MNCs in China Shift Strategy: From Selling Drugs to Snapping Up Local Innovation Assets

With the CIIE schedule now halfway through, although the buzz is beginning to fade, the blockbuster products poised to transform the industry remain impressive.

For instance, BBM-H901 injection, making its global debut, is the first recombinant adeno-associated virus (AAV) gene therapy in China to have successfully submitted a New Drug Application (NDA). It holds the promise of ushering China’s hemophilia diagnosis and treatment into the era of gene therapy, thereby transforming the lifelong medication regimen for patients with hemophilia B. Additionally, the kidney disease portfolio, unveiled for the first time, includes iptacopan, a small-molecule complement factor B inhibitor, and atrasentan, an oral endothelin A receptor antagonist. As transformative therapies in the field of nephrology, they are highly likely to become the next blockbuster drugs.

Setting aside technology and market considerations, these two products also have impressive pedigrees.BBM-H901 injection is a cutting-edge product that Takeda licensed from BeiGene in October 2023.; the nephrology product portfolio originated from an acquisition by Novartis,In January 2024, Novartis officially acquired Chinook Therapeutics, thereby expanding its nephrology product portfolio in China.This means that both products are “Made in China.” In fact, there were many such “Made in China” products at this CIIE, with companies including Merck & Co., Sanofi, GlaxoSmithKline, and Roche Pharmaceuticals all involved.

And this may be just the beginning. During the China International Import Expo (CIIE), multinational corporations (MNCs) have nearly all expressed a strong willingness to intensify their “investment in China,” with related transactional collaborations currently underway. Coupled with the current fervor in business development (BD) and mergers and acquisitions (M&A) within the pharmaceutical industry, a new trend is becoming increasingly apparent:MNCs Are Shedding Their Sales-Driven Image and Accelerating Acquisitions of China’s Innovative Drugs。

“Cash-Sprinkling” BD: Nearly $50 Billion Splurged in Two Years

A key theme of the China International Import Expo (CIIE) is trade, and just one week before this year’s CIIE, two major deals drew widespread attention across the industry.

One deal is a major collaboration between Genentech, a member of the Roche Group, and Rigor Pharmaceuticals regarding next-generation CDK inhibitors. It is reported thatThe upfront payment for this deal alone reached $850 million, setting a new record for the highest upfront payment in the out-licensing of domestically developed molecular entities.. The other comes from AstraZeneca, regarding a preclinical innovative small-molecule lipoprotein(a) (Lp(a)) inhibitor YS2302018,Signed a blockbuster partnership deal worth over $2 billion with CSPC Pharmaceutical Group。

