Domestic Players Break Through in an Import-Dominated Ophthalmic Segment!

“Domestic high-end intraocular lenses are developing quite rapidly, with a pace exceeding expectations!” Investors remarked thus on the latest landscape of the intraocular lens market.

Facing imported products that hold market advantages across high-, mid-, and low-end segments, domestically produced alternatives are accelerating their breakthroughs, with particularly frequent good news in the high-end intraocular lens sector since 2024.

In September 2024, the first domestically developed trifocal intraocular lens (IOL) by Leiming Vision Care received regulatory approval for market launch, breaking the monopoly held by imported products. By integrating trifocal technology, smooth phase technology, axial progressive extended depth of focus (EDOF) technology, and achromatic technology, this product delivers high-quality full-range vision for distance, intermediate, and near distances.

In addition, Aierbo Nuode’s extended depth-of-focus intraocular lens, Century Kangtai’s extended depth-of-focus intraocular lens, and SamiVision’s trifocal intraocular lens were successively included in the “green channel” for innovative medical device approval in 2024.

Currently, domestically produced intraocular lenses are predominantly mid- to low-end products; high-end products have managed to break through despite constraints such as a late start and a scarcity of optical design talent.

Intraocular Lens Products Currently in the “Green Channel” for Approval, Source: National Medical Products Administration

As the most widely used artificial organ globally, the core advanced technologies for intraocular lenses (IOLs) are held by four major international ophthalmic medical device companies—Alcon, Johnson & Johnson, Bausch + Lomb, and Zeiss—which also command the majority share of the global IOL market.

The market landscape in China is similar. According to industry data, the aforementioned four companies collectively account for more than 60% of the Chinese market share. In addition, foreign brands such as HOYA, Lantech, Nari (UK), and HumanOptics also hold a certain presence in the domestic market, while the market share of domestically produced brands stands at around 20%.

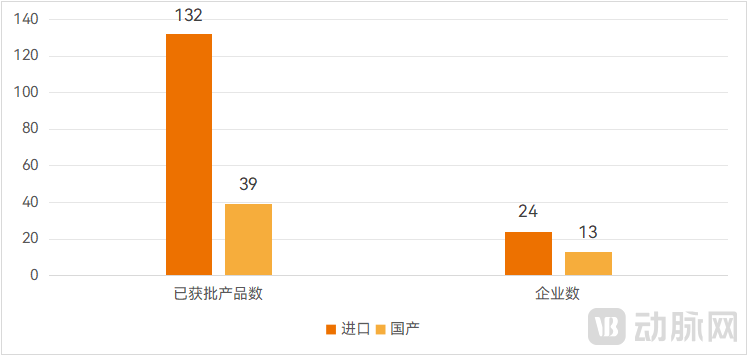

At the product level, according to statistics from VCBeat, more than 170 intraocular lens (IOL) products have been approved in China to date, including 132 imported products and 39 domestically produced ones.

Status of Approved Intraocular Lens Products in China, Source: National Medical Products Administration

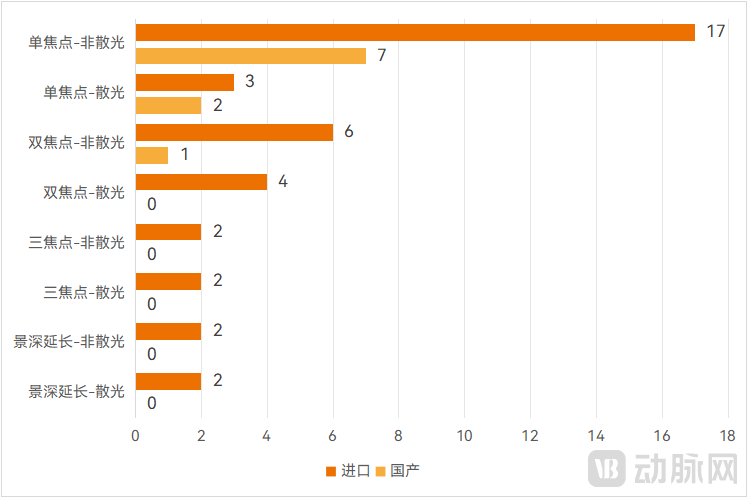

Since 2024, the first national centralized procurement of intraocular lenses organized by the state has been successively implemented across China. The distribution of selected products in this procurement intuitively demonstrates the dominant position of imported products.

