Sichuan Shuangma Acquires 92.17% Stake in Shenzhen Jianyuan for RMB 1.596 Billion at 184.50% Premium, Entering GLP-1 Peptide Drug Market

On the evening of October 21, Sichuan Shuangma announced its intention to use proprietary and self-raised funds to acquire a 92.1745% equity stake in Shenzhen JYMed Technology Co., Ltd. from Xingyin Pharmaceutical and Xingyin Group at a total transaction price of RMB 1.596 billion.As of the valuation reference date of June 30, 2024, the premium rate on the transaction consideration for this deal was 184.50%.

On October 22, Sichuan Shuangma opened at the daily price limit up, and hit the limit multiple times during intraday trading on the 23rd. As of the market close on the 23rd, Sichuan Shuangma’s total market capitalization reached RMB 14.05 billion.

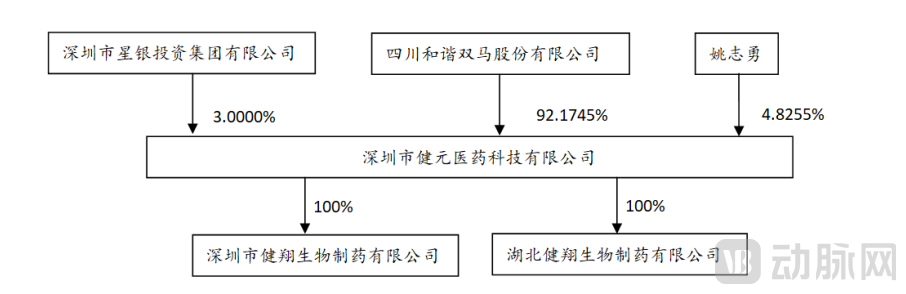

Specifically, Sichuan Shuangma intends to acquire a 78.5458% equity interest in Shenzhen JYMed Technology Co., Ltd. held by Xingyin Pharmaceutical for RMB 1,360,380,865.98, and a 13.6287% equity interest in Shenzhen JYMed Technology Co., Ltd. held by Xingyin Group for RMB 236,043,463.92. Upon completion of the transaction, Sichuan Shuangma will hold a 92.1745% equity interest in Shenzhen JYMed Technology Co., Ltd., Xingyin Group will hold a 3.0000% equity interest, and the individual Yao Zhiyong will hold a 4.8255% equity interest. After the implementation of this transaction, Shenzhen JYMed Technology Co., Ltd. will become a controlling subsidiary included in the Company’s consolidated financial statements.

(Equity Structure Diagram of JYMed After the Transaction)

The announcement stated that, upon completion of the transaction, Sichuan Shuangma will seize growth opportunities in the biopharmaceutical industry, integrate biopharmaceutical operations into its business segments, optimize asset allocation, enhance the profitability and market competitiveness of its assets, and comprehensively improve the company’s sustainable development capabilities.

Sichuan Shuangma, fully named “Sichuan Harmony Shuangma Co., Ltd.” and formerly known as “Sichuan Shuangma Cement Co., Ltd.,” traces its roots to the Jiangyou Cement Plant established in 1956, one of the 156 key construction projects during China’s First Five-Year Plan. The company’s core business encompasses the production and sales of cement products and construction aggregates. It was listed on the Main Board of the Shenzhen Stock Exchange in August 1999.

Since 2016, Sichuan Shuangma has undergone a transformation and upgrading of its assets and business operations. In that year, partners affiliated with IDG Capital acquired a 50.93% stake in the company through an investment entity, thereby gaining controlling interest in Sichuan Shuangma and initiating the expansion of IDG Capital’s long-term strategic layout and industrial influence.In 2018, Beijing Hexie Hengyuan Technology Co., Ltd. (“Hexie Hengyuan”), the controlling shareholder of Sichuan Shuangma, entered into an “Acting-in-Concert Agreement” with Gold Booster Limited. Following the execution of the agreement, Hexie Hengyuan controlled 69.07% of the equity interest in Sichuan Shuangma, with the ultimate actual controller being partners affiliated with IDG Capital.

