Frenzied Price Wars Are Not the Way Forward for China's Dental Industry

As the “extreme price war” in the oral care industry raged from the beginning of the year to nearly its end, industry chaos has begun to emerge.

Recently, the Shanghai 12345 Citizen Service Hotline received a large number of complaints regarding numerous Shanghai residents being frequently subjected to unsolicited calls for months on end from individuals claiming to represent certain dental implant clinics offering low-cost implants, which has disrupted their daily lives. Despite media coverage, such telemarketing harassment continues unabated.

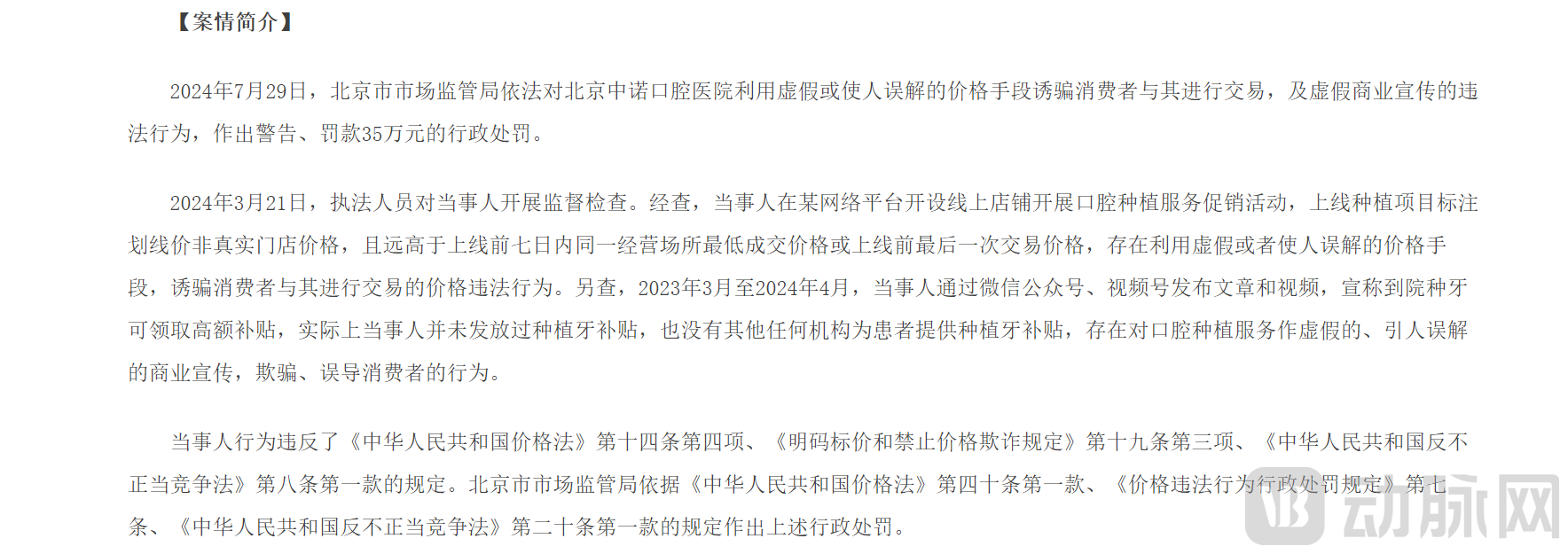

This is not an isolated case. In September this year, the Beijing Municipal Administration for Market Regulation released findings from its “Iron Fist” campaign, revealing that a dental hospital in Beijing had engaged in false advertising for dental implant services online and used deceptive or misleading pricing to lure consumers. Meanwhile, some institutions are not content with merely profiting from a single tooth: according to a report by China National Radio’s Voice of China, unscrupulous providers have been extracting not only diseased teeth but also healthy ones, even coaxing patients into having healthy teeth removed under the pretext that more extractions enable more implants.

▲Image source: Beijing Municipal Administration for Market Regulation

“Low-price baiting and high-price harvesting: These cutthroat competitive practices disrupt the normal order of the industry.“Cai Jing (a pseudonym, at the interviewee’s request), a partner at a dental chain in Shanghai, told VCBeat, ‘This has had a negative impact on the healthy development of the entire dental industry ecosystem and has accelerated industry volatility.’”

Under immense pressure, 2024 witnessed frequent news reports of dental clinics being transferred or shutting down and absconding, as the industry began to undergo a rigorous shakeout. According to data from Haodeya DataLab, the net increase in the number of dental medical service institutions across China in the first half of 2024 was 5,059, representing a year-on-year decline of 32.53%, with the total number of deregistrations and revocations amounting to 2,401.