Distribution of Imported and Domestically Produced Products in the National Centralized Procurement of Intraocular Lenses

Source: National Joint Procurement Platform for Pharmaceuticals and Medical Consumables

The intraocular lenses (IOLs) included in this round of centralized procurement comprise eight major categories, covering products across low-, mid-, and high-end segments. Among the low-end representative products, namely monofocal non-toric IOLs, 17 imported products and 7 domestically produced products were selected. In the mid-end segment, only products from Aier Medical (Aibonode) and Rayner Vision Care were selected. For high-end products, all selected trifocal IOLs and Extended Depth of Focus (hereinafter referred to as EDOF) IOLs are imported.

In other words, in terms of the number of awarded products, imported products hold a clear advantage across low-end, mid-range, and high-end categories; when calculated in conjunction with the procurement volume of various product types, there is also a significant disparity between imported and domestically produced products.

Trifocal and extended depth of focus (EDOF) intraocular lenses are high-end products with significant technical barriers and represent a key area of research and development. These two categories not only treat cataracts but also provide more continuous, higher-quality vision at distance, intermediate, and near ranges, substantially reducing patients’ dependence on glasses after cataract surgery. However, no domestic companies have had such products included in centralized volume-based procurement, and there were zero domestically approved products prior to 2024. The market remains dominated by Alcon, Zeiss, and Johnson & Johnson.

Notably, the world’s first trifocal intraocular lens (IOL), the ZEISS AT LISA tri 839MP, was launched in 2012 and has been on the market for over a decade. Imported products have already established significant advantages in research and development, mass production, and clinical application.

In fact, mid- to low-end intraocular lenses (IOLs) account for the largest volume of usage, while high-end products represent only about 10% of the market share; however, strategic positioning in the high-end segment is crucial for companies.

“Even looking ahead to the next five years, monofocal intraocular lenses (IOLs), which primarily restore vision, will remain the market mainstream. However, high-end products offer higher profit margins, and the market share of functional IOLs is continuously increasing, making this segment a critical battleground for enterprises,” said Fan Rongkui, Managing Director at Yifeng Capital. He noted that the material and technological barriers underlying high-end products are also important manifestations of a company’s core competitiveness and product brand strength.

Currently, domestically produced intraocular lenses (IOLs) in China are predominantly mid- to low-end products. In the high-end segment, Aierbo Nuode has begun to break the monopoly held by multinational corporations, launching the first—and so far only—domestically produced bifocal IOL in 2022. Furthermore, according to Fan Rongkui, companies such as Century Kangtai, Leiming Vision Care, and Haohai Biological Technology along with its subsidiary IOL manufacturer have all achieved breakthroughs in recent years in areas including optical design and manufacturing processes for intraocular lenses.

Fan Rongkui stated that in the realm of high-barrier products such as trifocal and extended depth of focus (EDOF) intraocular lenses, although multinational corporations have had their products on the market for many years, recent updates by various companies have been merely incremental improvements. No next-generation or substitute products have emerged yet, creating a window of opportunity for domestic manufacturers to catch up. “Of course, Chinese-made products need to overcome challenges in multiple areas, including optical design, precision machining, and mass production. For instance, Century Kangtai has overcome the difficulties in optical design through industry-academia-research collaboration.”

Shi Baona, General Manager of SymEyes, stated that the primary purpose of trifocal intraocular lenses is to focus light entering the eye through different paths onto the retina. This requires altering conventional optical pathways to achieve clear vision at distance, intermediate, and near ranges. While various design approaches can be adopted to achieve this goal, key challenges in developing high-end products include determining the specific design that accomplishes this without adversely affecting light energy distribution, while minimizing undesirable visual effects such as light energy loss, chromatic aberration, and halos. Another major challenge lies in the translation from design to actual product realization, which involves manufacturing processes, raw materials, and process stability.

As Latecomers, What Is the Key to Catching Up for Domestically Produced Products?

In Shi Baona’s view,Domestic companies need to build core technology platforms and lay a solid foundation, and efficiently deploy high-quality full-line products on stable technology platforms to meet the multifaceted needs of patients.

