1-Year CGM Approved, 2-Year Version on the Horizon: Is the Industry About to Be Disrupted?

As a multi-billion-dollar market segment, CGM has always been a fiercely contested battleground for industry leaders.

Abbott and Dexcom have cultivated this sector for decades, capturing the majority of the global market share. Although Medtronic holds the distinction of launching the first continuous glucose monitoring (CGM) system and seeks to create a differentiated advantage through integration with insulin pumps, it has gradually fallen behind in recent years. After misjudging the growth potential of CGM technology, Roche made a strategic pivot to urgently enter the market, positioning CGM as the primary driver for growth in its diabetes care business over the coming years.

Eversense 365 Implantable Long-Term CGM, image source: company official website

Under the successive market education efforts by major industry players, most users have come to view continuous glucose monitoring (CGM) devices as small, wearable patches with an approximate usage cycle of two weeks. However, Senseonics has defied this norm through years of steadfast commitment, extending the CGM device’s usage duration to 365 days by adopting an implantable approach.

Can its emergence disrupt the industry landscape, spark a new wave of technological innovation, or achieve commercial success? VCBeat attempts to answer these questions.

The bustling CGM market never lacks new topics.

Recently, U.S. company Senseonics announced that its next-generation Eversense 365 CGM system has received FDA approval, with indications covering patients aged 18 and older with type 1 and type 2 diabetes.

As its name suggests, unlike the familiar CGM systems with a usage duration of approximately two weeks, Eversense 365 can be used continuously for 365 days. It is currently the longest-lasting CGM on the market, significantly reducing the frequency of device replacements for patients and providing a more long-term blood glucose monitoring solution.

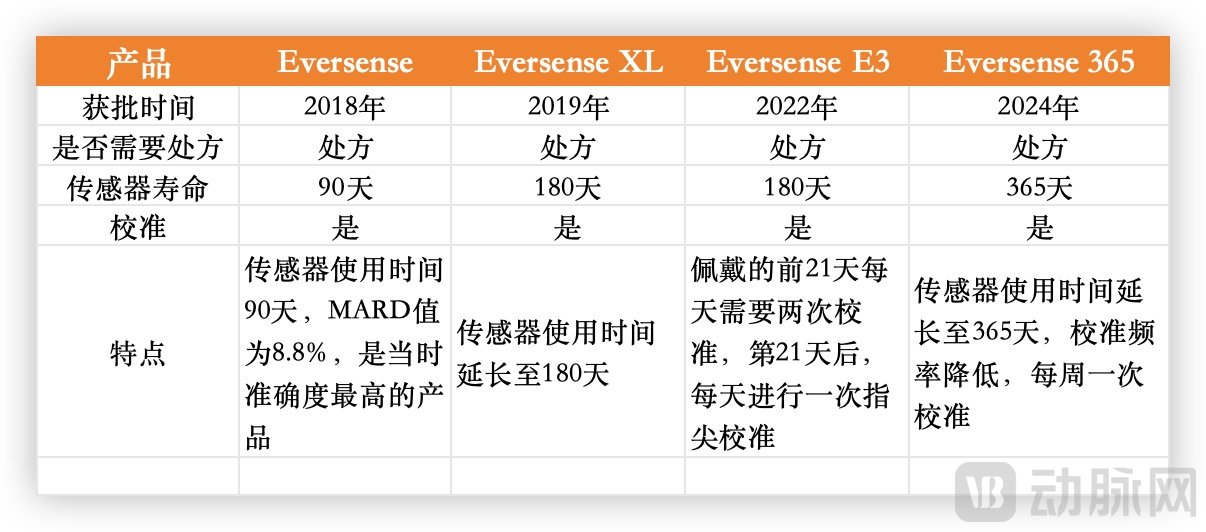

Unlike Dexcom, Abbott, and the newly entered Roche, Senseonics chose a different technological path from the outset. Starting with a 90-day wear time for its first-generation product in 2018, followed by subsequent iterations extending to 180 days, and now with the approval of its 365-day product, can Senseonics disrupt the existing CGM market landscape?

