2024 Health Insurance Industry Research Report: Annual Revenue Set to Surpass RMB 1 Trillion for the First Time, with Coverage for Individuals with Pre-existing Conditions Emerging as a Key Growth Driver

In recent years, the penetration rate of health insurance has increased, but its growth rate has slowed. Meanwhile, the substantial demand from individuals with pre-existing conditions remains unmet. It is estimated that the potential premium revenue from this segment could reach RMB 400 billion. On the other hand, health insurance products suffer from severe homogenization, there is an insufficient variety of mid-tier medical insurance options, and customer experiences—particularly in claims processing and health management services—require improvement.

The mismatch between supply and demand is the primary bottleneck to further growth in the health insurance market. Supply-side reform centers on developing insurance products for individuals with pre-existing conditions and enhancing experience-driven services. Innovations are also emerging, including comprehensive insurance products, one-stop services, specialized disease centers, intelligent service delivery, and the integration of service responsibilities into insurance coverage.

For insurance companies, what are the respective pain points in product design, service delivery, technology application, and payment processes? And what role do health management companies play in addressing these issues? This report analyzes the challenges and innovative solutions in the health insurance industry through surveys of 12 enterprises and nearly 20 experts, arriving at the following conclusions:

1. Health insurance products possess both financial and consumption attributes; in recent years, their development has primarily been driven by the expansion of their consumption attribute. From an underwriting perspective, the evolution of health insurance has progressed through three stages: “strict underwriting,” “lenient underwriting,” and “targeted underwriting.”

2. According to statistics from the National Financial Regulatory Administration, the premium income of the health insurance market reached RMB 742.2 billion as of August 31, 2024. Based on the average monthly premium forecast, the health insurance premium income in 2024 is expected to exceed RMB 1 trillion, marking the first time the health insurance market may break through the trillion-yuan threshold.

3. The supply of health insurance is gradually shifting from sales-driven to service-driven, with equal emphasis on performance and customer perceived value. “Insurance + Health Management Services + Technology” has become the standard, while proactive management, disease-specific management, one-stop services, and experience-centric approaches have emerged as new trends among insurance companies.

4. The key to integrating social and commercial insurance lies in data sharing, with data structuring representing the future direction. On the government side, in addition to supporting data sharing between basic medical insurance and commercial health insurance, it is also necessary to provide marketing endorsements or research support for commercial insurance.

5. In the future, insurance products will tend toward personalization, with the empowering role of technology becoming increasingly prominent; mid-end medical insurance will gradually diversify and extend coverage to non-standard risks; however, personalized premiums, which involve insurance underwriting and sales processes, may not be immediately feasible.

6. Service accountability shifts the focus from managing operational risks to managing consumer experience, transforming compensation payouts into service delivery. This enables customers to enjoy a better and more timely experience during hospitalization, thereby significantly expanding the market.

Market Size Poised to Surpass One Trillion Yuan as Policy Support Reaches New Heights

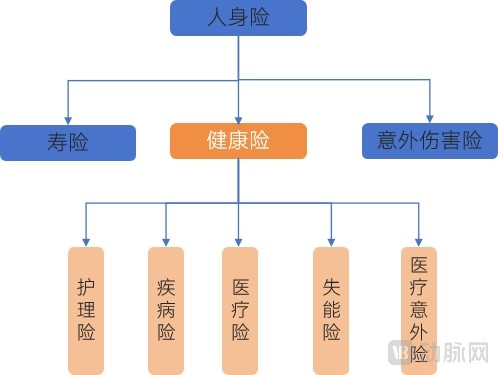

Health insurance refers to insurance under which an insurer pays benefits to the insured upon the occurrence of health-related events or medical care services. It primarily includes critical illness insurance, medical expense insurance, long-term care insurance, disability income insurance, and medical accident insurance.

Composition of Health Insurance

Image source: VCBeat

Stage: Consumer Attributes of Products Become Prominent, with Technology and Services Facilitating Resource Integration

Health insurance products possess both financial and consumption attributes, with recent development primarily characterized by the expansion of their consumption attribute. In terms of progress in consumer positioning, health insurance products have mainly evolved through three stages: “no consumption attribute – limited consumption attribute – pronounced consumption attribute.”

The first phase is the critical illness insurance stage, during which health insurance products and consumption are not directly correlated; similar to life insurance in positioning, they serve as compensation for income loss.

The second phase emerged with the advent of products such as million-yuan medical insurance, terminal medical insurance, and long-term medical insurance. During this period, health insurance acquired a certain payment function for healthcare consumption; however, this attribute was passive, with reimbursement and compensation limited to aleatory events—such as hospitalization and surgery—that carry a measurable probability of risk.

The third phase involves insurance tailored to specific population segments, such as when insurers cover payments for particular diseases or demographic groups. In this context, the consumer-oriented nature of healthcare becomes more pronounced, encompassing stages such as pre-diagnosis prevention, post-hospitalization care, and during-clinic consultations for targeted populations.

From the perspective of underwriting criteria, the development of health insurance has undergone the stages of “strict underwriting,” “lenient underwriting,” and “targeted underwriting.”