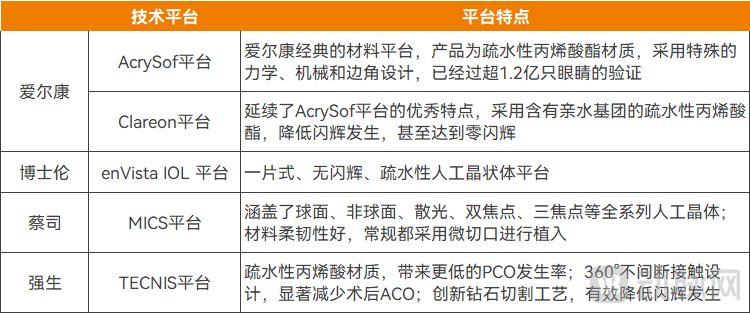

It is understood that the four major multinational giants in the intraocular lens (IOL) market each have their own core platforms. Alcon has successively launched the AcrySof and Clareon platforms; Johnson & Johnson’s TECNIS platform IOLs have been on the market for 23 years; Carl Zeiss Meditec owns the TECNIS platform; and Bausch + Lomb has established the enVista platform.

Intraocular Lens Platforms of Major Multinational Corporations, Source: Public Reports

Why Does the Research, Development, and Manufacturing of Intraocular Lenses Require a Technology Platform?

Only an advanced and efficient technology platform can continuously support a rich portfolio of functional intraocular lens (IOL) products, ensuring high-quality performance for each product, providing clinicians with better solutions, and delivering improved postoperative experiences for patients.

Currently, some domestic enterprises have also established their own technical platforms, including Aierbo Nuode’s Proming platform, Century Kangtai’s Mercury platform, and Saimeishi’s MOM platform.

For example, SightGlass Vision spent several years building an advanced MOM technology platform that integrates cutting-edge materials science, precision optical design, and advanced molding and injection technologies. This has been the primary reason for its ability to efficiently and rapidly deploy a full product line in a short period.

In addition to building a foundation through platforms, domestic enterprises have also implemented numerous product-level differentiations or further enhanced visual effects.

Domestic trifocal and EDOF intraocular lenses under development or in the approval process; Source: National Medical Products Administration, corporate official websites and WeChat accounts

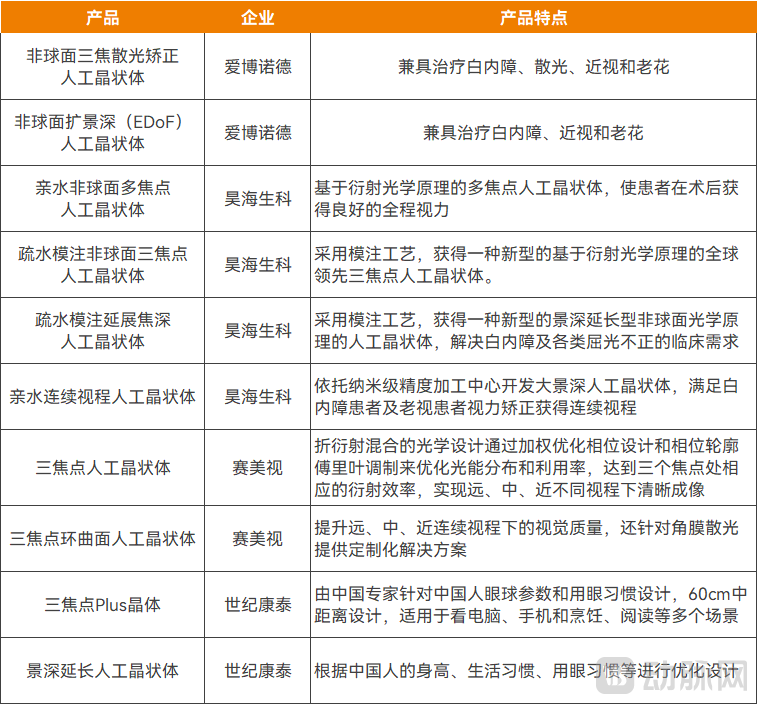

For example, Leiming Shikang’s approved trifocal product integrates trifocal technology, smooth phase technology, axially progressive extended depth of focus (EDOF) technology, and achromatic technology. In previous Phase III clinical trials, it demonstrated excellent uncorrected distance, intermediate, and near vision, with statistically significant superiority in intermediate vision.