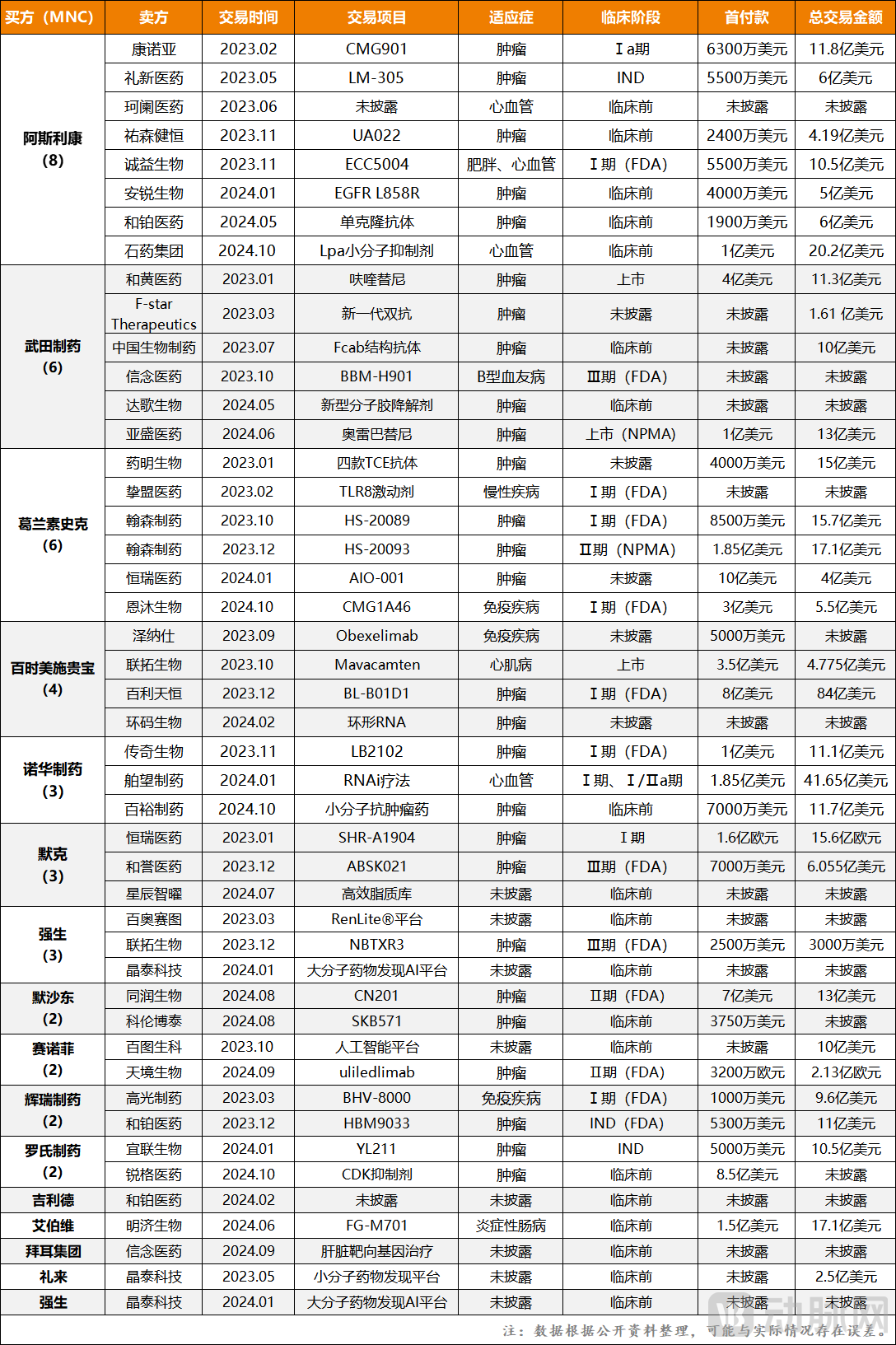

Figure 1. Selected BD Transactions Between MNCs and Chinese Assets, January 2023–October 2024

Figure 1. Selected BD Transactions Between MNCs and Chinese Assets, January 2023–October 2024

In fact, this is just the tip of the iceberg. If we extend the timeline, there are many more blockbuster deals and sky-high collaborations of this kind. According to incomplete statistics from VCBeat,From January 2023 to October 2024, business development (BD) deals between multinational corporations (MNCs) and innovative Chinese pharmaceutical companies exceeded 80, with the total transaction value approaching the $50 billion mark.. This stands out particularly against the current market winter, so what industry signals is it actually conveying?

First, multinational corporations (MNCs) are increasingly intensifying their investments in business development (BD), leading to more frequent transactions.. Starting in 2023, a wave of business development (BD) activities gradually swept through China’s pharmaceutical industry, leading to a direct outcome: for the first time in 2023, the total upfront payments secured by Chinese innovative drug companies through BD deals surpassed the total funds raised through initial public offerings (IPOs). Into 2024, this momentum has continued and intensified further. Throughout this process, multinational corporations (MNCs) have undoubtedly taken center stage. For example, GlaxoSmithKline alone engaged in two major collaborations with Hansoh Pharmaceutical in the field of antibody-drug conjugates (ADCs), involving a total amount of up to $3.3 billion. Additionally, Novartis acquired stakes in two Chinese biotech firms within just three days.