Constrained by the broader macroeconomic environment, intensifying competition within the dental industry has become inevitable. However, in recent research and interviews conducted by VCBeat, professionals with years of experience in the dental sector generally agree that a relentless race to the bottom on price is not a sustainable path forward for the industry.

“1-Yuan Group-Buy Dental Implants” Ultra-Low-Price Promotions Are Unfolding in the Dental Industry.

Behind this, on the one hand, is the widespread competition among numerous institutions to safeguard their performance following the full implementation of China’s centralized volume-based procurement policy for dental implants; on the other hand, amid the broader macroeconomic environment, competition for patient acquisition within the industry has intensified.

It has been observed that, compared with 2021, many dental institutions experienced a significant decline in revenue during this year, with no small number reporting drops of up to 30%. In terms of gross profit margin, dental institutions generally maintained around 40% in previous years, while some leading players reached approximately 50%. Currently, it is considered favorable for dental institutions to maintain a gross profit margin of 25%–35%, reflecting a marked decline.

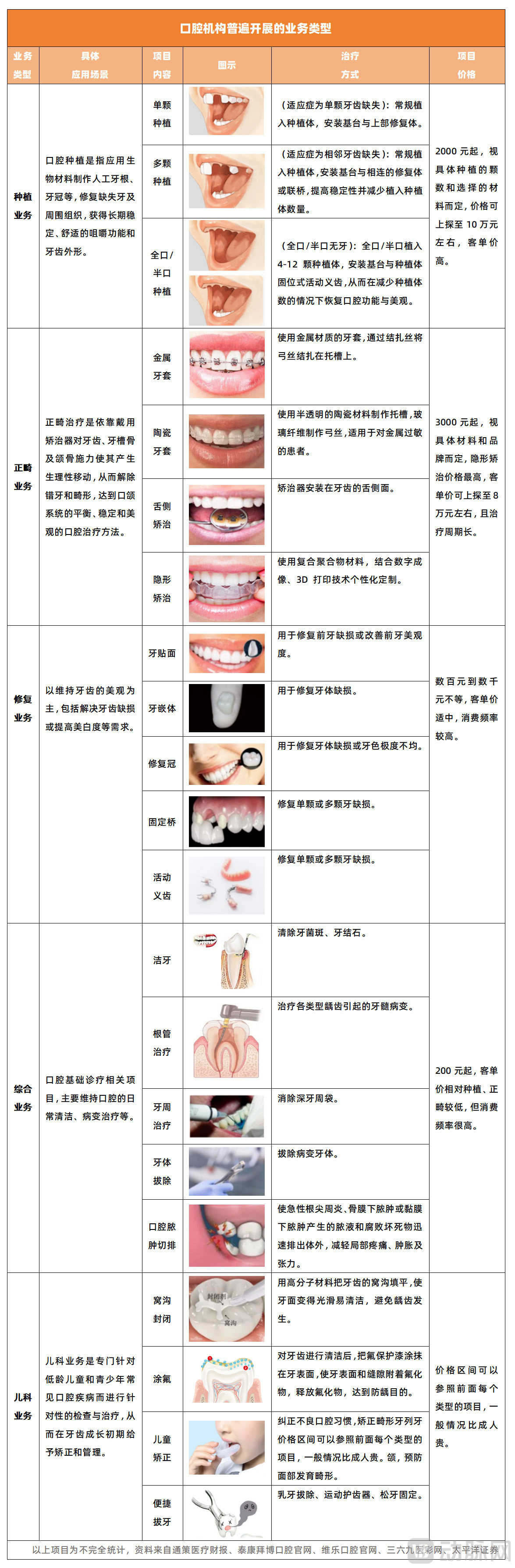

Declines in revenue and profit are, in fact, linked to the historical revenue structure of dental institutions. Within the industry, the business revenue of dental institutions primarily comprises dental implant services, orthodontic services, prosthodontic services, general dental services, and pediatric dentistry services.Dental implant and orthodontic services, characterized by their high average transaction value, are the two most profitable business lines in terms of overall institutional revenue. This is particularly true for dental implant services.

▲ Graphic by VCBeat

Precisely because of their past overreliance on a single business line, many dental institutions have struggled to sustain high labor costs and operational expenses amid volume-based procurement and price wars, making their operations increasingly difficult.