Century Kangtai’s trifocal product was designed by Chinese experts based on the ocular parameters and visual habits of the Chinese population. It features a 60 cm intermediate-distance design, providing continuous vision for activities such as computer and smartphone use, cooking, and reading.

Simeishi’s trifocal product adopts a hybrid refractive-diffractive optical design. By optimizing light energy distribution and utilization through weighted phase optimization and Fourier modulation of the phase profile, it achieves clear imaging at distance, intermediate, and near vision ranges, thereby meeting diverse visual needs.

In 2024, the approval of numerous products or their entry into the regulatory “green channel” for expedited review became a significant turning point for breakthroughs in high-end intraocular lenses (IOLs). Fan Rongkui believes that multiple high-end IOLs are expected to receive approval successively from the first half of 2024 through 2025, helping domestically produced IOLs advance to a new level. “Overall, the development of domestically produced high-end IOLs is progressing very rapidly, exceeding expectations.”

As the aging process accelerates, growth in China’s intraocular lens (IOL) market is inevitable. With several representative high-end products having received approval and entered the market, what are the next breakthrough directions for domestically produced IOLs?

Shi Baona believes that after decades of development, intraocular lenses (IOLs) currently available on the market show little difference in their basic optical performance, while other functionalities have become relatively comprehensive.One of the future product directions is to address common clinical issues associated with these products. In terms of clinical effectiveness, the goal is to achieve truly clear vision throughout the entire visual range. Regarding clinical adverse reactions, the aim is to resolve issues such as halos and glare associated with trifocal intraocular lenses (IOLs), prolonged postoperative adaptation periods, and blurred vision caused by uneven light distribution. For toric IOLs, which impose higher requirements on technical platforms and materials, it is essential to ensure excellent rotational stability to maintain the correct astigmatic axis alignment, thereby providing stable and reliable astigmatism correction.

Another trend is the development of specialized intraocular lenses that address concomitant ocular conditions.Shi Baona noted that drug-eluting intraocular lenses are used to prevent and treat endophthalmitis after cataract surgery, and that artificial iris diaphragm intraocular lenses are being developed for patients with iris deficiency.

Adjustable intraocular lenses are widely recognized within the industry as the future trend and represent the most ideal product form.Such products are designed to simulate the accommodative function of the natural human eye. Although major international companies have made numerous attempts in areas such as material selection and structural design, they have not yet achieved satisfactory clinical outcomes. Consequently, no intraocular lens that is safe for implantation and truly possesses sufficient accommodative ability has been developed to date.

“The R&D of adjustable intraocular lenses faces significant challenges, which are closely related to human physiological structures;The future development and application of adjustable intraocular lenses may be combined with AI and active technologies to simulate the human eye’s accommodative function as closely as possible. However, the product development process will be very lengthy."Shi Baona stated."

In 2024, the national centralized procurement of intraocular lenses (IOLs) was gradually implemented. Among the selected products, imported brands not only accounted for the majority of the market share, but also saw significant price reductions, with multiple imported products represented by Alcon leading the way.

The current round of national centralized procurement, along with multiple previous rounds of local centralized procurement, has made the pricing of intraocular lenses increasingly transparent and provided the public with a more intuitive understanding of major domestic and international manufacturers and their products.

However, Shi Baona stated that when prices are comparable, patients tend to opt for imported products, and clinicians are more inclined to accept them—a mindset that will be difficult to change in the short term. “If we were to go back ten years, there was indeed a significant gap between domestically produced and imported products. However, despite a late start, Chinese manufacturers have rapidly caught up within just a few years. Their products now show no obvious differences from international counterparts, with certain performance metrics even surpassing those of global brands, thereby providing patients with more options tailored to their individual needs. Influenced by traditional perceptions, brand recognition remains a major challenge for domestic products. As more high-end Chinese products enter the market, companies must work together to build stronger brand influence.”

References:

Aierbode Prospectus

Happy Vision and Psychology: Innovation and Accumulation in IOL Technology—The Legendary Story of TECNIS