From a product perspective, this is indeed a highly anticipated product.

As Senseonics’ fourth-generation implantable long-term continuous glucose monitoring (CGM) system, Eversense 365 comprises the same components as its predecessor, Eversense E3: a sensor, a smart transmitter, and a mobile application. Compared with the previous generation, it not only doubles the wear duration but also significantly reduces the calibration frequency, offering a more user-friendly experience.

Eversense Series CGM Product Iteration Roadmap, Compiled from Publicly Available Information

Although the reduction from daily calibration in the previous generation to weekly calibration represents a significant advancement, it seems somewhat out of step with current expectations, as CGM users now regard calibration-free operation as a basic feature that any CGM should offer.

Furthermore, Eversense 365 has obtained certification as an integrated continuous glucose monitoring (iCGM) system, meaning it can be integrated with compatible medical devices for use as part of a closed-loop insulin delivery system. This integration potential positions Eversense 365 not merely as a monitoring device, but also as a key component of future comprehensive diabetes management solutions. Senseonics aims to leverage this capability to expand its user base.

Overall, Eversense 365, an implantable long-acting CGM, is a product with obvious advantages and even more pronounced disadvantages.

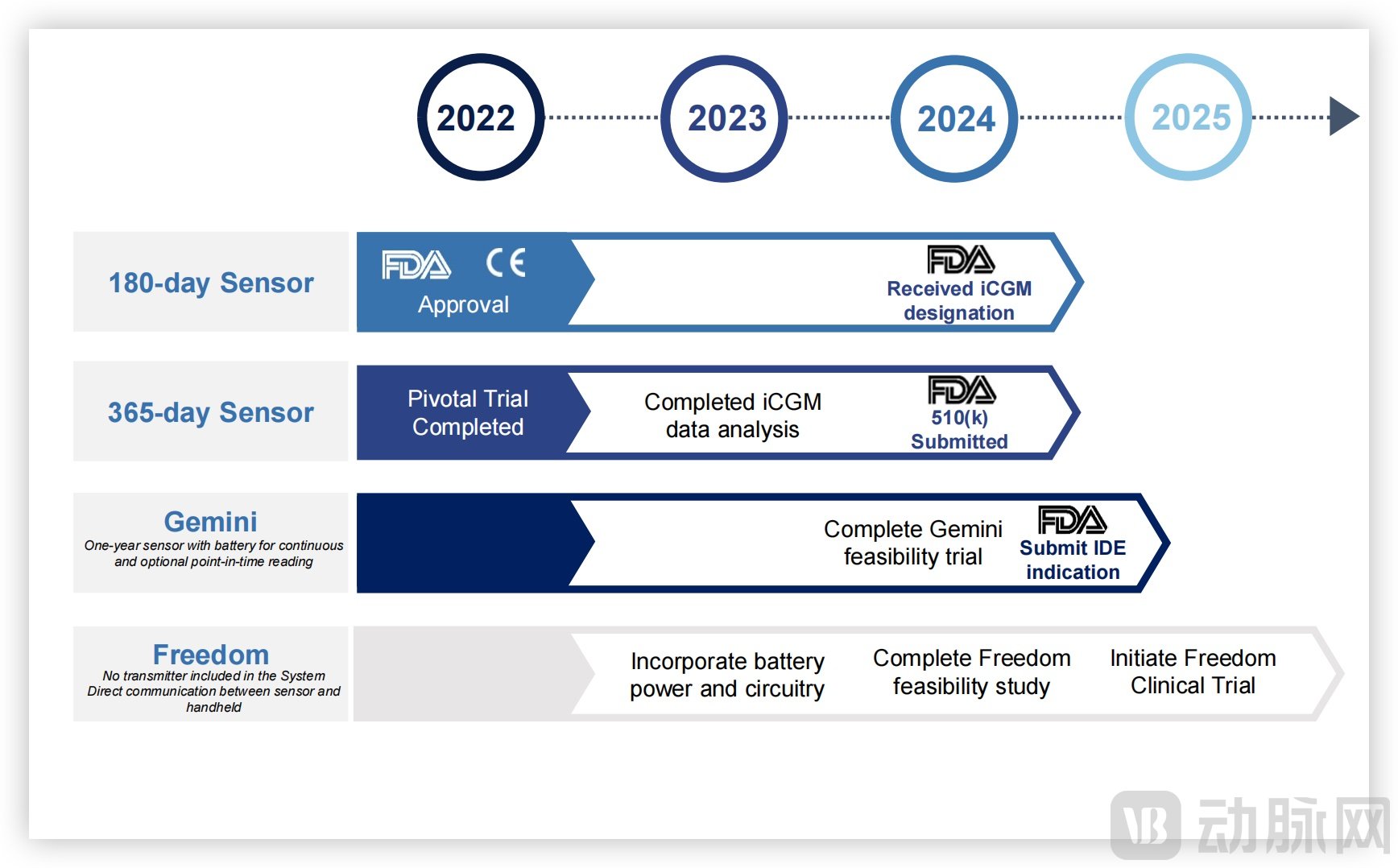

Senseonics’ Product Portfolio, Source: Company Website

Senseonics is well aware of its own disadvantages, so in addition to Eversense, it has two products under development: the Gemini System and the FREEDOM SYSTEM. Among them, the Gemini System is a fully implantable, self-powered system that can operate independently. It does not require users to wear a smart transmitter on their arm but instead connects directly to a mobile phone via NFC. The FREEDOM SYSTEM builds on this by adding Bluetooth functionality for a more seamless user experience. Currently, the Gemini System has entered human clinical trials.

Senseonics has chosen a niche path, which inevitably means its commercialization journey will not be smooth.

A product with significant strengths and pronounced weaknesses warrants close attention to its revenue performance.