Therefore, starting in 2016, Sichuan Shuangma gradually explored business opportunities in the private equity investment sector. According to information on its official website, Tibet Jinhe Venture Capital Management Co., Ltd., a subsidiary of Sichuan Shuangma,The current assets under management (AUM) exceed RMB 22 billion.including the “Hexie Jinyu Industrial Fund” registered in Henan Province (Zhengzhou City), the “Hexie Jinhong Fund” in Yiwu City, and the “Hexie Green Industrial Fund” in Yibin City. The investment directions of the three funds includeInternet, cross-border e-commerce logistics, new energy, intelligent manufacturing, semiconductors, etc.

Based on Sichuan Shuangma’s performance reports from the past three years, the compound annual growth rate (CAGR) of its total operating revenue was negative, although the overall decline was modest. Total operating revenue stood at RMB 1.224 billion in 2021, RMB 1.220 billion in 2022, and RMB 1.219 billion in 2023. However, revenue across different business segments exhibited significant fluctuations in 2023.In terms of private equity investment fund management business, good results were achieved in 2023, thereby driving the growth of overall net profit—the net profit attributable to shareholders of the listed company was RMB 910 million to RMB 1.03 billion, representing a year-on-year increase of 10.24% to 24.78%, with basic earnings per share expected to be RMB 1.2 to RMB 1.35.

Based on the data, in 2022, the cement industry generated revenue of RMB 728 million, accounting for 59.72% of total operating revenue; private equity fund management revenue amounted to RMB 273 million, representing 22.39% of total operating revenue; and aggregate revenue reached RMB 218 million, constituting 17.88% of total operating revenue. In 2023, cement revenue declined by 20.97% year-on-year to RMB 576 million, accounting for 47.21% of total operating revenue;Private equity fund management income reached RMB 466 million, a year-on-year increase of 70.52%, accounting for 38.19% of operating revenue;Aggregate revenue reached RMB 178 million, a year-on-year decrease of 18.37%, accounting for 14.60% of total operating revenue.

Specifically, Sichuan Shuangma has made significant progress in its private equity fund business, continuously attracting new limited partners (LPs), including Guangzhou Industrial Investment New Energy Special Fund of Funds Partnership (Limited Partnership), Jiangxi State-owned Capital Operation Holding Group Co., Ltd., Shenzhen Century Kaihua Investment Fund Co., Ltd., Futaihua Industry (Shenzhen) Co., Ltd., and Manulife-Sinochem Life Insurance. The registered size of the “Harmony Green Industry Fund” has surged to RMB 9.3 billion.

In addition, in January this year, Tianjin Saikehuan Enterprise Management Center (Limited Partnership), a party acting in concert with the controlling shareholder of Sichuan Shuangma and a shareholder holding more than 5% of the shares, signed share transfer agreements respectively with CITIC Financial Asset Management Co., Ltd. and Zhongrong Life Insurance Co., Ltd. regarding Sichuan Shuangma, thereby changing its indirect holdings in Sichuan Shuangma through Tianjin Saikehuan to direct holdings. The total consideration for the share transfer to CITIC Financial Asset Management Co., Ltd. amounted to approximately RMBRMB 889 million; the total transfer price for Zhongrong Life Insurance shares amounts to762 millionYuan。Upon completion of the transfer, CITIC Financial Asset Management and Zhongrong Life Insurance became the registered shareholders of Sichuan Shuangma.

On one hand, the performance of private equity funds has shown a trend of continuous growth; on the other hand, the support from multiple limited partners (LPs) reflects their long-term optimism about Sichuan Shuangma’s investment direction in new energy and green industries. Moreover, IDG Capital and Sichuan Shuangma have ambitions beyond industrial transformation, turning their attention to the commercialization of scientific research achievements and innovative incubation.

In April this year, Sichuan Shuangma planned to use its own funds to establish a wholly-owned subsidiary, "Shanghai Hexie XinZhi Technology Development Co., Ltd.," in Xuhui District, Shanghai, with a registered capital of 500 million yuan (subject to the approval and registration by the market supervision and administration department). This subsidiary willFocusing on industrial directions driven by technological innovation, we prioritize investments in fields such as biomedicine, artificial intelligence, and industrial technology, adopting a systematic and platform-based model for startup incubation.Promote the commercialization of scientific and technological achievements, identify and cultivate high-tech enterprises with significant growth potential, strong comprehensive benefits, and leading driving effects... Meanwhile, continuously enhance the company’s profitability and strategically position its industrial direction for future business transformation.