The first phase is essentially limited to insurance for healthy individuals, involving strict underwriting. For instance, critical illness insurance and long-term medical insurance require explicit health declarations, with verification conducted during the claims process, thereby covering only “healthy individuals.”

The second stage involves health insurance under relaxed underwriting conditions, such as inclusive insurance and Huimin Bao; the third stage features exclusive insurance products tailored for specific populations, which impose stricter controls on risk adverse selection and other aspects, leveraging advanced insurance technologies such as gamified underwriting and interactive policies. See the figure below for details:

The Evolution of Product Positioning and Underwriting Criteria in Health Insurance

Image source: VCBeat.

In terms of business model, the industry has evolved from offering single products to leveraging technology and services for resource integration. In its early stages, the health insurance industry had a relatively simple business model, primarily operating as an ancillary line of business attached to life or property insurance.

Following its entry into the phase of specialized development, the health insurance industry began to gradually decouple from life and property insurance, establishing a specialized operational model. During the subsequent stage of product diversification, the variety of health insurance products expanded significantly, beginning to cover broader scopes of protection and address more granular demographic needs.

This period was characterized by the launch of critical illness insurance, medical insurance, and other products, as well as customized insurance offerings tailored to specific populations or diseases. Meanwhile, insurers began leveraging new technologies such as big data and artificial intelligence to enhance the precision of risk assessment and pricing.

Having entered a phase of service integration and technology-driven innovation, the health insurance industry has begun to focus on building a comprehensive health service ecosystem, integrating resources from healthcare, health management, and insurance sectors to provide consumers with one-stop health management solutions.

Policy: Increasingly Intensive in Recent Years, with Unprecedented Strength

As population aging intensifies and the national social security system advances, policies targeting health insurance have become increasingly frequent in recent years. We have reviewed 21 policies issued over the past six years and found that, while continuing to promote collaboration between commercial health insurance and basic medical insurance, recent policy initiatives have placed particular emphasis on supply-side reforms in the commercial health insurance sector.

The policy primarily covers three areas: products and services, elderly care, and critical illness. Regarding products and services, the focus is on encouraging differentiation and full-lifecycle coverage. In the realm of elderly care, efforts are being advanced through exclusive products and long-term care insurance. For critical illness, the emphasis is mainly on cancer prevention and treatment, with encouragement given to improving critical illness insurance and assistance programs. Details are as follows:

Key Focus Areas of Recent Health Insurance Policies

Image source: VCBeat

From a temporal perspective, since 2022, policy emphasis on commercial health insurance has intensified and become more specific. The density of supportive policies for commercial health insurance has increased, providing not only support for its development and mandating coordinated development with basic medical insurance, but also outlining directions for customized health service packages.

Review of Recent Health Insurance Policies

Image source: VCBeat

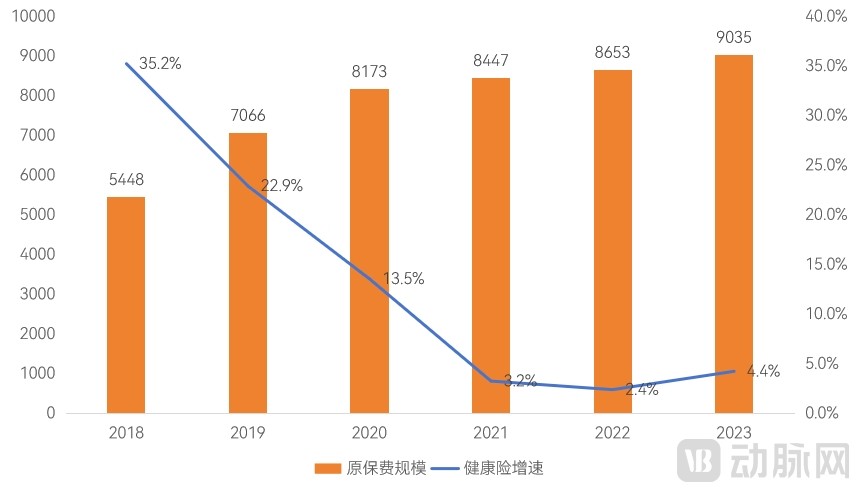

Market: Scale May Exceed One Trillion, with Insured Patients as a Strong Growth Driver

As of 2023, the premium income of China’s commercial health insurance market reached RMB 903.5 billion, a year-on-year increase of 4.4%, marking the third consecutive year with single-digit growth rates. According to statistics from the National Financial Regulatory Administration, the premium income of the health insurance market amounted to RMB 742.2 billion as of August 31, 2024. Based on the average monthly premiums, the health insurance premium income for 2024 is projected to exceed RMB 1 trillion.

