Rebuilding a RMB 50 Billion Biotech: How a Traditional Pharma Successfully Pivoted to Innovation

CSPC

Innovative Drug Research and Development, Manufacturer

CSPC Innovation

Biopharmaceutical, API, and Functional Food Developer

Recently, Xinovate, an A-share listed company, finalized its restructuring plan to acquire 100% equity interest in CSPC Baicell Biologics for RMB 7.6 billion, with 10% paid in cash and the remainder through the issuance of new shares.

Although it was merely a routine restructuring, over the past year, CSPC Innovation has successively integrated Julishi Biopharma and CSPC Baike, even changing its name to “CSPC Innovation Pharmaceutical.” During this same period, the market capitalization of CSPC Innovation surged approximately threefold, approaching RMB 50 billion. It now ranks among the top biopharmaceutical companies on the ChiNext board, with its valuation closing in on that of its parent company, CSPC, which stands at RMB 70 billion.

Back in mid-September, CSPC Pharmaceutical Group Limited announced a substantial HK$5 billion share repurchase program on the Hong Kong stock market over two years, instantly topping the list of domestic listed pharmaceutical companies by repurchase amount. At current market valuations, HK$5 billion could acquire five or six already-listed biotech firms in the Hong Kong market. Yet CSPC chose to repurchase and cancel its own shares. Perhaps, as stated in the announcement:

I. Confident in business development; II. Stock price is too low.

What underpins CSPC’s strong confidence is, of course, its successful transformation in innovative drugs in recent years.