“Some institutions have adopted an assembly-line approach to dental implant procedures, drastically deviating from the medical essence of implant dentistry in order to capture the vast majority of new consumers who are highly price-sensitive and lack medical knowledge. In the long run, the ‘Pinduoduo model’ emerging in the oral implant market will have a greater impact than the centralized procurement policy,” said Lv Jianming, founder of Topchoice Medical, at the company’s annual general meeting of shareholders held in late June this year.

Cai Jing, a partner at the aforementioned dental chain, stated bluntly: “Unlike certain manufacturing sectors that can sustain reasonable profits by continuously lowering prices to expand market share, the dental industry requires institutions to provide comprehensive services ranging from diagnosis and treatment to long-term follow-up and health management once a patient relationship is established. From this perspective, the common misconception that dentistry is an ‘exorbitantly profitable industry’ stems primarily from overlooking the value of long-term medical services.”

In other words,Under an ultra-low-price strategy, the dental industry faces at least three major challenges:

· First, when institutions engage in aggressive price wars by setting prices far below the market average, their own profits are severely diluted, even leading to substantial losses; meanwhile, competitors experience a sharp decline in patient volume and revenue, plunging the industry into a vicious cycle.

· Second, due to low-price strategies, dentists’ commission-based income has declined. To maintain their previous income levels, some dentists may resort to unnecessary extractions and excessive treatments while reducing the quality of follow-up care, thereby undermining the long-term assurance of patients’ oral health.

· Third, due to the aforementioned negative impacts, patients will lose trust in dental institutions, making the cost of restoring doctor-patient relationships in the future market extremely high.

“Low prices certainly cannot be the sole option in the dental industry,” said Liu Chenyang, a partner at a financial advisory firm who has long focused on the dental sector. “Although we often describe dental medical services as consumer healthcare, highlighting the industry’s consumer-oriented nature, the essence of dental services remains medical care.”In healthcare, safety and efficacy must be prioritized.“With ultra-low prices, how can safety and efficacy be guaranteed?”

Therefore, the dental industry urgently needs to shift its mindset, moving away from relentless price wars and instead ensuring that quality matches price, thereby avoiding practices that compromise medical safety and efficacy or disregard patients’ long-term oral health.

Amid fierce competition, price wars in the dental industry are unlikely to abate in the short term. In response, dental institutions must take proactive measures and identify appropriate strategies to break through amidst industry volatility.