2018–2023 Original Premium Income from Health Insurance

Data Source: National Financial Regulatory Administration

Diversifying Products, Payment Drives the Industry

Current Situation: The Supply-Demand Contradiction Is Prominent, and Product Development and Promotion Face Challenges

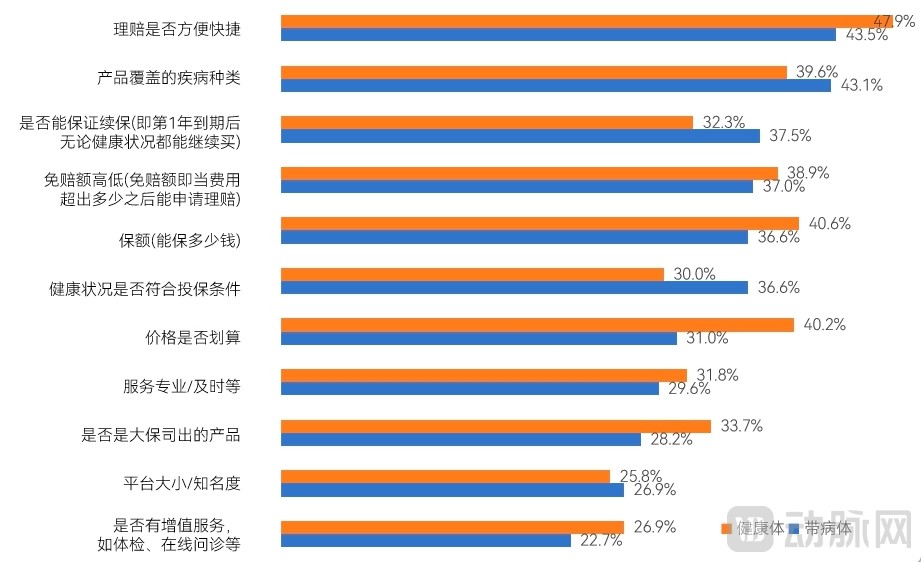

Individuals with pre-existing conditions exhibit strong demand for health services and demonstrate lower price sensitivity compared to healthy individuals. According to the "Research Report on Insurance Innovation for Individuals with Pre-existing Conditions," unlike healthy individuals who prioritize experience-oriented features such as value-added services that streamline claims processing, those with pre-existing conditions place greater emphasis on tangible protections, including policy renewability and the scope of covered diseases.

When asked, “What factors do you primarily consider when purchasing insurance?” both healthy individuals and those with pre-existing conditions are most concerned about “the ease of claims settlement.” The factor with the greatest disparity in concern between healthy individuals and those with pre-existing conditions is “whether the price is cost-effective,” as detailed below:

Considerations for Insurance Purchase by Healthy and Non-Healthy Individuals

Data source: Shuidi Bao

Current insurance products for individuals with pre-existing conditions are subject to numerous restrictions and limited variety. Among the policies available to this demographic, underwriting requirements are stringent, with extensive stipulations typically imposed on deductibles, coverage periods, eligibility criteria, and scope of benefits. These measures are, of course, designed based on risk control considerations.

Pre-existing condition individuals who can relatively easily obtain insurance coverage are primarily those with chronic diseases characterized by a long disease course, relatively slow progression, and minimal impact on daily life, or those whose conditions are closely related to medication adherence and disease management, such as patients with hypertension, diabetes, thyroid nodules, hepatitis B, or kidney disease.

Overall, the insurance industry for individuals with pre-existing conditions is in its early stages. On one hand, data scarcity acts as a major obstacle to pricing and risk control, hindering product development; furthermore, designing insurance products for this population challenges the traditional operational logic of the insurance industry.

Although China has a large population of individuals with pre-existing conditions, not all such individuals fit the law of large numbers required by traditional commercial insurance. Insufficient underwriting scale can increase the volatility of loss ratios, leading insurers to incorporate higher safety margins in their pricing. In short, data scarcity makes it difficult to manage pricing and risk control for insurance products covering individuals with pre-existing conditions.

On the other hand, there is insufficient integration between insurance for individuals with pre-existing conditions and the healthcare and pharmaceutical sectors. Insurance for this population must be deeply integrated with medical services and pharmaceuticals to jointly manage risk control. Relying solely on the traditional commercial health insurance model—using conventional algorithms, models, and liability limitations—is inadequate for mitigating claim risks arising from over-treatment and exorbitant pharmaceutical costs.

In addition, insurance products for individuals with pre-existing conditions face similar challenges in promotion. Precisely reaching this target population remains a difficult task. Moreover, unlike coverage for specific fixed conditions with limited eligible populations, most conditions struggle to achieve sufficient enrollment volume, making it difficult to realize economies of scale.

Challenges Facing the Development of Insurance for Individuals with Pre-existing Conditions

Image source: VCBeat

Product: Requires multi-party collaboration to address; established paradigms remain distant, while innovations continue to emerge

From a top-level design perspective, it is necessary to integrate data from hospitals, basic medical insurance, and commercial health insurance to provide greater support. If patient and disease data from public hospitals, along with reimbursement data for various diseases from medical insurance authorities, can be shared with commercial health insurance companies, this would encourage insurers to actively expand their markets. By leveraging such data for actuarial analysis, insurers can develop health insurance products that better meet public demand, achieve precise pricing, and ultimately create more accurate and practical commercial health insurance offerings.