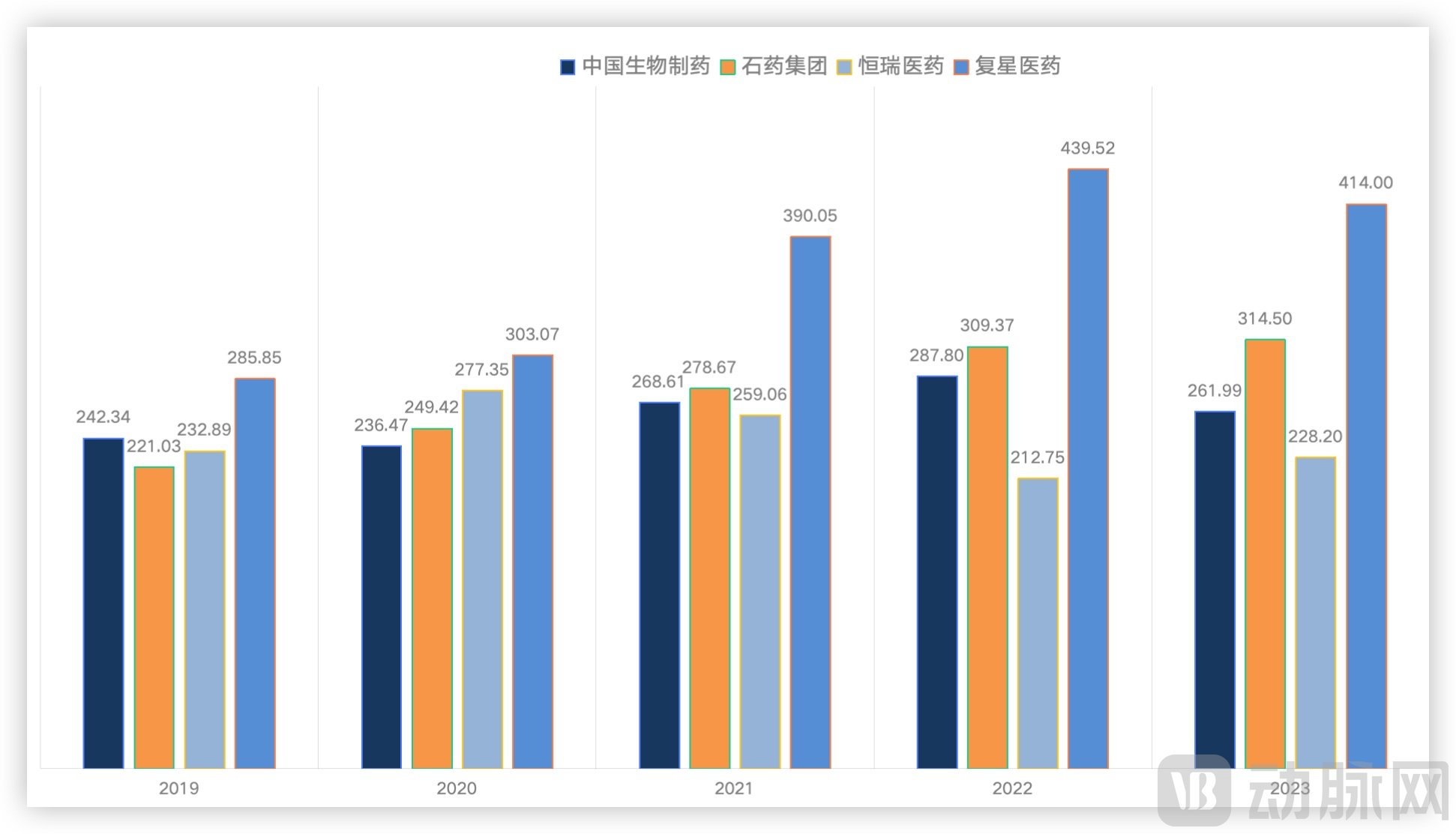

In terms of revenue alone, CSPC ranks among the top pharmaceutical companies in China, providing the financial foundation necessary for its transformation.

Based on revenue data from the past five years, CSPC’s overall revenue performance has been highly stable, demonstrating a steady upward trend. In terms of revenue structure, CSPC has intentionally reduced the proportion of its active pharmaceutical ingredient (API) business in recent years, focusing instead on expanding its finished drug segment. By 2023, revenue from finished drugs had reached RMB 25.6 billion; in the first half of 2024, this figure stood at RMB 13.55 billion, representing a year-on-year increase of nearly 5 percentage points and accounting for approximately 83% of total revenue. When combined with revenues from APIs, functional foods, and other businesses, CSPC’s overall performance is comparable to that of established pharmaceutical companies such as Hengrui Medicine and Chia Tai Tianqing, placing it firmly within the top tier of China’s pharmaceutical industry.

CSPC's Revenue Performance Over the Past Five Years, Based on Corporate Financial Reports

CSPC's currently marketed drugs are primarily concentrated in the central nervous system and oncology sectors.

The CNS business generated RMB 5.236 billion in revenue in H1 2024, while the oncology segment recorded RMB 2.683 billion, accounting for 38.6% and 19.8% of total finished drug revenue, respectively. The core blockbuster product, NBP (butylphthalide soft capsules and butylphthalide sodium chloride injection), is a Class 1 new drug indicated for stroke. The soft capsule formulation was approved for market launch in 2005, followed by the injection in 2010. From 2020 to 2023, annual sales of butylphthalide consistently exceeded RMB 6 billion.

In the oncology field, the main products include Jinyouli, DuoenDa, and Jinlitai. Among them, Jinyouli is the first domestically developed long-acting granulocyte colony-stimulating factor (G-CSF) drug in China, classified as a Class 1 new biological therapeutic agent, used for the prevention and treatment of infections and fever caused by neutropenia in patients undergoing chemotherapy. DuoenDa is the world’s first marketed liposomal mitoxantrone. Jinlitai is the first IgG4 RANKL inhibitor, indicated for adult patients with giant cell tumor of bone that is unresectable or where surgical resection would likely result in severe functional impairment; it was approved by the National Medical Products Administration (NMPA) in September 2023.

Revenue Composition of CSPC's Finished Drug Business, Data Sourced from Corporate Financial Reports

It is precisely the stable revenue that underpins CSPC’s strategic transformation. In recent years, CSPC Pharmaceutical Group has continuously increased its investment in innovative drug R&D. In the first half of 2024, R&D expenditures reached RMB 2.542 billion, accounting for 15.6% of total revenue. From 2019 to June 2024, cumulative R&D investment amounted to nearly RMB 20 billion.

