Northeast Pharma Acquires 70% Stake in Dingcheng Peptide Source for RMB 187 Million to Enter TCR-T Cell Therapy

Valued at RMB 187 million.

Northeast Pharmaceutical Group Co.,Ltd. finally disclosed the proposed acquisition amount in its announcement on November 6, 2024.

Previously, on August 5, 2024, Northeast Pharmaceutical Group Co., Ltd. convened the 29th Meeting of the Ninth Board of Directors, where the proposal regarding the signing of the "Framework Agreement on Equity Acquisition" was reviewed and approved with 11 affirmative votes (unanimous approval). On August 6, 2024, the Company disclosed the "Announcement of Northeast Pharmaceutical Group Co., Ltd. on Signing the Framework Agreement on Equity Acquisition" (Announcement No.: 2024-047), proposing to acquire a 70% equity interest in Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. (hereinafter referred to as "Dingcheng Peptide Source").

At that time, two products from Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. were on the verge of entering clinical trials. The proposed acquisition announcement triggered a sharp market reaction, driving Northeast Pharmaceutical Group Co., Ltd.’s stock price to rise for four consecutive trading days and pushing its market capitalization close to RMB 8 billion. This represents an increase of nearly 40% compared to the RMB 5.7 billion market cap recorded on August 5.

On November 6, Northeast Pharmaceutical Group Co., Ltd. announced that the “Proposal on Signing the <Equity Acquisition Agreement>” was unanimously approved by its Board of Directors again. Northeast Pharmaceutical entered into an agreement with Zhang Rong to acquire in cash, using its own funds, a 70% equity interest in Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. held by the transferor. The parties determined the consideration for this equity acquisition to be RMB 186,755,022.22, valued at RMB 187 million.

As one of the “four major legacy pharmaceutical companies,” Northeast Pharmaceutical Group Co., Ltd. started with active pharmaceutical ingredients (APIs) and later gradually expanded into traditional formulation manufacturing. For many years, however, it had no plans to enter the innovative drug sector; when it finally made its move, it directly embarked on the development of TCR-T therapy. Another surprising aspect is that Northeast Pharmaceutical’s R&D expenditure has long remained below 1%. In this regard, Feng Xiao stated that if the acquisition is successfully completed, ample funding will be allocated for scientific research and translational medicine, with “no upper limit.”

Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. was established in 2014 and is primarily engaged in cell therapy. Its two most advanced product candidates are poised to enter clinical trials, involving the recently prominent TCR-T therapy. According to Feng Xiao, Deputy General Manager and Chief Scientist of Northeast Pharmaceutical Group Co., Ltd., the actual controller of Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. has declined acquisition offers from several well-known institutions.

Vying for China’s First on the Curve

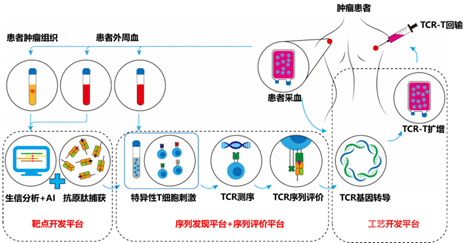

Beijing Dingcheng Peptide Source Biotechnology Co., Ltd., established in 2014, is an R&D-focused enterprise dedicated to the development and translation of cell therapy products for solid tumors. Its proprietary TCR technology platform comprises six sub-platforms addressing target selection, precise targeting, systematic evaluation, and unleashing T-cell potential, thereby forming a closed-loop system that spans target discovery, sequence identification, sequence evaluation, process development, functional enhancement, and TCR protein therapeutics.

TCR-T (T cell receptor T) is an immunotherapy technique based on human T cells. It utilizes T cells obtained from cancer patients, which are genetically modified to express TCR genes capable of specifically recognizing tumor antigens, thereby endowing the T cells with the ability to identify and attack tumor cells. After ex vivo expansion, these engineered T cells are infused back into the patient to treat cancer.

TCR protein therapeutics are a novel class of biologic macromolecule drugs. Unlike TCR-T therapy, they do not require the use of patients’ own T cells. Currently, TCR protein therapeutics primarily function by fusing the T-cell receptor (TCR) with a CD3 antibody to activate the patient’s endogenous T cells to attack tumor cells. These bispecific molecules can recognize peptide–major histocompatibility complex (pMHC) molecules on the tumor surface and link T cells to tumor cells via the CD3 antibody, thereby inducing T cell-mediated tumor cell killing.

According to the official website of Beijing Dingcheng Peptide Source Biotechnology Co., Ltd., its proprietary sequence discovery platform—the Find the Ideal Receptor for Solid Tumor Treatment (FIRST) platform—has been iterated to version 3.0. This platform has identified TCR sequences that are inaccessible to peer companies, with no relevant reports found in global patent databases or published academic literature. Furthermore, for targets already pursued by competitors, Dingcheng Peptide Source’s FIRST 3.0-based development achieves a competitive advantage characterized by “unique offerings where others have none, and superior quality where others do.”

