Over $5 Billion in Milestone Payments Received: China's Innovative Drugs Are Moving Beyond 'One-Time' BD Deals

HUTCHMED

Biopharmaceutical Manufacturer

Although the market remains in a winter chill, some are quietly getting rich.

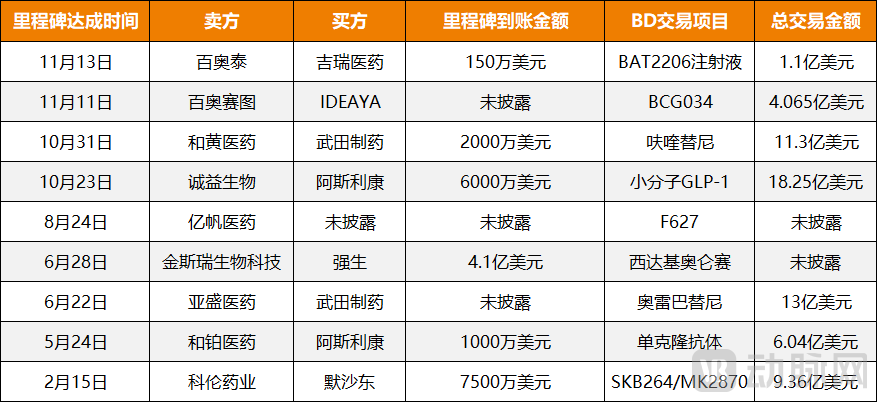

On October 31, HUTCHMED announced that, as the sales of fruquintinib for the treatment of metastatic colorectal cancer exceeded US$200 million, in accordance with the agreement,HUTCHMED to Receive $20 Million Milestone Payment from Takeda. In fact, this is not the first milestone payment received by HUTCHMED; in November 2023, fruquintinib was officially approved for marketing in the United States,HUTCHMED Also Receives $35 Million Milestone Payment from Takeda。

Figure 1. Selected Milestones of Chinese Innovative Drug Companies in 2024 (Source: Public Information)

Achieving two milestone deals in succession is no easy feat, but HUTCHMED is not an isolated case. On October 23,Chengyi Biopharma Announces Receipt of $60 Million Milestone Payment from AstraZeneca, this milestone was triggered by the first patient dosing in the Phase 2b clinical trial of the small-molecule GLP-1 receptor agonist ECC5004/AZD5004. Looking further back in time, includingKelun Pharmaceutical, Bio-Thera Solutions, GenScript Biotech, Yifan Pharmaceutical, Harbour BioMed, Ascentage Pharmaand others have also received milestone payments successively this year, with the total amount received now exceeding US$700 million.

This is truly a rare sight. Although sky-high business development (BD) deals and exorbitant upfront payments have frequently emerged in the past year or two, disclosures regarding milestone payments as subsequent installments have been relatively scarce. Now, with milestone payments arriving one after another,Does this mean that the era of “upfront payments only, no milestones” in China’s pharmaceutical industry is now a thing of the past?

HUTCHMED Rakes in $1 Billion in Six Months: How Did It Achieve Such Effortless Success?

Driven by the wave of business development (BD) deals, many innovative pharmaceutical companies have leveraged this trend to turn losses into profits, with HUTCHMED being a typical representative. According to its annual report, HUTCHMED’s revenue and net profit in 2023 were $838 million and $101 million, respectively. Revenue increased by 97% year-on-year, while the company swung from a loss in 2022 to a profit. Notably, this marks HUTCHMED’s first profitable year since its listing on the Hong Kong Stock Exchange in 2021, as well as its first return to profitability in five years.

This success is, of course, inseparable from the successful global expansion of its first innovative drug, fruquintinib. In January 2023, HUTCHMED officially granted Takeda the global rights outside China, with a total transaction value of up to $1.13 billion, setting a new record for out-licensing deals of Chinese small-molecule novel drugs. Although HUTCHMED initially received only a $400 million upfront payment, this amount alone accounted for half of HUTCHMED’s total revenue in 2023 and was key to achieving profitability.