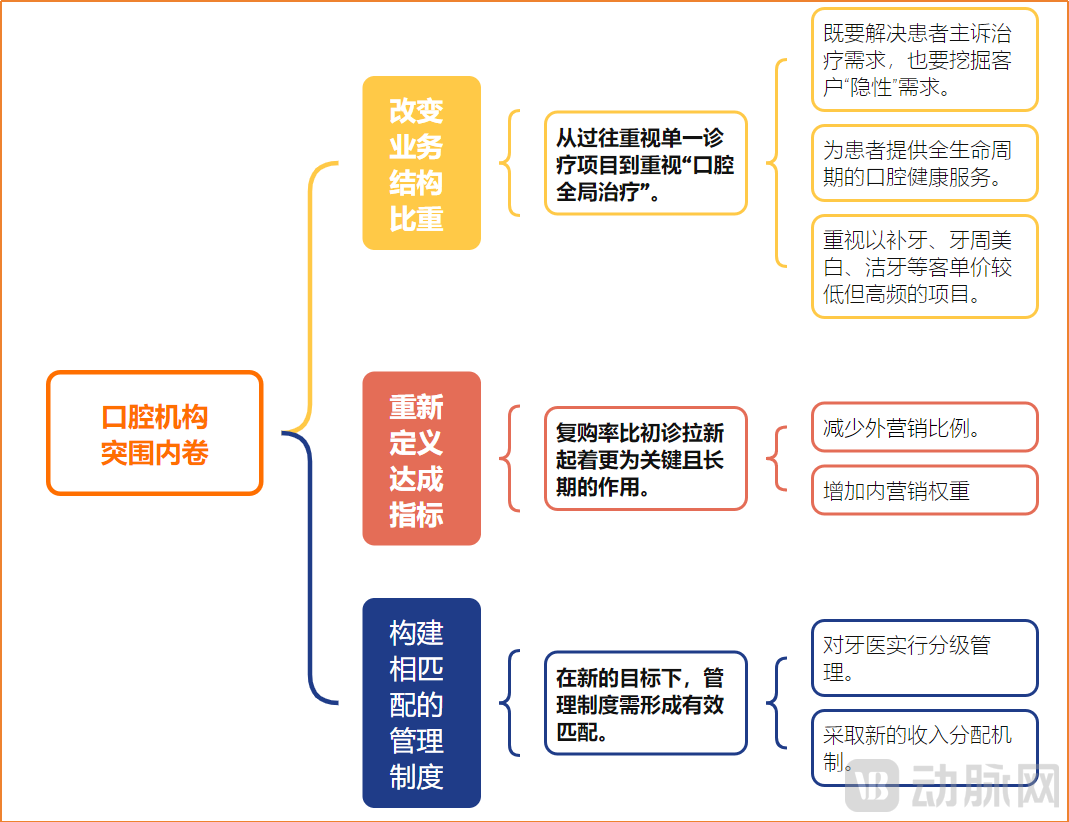

According to VCBeat’s research and insights,Currently, many leading institutions in the industry have largely reached two major consensuses: first, to transform their business structure by evolving from a past emphasis on single diagnostic and treatment procedures toward “comprehensive oral healthcare”; second, to deeply recognize that, in achieving performance targets, customer retention rates play a more critical and long-term role than acquiring new patients.

First, in terms of business structure, dental institutions need to strike a balance among the proportions of implantology, orthodontics, and preventive dental services. “Institutions must not only understand and meet patients’ primary treatment needs upon visiting but also uncover their ‘latent’ needs, thereby providing comprehensive oral health services throughout the patient’s lifecycle,” said Cai Jing, a partner at a dental chain organization. “For most dental patients, addressing oral health issues typically requires multiple visits. While one-off transactions may yield short-term gains, they come at the expense of repeat visits and referrals.”

To achieve this transformation, dental institutions need to realign their revenue distribution models by incorporating patient satisfaction as a key performance indicator linked to business targets.

Furthermore, making the improvement of repurchase rates a core business strategy to achieve key performance indicators is intrinsically linked to transforming the business structure. In the dental industry, it is common practice to acquire customers through heavy advertising; however, this approach fundamentally focuses on new customer acquisition, which necessitates continuous increases in marketing expenditures for dental institutions.

Regarding this issue,The industry has summarized two approaches: external marketing and internal marketing.External marketing refers to the common approach aimed at acquiring first-time patients, while internal marketing focuses on driving repeat purchases and patient referrals.

Methods for increasing the number of customers per transaction include external marketing and internal marketing. External marketing targets store visits, primarily aiming to increase the number of first-time patients who visit naturally (not through referrals). Internal marketing, on the other hand, focuses on conversion, repeat purchases, and referrals after customers arrive at the facility. Therefore, internal marketing increases the number of follow-up visits as well as the number of referred patients among first-time visitors.

It is important to note that the marginal profits of traditional high-ticket dental implant services, which are affected by centralized procurement, continue to decline (a trend that may also extend to orthodontics), significantly diminishing the returns on customer acquisition. In contrast, prioritizing low-cost but high-frequency services such as fillings, periodontal whitening, and dental cleaning will effectively improve the company’s revenue structure.

“Internal marketing often determines more than 60% of outpatient volume, while external marketing can only influence approximately 30%–40%.” This was observed by Liu Chenyang, a partner at FA, during his corporate research.

In addition to implementing the aforementioned measures, dental institutions must also adopt corresponding management systems.Professor Zhang Jincai, former Vice President of the Guangdong Medical Doctor Association and former President of its Stomatologists Branch, stated at an event: “In the current context of centralized procurement policies, it is particularly important to implement tiered management for dental implant surgeons. This not only determines which physicians are qualified to perform surgeries but also involves allocating procedures of varying complexity according to physicians’ levels and competencies. Surgeries that exceed a physician’s scope of competence must be conducted under the guidance of senior physicians to ensure treatment quality. Tiered management is not limited to the field of dental implants; rather, it is an essential component of overall surgical management in healthcare. The tiered management system serves both as a fundamental measure to ensure medical quality and as a guarantee for patients to receive high-quality medical services.”

In addition to implementing tiered management of physicians, dental institutions can diversify their product portfolios to adapt to market changes. Taking Topchoice Medical as an example, the company has adopted differentiated pricing for its dental implant services based on market segmentation, introducing a comprehensive “dental supermarket” concept spanning high-, mid-, and low-tier offerings: high-end implants are performed by renowned specialists using premium products; mid-range implants are carried out by young and middle-aged dentists using mid-to-high-end products; and entry-level implants are performed by young and middle-aged dentists using cost-effective products. By achieving full coverage across high-, mid-, and low-end market segments, the company better meets patient demands, enabling its implant business to drive volume growth through strategic pricing.