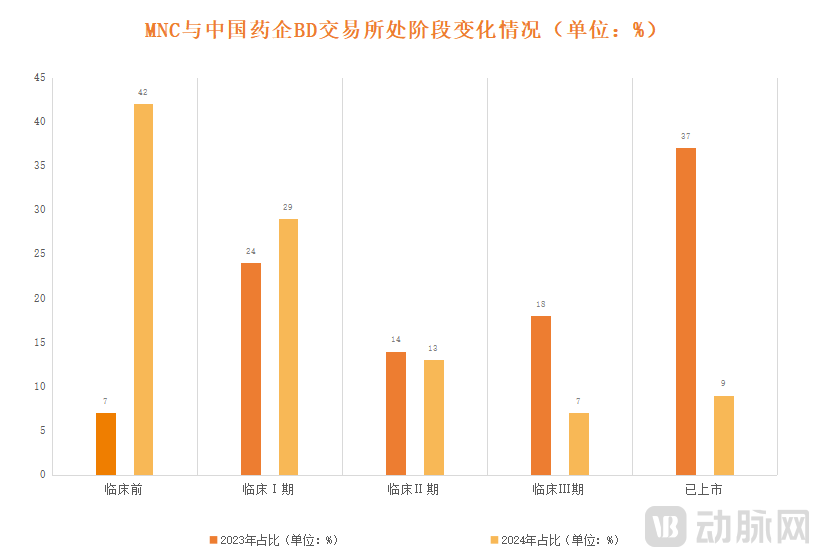

Figure 2. Changes in the Stages of BD Transactions Between MNCs and Chinese Pharmaceutical Companies

Figure 2. Changes in the Stages of BD Transactions Between MNCs and Chinese Pharmaceutical Companies

The second point is that transaction assets are gradually extending from the mid-to-late stages to the early stage.According to the "2023 BD Report on Chinese Pharmaceutical Companies" previously released by VCBeat, China’s business development (BD) deal assets in 2023 were primarily focused on Phase III clinical-stage and marketed products. However, this trend has shifted significantly in 2024. Among the nearly 40 BD transactions completed by multinational corporations (MNCs) this year, more than 80% involved assets in Phase I clinical trials or earlier stages. A typical example is the collaboration between Novartis and Bowang Pharmaceutical. Early this year, Novartis entered into a major partnership with Bowang Pharmaceutical for a Phase I clinical asset, with a deal value reaching up to $4.1 billion.

Figure 3. Top 10 Deals Between MNCs and Chinese Pharmaceutical Companies

Figure 3. Top 10 Deals Between MNCs and Chinese Pharmaceutical Companies

The final point focuses on disease areas.MNCs Leverage BD Not Only to Strengthen Their Pipelines, but Also to Focus on “China-Style” NeedsAn analysis of drug types involved in business development (BD) transactions between multinational corporations (MNCs) and Chinese pharmaceutical companies over the past one to two years reveals that antibody-drug conjugates (ADCs), large-molecule drugs, and small-molecule drugs remain the primary focus. Among these, ADCs are the most prominent, accounting for six of the top ten deals. This trend is driven by specific factors: oncology remains the central therapeutic area in BD transactions and a key component of MNCs’ competitive moats. Compared with traditional therapies, ADCs demonstrate superior efficacy and fewer side effects in cancer treatment, resulting in substantial market value and positioning them as a new growth engine for MNCs.

Beyond focusing on their own pipelines, multinational corporations (MNCs) are further honing in on local market demands through business development (BD). A case in point is Takeda’s in-licensing of BBM-H901 from Belief BioMed, which targets nearly 100,000 patients with hemophilia B in China. Additionally, AbbVie made a significant $1.7 billion investment to acquire the TL1A antibody FG-M701 from Mingji Biologics. This asset focuses on inflammatory bowel disease (IBD), a condition whose patient population in China is rapidly expanding and trending younger, making the market demand particularly pronounced.

Overall, for multinational corporations (MNCs), 2024 not only saw the continued momentum of the business development (BD) boom with increased capital investment, but also a more focused BD strategy that prioritized early-stage innovative projects. The underlying objective is clear: to engage more deeply in China’s healthcare innovation landscape and thereby unlock greater market opportunities. This strategic shift was clearly reflected in the launch of several blockbuster products and related collaborations unveiled at this year’s China International Import Expo (CIIE).