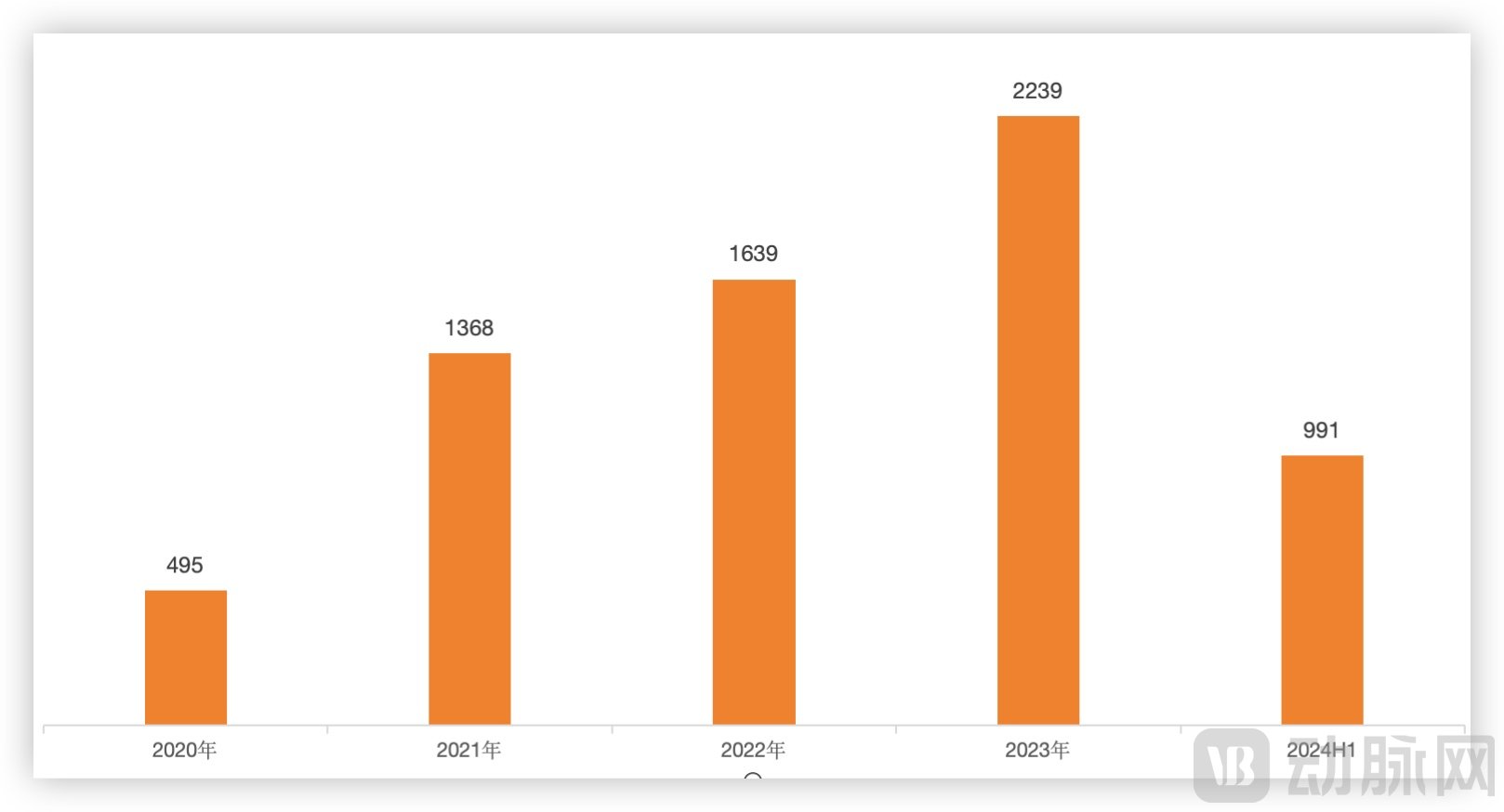

Based on revenue data from recent years, Senseonics’ products have failed to gain significant market traction. Although the company’s revenue has been on an upward trend since 2020, its overall scale remains modest. Even last year, when revenue reached a historical high, total annual revenue amounted to only $23 million, and the company has consistently operated at a loss.

Senseonics’ Revenue in Recent Years (Unit: USD 10,000), Data Sourced from Financial Reports

In contrast, Dexcom, which focuses on CGM, generated over $3.6 billion in revenue in 2023, while Abbott’s global income from CGM exceeded $5 billion. The two are not even in the same league in terms of scale.

Based on information disclosed in Senseonics’ earnings conference call, we can make a rough estimate.

Senseonics expects the total number of users in 2024 to be approximately 6,000. With revenues of around $10 million in the first half of 2024 (1H 2024), a simple calculation suggests that this $10 million in revenue corresponds to approximately 3,000 new patients. Based on this estimate, Senseonics’ cumulative user base from 2020 through 1H 2024 is approximately 20,000. In contrast, Abbott’s continuous glucose monitoring (CGM) system has already surpassed 4 million users globally.

As a representative of implantable long-term CGM, Senseonics’ market performance has been underwhelming, and its share of the global CGM market remains modest. With the launch of its next-generation product, Senseonics expects its user base to grow from 6,000 in 2024 to 12,000 in 2025. Despite the projected 100% growth, this increase is unlikely to significantly disrupt the overall industry landscape.

Senseonics has also recognized its own limitations and enlisted Ascensia Diabetes Care, a blood glucose meter company with an 80-year history, to handle the exclusive global distribution of its products. Ascensia will also explore collaborations with insulin pump manufacturers to expand its product portfolio.

Why Is a Highly Differentiated and Unique Product Not Accepted by the Market? To Answer This Question, We May Need to Address It from the Following Aspects.

Is Duration of Use Truly the Decisive Factor?