Since then, CSPC has been accelerating its transformation in the innovative drug sector through a series of strategic moves, including the restructuring of Sinopharm, share buybacks, and the recruitment of high-end talent.

With CSPC’s series of strategic moves, Xinnoway is now on par with any domestic biotech company.

Established in 2006, Xinnoway was formerly a subsidiary under the health and wellness segment of CSPC Pharmaceutical Group Limited (CSPC). It was spun off and listed in 2019, becoming CSPC’s listing platform on the A-share market. Through resource integration, CSPC has successively injected its innovative drug assets into the company, positioning it as the group’s platform for innovative drug operations.

As a major global producer of chemically synthesized caffeine, Xinnowell supplies raw materials to well-known beverage companies such as PepsiCo, Coca-Cola, and Red Bull. Although its acquisition of CSPC Shengxue, a subsidiary of CSPC Pharmaceutical Group, enabled it to obtain the active pharmaceutical ingredient (API) for acarbose and related anhydrous glucose businesses, this move was viewed merely as an expansion of its existing operations and failed to generate significant ripples in the capital markets.

A turning point emerged in the second half of 2023, when Xinnuowei announced a plan to inject RMB 1.871 billion in cash into CSPC’s subsidiary, Jushi Biologics, to acquire a 51% equity stake and gain controlling interest. Jushi Biologics primarily focuses on the research and development of antibody-based drugs, antibody-drug conjugates (ADCs), and mRNA vaccines, serving as one of CSPC’s key platforms for innovative drug development. Its product, “DuenTai,” is the first domestically approved mRNA vaccine targeting COVID-19.

Xinnuowei has also leveraged this acquisition to successfully transition from a functional food company into an innovative pharmaceutical enterprise.

By January 2024, after completing the transfer of equity in Jushi Biologics, Xinuowei announced its continued acquisition of CSPC Baike, a subsidiary under CSPC Pharmaceutical Group. However, the transaction was delayed for nine months, with the detailed plan only being disclosed in mid-October. According to the company’s announcement, Xinuowei will acquire 100% of the equity in CSPC Baike, collectively held by Weisheng Pharmaceutical, CSPC Shanghai, and Enbipu Pharmaceutical, for a total consideration of up to RMB 7.6 billion.

As an innovative pharmaceutical company with exclusive commercialized products, CSPC Baike contributes approximately RMB 2 billion in stable cash flow to CSPC annually, reflecting its substantial asset base. As of June 30, 2024, CSPC Baike’s cash and cash equivalents amounted to approximately RMB 1.386 billion, with total assets reaching around RMB 4.591 billion.

This marks the second time CSPC has reallocated its innovative drug assets, following the earlier move involving Jushi Biologics, signaling a further step in CSPC’s innovation-driven transformation.

From the perspectives of both innovation capability and future product potential, Xinuowei will ascend to a higher level following its secondary merger and acquisition.

In 2023, CSPC Baike achieved revenue of RMB 2.32 billion and net profit of approximately RMB 780 million; in the first half of 2024 (2024H1), it recorded revenue of approximately RMB 920 million and net profit of approximately RMB 390 million. The primary driver of its revenue is JinYouLi, a long-acting granulocyte colony-stimulating factor (G-CSF) formulation. In 2023, JinYouLi generated sales of approximately RMB 2.25 billion.

In the announced transaction plan, CSPC Baike committed that if the equity closing is completed by December 31, 2024, its net profits for the three-year period from 2024 to 2026 shall be no less than RMB 435 million, RMB 393 million, and RMB 436 million, respectively; if the equity closing occurs after this date, it commits that its net profits for the three-year period from 2025 to 2027 shall be no less than RMB 393 million, RMB 436 million, and RMB 502 million, respectively.