Strategic Shift: De-emphasizing Sales, Prioritizing Chinese-Style Innovation

In the 1980s and 1990s,MNCs began to flood into China in large numbers,Its primary objective is to leverage China’s market potential for sales.. This is because, at the time, China’s innovative drug development was relatively lagging behind; multinational corporations (MNCs) were able to rapidly dominate the Chinese market and secure substantial profits by leveraging their robust sales capabilities and multi-tiered distribution models.

However, as time has progressed, the competitive landscape for multinational corporations (MNCs) in the Chinese market has undergone significant changes: on one hand, China’s pharmaceutical industry is continuously maturing, with the gap between domestic pharmaceutical companies and MNCs narrowing considerably; on the other hand, market measures such as the “National Reimbursement Drug List + Volume-Based Procurement” have been progressively intensified, substantially increasing the competitive pressure on MNCs. This means that,The old sales-driven logic is no longer effective, and MNCs urgently need to identify new growth drivers by shifting their strategic direction.。

At this critical stage,BD is considered the most reasonable approach at present.This was further validated at this year’s China International Import Expo (CIIE), where multinational corporations (MNCs) not only launched more “Made-in-China” products but also actively sought to connect with a greater number of Chinese medical innovation assets. Keywords such as “Invest in China” and “localization” were repeatedly emphasized by MNCs.

So, what is the reason?

This must be examined from multiple dimensions.First, business development (BD) can alleviate the significant pressure that the patent cliff imposes on multinational corporations (MNCs).. As is well known, the patent cliff is virtually the most dreaded ordeal for multinational corporations (MNCs). According to statistics from BOCOM International, in the first year after a generic drug or biosimilar enters the market, sales of the originator drug decline by an average of 37%, and continue to drop by more than 60% in the second year. This means that a blockbuster drug with $1 billion in annual revenue will generate less than $300 million in the second year after patent expiry, representing a substantial financial loss.

To address this, multinational corporations (MNCs) have opted to proactively bridge the gap through business development (BD) activities. Taking the collaboration between Takeda and Ascentage Pharma as an example, the in-licensed olverembatinib not only serves as a successor to ponatinib, whose patent is set to expire in 2026, but also positions Takeda to compete with Novartis’s flagship product, asciminib, thereby safeguarding its industry standing in the third-generation tyrosine kinase inhibitor (TKI) segment. In fact, numerous similar transactions have taken place, with MNCs significantly advancing their strategic planning cycles and placing greater emphasis on early-stage drug assets.

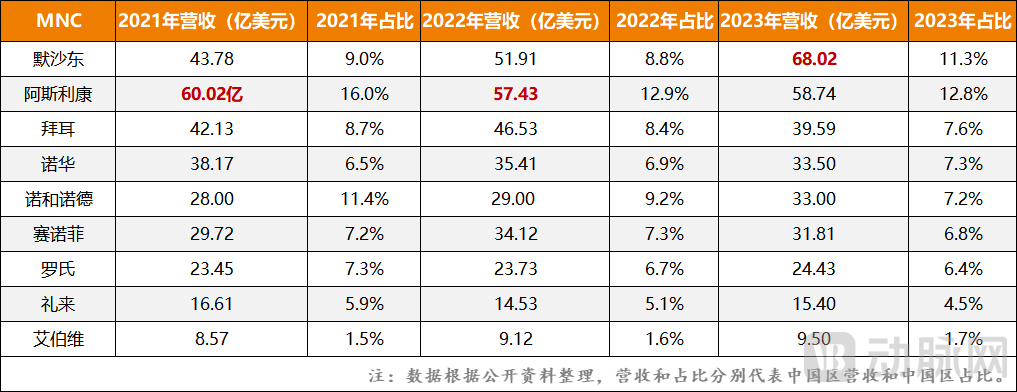

Figure 4. Changes in Revenue and Proportion of MNCs in China from 2021 to 2023

Figure 4. Changes in Revenue and Proportion of MNCs in China from 2021 to 2023

Second, declining performance is driving MNCs to seek new growth curves.. In 2023, Merck & Co. surpassed AstraZeneca to become the top revenue-generating multinational corporation (MNC) in the China market. This outcome was primarily driven by two factors: first, Merck & Co. continuously expanded its business development (BD) efforts, introducing more innovative products to China and achieving rapid performance returns; second, AstraZeneca faced market headwinds, with a significant decline in its core businesses, particularly in respiratory care.