For insurers, the research, design, and iteration of insurance products for individuals with pre-existing conditions require careful consideration at every step. Compared with conventional health insurance, risk control measures for health insurance covering pre-existing conditions are more critical and sophisticated, often employing a comprehensive approach that integrates channel management, underwriting, internal “blacklists” and “gray lists,” policy terms (including deductibles, coverage scope, and reimbursement ratios), and reinsurance to mitigate risks.

This necessitates thorough preliminary research, product design, and continuous iteration. Underwriting health insurance for individuals with pre-existing conditions involves a substantial workload in the pricing phase, and requires ongoing post-launch retrospective analysis to optimize risk control measures and even the fundamental pricing assumptions.

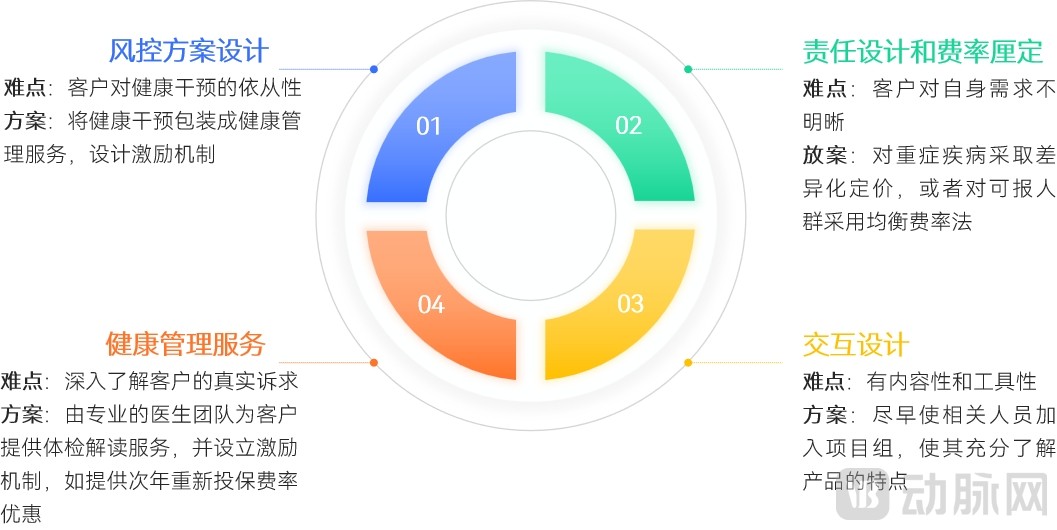

Product design for insurance covering individuals with pre-existing conditions is critical; each stage presents specific challenges and potential solutions, as illustrated in the figure below:

Challenges and Solutions in Each Stage of Product Design

Image source: VCBeat

In practice, the paradigm remains elusive, while innovations continue to emerge. We observe that many insurers are attempting to broaden product coverage to reach a wider and more precisely targeted population, while further enhancing the level of protection.

For instance, this July, AIA Life Insurance also launched its first tax-advantaged long-term care insurance product, “Youxiang Changban.” If the insured is diagnosed with one of the 10 specified diseases stipulated in the contract, or sustains Grade 1–3 disability due to an accident, a lump-sum long-term care benefit will be paid. With eligibility for individuals aged 7 days to 70 years, the product further enhances the inclusiveness of its offerings and services.

In addition, Taiyi Guanjia, in collaboration with insurance companies, has launched “Jia An Xin 2.0,” which is available in two versions: Plan A and Plan B. Plan A is a three-year million-yuan medical insurance policy, while Plan B is a one-year million-yuan medical insurance policy. Specifically tailored for middle-aged and elderly individuals as well as those with pre-existing health conditions, these plans offer broader eligibility age ranges, simpler underwriting requirements, longer coverage periods, and more attentive health services.

In addition, “Jia An Xin” has added services including home-based health indicator monitoring, five core areas of basic health management (exercise and nutrition management, pain management, Traditional Chinese Medicine wellness and conditioning, skin care management, and constipation management), one-stop critical illness management, and medical escort services for critical illness treatment.

According to the "China Elderly Health Report" jointly released in April 2024 by scholars from Wuhan University and Peking University, the number of disabled elderly people aged 60 and above in China has reached 46.54 million and continues to rise. Additionally, Alzheimer's disease has become a significant cause of dementia among the elderly in recent years.

The primary causes of disability and dementia among the elderly fall into four categories: accidental falls, Alzheimer’s disease, stroke, and other causes, accounting for 24%, 18%, 17%, and 41%, respectively. In light of these factors, there is an urgent need to develop innovative comprehensive insurance products tailored to the elderly, and some companies have already begun exploring solutions to address this demand.

For example, Yuanmeng Kangjian has partnered with insurance companies to offer “Xiao Xin An,” a comprehensive insurance product for seniors aged 50–85. This product primarily provides three service components: an Alzheimer’s disease management program, an emergency treatment system for accidental fractures and stroke, and a care and support plan for disability and dementia. “Xiao Xin An” features relatively lenient underwriting criteria, allowing seniors with underlying chronic conditions such as hypertension or diabetes to purchase the policy, thereby broadening its applicability.