Not only in terms of revenue, but Baike Biologics’ robust product pipeline also serves as a strong complement to Xinnuowei. Through the acquisition, Xinnuowei has expanded its product portfolio into areas such as weight loss, muscle building, and blood glucose reduction, and has established a long-acting protein platform.

Taking the currently popular GLP-1 as an example, TG103 injection (an innovative long-acting recombinant human GLP-1 Fc fusion protein) and semaglutide injection (a long-acting GLP-1 analog) are undergoing Phase III clinical trials for indications of overweight/obesity and type 2 diabetes, with expected approval and market launch in 2026. In addition, Baike has also laid out a pipeline that includes a long-acting semaglutide injection (fluid crystal formulation), oral small-molecule GLP-1 tablets, as well as dual-target and triple-target products. Leveraging its platform-based long-acting technology, the company is further developing related products in the field of chronic disease treatment.

Of course, mergers and acquisitions are merely the first step; thorough digestion and integration require considerable effort. From the newly released financial report of CSPC Innovation, we can also observe the impact brought about by the acquisition of Jushi Biologics.

According to the third-quarter report of CSPC Innovation (formerly known as Xinnuowei), the company achieved revenue of RMB 1.479 billion in the first three quarters, a year-on-year decrease of 23.66%; net profit attributable to shareholders of the parent company was RMB 139 million, a year-on-year decrease of 63.50%. The decline in performance is mainly attributed to two factors: first, the drop in prices of products from its original core business; second, the significant increase in R&D expenses following its transition into innovative drugs.

From Q1 to Q3 2024, Julshi Biosciences, in which Xinuo Wei holds a 51% stake, incurred R&D expenses of RMB 404 million; among this, the R&D expenses for the third quarter amounted to RMB 186 million, representing a year-on-year increase of 48.40% and a quarter-on-quarter increase of 56.64%. The full-year R&D investment of Julshi Biosciences is expected to approach RMB 600 million, with the impact on consolidated expenses after inclusion by Xinuo Wei amounting to approximately RMB 300 million.

Of course, the impact is only temporary, and Jushi Biopharma may see revenue growth in the fourth quarter.

In Julistone Biopharma’s product pipeline, the PD-1 inhibitor enlanucimab and omalizumab were approved in June and October of this year, respectively, and are expected to contribute to revenue in the fourth quarter. As planned, ustekinumab and a HER2-targeting antibody-drug conjugate (ADC) are also poised for launch and commercialization next year, which will propel Julistone Biopharma into a self-sustaining phase characterized by revenue growth driving a narrowing of losses. Furthermore, Julistone Biopharma submitted five investigational new drug (IND) applications this year, with partial approvals anticipated within the year. According to its pipeline roadmap, the company aims to advance new drug development at a pace of 2–3 IND approvals annually.

Several promising projects are also progressing smoothly. For instance, clinical data for the EGFR ADC product SYS6010 is expected to be released in the first half of 2025, while a Phase III clinical trial for its combination regimen with osimertinib is set to commence. During the earnings conference call, the company disclosed that it is actively negotiating licensing collaborations with two major international pharmaceutical companies for its EGFR ADC, and further progress in these partnerships is anticipated as more data becomes available.

Previously, Jushi Biologics entered into an exclusive licensing agreement with Corbus Pharmaceuticals for the development and commercialization of SYS6002, a recombinant humanized anti-Nectin-4 antibody-drug conjugate (ADC), in the United States and other countries, with potential deal values reaching up to $693 million. CSPC also licensed the global rights outside Greater China for SYSA1801, a novel Claudin18.2 ADC, to Elevation Oncology for RMB 1.195 billion. Both products remain subject to potential future milestone payments, indicating that Shinobiopharm (Xinnuowei) still has potential revenue streams ahead.

In other words, CSPC has injected many of its own preclinical pipelines, as well as those of Jushi Biologics and CSPC Bio-Pharm, into Xinnoway. This includes strategic layouts in hotspots such as CLDN18.2, Nectin4, EGFR ADCs, and TCEs. Currently, Xinnoway is no less competitive than any domestic biotech company.

"One step behind, always behind": This has been the impression CSPC has given in recent years.