At this point, the logic for turning losses into profits is similar to that of most current innovative drug companies, mainly relying on "sky-high BD + ultra-high upfront payments," but what makes HUTCHMED different is thatRather than recognizing it as a one-time revenue item, the company has continued to unlock the monetization potential of this transaction, securing two milestone payments within less than a year.. And this may just be the beginning. Based on market expectations for fruquintinib, its peak overseas sales are projected to exceed $1.5 billion, which means that HUTCHMED’s best days are still ahead, positioning it for continued effortless success in the future.

So, what is the reason?

First and foremost, the key lies in the product strength of fruquintinib. In fact, fruquintinib was co-developed by HUTCHMED and Eli Lilly. In 2013, the two parties signed a collaboration agreement, under which Eli Lilly obtained the domestic rights to fruquintinib in China and bore the majority of the development costs. Leveraging Eli Lilly’s resources, fruquintinib was ultimately approved in September 2018 in China for third-line treatment of colorectal cancer, becoming the first innovative targeted therapy approved for the treatment of metastatic colorectal cancer. Since then, fruquintinib has gained significant prominence. By 2023, its sales in the Chinese market had exceeded $100 million, capturing a substantial market share of 47% among patients receiving third-line treatment.

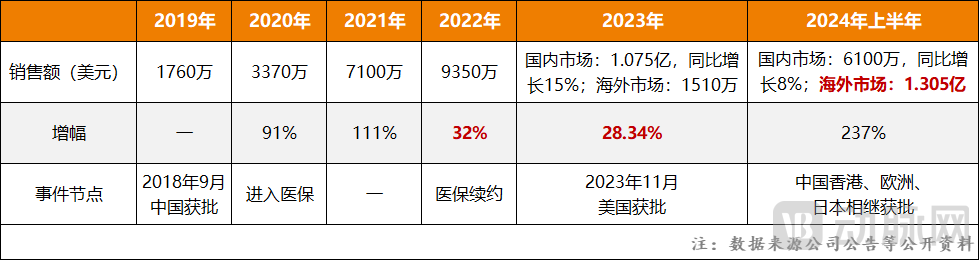

However, influenced by factors such as price reductions under the national medical insurance program, although fruquintinib’s revenue has continued to increase over the past one to two years, its growth rate has slowed significantly. The collaboration with Takeda has opened up new avenues for growth. In terms of approval progress, fruquintinib was officially launched in the U.S. market in November 2023, and subsequently received approval in the European Union and Japan in June and September of this year, respectively.It has become the first and, to date, only Chinese original innovative drug to successfully enter the three benchmark markets of the United States, Europe, and Japan.。

Figure 2. Sales Performance of Fruquintinib

Figure 2. Sales Performance of Fruquintinib

On the other hand, there is the speed of commercialization. After fruquintinib was officially launched in the United States, it was priced at $25,200 per box, more than 20 times its price in China. Despite this, sales of fruquintinib were not affected in the least; instead, they experienced explosive growth. The first prescription was written within 48 hours of its U.S. launch, and within less than two months, fruquintinib’s U.S. sales had reached $15 million.In the first half of this year, fruquintinib generated another $151 million in revenue, a figure comparable to its full-year sales in the Chinese market in 2023.。

In this rapid advancement, Takeda has certainly played an indispensable role. In fact, constrained by the patent expirations of multiple blockbuster drugs, Takeda is in need of fresh additions to its portfolio; therefore, it has been particularly vigorous in promoting fruquintinib, including facilitating overseas regulatory approvals and accelerating market channel expansion. Leveraging Takeda’s support, fruquintinib’s market share continues to expand, which means that subsequent milestones will be gradually unlocked, resulting in further payments to HUTCHMED in the future.

22% Fulfillment Rate: Milestone Payments Prone to Change

HUTCHMED is merely a microcosm, representing a model of “milestone payments at the sales stage,” which is becoming a typical pattern for Chinese innovative drugs to go global, namely, “leveraging partners to expand overseas.” However,Milestones are not limited to market metrics; they also encompass key nodes such as R&D progress and product approvals.。

Taking Kelun Pharmaceutical as an example, in February this year, the company received a $75 million milestone payment from Merck & Co. for officially launching three global pivotal Phase III clinical trials of its novel Trop2 ADC drug, SKB264 (MK-2870). Additionally, in June this year, Legend Biotech, a wholly-owned subsidiary of GenScript Biotech, received a total of $410 million in milestone payments, triggered by significant development progress of its licensed product, ciltacabtagene autoleucel.