“Xiao Xin An” innovatively integrates health services with insurance coverage. In addition to covering emergency medical expenses, it provides comprehensive assessment, prevention, emergency treatment, post-event care, and rehabilitation for risks associated with disability and dementia in the elderly, thereby holistically addressing their health concerns.

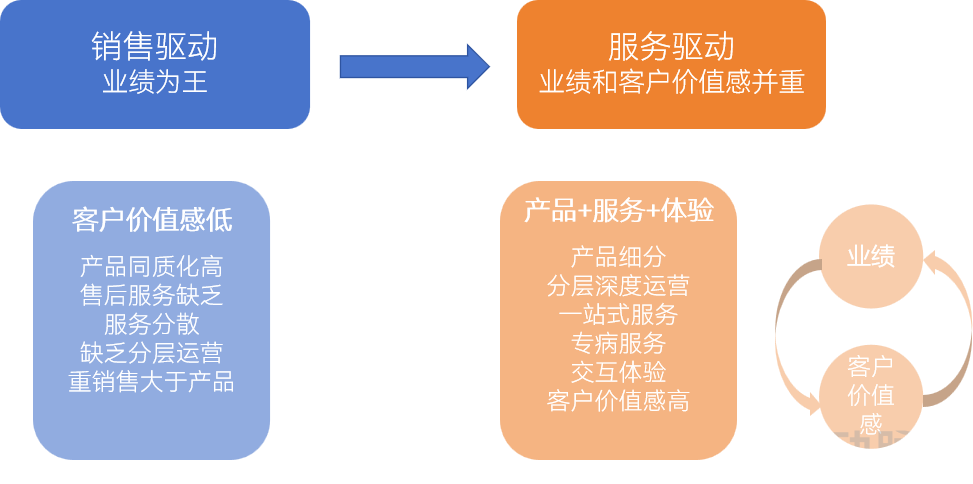

Service: Entering Deep Waters, Updating Concepts, Experience is King

Currently, the health insurance industry is undergoing a transition from sales-driven to service-driven models. The core of this shift lies in placing greater emphasis on consumer needs and enhancing customers’ perceived value, rather than merely selling insurance products. This involves creating more targeted combinations of products, services, and experiences, implementing in-depth customer engagement, and delivering one-stop services as well as disease-specific management. Details are illustrated in the figure below:

Schematic Diagram of the Transition in Health Insurance Supply from Sales-Driven to Service-Driven

Image source: VCBeat

From Passive Claims Settlement to Proactive Full-Process Management: Customer Experience Is Paramount. Today, the model of “insurance + health management services + technology” has become standard practice. Drawing on the development patterns of health insurance and health management in various mature economies, commercial insurers in China—acting as one of the payers for medical expenses—are actively seeking to transform their role from “passive claims settlement” to “proactive full-process management.” They are evolving from mere payers into managers of integrated health management services, placing greater emphasis on customer experience, continuously improving service quality, and diversifying their product offerings.

For instance, in terms of service experience during the claims process, most policies that resulted in payouts previously would compensate the insured immediately after meeting the insurance policy terms, but without providing an explanation for the payout. For example, there was no medical perspective offered to explain why a specific amount was compensated, nor any discussion of how current medical treatments might impact future health outcomes.

Currently, we are seeing companies begin to provide such services to users, explaining claim settlements to enhance user experience, while also communicating about subsequent health management services and potential risks, thereby strengthening customers’ trust in insurance companies.

Technology: AI Expands the Boundaries of Health Insurance, Empowering Insurers’ Value Chain

In the realm of health insurance, AI is applied across every link of the insurance value chain. AI empowers numerous aspects of health insurance; from a front-end perspective, technologies such as big data-based user tagging systems and intelligent health insurance product recommendations are leveraged to deeply uncover customer needs and enhance channel efficiency.

From the backend perspective, leveraging technologies such as high-precision risk identification and intelligent claims adjudication can mitigate underwriting and claims risks while improving the efficiency of claim processing. Overall, AI empowerment enhances product differentiation, boosts user perception and customer stickiness, effectively controls disease risks, and reduces claim payouts.

AI-Empowered Value Chain of Insurance Companies

Image source: VCBeat

Meanwhile, health management companies are gradually emerging as new technological players in the health insurance industry. By developing intelligent applications, these companies can monitor users’ physiological indicators through smart devices. Leveraging risk prediction models, they provide health management guidance via a hybrid approach of human expertise and AI to delay disease progression. Furthermore, by offering integrated online and offline medical services, they optimize the healthcare experience for patients, improve policyholders’ physical well-being, and enhance medical service delivery, thereby reducing claims risks across multiple dimensions.

For example, Huamei Haolian has developed intelligent service products such as “AI Doctor Assistant,” “AI Digital General Practitioner,” “AI Precision Medical Care,” and “AI Physical Examination Report Interpretation,” transforming artificial intelligence technology from back-end support and theoretical foundations into front-end, practical tools.