Deeply engaging in industries characterized by high technical barriers and a concentration of scientific research and innovation may well be the rationale behind Sichuan Shuangma’s significant acquisition of Sichuan Jianyuan.

Peptide-based therapeutics cover a wide range of indications, including diabetes, oncology, osteoporosis, chronic pain management, endocrine disorders, multiple sclerosis, anti-infective treatments, and irritable bowel syndrome. Blockbuster products in the peptide sector include insulin, growth hormone, semaglutide, glatiramer acetate, and oxytocin, as well as currently highly popular weight-loss drugs such as semaglutide, tirzepatide, and liraglutide.

Shenzhen JYMed Technology Co., Ltd. (Shenzhen JYMed), established in 2009, is a biopharmaceutical enterprise integrating independent R&D, manufacturing, sales, and customized R&D and manufacturing of peptide products. Its core businesses include the R&D and manufacturing of peptide active pharmaceutical ingredients (APIs), contract development and manufacturing organization (CDMO) services for peptides, and the R&D and manufacturing of cosmetic peptides, with its products widely applied in the pharmaceutical and cosmetics industries.

The announcement pointed out that Shenzhen JYMed Technology Co., Ltd. is a domestic enterprise with scale advantages in peptide active pharmaceutical ingredients (APIs). It currently has established an R&D center, a new drug development and research platform, as well as two major production bases: Hubei Jianxiang and Shenzhen Jianxiang.The total production capacity of chemically synthesized peptides has now reached the scale of several tons, ranking among the top in the industry.Benefiting from the rapid growth of GLP-1 receptor-targeting peptide drugs in the global market, overall operating revenue has increased significantly in recent years, with major revenue streams distributed across the United States, Europe, and China.

Currently, the revenue of Shenzhen JYMed Technology Co., Ltd. is primarily derived from its peptide active pharmaceutical ingredient (API) business.Peptide-based active pharmaceutical ingredient (API) products mainly include more than 20 varieties, such as semaglutide, tirzepatide, liraglutide, degarelix, and oxytocin.Among them, five varieties, including semaglutide and tirzepatide, have completed the U.S. FDA DMF (Drug Master Files) filing.The CDMO business encompasses project-based contracted R&D, contracted manufacturing, and the sale of custom peptides. Its primary clients include innovative pharmaceutical companies and research institutions. Notably, some pharmaceutical enterprises have partnered with Shenzhen JYMed since the product development phase, establishing stable collaborative relationships, with Shenzhen JYMed expected to become their main supplier upon future drug commercialization. The cosmetic peptide business focuses on the production of raw materials for cosmetics, with key products including copper peptides, acetyl hexapeptide, conotoxin peptides, and blended cosmetic peptide formulations. These products, designed for anti-aging and anti-wrinkle applications, are primarily supplied to leading global cosmetics companies.

Shenzhen JYMed Technology Co., Ltd. has been deeply engaged in the peptide field for many years, establishing a comprehensive R&D system that includes platforms for complex peptide and peptidomimetic chemical synthesis and modification, peptide fragment design and synthesis, purification using multiple separation techniques, and drug sustained- and controlled-release formulation development. The R&D Center primarily undertakes full-process research on innovative drugs and generics, with a focus on synthetic peptide therapeutics, covering project initiation, evaluation and screening, process design and development, quality studies, preclinical pharmaceutical evaluations, and clinical trial applications. Its core R&D team boasts over 20 years of experience in peptide drug development, underpinned by profound professional expertise and extensive practical knowledge.

In the long term, domestic demand for peptide drugs and active pharmaceutical ingredients (APIs) may usher in a new surge, driven by the expiration of originator drug patents, the entry of domestically produced generic drugs, and the emergence of blockbuster innovative therapies such as peptide-drug conjugates.Semaglutide’s domestic patent in China is set to expire in 2026. Numerous Chinese generic drug manufacturers have already made strategic arrangements, which will further stimulate production order demand, and the imbalance between supply and demand is expected to persist. According to Frost & Sullivan data, the global market size for peptide-based drugs, measured by sales revenue, is projected to reach $261.2 billion by 2032, while the Chinese market for peptide-based drugs is anticipated to attain RMB 251.2 billion.