If a CGM could accurately measure blood glucose levels 365 days a year, it would undoubtedly be a groundbreaking product. However, Senseonics has already launched 90-day and 180-day products, which are significantly longer-acting compared to mainstream CGMs. Yet, the market response has been lackluster. This suggests that the key issue may not lie in the duration of use, but rather in whether extending the device’s lifespan can deliver additional value, such as:

Do long-acting products offer a better user experience?

From the perspective of product usage workflow, Eversense series products require implantation by a professional physician, along with the application of a transmitter on the skin. This transmitter is responsible for reading data and transmitting it to a mobile phone via Bluetooth. Meanwhile, the transmitter needs to be removed every 24 to 36 hours for recharging before being reapplied for use.

Compared to mainstream continuous glucose monitoring (CGM) systems, its key advantage lies in a single surgical implantation that provides up to 365 days of use, whereas CGM sensors require replacement every two weeks. However, given the current convenience of CGM wearables, biweekly replacement is hardly an issue. The mismatch between the sensor’s long-term durability and the transmitter’s short lifespan renders this product inherently contradictory.

Furthermore, the implantation process itself serves as a significant deterrent for users. The older Eversense models required two surgical procedures per year, while the newer models, with their extended usage duration, require one procedure annually. The surgery involves local anesthesia followed by a 0.2–0.3 inch (approximately 5–8 mm) incision to create a subcutaneous pocket in the fatty tissue for sensor placement. Postoperatively, the wound must be kept dry and clean for five days. Although this is a minimally invasive procedure with a very short operative time, the risks of postoperative infection and scarring remain.

In that case,Do Implantable CGMs Have Selling Points That Appeal to Mainstream CGM Users?

From an accuracy standpoint, the Eversense series does not appear to hold a competitive advantage. The Mean Absolute Relative Difference (MARD) of Eversense 365 is 8.8%, compared with 8.2% for Dexcom G7, 7.6% for Abbott FreeStyle Libre 3, and 8.66% for MicroTech Medical’s AiDEX X in China. Thus, it offers no decisive appeal to users in terms of accuracy.

Of course, price is also a critical factor. Currently, for patients enrolled in the PASS (Patient Assistance and Simple Savings) program, the out-of-pocket cost for Eversense 365 is $199, plus approximately $550 for the surgical procedures to insert and remove the sensor, resulting in an annual usage cost of around $750. In contrast, Dexcom G7, another mainstream CGM product in the U.S. market, has a monthly out-of-pocket cost ranging from approximately $0 to $20, depending on insurance coverage, leading to an annual out-of-pocket expense of roughly $0 to $240.

Given these issues, coupled with the lack of a price advantage, it is hardly surprising that Eversense’s sales have remained stagnant in recent years. From a production standpoint, since each user requires only one device per year, overall sales volume remains low. This precludes economies of scale, making cost reduction difficult and preventing any significant price decrease. This vicious cycle has become an intractable deadlock.

Therefore, some industry players believe that current implantable long-acting CGMs are more suitable for inpatient settings and a small subset of critically ill patients, having limited impact on the existing CGM market. Consequently, these companies have no immediate plans to develop such products, focusing instead on optimizing their existing offerings to continuously enhance user experience.

The technological pathway of implantable long-acting CGM should not be dismissed merely due to its current limitations.

In June 2024, Glucotrack announced the completion of its second long-term preclinical study on its implantable continuous blood glucose monitor (CBGM). This CBGM combines the accuracy of traditional BGM with the durability of CGM, minimizing the limitations of both methods as much as possible.

In terms of usage, all components of this CBGM are implanted into the patient’s body, eliminating the hassle and discomfort associated with frequently removing the transmitter for recharging and reapplication, while effectively safeguarding patient privacy. Regarding service life, the device can operate for more than two years after implantation, providing at least two years of continuous and accurate blood glucose monitoring, thereby facilitating patient self-management. In this preclinical study, the Mean Absolute Relative Difference (MARD) at day 90 was 4.7%, preliminarily validating the sustained accuracy of the CBGM. Furthermore, as glucose is measured directly from the blood, the system effectively mitigates the lag in blood glucose readings commonly observed in traditional CGMs that rely on interstitial fluid measurements.