On August 8, 2024, according to the official website of the Center for Drug Evaluation (CDE) under the National Medical Products Administration (NMPA), Dingcheng Peptide Source’s DCTY1102 injection received implicit approval for clinical trials from the NMPA. DCTY1102 injection is the world’s first TCR-T cell therapy product targeting the HLA-A*11:01 genotype and KRAS G12D mutation, with indications for advanced malignant solid tumors such as pancreatic cancer and colorectal cancer. The approval of this Investigational New Drug (IND) application marks a milestone for Dingcheng Peptide Source. HLA-A*11:01 is the most prevalent HLA phenotype in the Chinese population, accounting for 21%. KRAS is one of the most critical core driver genes in pancreatic cancer, with KRAS mutations detectable in approximately 90% of pancreatic cancer patients. Among these, the KRAS G12D mutation is the most common subtype, with an incidence rate exceeding 40%.

During the same period, Adaptimmune’s Tecelra, a drug approved by the U.S. Food and Drug Administration (FDA), was launched overseas for the treatment of unresectable or metastatic synovial sarcoma in adults who have previously received chemotherapy. Tecelra is commercially priced at $727,000 (approximately RMB 5.22 million), setting a new global record for the most expensive “cell therapy.” In China, Xiange Pharmaceutical, a leading company in TCR-T cell immunotherapy, has had its novel TCR-T cell therapy drug, TAEST16001 injection, included in the Breakthrough Therapy designation. The company has completed Phase I clinical trials and the first stage of Phase II clinical trials at the Sun Yat-sen University Cancer Center in Guangzhou and Peking University Cancer Hospital, making it one of the most advanced products in the country.

Back in 2022, the approval of Kimmtrak achieved multiple “firsts,” marking a milestone breakthrough: it was the first TCR-T therapy approved by the FDA, the first bispecific T-cell engager approved by the FDA for the treatment of solid tumors, and the first—and currently only—FDA-approved therapy for unresectable or metastatic uveal melanoma.

According to an announcement by Northeast Pharmaceutical Group Co., Ltd., Dingcheng Peptide Source’s DCTY1102 injection is poised to become the second TCR-T cell therapy targeting KRAS G12D globally, and the first in China, to enter Phase I clinical trials. Its therapeutic advantage lies in its ability to recognize intracellular antigens presented by MHC molecules, thereby demonstrating efficacy against solid tumors. However, using this as a starting point to achieve rapid advancement requires overcoming well-known challenges associated with TCR-T therapies, such as HLA restriction, limited TCR-T cell homing, and insufficient T-cell persistence in vivo. Furthermore, to achieve commercialization goals, DCTY1102 injection will need to deliver more compelling clinical efficacy data.

From “SOE Hunter” to the Second M&A

The fervor surrounding TCR-T therapy in August spilled over into the capital markets, igniting interest among Chinese pharmaceutical companies. On August 5, Northeast Pharmaceutical Group Co., Ltd. convened a meeting to discuss the proposed acquisition of Beijing Dingcheng Peptide Source Biotechnology Co., Ltd., which is engaged in similar TCR-T therapy research—a move that can be described as striking while the iron is hot.

Northeast Pharmaceutical, one of the four time-honored pharmaceutical enterprises in China, was listed on the Shenzhen Stock Exchange in 1996. The company’s product portfolio encompasses ten major series, including vitamins, anti-infectives, reproductive system and sex hormones, nervous system agents, anti-HIV drugs, gastrointestinal medications, narcotic and psychotropic substances (including ephedrine-containing products), other generic drugs, in vitro diagnostic reagents, and general health products. As of the end of 2023, the company had obtained 354 drug approval documents, among which 241 specifications were included in the National Reimbursement Drug List, and 120 specifications were listed in the National Essential Medicines List.

As a time-honored pharmaceutical enterprise, Northeast Pharmaceutical Group Co., Ltd. faces significant impacts and challenges due to the intensifying competition in the active pharmaceutical ingredient (API) and generic drug sectors. This heightened rivalry is driven by the deepening implementation of China’s national centralized volume-based procurement, the comprehensive rollout of the consistency evaluation for generic drugs, and the aftermath of the COVID-19 pandemic.

In 2018, Fangda Group invested in Northeast Pharmaceutical Group Co., Ltd. (Northeast Pharm), resulting in a change of the company’s actual controller from the Shenyang Municipal State-owned Assets Supervision and Administration Commission to Fang Wei. Known as the “SOE Hunter” for his expertise in capital operations, Fang Wei typically acquires traditional assets at low prices, revitalizes corporate performance through measures such as cost streamlining, and then exits. Between 2018 and 2021, Fang Wei, through Fangda Group and Fangda Steel, gradually became the actual controller of Northeast Pharm by acquiring approximately 55% of its shares via various methods, including cash purchases of privately placed shares, centralized bidding transactions, equity transfers, and tender offers.