To reverse the trend, AstraZeneca has intensified its adjustments in China since 2023, with a particular emphasis on increasing investment in business development (BD). The company has completed eight transactions to date, paying nearly $500 million in upfront fees alone. This strategic shift is driven byCompared with building an in-house team to pioneer innovation, the business development (BD) model for innovative drugs in China is clearly more cost-effective.On the one hand, China’s innovative drugs have already gained a certain level of competitiveness; on the other hand, these innovative drugs are often better tailored to the Chinese market, enabling rapid regulatory approval and market entry, thereby securing first-mover advantage. Furthermore, by opting for business development (BD) partnerships instead of in-house R&D, multinational corporations (MNCs) can effectively control overall costs, thereby further amplifying their ultimate returns.

The final point is to look at the entire Chinese innovative drug market,It is undoubtedly the best time for MCNs to acquire high-quality Chinese biotech companies at low prices.Specifically, influenced by factors such as the tightening of IPOs for pre-profit biotech companies on the STAR Market and a capital winter, most domestic biotechs are currently facing certain “cash flow” pressures. Business development (BD) transactions have not only become one of the most important exit channels but have also opened up new monetization pathways for innovative drugs in China. Several pharmaceutical companies have even achieved a turnaround from losses to profits through BD, with typical representatives including Ascentage Pharma, Baili Tianheng, and Kelun-Biotech.

To capture this wave of hot money, numerous Chinese innovative drug companies have elevated business development (BD) to a top strategic priority. They are not only investing heavily in expanding their BD teams but also actively engaging with multinational corporations (MNCs), with the China International Import Expo (CIIE) serving as a typical platform for such exchanges. As a result, major MNC booths were crowded with core BD personnel from various pharmaceutical companies. For MNCs, driven by strong supply and demand dynamics, this presents an opportunity to incorporate more high-quality Chinese assets into their portfolios in the most cost-effective manner, undoubtedly making it a win-win collaboration.

Therefore, at this China International Import Expo (CIIE), it was evident in both the booth presentations and the core viewpoints articulated thatMNCs no longer view the Chinese market merely as a sales target; instead, they regard it as a source of innovation and a new frontier for identifying fresh profit drivers.。

In response, a representative from a multinational corporation (MNC) told VCBeat, “With the rapid rise of innovative drugs in China, the value of the Chinese pharmaceutical market for MNCs is no longer limited to simply ‘selling drugs.’”In the future, the MNC that emerges as the most competitive player in the Chinese market will undoubtedly be the one capable of rapidly integrating into China’s pharmaceutical industry—specifically, by deeply engaging in the nation’s healthcare innovation ecosystem and accelerating the regulatory approval and market launch of more innovative drugs developed in China.. In this process, high hopes are pinned on business development (BD), prompting multinational corporations (MNCs) to make aggressive bets.

Localization of MNCs: Deeper Collaboration, Broader Horizons

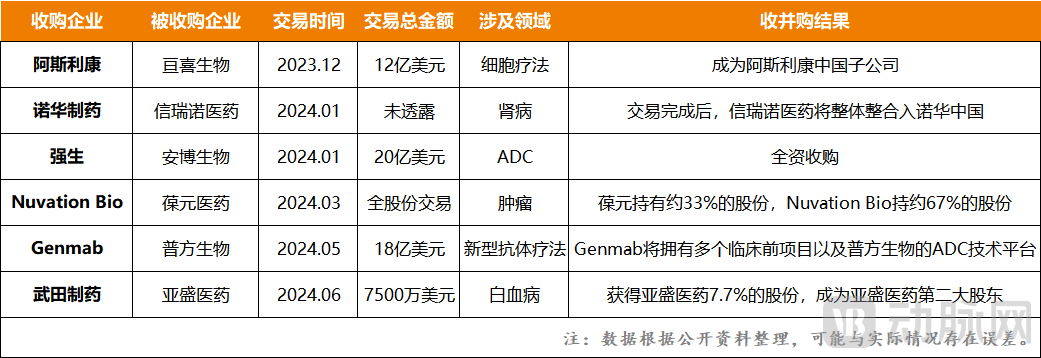

In December 2023, AstraZeneca announced the acquisition of Gracell Biotechnologies for a total consideration of $1.2 billion.This marks the first time an MNC has acquired a domestic biotech company in its entirety.. This has undoubtedly opened the door to a new era, with companies such as Novartis, Nuvation Bio, Genmab, Johnson & Johnson, and Takeda subsequently joining the wave of mergers and acquisitions. This may only be the beginning; industry sources reveal that Legend Biotech has received acquisition offers from multinational corporations (MNCs), raising expectations for a historic mega-merger.