CBGM R&D Progress Roadmap, Image Source: Company Official Website

Unlike the Eversense series, the continuous blood glucose monitoring (CBGM) sensor launched by Glucotrack is not implanted subcutaneously; instead, it is placed in the epidural space of study subjects to obtain readings from the spinal epidural space. This approach can be integrated with existing treatments for patients with painful diabetic neuropathy (PDN), delivering low-level electrical stimulation directly to the spine to alleviate pain. Furthermore, by adopting an electrochemical method for monitoring blood glucose fluctuations, its accuracy has been significantly improved compared to the optical-based Eversense system.

Recently, Glucotrack announced a collaboration with Focus to develop an implantable continuous blood glucose monitor (CBGM). Under the agreement, Focus will be responsible for the hardware and firmware design of the device. Both parties aim to seamlessly integrate blood glucose monitoring into daily life, minimize device management time, and enable unobtrusive use for patients.

Glucotrack’s CBGM technology is undoubtedly an innovation worth anticipating. It perfectly addresses the shortcomings of existing implantable long-term CGM products. With its ultra-long service life and high precision, CBGM technology is poised to fill this market gap, while also driving other companies in the industry to accelerate technological innovation and improvements. By meeting the ever-growing market demand with more convenient and discreet monitoring solutions, it will significantly enhance the quality of life for diabetes patients.

Since the beginning of this year, the CGM sector has seen a flurry of activity, with a global CGM race already underway.

In March, Dexcom launched two key products—the G7 CGM system and the Stelo over-the-counter CGM device—with the former targeting the professional medical market and the latter aimed at general consumers.

In June, Abbott announced that its two over-the-counter CGM products, Lingo and Libre Rio, had received FDA approval. Lingo is targeted at non-diabetic individuals aged 18 and older who seek to improve their metabolic health, while Libre Rio is specifically designed for patients with type 2 diabetes aged 18 and older who do not use insulin.

In July, Roche announced that its first CGM product, the Accu-Chek SmartGuide CGM solution, had received CE certification, marking Roche’s official entry into the CGM market.

In August, Medtronic announced that its new CGM product, Simplera, received approval from the U.S. FDA.

In August, Abbott and Medtronic partnered to develop an integrated CGM that connects with Medtronic’s automated insulin delivery (AID) system and smart insulin pen systems.

As can be seen, industry leaders are continuously increasing their investments in the CGM market this year. For all participants, the intensity of competition has escalated, even in the Chinese domestic market. With the mass launch of domestically produced CGMs, competition is becoming increasingly fierce, making price and cost control key factors for companies competing in this arena.

As CGMs are targeted at consumer-end users and possess certain stockpiling characteristics, they have become a staple in major e-commerce promotional campaigns. Manufacturers including MicroTech Medical, Sinocare, Silicon Based Bionics, and Yuwell have actively participated. According to the “618” Consumer Insights Report (2024) released by China News Service Jingwei Institute, sales of blood glucose meters increased by over 40%.

Some industry insiders also believe that current market competition is largely a battle for existing market share, with insufficient development of new market segments and no truly “breakout” product emerging. Although products like Eversense are not yet fully mature, the advent of diverse product forms—such as the non-invasive glucose monitor previously approved from Jingce Medical—has injected innovative vitality into the industry through their participation.

For instance, in the domestic CGM market, beyond price competition, we are seeing companies like MicroTech Medical with its AiDEX X and Ottai with its M8 striving to make their products thinner and lighter, thereby enhancing user comfort by making them less perceptible. For patients with diabetes, the ultimate goal of technological pathways and product forms is to simplify the blood glucose monitoring process and make glucose management easier. We look forward to the emergence of more technological approaches and superior product designs that will give rise to breakthrough products capable of reaching a broader audience.