Figure 3. Top 10 BD Deals for Innovative Drugs in China, January–November 2024

Figure 3. Top 10 BD Deals for Innovative Drugs in China, January–November 2024

In fact, there are many other “R&D progress milestones” of this kind, all of which are expected to be realized in batches in the future. According to incomplete statistics from VCBeat,Among the nearly 50 business development (BD) deals completed by Chinese pharmaceutical companies this year, more than 80% involved assets in Phase I clinical trials or earlier stages.Among these deals are several high-value collaborations. For instance, a recently finalized business development (BD) partnership valued at $3.288 billion involves Merck & Co. licensing LM-299, a PD-1/VEGF bispecific antibody from Lixin Biopharma, which is currently in Phase I clinical trials. Additionally, earlier this year, Novartis entered into a landmark $4.1 billion BD agreement with Bowang Therapeutics, also based on a Phase I clinical asset. According to the milestone payment schedules, both companies are highly likely to receive multiple milestone payments within the next one to two years.

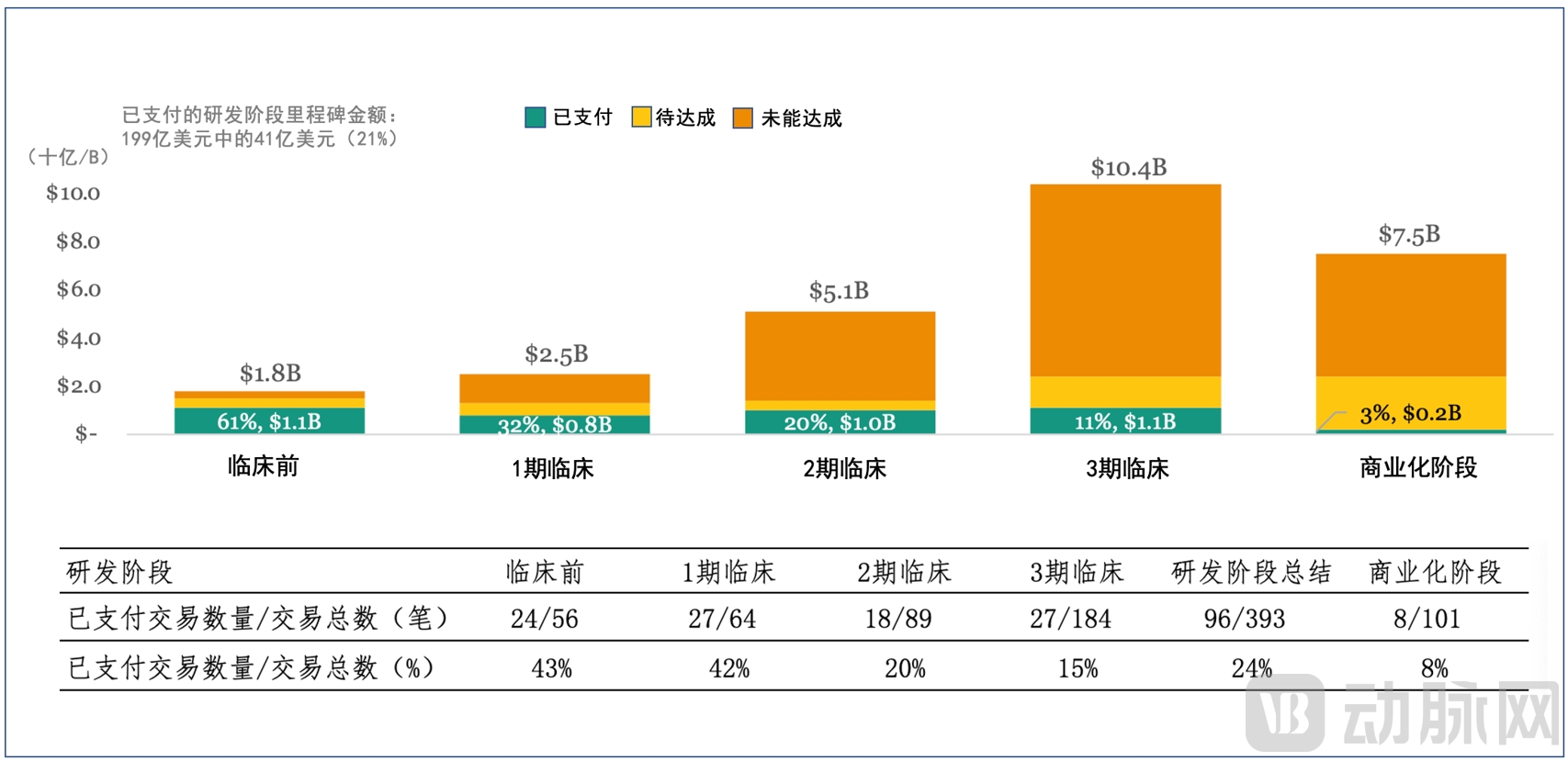

Figure 4. Achievement of Milestones Across R&D Stages for Biopharmaceuticals with Mid-2023 Expirations (Source: R&D Ke)

Figure 4. Achievement of Milestones Across R&D Stages for Biopharmaceuticals with Mid-2023 Expirations (Source: R&D Ke)

Of course, this is merely a rationalized estimate. Although the receipt of milestone payments is increasingly frequent, the fact that cannot be overlooked is thatSignificant uncertainty remains regarding milestones, particularly as transaction items continue to advance, disputes or potential disputes involved will gradually become more prominent, and this will have a direct impact on the fulfillment of milestones. According to data from 2023,In biopharmaceutical M&A transactions, the milestone achievement rate is only 22%, and the amount triggered by achieving these milestones is even lower, with only 3% of the total amount being received as milestone payments.。

So, where exactly is the milestone stuck?

First and foremost, the milestones were not triggered, including failures in clinical trials, delays in product approval, and market sales falling short of expectations.. In fact, in business development (BD) transactions within the biopharmaceutical sector, milestone payments are structured specifically to hedge against the risk of failure in final product development or commercialization. Historical data from numerous deal terminations indicate that such occurrences are relatively common, primarily due to the inherent lack of robustness in the underlying assets.