In terms of process, Huamei Haolian leverages pre-consultation services—including electronic health record creation, digital doctors, and AI triage systems—to enable early detection and treatment. During consultation, its technological middle platform, featuring a digital case management platform, standardized triage system, and quantitative quality control indicators, facilitates triage management and rational drug use, thereby avoiding overtreatment. Post-consultation, the company employs an AI-powered intelligent follow-up system, a nationwide medical network, and an offline team of over 500 healthcare professionals to conduct regular follow-ups and reduce recurrence rates. By implementing risk control across pre-, intra-, and post-consultation stages, Huamei Haolian ultimately lowers the overall claims ratio.

Payment: Diversified Payment Methods Drive Industry Innovation, with Shanghai’s Demonstration Effect Gradually Emerging

The “multi-party cost-sharing and diversified payment” system has long attracted significant attention. Currently, China’s healthcare financing remains dominated by basic medical insurance; although a multi-tiered medical security system has been established in framework, its structural balance and weighting still require refinement.

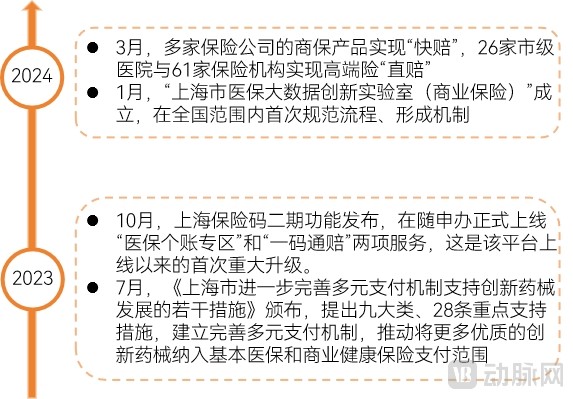

Shanghai has taken the lead in breaking new ground, introducing unprecedented policy support for commercial health insurance while vigorously advancing implementation efforts and achieving tangible results across multiple areas.

Shanghai Strives to Advance the Implementation of a Diversified Payment Mechanism

Image source: VCBeat

Judging from current results, Shanghai’s initiatives have undoubtedly been successful: in 2023, medical institutions in Shanghai purchased nationally negotiated innovative drugs worth RMB 10.8 billion, a year-on-year increase of 73.1%; multiple municipal hospitals and insurance providers have implemented “direct settlement” for high-end insurance plans; and a “Big Data Laboratory” has been established to enable sharing of medical insurance data, allowing numerous insurance companies to develop more precisely tailored products based on this data.

For users, enhanced experiences and greater benefits naturally lead to higher satisfaction; for enterprises, Shanghai has introduced numerous supportive policies, gradually fostering an environment that encourages the purchase of commercial health insurance.

Certainly, the fundamental reasons for Shanghai’s emergence as a “model” are twofold: on one hand, the Shanghai Municipal Healthcare Security Administration has ample funding; on the other, the government maintains an open attitude, actively seeking solutions and rigorously implementing them.

Data sharing enables insurers to develop products more efficiently and accurately; improvements in users’ claims, operational, and payment experiences have enhanced customer satisfaction; and the increasing coverage of innovative drugs and medical devices under medical insurance has helped pharmaceutical companies reduce costs. These are practical implementations by the Shanghai Municipal Government from the perspectives of enterprises, users, and pharmaceutical companies, which will also serve as an effective demonstration model.

Further Advancement of Social-Commercial Integration: Service Accountability May Be the Direction

Integration of Social and Commercial Sectors Requires Breakthroughs in Data Sharing, While Medical-Insurance Collaboration Needs Institutional Balance

The key to integrating social and commercial sectors lies in data sharing, with data structuring representing the future direction. The healthcare insurance, medical care, and pharmaceutical sectors possess vast data resources and rich application scenarios. Activating these data elements and improving and standardizing data circulation rules will provide essential data support for insurers’ actuarial work in developing insurance products, enabling them to create more universal and mass-market coverage products and facilitate direct online claims settlement.

To unlock greater value from current health insurance data after de-identification, further structuring is required, along with the gradual establishment of pricing models for different disease categories. This approach enables the derivation of disease incidence rates from health insurance data and provides insights into the cost structure of treatment, including the respective proportions attributable to medical services, pharmaceuticals, and consumables. The higher the granularity, completeness, and timeliness of the data, the greater its value.

Meanwhile, in addition to supporting data sharing, it is necessary for the government to provide marketing endorsements or research support for commercial health insurance.

Government Initiatives in the Integration of Social and Commercial Sectors

Image source: VCBeat

On the other hand, ideally, medical-insurance collaboration can enhance customers’ perceived value. However, current medical-insurance partnerships operate more at a macro level, primarily directing patient flow from insurers to hospitals. Existing collaborations are largely macro-level in nature, such as providing medical expertise for product design or delivering post-service support for commercial insurance.