In fact, as early as 2020, CSPC had expressed interest in listing on the STAR Market, aiming to become another Hong Kong-listed pharmaceutical company to adopt the “A+H” model on the STAR Market following Junshi Biosciences. At the time, CSPC stated that its consideration of a STAR Market listing was driven by the goal of leveraging financial instruments to further tap into the innovative high-tech capital market after completing its “Hong Kong shares + A-shares” capital structure, thereby fostering high-quality development.

At that time, CSPC was navigating a difficult phase in its innovation-driven transformation. To avoid potential conflicts with its self-developed anti-PD-1 monoclonal antibody in clinical trials and future commercialization, the company decided to terminate its collaboration with Junshi Biosciences and paid milestone payments to Junshi as stipulated in the cooperation agreement. Subsequently, issues also arose in its partnership with SinoCellTech.

In such a macro environment, CSPC urgently needed to broaden its financing channels. As this path ultimately proved unviable, Xinnuowei, which had previously listed on the A-share market, became the vehicle for CSPC Group’s earnest aspirations to accelerate its innovation-driven transformation.

Market analysts suggest that had CSPC spun off several innovative drugs and part of its pipeline from its subsidiaries and injected them into Xinnuowei for an IPO at the time of its listing, rather than focusing primarily on the R&D, production, and sales of functional foods in the general health sector, Xinnuowei would have had a strong chance of reaching a market capitalization of RMB 100 billion given the market environment then. Although Xinnuowei remains highly promising thanks to CSPC’s adept strategic maneuvering, the landscape has shifted significantly. As market conditions are now markedly different, the company faces considerable challenges in further expanding its market valuation.

CSPC may have also recognized the crisis, as evidenced by its frequent recent personnel changes aimed at supporting its overall innovation-driven transformation strategy.

In early September, CSPC issued an announcement appointing Dr. Liu Yongjun as Executive President and President of Global R&D of CSPC Pharmaceutical Group Limited. He will be responsible for the group’s R&D, pipeline strategy, and the development of international business. Dr. Liu previously held senior R&D executive positions at Schering-Plough and AstraZeneca, and later served as Head of Global Research at Sanofi. Prior to joining CSPC, he was in charge of global R&D, pipeline strategy, business collaborations, and international operations at Innovent Biologics.

In late September, CSPC Innovation appointed Yao Bing as the new Chairman of the Board and stated externally: “Chairman Yao Bing has extensive experience in innovative drugs. The company’s future focus will be on innovative pharmaceuticals, making Mr. Yao’s background more aligned with the company’s development strategy.” The move clearly demonstrates a commitment to rejuvenating the management team and continuing its innovation-driven transformation.

Currently, Xinnuowei’s market capitalization on the A-share market has approached RMB 50 billion, while CSPC’s total market capitalization on the Hong Kong stock market stands at just over RMB 70 billion. CSPC has not only retained its controlling stake in Xinnuowei but also gained an additional financing channel, with the asset valuation significantly higher than before. This will undoubtedly provide greater support for CSPC’s future development.

To some extent, CSPC’s strategic transformation of Xinnuowei represents an unconventional case of a pharmaceutical company pursuing dual “A+H” listing.

Following CSPC, China Biopharmaceutical has also preliminarily completed its “A+H” listing structure. Is Hengrui next in line?

On the evening of October 30, China Biopharmaceutical Holdings Limited announced via a filing with the Hong Kong Stock Exchange that it would acquire up to a 55% stake in Jiangsu Haoyu Biomedical Co., Ltd., a company listed on the STAR Market, through negotiated transfer and tender offer. Upon completion of the acquisition, Haoyu will become a listed subsidiary of China Biopharmaceutical Holdings in the A-share market. This transaction also represents a rare case of a pharmaceutical company acquiring an in vitro diagnostics (IVD) device manufacturer.