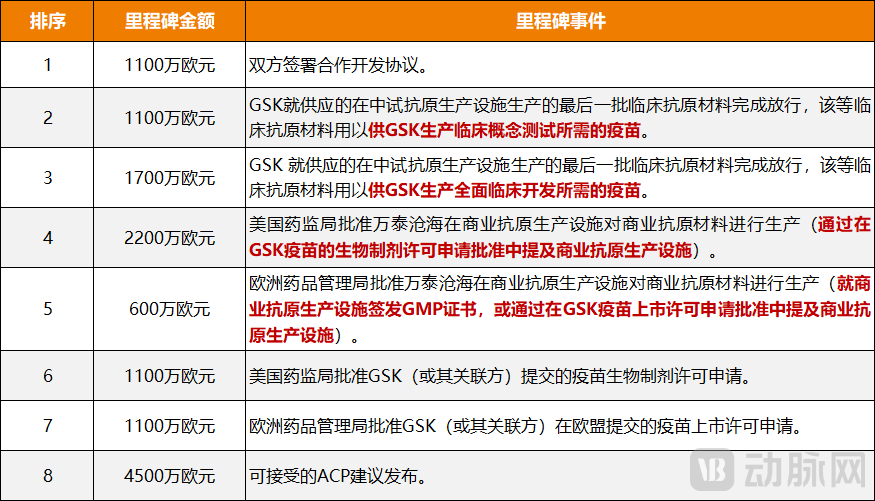

Figure 5. Milestone Payment Schedule Agreed Upon by GSK and Wantai Bio

Second, unclear milestone definitions can also easily lead to disputes during subsequent performance.Taking the termination of the agreement between Esperion and Daiichi Sankyo as an example, in 2019, Daiichi Sankyo acquired exclusive commercialization rights for two of Esperion’s combination products in Europe and other regions for an upfront payment of $150 million and milestone payments of up to $900 million. In December 2022, the Phase III CLEAR Outcomes trial, which evaluated Nexletol for an expanded indication, met its primary endpoint of MACE-4 (Note: MACE-4 comprises four cardiovascular event risks: stroke, cardiovascular death, myocardial infarction, and coronary revascularization). Esperion believed that, under the collaboration agreement, it was entitled to a $300 million milestone payment. However, Daiichi Sankyo refused, arguing that if the milestone payment were to be triggered, the reduction in MACE-4 risk should be at least 15%, whereas the observed reduction was only 12.98%, falling short by approximately 2%.

Of course, Esperion has its own argument, claiming that it met the endpoint targets stipulated in the agreement, namely that Nexletol reduced the risk of heart attacks by 27%. Therefore, the core of the dispute between the two parties actually lies in the ambiguous definition of trial endpoints in the agreement terms—specifically, whether it refers broadly to the risk of all cardiovascular events or specifically to the risk of heart attacks, which was clearly not specified in the early agreement.

The final point is strategic adjustment, whereby the buyer proactively terminates the partnership in response to changes in market conditions.Taking Novartis’s “return” of BeiGene’s PD-1 inhibitor as an example, although the drug had just been approved in Europe and its marketing application had been accepted by the U.S. FDA prior to the return, Novartis still chose to make the painful decision to divest. The core reason was a sudden shift in the competitive landscape: by 2023, Keytruda (“K-drug”) had accumulated more than 45 indications, becoming a new global blockbuster drug. As a competitor, it was undoubtedly a prudent strategy for Novartis to avoid direct confrontation and cut its losses in a timely manner.

In addition, Merck & Co. has recently terminated two preclinical ADC collaborations with Kelun-Biotech in succession. The key reason is also the changing market landscape: there are now nearly 10 Claudin18.2-targeting ADC drugs under development, and three companies have already initiated Phase III clinical trials. Merck’s SKB315 clearly lacks an advantage in clinical development progress, making it difficult to achieve a late-stage breakthrough in the future.

In this regard, a senior BD executive remarked, “Compared with the upfront payments that can be reliably secured, achieving milestones in BD transactions is indeed much more challenging, as numerous factors are involved. Beyond product-related considerations, market conditions and industry dynamics also have a direct impact. Therefore,”The more one faces sky-high deals with seemingly astronomical figures, the more crucial it is to maintain a clear head. It is not enough to focus solely on the total transaction value; greater attention must be paid to the amount that can be truly secured as net gain. This is the key to successful business development (BD) transactions.。”