For instance, Zhongshan Hospital partnered with PICC to establish the “Zhongshan-PICC Innovation Research Center,” a pioneering initiative. According to reports, the center will conduct research on various health insurance topics, including refined medical management and optimized commercial insurance benefit design, aiming to alleviate payment-side pressures and lay the groundwork for the hospital’s next steps in optimizing its disease-case mix and facilitating precise patient referral for complex and rare conditions.

In terms of benefit distribution, there is a game-theoretic dynamic between hospitals and insurance companies, necessitating institutional mechanisms to achieve balance. During the utilization of insurance products, insurers interact with hospitals only at the time of claims settlement. Since hospital revenue constitutes insurance losses (i.e., costs), a conflict of interest exists between the two parties. Therefore, an institutional equilibrium between hospitals and insurers is required, or official authorities should provide prescribed solutions.

For instance, drawing on certain foreign systems, some hospitals or insurers provide services rather than monetary compensation for claims in specific circumstances, and some countries redistribute the surplus from insurance premiums.

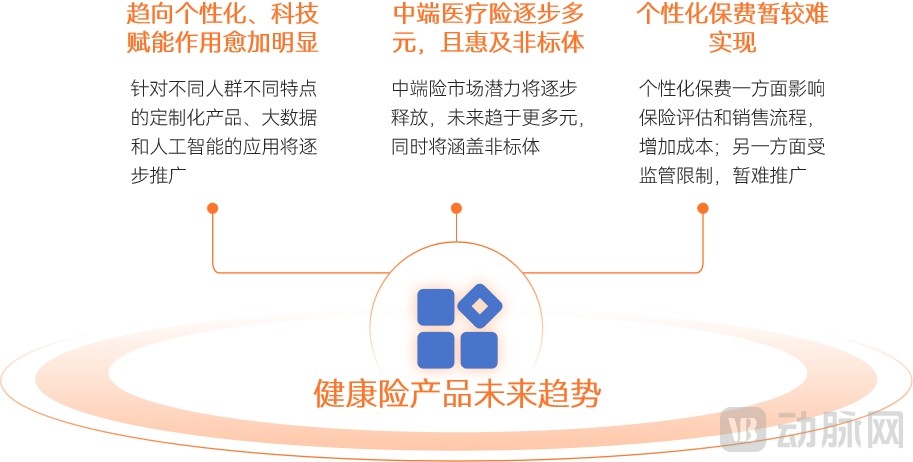

Products Are Becoming More Personalized: Mid-Tier Medical Insurance May Benefit Individuals with Non-Standard Health Profiles

Regarding the product, we conducted discussions on product direction, target demographics, and premiums, as detailed below:

Future Trends in Health Insurance Products

Image source: VCBeat

On the one hand, health insurance products will tend towards personalization, with the enabling role of technology becoming increasingly prominent. On the other hand, as technology continues to advance, health insurance and insurance products for individuals with pre-existing conditions will increasingly leverage big data, artificial intelligence, and other technological tools for risk assessment, pricing, and product design. Through precise risk-based pricing and tailored product design, these innovations will better meet consumers’ protection needs.

On the other hand, mid-tier medical insurance products will gradually diversify and increasingly extend coverage to individuals with non-standard health profiles. In terms of existing market segments, Huiminbao (city-specific supplemental medical insurance) products cover a broad portion of the low-end medical insurance market, while the penetration rate of high-end medical insurance has increased in recent years but remains limited in overall development.

The advantages of mid-tier medical insurance are evident, with relatively broad coverage and premiums typically maintained at a reasonable level, indicating significant potential for future market growth. Although million-yuan medical insurance plans have already penetrated the mid-tier market, product segmentation within this segment remains insufficient. Future offerings are expected to become more diversified. Furthermore, there is still a substantial gap in insurance products tailored to non-standard risk profiles in the mid-tier market.

Finally, personalized premiums involve insurance underwriting and sales processes, which may not be feasible at present. Unlike auto insurance, where premiums for the following year are individually adjusted based on the policyholder’s claims experience during the current year, health insurance premiums are typically fixed and do not adopt a differentiated pricing structure based on the insured’s health status or claims history.

The underlying reason is that, for insurance companies, if they design promotion and assessment stages prior to insurance sales and conduct customer acquisition only after the assessment, they will have a certain understanding of the customers’ risks. However, implementing targeted sales based on different customer risk levels will inevitably lengthen the insurance sales process, thereby affecting sales outcomes.

If risk assessment is conducted after the sale of an insurance policy, with subsequent coverage determined based on the identified risks and the sum insured adjusted upward or downward according to the scope of insurance liability, this approach may appear straightforward in practice but could actually prove challenging to implement.

Here, industry regulatory rules prevent flexible premium adjustments. Meanwhile, risk assessment incurs costs, and different risks correspond to different plans, making it difficult for insurers’ end-to-end processes and systems to provide adequate support. Furthermore, from the customer’s perspective, learning that they are classified as a “standard risk” after assessment may reduce their willingness to purchase; conversely, if they are identified as high-risk, they may struggle to accept the result internally. These irrational factors can influence their purchase intent.