Since then, Northeast Pharmaceutical Group Co., Ltd. has undergone a transformation, intensifying its efforts in innovative drugs and high-barrier generic medicines. The company aims to build a competitive, tiered product portfolio in therapeutic areas including central nervous system disorders, oncology, autoimmune diseases, and metabolic and endocrine conditions, thereby establishing a “dual-innovation” driven model characterized by innovation-led development complemented by generic follow-ons.

One piece of evidence is that Northeast Pharmaceutical Group Co., Ltd. introduced the preclinical antibody drug pipeline from the U.S. company MedAbome in September 2022 and signed a cooperation agreement to jointly develop ADC drugs and CAR-T cell therapy products based on the MAb11-22.1 antibody. The agreement also stipulates that the U.S. pharmaceutical company will assist Northeast Pharmaceutical in building an ADC platform and a CAR-T cell therapy technology platform. The upfront payment for the aforementioned transaction was USD 6 million and RMB 6 million; subsequent milestone payments of USD 7 million and RMB 7 million will be made upon achievement of specified conditions; plus royalties on net sales of new drugs from future projects.

Two years later, Northeast Pharmaceutical Group Co., Ltd. once again took action to acquire a 70% equity stake in Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. It is worth noting that although the innovative drug sector has felt relatively cool, the cell therapy and ADC (Antibody-Drug Conjugate) sectors where MedAbome and Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. operate remain hot, as evidenced by the BD transactions in 2024.

Navigating an Era of Change: A Two-Way Commitment

Northeast Pharmaceutical Group Co., Ltd. faces undiminished challenges.

First, the company’s controlling shareholders and management team must be mentally prepared for the substantial capital outlays required for innovative drug development. Northeast Pharmaceutical Group Co., Ltd.’s current financial position is less than ideal, and this M&A-driven transformation model inevitably draws comparisons to Hengrui Medicine. Even a powerhouse like Hengrui, which has relied on cash flows from generic drugs to fund the hefty R&D investments in innovative medicines, has undergone a long and arduous journey.

Generic drugs and innovative drugs also differ in their strategic approaches. The most core criteria for evaluating a drug remain clinical need and clinical value. To achieve clinical advantage, the key lies in the capacity for re-innovation following the introduction and assimilation of existing technologies, as well as in establishing genuine innovative technology platforms, while simultaneously possessing the capabilities for efficient development and rapid iteration.

Biological innovative drugs, such as antibody-drug conjugates (ADCs) and chimeric antigen receptor T-cell (CAR-T) therapies, require substantial capital investment, involve lengthy R&D cycles, and carry high risks. They also impose stringent demands on technological platforms and talent, thereby further increasing the difficulty of independent research and development. In the face of increasingly intense homogeneous competition in the field of biological innovative drugs (e.g., target homogenization), there are growing demands for originality in technology and products, as well as for differentiated competitive strategies.

Innovative drug company Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. is also facing pressure.

Relevant financial data show that Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. generated operating revenues of RMB 103,300 and RMB 153,900 in 2023 and the first half of 2024, respectively, with corresponding net profits of approximately -RMB 127 million and -RMB 53.3539 million. Based on the share acquisition price by Northeast Pharmaceutical Group Co., Ltd., the overall valuation of Beijing Dingcheng Peptide Source Biotechnology Co., Ltd. is estimated at approximately RMB 266 million. Under such circumstances, continued research and development of promising targets will inevitably incur substantial cash burn, while financing has also become a challenge.

In contrast, mergers and acquisitions have become a more viable option.

Even though Northeast Pharmaceutical Group Co., Ltd. is not currently in a comfortable financial position, as a time-honored enterprise, it possesses significant long-term accumulated strengths. First, there are policy advantages. As the largest pharmaceutical company in Liaoning Province, it is more likely to receive local government support and fiscal subsidies. Furthermore, it benefits from corresponding policy support in areas such as taxation, finance, research and development, and drug registration—resources that are far more difficult for ordinary private enterprises to secure. Second, there are product advantages. Traditional pharmaceutical companies have accumulated a vast portfolio of products over the years; some may even have reserves numbering in the thousands. This extensive resource pool of products, combined with forward-looking selection strategies, holds the potential to revitalize these promising drug candidates. Third, there are channel advantages. Having previously operated under state-owned capital, the company has established mature sales channels, thereby encountering fewer obstacles in commercial implementation.

More importantly, both ADCs and cell therapies represent sectors with immense growth potential. Northeast Pharmaceutical Group Co., Ltd.’s acquisitions have not reached the level of “reckless spending” or “indiscriminate buying”; rather, its strategic transformation has already begun, making any halt inconceivable. The market is eagerly awaiting the moment when Northeast Pharmaceutical truly leverages R&D innovation in these high-profile fields to achieve a dual focus on both generic and innovative drugs.