▲Graphic by VCBeat

▲Graphic by VCBeat

Additionally,Given that an emphasis on full-mouth treatment may have a short-term impact on employee performance, dental institutions should also adopt new revenue distribution mechanisms.Multiple industry experts have pointed out that to maintain employee stability in a competitive environment, dental institutions should shift their focus from short-term incentives to medium- and long-term incentives. This involves transitioning from high commissions and bonuses to substantial year-end profit-sharing, as well as implementing well-designed stock option plans to share future growth with the team.

It is evident that dental institutions must undergo more substantial transformations—whether in their operational philosophy and business structure, or in their product strategies and management practices—to achieve sustainable growth amidst the industry’s profound upheaval.

“Two key factors determine whether the dental industry in a given region can achieve long-term development: one is population, and the other is the level of economic development. Therefore, in our investment decision-making process, we often conduct detailed comparisons between China’s dental industry and those in Europe, the United States, and other regions to assess the current stage of China’s dental sector and identify opportunities,” said Liu Chenyang.

Liu Chenyang believes that, compared with Europe and the United States,China’s oral care industry still has room for high-speed growth, but it is currently undergoing a period of intense volatility and profound transformation, making it an unfavorable time for investment., prudent investment institutions will focus on observing high-quality enterprises that are implementing effective reforms and possess the potential for chain expansion at this moment. Once these dental clinics “weather” this period, those that emerge successfully will participate in the global competition within the industry. “It is essential to prioritize the improvement of profitability and the continuous accumulation of reputation. Dentistry is a long-term industry; practitioners must be ‘marathon runners’ rather than sprinters. Therefore, they should avoid becoming trapped in unending ‘price wars.’”

Take Spain’s former dental chain iDental as an example. After its establishment in 2014, it rapidly grew into an industry leader through an ultra-low-price strategy and was even dubbed by Spanish media as the “world’s largest dental chain.” Yet its rise was swift, and its fall equally abrupt; in June 2018, iDental ceased operations.

It turns out that, in order to quickly stand out from its competitors, iDental reduced the price of its dental implant packages—originally around €2,000 per implant—to approximately €500 per implant through a series of discounts and subsidies. Furthermore, the company offers installment financing at this price point, lowering the actual monthly payment to just over ten euros, thereby significantly boosting users’ willingness to pay.

The key question here is: How can iDental reduce the cost of a dental implant solution from around €2,000 per unit to approximately €500 per unit?The answer is to sacrifice the quality of medical services.

Specifically, to cut costs, iDental has strictly controlled the number of dentists and recruited inexperienced graduates through “paid internships.” These interns receive mentorship from experienced dentists and directly practice dental implant procedures on real patients, while their compensation is only one-fifth to one-tenth that of licensed dentists.

According to overseas media reports, a patient, after comparing multiple dental clinics, was ultimately drawn by iDental’s exceptionally low prices and chose to undergo dental treatment there. However, the patient developed a postoperative infection, sustained high fevers, and soon experienced implant failure. Data from the local industry association showed that in 2016, iDental accounted for as much as one-quarter of all dentist–patient disputes in Spain’s dental care services. By 2018, the number of patients affected by iDental had reached tens of thousands.

Reputation Collapse and Sharp Decline in User Base: Former Star Institution iDental Falls from Grace, Founder Imprisoned for Causing Numerous Medical Malpractice Incidents and Engaging in False Advertising

Taking iDental as a cautionary tale, China’s dental industry must not repeat the missteps that led to the downfall of Spain’s dental chain giants; instead, it should advance steadily and remain committed to long-termism. “The current stress test presents an excellent opportunity for Chinese dental enterprises to build sufficient resilience. When the next growth cycle arrives, those companies that have been tempered during this phase will emerge at the forefront,” said Liu Chenyang.

In this process, every participant in the dental industry must bear in mind the original aspiration of “prioritizing the quality of medical services” to usher in more robust growth.

References:

1: “Which ‘Dental Implant Hospital’ Is Behind the Crazy Phone Harassment of Shanghai Residents?” — Shangguan News

2: “From ‘Oral Health Charity’ to ‘Biggest Scandal’: The Downfall of Spain’s Low-Cost Dental Chain” — Implants Without Borders