On the global market, the rivalry between Novo Nordisk and Eli Lilly has expanded worldwide. Peptide CDMOs are primarily establishing their own facilities or forming partnerships in Europe and the United States, while simultaneously accelerating the expansion of global production capacity and gradually increasing investment in manufacturing capabilities at their Chinese plants. Since last year, Novo Nordisk has invested over RMB 5 billion to bolster the expansion of its Chinese manufacturing facilities; in October, Eli Lilly invested RMB 1.5 billion to upgrade the production capacity of its Suzhou plant, thereby scaling up the manufacturing of tirzepatide.

Even conservatively speaking, given unknown systemic risks and supply chain security concerns, China’s peptide active pharmaceutical ingredient (API) supply and contract development and manufacturing organizations (CDMOs) have not yet fully penetrated the global market, but still maintain significant cost and industrial chain advantages. As originator drugs gain approval for weight-loss indications and domestically produced generics receive regulatory approval, the cost advantage of China’s peptide APIs will become more apparent, further expanding capacity markets both domestically and internationally.

A vast market lies ahead, but securing a foothold in peptide manufacturing and CDMO—sectors characterized by high technological barriers—is no easy feat.In China, the companies capable of establishing peptide manufacturing capacity and handling a wide variety of end products are primarily those that have expanded from peptide active pharmaceutical ingredient (API) production to peptide contract development and manufacturing organization (CDMO) services (such as Shenzhen JYMed Technology Co., Ltd.), as well as small-molecule CDMO enterprises with strong existing capabilities, and a very small number of companies specializing exclusively in peptide CDMO.

For pharmaceutical companies involved in peptide drugs, the early-stage investment for peptide production is high and time-consuming, with few companies able to develop independently without relying on CDMOs. Compared to small-molecule drugs, peptide drugs have more complex structures, intricate combinatorial peptide synthesis methods, and numerous considerations. Additionally, impurity generation during synthesis is complex and diverse, making purification particularly challenging.

Controlling peptide impurities throughout the entire manufacturing process presents a significant challenge. Unlike small-molecule drugs, which can achieve purity levels of 98.5% or even 99%, achieving a purity of 93–94% for peptides is already considered excellent. The wide variety of impurities makes the establishment of quality standards highly complex. Typically, in innovative small-molecule pharmaceutical companies, the ratio of personnel engaged in process development to those in analytical development is 1:1. However, due to the substantial analytical challenges associated with peptides, this ratio needs to be expanded to 1:2 or even 1:3.

Furthermore, there are significant barriers to scaling up and achieving large-scale production of peptide manufacturing processes. During the synthesis of peptide drugs, a wide variety of protecting agents are required. The selection and use of these protecting agents have become a key focus of environmental organizations. Continued reliance on traditional solvents poses substantial challenges, necessitating the exploration of novel protecting agents as alternatives.

The flip side of high barriers is high returns and more stable upstream and downstream relationships within the industry chain.Peptide drug developers require CDMOs to provide sample synthesis during the preclinical research phase, and later rely even more heavily on CDMOs’ industrialization expertise in process development and quality control for new drug launches. Consequently, peptide pharmaceutical companies exhibit a stronger dependence on such services. Given the complex production processes and significant quality control challenges associated with peptides, it is typically necessary to complete the entire manufacturing process—from starting materials to active pharmaceutical ingredients (APIs)—within a single enterprise, as handoffs at intermediate stages are difficult. This results in a high demand for integrated solutions.

According to Frost & Sullivan, the market size of China’s peptide CDMO industry reached RMB 3.8 billion in 2023 and is projected to further increase to RMB 30.7 billion by 2032, representing a compound annual growth rate (CAGR) of 25.9%. By then, China’s global market share in the peptide CDMO sector is expected to reach approximately 22%, up from only around 5% in 2020.

References:

VCBeat: “China’s Peptide CDMOs: Becoming Increasingly Competitive?”

Institutional Investors Comment on “Sichuan Shuangma, Now Controlled by IDG Capital, to Establish a Technology Development Company”

Cailian Cloud: "Sichuan Shuangma - Financial Analysis and Long-Term Investment Value"

Chenxiao M&A: “Sichuan Shuangma’s RMB 1.596 Billion Cross-Industry Acquisition of Shenzhen JYMed, a Leading Peptide API Manufacturer: Is IDG Capital Behind the Deal?”