It is worth noting that with Sinopharm’s acquisition of CSPC Baike, rumors of Hengrui Medicine listing on the Hong Kong Stock Exchange, and China Sino Biopharmaceutical’s recent acquisition, the three established pharmaceutical giants undergoing domestic transformation appear to have coordinated their moves to establish “A+H” share structures. What does this trend signify for the industry?

In recent years, although China Biopharm has maintained its revenue with the support of its subsidiaries, Chia Tai Tianqing and Sinovac, it is still seeking a second growth curve. For instance, Chia Tai Tianqing’s extensive portfolio in the autoimmune field represents a key focus of its innovative development. Meanwhile, Hybribio specializes in the research and development of diagnostic reagents for allergic and autoimmune diseases. The integration of their businesses can connect multiple stages in the autoimmune sector, from diagnosis to drug R&D, thereby enabling full-lifecycle services and achieving a synergistic effect where 1+1>2. Additionally, Hybribio’s desensitization drugs can also be empowered by China Biopharm’s resources.

Like CSPC, China Biologic Pharmaceuticals had as early as 2021 sought to list on the STAR Market to achieve an “A+H” dual-listing status, but the plan did not materialize at that time. In light of previous developments, whether China Biologic Pharmaceuticals will now pursue a back-door listing on the A-share market has sparked market speculation.

Meanwhile, Hengrui, another established pharmaceutical company, may be considering a secondary listing in Hong Kong. Not long ago, market rumors suggested that Hengrui was contemplating an IPO on the Hong Kong Stock Exchange, aiming to raise approximately $2 billion. In its announcement, Hengrui neither denied nor confirmed these reports, stating only that it had conducted preliminary research and consultations regarding financing in overseas capital markets. If this trend continues, all three representative companies driving the innovative transformation of China's pharmaceutical industry will ultimately complete their "A+H" share structure listings.

The high profit margins in the medical aesthetics sector have also become a target for traditional pharmaceutical companies seeking cross-industry transformation.

In late October, Jiangsu Wuzhong released its third-quarter report for 2024. The company achieved an operating revenue of RMB 1.647 billion in the first three quarters, a year-on-year increase of 9.58%, while net profit attributable to shareholders surged by 311.54% year on year. The introduced “youthful face injection” AestheFill has become the second growth driver for its performance.

Data shows that in the first three quarters, Jiangsu Wuzhong’s medical aesthetics segment achieved cumulative main business revenue of RMB 198.7246 million, representing a staggering year-on-year increase of 4,175.12%; gross profit reached RMB 163.2956 million, with a year-on-year surge of 6,465.52%. In the preceding years, apart from a net profit of RMB 21 million in 2021, Jiangsu Wuzhong incurred cumulative losses exceeding RMB 650 million over the other three years.

This established pharmaceutical company, which successfully listed on the A-share market in the last century, previously focused primarily on generic drugs. Despite its considerable scale, its profitability remained low. In recent years, Jiangsu Wuzhong has adopted a dual-engine development strategy centered on “pharmaceuticals + medical aesthetics,” and in 2021, it secured the distribution rights for AestheFill, a “youth-restoring injection” product from the South Korean company Regen Biotech.

AestheFill received approval in January this year and was officially launched in April. In less than six months, it has been regarded as the product most likely to drive profitability for Jiangsu Wuzhong. In addition to poly-L-lactic acid (PLLA) fillers (“baby face” injections), Jiangsu Wuzhong is making in-depth strategic deployments across multiple sectors, including hyaluronic acid, collagen, lipolytic injections, and skin boosters (“infant needles”), with the aim of establishing a comprehensive portfolio of medical aesthetic products.

For established traditional pharmaceutical companies, the past decade has been a critical period for transitioning toward innovation. Legacy players such as CSPC, Sino Biopharmaceutical, and Hengrui Medicine have each carved out development paths suited to their own strengths in this innovative transformation. Although their specific trajectories are not easily replicable, leveraging their inherent advantages to garner greater attention from capital markets remains an essential consideration during this transition. For these established pharmaceutical enterprises, having completed the construction of financing channels, the next challenge lies in becoming globally competitive Big Pharma companies. The journey of innovative transformation is endless.