Figure 5. Key M&A Events Involving Multinational Corporations Acquiring Chinese Pharmaceutical Companies

Figure 5. Key M&A Events Involving Multinational Corporations Acquiring Chinese Pharmaceutical Companies

From the frenzied betting on BD to attempts at mergers and acquisitions,All of which serve as proof that MNCs are accelerating their integration into China’s healthcare innovation ecosystem.. In fact, this is also the key message that MNCs conveyed to the industry at this CIIE: a deep focus on localization strategies. In addition to introducing more blockbuster products to China and making China their global launch site, they are also actively seeking opportunities to collaborate with more high-quality Chinese assets.

To this end, multinational corporations (MNCs) have been continuously innovating their collaboration models with Chinese pharmaceutical companies, such as co-developing technologies in cutting-edge fields and sharing risks. Meanwhile, MNCs are also leveraging business development (BD) to help Chinese pharma companies expand globally. A typical example is the partnership between Takeda and Ascentage Pharma: after becoming the second-largest shareholder of Ascentage through BD activities, Takeda has successfully launched olverembatinib onto the global market.

Additionally, the “NewCo” model is gaining traction among multinational corporations (MNCs). A “NewCo” is typically established through capital assembly, whereby a pharmaceutical company spins off its pipeline and licenses it to the NewCo in exchange for equity and funding. The ultimate exit strategy involves either selling the NewCo to an MNC at a premium or listing it on the capital markets. For instance, Pfizer has already generated two multi-billion-dollar NewCo success stories: by partnering with Bain Capital to establish Cerevel and Telavant, both of which were subsequently acquired at high valuations by AbbVie and Roche, respectively, yielding substantial returns for Pfizer.

A “NewCo” partnership was also established during this CIIE: Nanjing Vitalis Biologics and venture capital firm Aditum announced the formation of Oblenio Bio, a new drug development company based on LBL-051, the world’s first CD19×BCMA×CD3 trispecific T-cell engager antibody. The two parties have entered into an exclusive option and licensing agreement, with an upfront payment of nearly RMB 240 million. Notably, this marks the first overseas expansion via the NewCo model for a domestically pioneered antibody therapy.

Of course,MNCs’ innovative collaborations extend beyond pharmaceutical companies and capital investors to include governments and academic research institutions, directly resulting in the widespread establishment of numerous innovation centers and production bases in recent years.。

Taking Roche as an example, in 2022, the Roche Shanghai Innovation Center was officially upgraded to the Roche China Innovation Center, granting it independent decision-making authority for new drug research and early-stage development. In 2023, the Roche China Innovation Accelerator was formally established to drive the translation of more scientific achievements into commercial products. In 2024, at this year’s China International Import Expo (CIIE), Roche launched the “Digital Health Incubator 2.0,” an integrated platform designed to streamline stages from clinical concept validation through product development to regulatory approval and market launch, thereby accelerating the market entry of innovative projects.

In addition to Roche, Johnson & Johnson, Takeda, Novartis, GlaxoSmithKline, and Merck also officially announced multi-dimensional collaborations with China’s healthcare innovation ecosystem at this year’s China International Import Expo (CIIE), which will bring significant changes to pharmaceutical innovation in China.

It is not difficult to see that,MNCs Are Building a “Co-prosperity” Relationship with China’s Healthcare Innovation Ecosystem, and as multinational corporations (MNCs) deepen their localization strategies in China, they will unlock new growth opportunities, while Chinese innovative drugs will gain access to more top-tier resources. This means that more blockbusters will emerge in the Chinese market in the future, bringing with them greater market opportunities.