From a macro perspective, foreign insurers, such as those in the United States, often own hospitals or medical resources and primarily offer group insurance policies, allowing for flexible plan design. In contrast, there is a disconnect between insurers and hospitals in China, preventing flexible arrangements; therefore, personalized premiums are not currently feasible.

Accountabilizing Service Delivery to Enhance Customer Experience: Challenging to Implement Extensively at This Stage

Service-Oriented Liability: Transforming Claim Payouts into Care ServicesService-oriented liability transforms monetary claim payouts into direct care services, enabling customers to enjoy a better and more timely experience during hospitalization. Under this model, when a customer files an insurance claim, the insurer engages a health management company to provide services directly to the customer, rather than disbursing a cash payment. After the services are rendered, the health management company settles the costs with the insurer. Throughout this process, the customer does not need to purchase services out-of-pocket, nor do they receive any monetary compensation from the insurer.

Currently, such products are not integrated, as many insurance policies do not cover inpatient care costs. Some policies offer hospitalization allowances, paying a fixed amount based on the number of days hospitalized; however, these are largely post-event compensations that can only be claimed after discharge, resulting in a lag in reimbursement.

If claims services are included, customers can access them during their hospitalization. Many customers struggle to find reliable service resources on their own; therefore, some may prefer plans that offer premium claims services. Assigning clear service responsibilities enhances the customer’s healthcare experience.

The institutionalization of service accountability faces challenges related to policy and quantification, with considerable ground still to be covered. On September 9, 2020, the official website of the China Banking and Insurance Regulatory Commission (CBIRC) formally issued the Notice on Regulating Health Management Services Provided by Insurance Companies (hereinafter referred to as the “Notice”).

The Notice stipulates that if the health management services provided by insurance companies are included in the liability clauses of insurance products, their allocated costs shall not exceed 20% of net premiums, whereas this ratio was 10% under previous regulations.

Although the proportion of services has increased, it remains severely constrained. Currently, some insurance companies are attempting to incorporate home care into their coverage responsibilities and are also exploring the inclusion of inpatient nursing services. However, it is not yet realistic for service coverage to encompass the entire consumer chain.

Furthermore, the assignment of service liability faces challenges related to quantification and pricing. In this context, China’s health insurance sector can use basic medical insurance as a benchmark: if a service is covered by basic medical insurance, commercial insurance can also provide reimbursement, as seen with digital therapeutics that have been admitted into hospitals. However, pricing and transfer payment mechanisms for services not covered by basic medical insurance remain to be explored. Although theoretically sound from an economic perspective, significant progress is still required in the future.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1 Overview: Market Size Poised to Surpass One Trillion Yuan as Policy Support Reaches New Heights

1.1 Stage: The consumer attributes of products become prominent, with technology and services facilitating resource integration

1.2 Policies: Increasingly Intensive in Recent Years, Reaching New Heights in Strength

1.3 Market: Scale May Exceed One Trillion Yuan, with Insured Patients as a Strong Growth Driver

Chapter 2 Innovation: Increasingly Diverse Products, Payment Mechanisms Driving the Industry

2.1 Current Situation: Supply-Demand Imbalance Becomes Prominent, Product Development and Promotion Face Challenges

2.2 Products: Requiring Multi-Party Collaboration; Paradigms Remain Distant as Innovations Emerge

2.3 Services: Entering Deep Waters, Updating Concepts, and Prioritizing Experience

2.4 Technology: AI Expands the Boundaries of Health Insurance and Empowers Insurers’ Value Chain

2.5 Payment: Diversified Payment Methods Drive Industry Innovation, with Shanghai’s Demonstrative Effects Gradually Emerging

Chapter 3 Corporate Case Studies

3.1 Taiyi Guanjia: Providing Professional Health Management Services for Middle-aged and Elderly Individuals and Specialized Disease Insurance

3.2 Huamei Haolian: One-Stop AI Healthcare Service Platform

3.3 Yuanmeng Kangjian: Building Smart Health Management Based on Technology and Payment Innovation

Chapter 4 Trends: Further Advancement of Social-Commercial Integration, with Accountability in Services as a Potential Direction

4.1 Integration of Social and Commercial Sectors Requires Breakthroughs in Data Sharing, While Medical-Insurance Collaboration Needs Institutional Balance

4.2 Products Are Becoming More Personalized; Mid-End Medical Insurance May Benefit Non-Standard Risks

4.3 Making Services Accountable to Improve Customer Experience: Difficult to Implement Extensively at the Current Stage

Please scan the QR code to add the assistant and obtain the full report. If you have already added the assistant, please initiate a query:

Special Acknowledgments (in the order of research interviews):

Mr. Li Shuo, Co-founder and COO of Taiyi Guanjia, MedXin Health, and Baoxian Jike; Mr. Yuan Ye, Vice President of Yuanmeng Kangjian; Mr. Ren Zhao, Head of the Innovation Business Department at Yuanmeng Kangjian; Ms. Xu Bingyu, Founder and CEO of Huamei Haolian; and Mr. Wang Shun, Head of Product for the Health Insurance Division at ZhongAn Insurance