Cliff-like Decline: BD Cannot Remain Merely a Stopgap for Immediate Crises

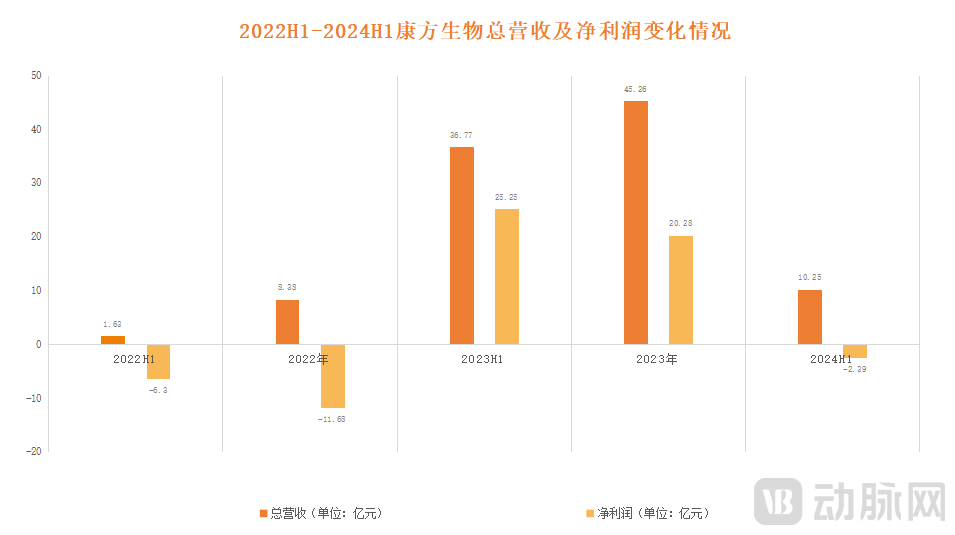

Whether upfront payments or milestone payments, both have become important engines driving the performance growth of some innovative drug companies in recent years, with no shortage of cases where they have turned around and moved from loss to profitability, includingHengrui Medicine, Ascentage Pharma, Baili Tianheng, Kelun-Biotech, Akeso, etc., are included.

Taking Akeso as a prime example, its revenue hit a record high of RMB 4.526 billion in 2023, representing a year-on-year increase of 440.35%. Driven by this growth, its net profit attributable to shareholders reached RMB 2.028 billion, marking its first annual profit since going public. This turnaround was primarily attributed to a landmark deal: in the first quarter of 2023, Akeso received an upfront payment of RMB 500 million for the licensing rights to ivonescimab, which accounted for as much as 80% of its annual revenue and was key to its shift from loss to profit.

Figure 6. Akeso’s Financial Performance (Source: Annual Reports)

Figure 6. Akeso’s Financial Performance (Source: Annual Reports)

However, the good times were short-lived. According to the latest 2024 semi-annual report, Akeso’s performance declined significantly, with a year-on-year drop of 72.13%, and it fell back into the vicious cycle of losses, reporting a net loss of RMB 239 million. This downturn was primarily due to the absence of substantial licensing income. In this sense, Akeso’s financial performance is directly tied to its business development (BD) activities—its success and setbacks alike can be attributed to BD.

In fact, this is not an isolated case. As the number of sky-high-priced business development (BD) deals continues to rise, similar cases are expected to emerge in large numbers in the future. Therefore,A pressing question in the industry has become increasingly prominent: how to sustain the value of business development (BD) and leverage capital to generate greater returns?

By analyzing typical cases and incorporating insights from industry experts, VCBeat believes that solutions primarily lie in two aspects,The first aspect is to fulfill as many milestone payments as possible.Specifically, this entails establishing a deep strategic partnership with the buyer and leveraging their strengths to accelerate the progress of licensed products in key areas such as R&D, regulatory approval, and market commercialization, thereby securing more substantial milestone payments.

The second aspect involves reinvesting the generated cash flows into new R&D initiatives or bolstering the existing pipeline, thereby building a diversified product portfolio and progressively transitioning toward a biopharmaceutical model.. This is actually similar to the monetization logic of investment institutions, which continuously channel revenue into new value targets in exchange for greater returns. Of course, during this process, the ability to identify investable projects is crucial and serves as the key differentiator for investment firms. When applied to the R&D phase, this “ability to identify projects” equates to an innovative pharmaceutical company’s capacity to discover and develop valuable pipelines and products.

In this regard, the founder of a pharmaceutical company remarked, “BD income is equivalent to an investment, typically involving substantial amounts, which can alleviate corporate funding constraints to some extent. However, in the long run, it cannot sustain continuous performance growth; the true growth potential of pharmaceutical companies lies in their products. Therefore, for pharmaceutical companies,”As BD deals are realized, innovative achievements must also be continuously delivered; only in this way can pharmaceutical companies truly emerge from the quagmire of losses, and the value of BD will continue to amplify.。”

This undoubtedly provides a strategic approach for innovative drug companies currently facing growth bottlenecks.

1. “How Much Can We Get from Milestone Payments?” — R&D Ke;

2. “Chinese Innovative Drugs Generate 1 Billion in Sales in the U.S. Within Six Months” – Jian Shi Ju;

3. “HUTCHMED: The Drifting Tale of Old Money” — Shenlan Guan.