driving Forces Behind the Deployment of Medical AI?

1.1 Policy-Driven Momentum for AI Procurement

1.2 AI Procurement Driven by Efficiency Enhancement

1.3 Attitudes of Certain Stakeholders Toward the Procurement of Medical AI

Chapter 2: Self-Transcendence and the Metamorphosis of Medical AI

2.1 Medical Imaging AI: Broadening Horizons, Imaging AI Moves Beyond the Radiology Department

2.2 Informatics AI: Once Passive Administrators, Now Proactively Embracing Healthcare IT

2.3 AI in Pharma: Seeking New Opportunities Amid Change During the Downturn

2.4 Discussion: Can a Large-Scale AI Product Portfolio Solve the Commercialization Challenge?

Chapter 3: Financing Winter, Medical AI Strives to Improve Cash Flow

3.1 Overall Decline in Primary Market Financing, with AI in Pharmaceuticals Showing Relative Strength

3.2 AI Companies Generally See Narrowing Losses, with Cost Reduction and Revenue Generation Becoming Core to Their Operations

3.3 Discussion: How Artificial Intelligence Can Save Itself Amidst a Market Downturn

Chapter 4: How Generative AI Disrupts Healthcare in the Era of Large Language Models

4.1 Cutting-Edge Technologies: From Discriminative AI to Generative AI

4.2 Discussion: How Many More Steps Must Large Models Take Toward Large-Scale Commercialization?

Chapter 5: Benchmark Cases of Medical Artificial Intelligence

5.1 Deepwise Medical: Self-developed Multimodal AI Engine Empowers Hospital Data Asset Management through Digital Intelligence

5.2 Yidu Tech: “Dual Middle-Platform” Strategy Drives Comprehensive Product Upgrades, Significantly Boosting Profitability

5.3 EgerMed: “In-House Pipeline + AI Services” Dual-Engine Strategy, Leading AI Drug Discovery in China

5.4 Bosh Medical: Leading the Domestic Market with Dual Product Lines in AI-MDT Radiotherapy and Surgery