Medical Aesthetics Industry Enters Fierce Customization Battle as Major Players File IPOs

This is a chaotic struggle involving both medical aesthetic institutions and upstream device manufacturers, rooted in the prevalence of customized products at medical aesthetic clinics over the past year or so.

Industry insiders commonly refer to these as OEM products, whereby medical aesthetics institutions collaborate with upstream device manufacturers to launch products under the institutions’ own brands. However, since most medical aesthetics institutions possess only the brand, while product design, R&D, registration, and manufacturing are all handled by the device manufacturers, these arrangements do not constitute OEM in the strict sense but rather exhibit stronger characteristics of ODM (Original Design Manufacturer) products. For clarity, this article uniformly refers to them as “customized products.”

According to incomplete statistics, there are currently more than 20 customized product brands on the market. Each brand is sold exclusively at medical aesthetic institutions under a specific medical aesthetic group, and a single group may offer multiple customized brands.

In the short term, customized products have, to some extent, reshaped the ecosystem between medical aesthetic institutions and upstream device manufacturers, as well as between domestically produced and imported products, establishing a certain balance.However, the fierce competition in the medical aesthetics product market, particularly price wars, has emerged in another form.

Browsing through online medical aesthetics platforms, one can spot some new faces among the well-known domestic and international brands such as Juvederm, Restylane, Runbaiyan, and Haiwei in the list of injectable products. On the product detail pages, descriptions like “Exclusively Supplied to XX Institution” or “Exclusively Customized by XX Institution” are often visible, which are typical examples of customized products.

Several years ago, some medical aesthetic institutions began collaborating with upstream suppliers to develop customized products, a trend that has intensified markedly over the past year. The initiatives have been primarily led by large chain medical aesthetic providers, with hyaluronic acid-based products being the main focus due to their high average transaction value, relatively mature technology, and broad range of available upstream options.

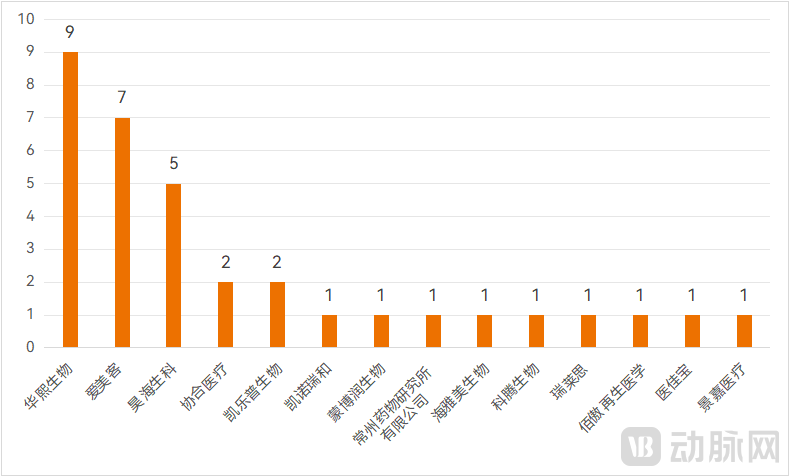

To date, institutions such as Mylike, Yestar, Langzi Medical Aesthetics, and Huamei have each developed multiple proprietary customized products, with Bloomage Biotechnology and Haohai Biological Technology serving as the primary suppliers.

Customized Products from Select Medical Aesthetics Institutions; Source: Public Corporate Information, SoYoung App

Why Are Medical Aesthetic Institutions Keen on Developing Customized Products? The Most Critical Factor Is Gaining Pricing Power to Secure Higher Profits.

The founder of a medical aesthetics institution in Shanghai once stated at a product launch event,Frequent price wars in the current medical aesthetics industry have placed immense survival pressure on institutions; while pricing power serves as a corporate moat, medical aesthetics institutions represent a notable exception lacking such power.

With customized products, medical aesthetic institutions gain more flexible pricing power over their private-label brands.The supply model of upstream enterprises has shifted from the traditional “product + brand” approach to “exclusive products,” meaning that medical aesthetic institutions can now source products at lower costs, thereby achieving greater profit margins.

Meanwhile, after years of operation, large medical aesthetic institutions, as well as some renowned physicians within them, have established influence in the minds of certain consumers. The endorsement by their proprietary brands can facilitate these consumers’ product purchase decisions. For instance, when promoting Heyisha and Helaili hyaluronic acid fillers, Mylike emphasized that these two products were carefully selected by Mylike and customized to meet the needs of its members. This undoubtedly reflects the institution’s emphasis on and strategic management of its consumer membership base.

Why Are Customized Products Concentrated on Hyaluronic Acid? This is primarily because companies represented by Bloomage Biotech, Haohai Biological Technology, and Imeik have driven a surge in hyaluronic acid products. As of November 2024, 34 hyaluronic acid injectable products from 15 domestic companies had received regulatory approval in China. With each product available in multiple specifications, there is a substantial number of brandable options, providing ample choices for customized products.

Status of Approved Hyaluronic Acid Injection Products, Source: National Medical Products Administration

Certainly, the customized model is also extending to other injectable products. For example, United Regal collaborated with Jinbo Bio to launch the Xinfuyuan Humanized Collagen Skin Booster. In 2024, United Regal further introduced the Silanduo “Beauty of Super Sequence” product set, which comprises two main components: HAP (hydroxyapatite bioceramic) and Silanduo No. 2 Hyaluronic Acid. The HAP is supplied by Bei’erkang Bio, while the hyaluronic acid is provided by Qisheng Bio, a subsidiary of Haohai Biological Technology.

Overall, against the backdrop of rising market penetration and increasing product diversification in the injectable medical aesthetics sector, customized products have become a key strategy for large medical aesthetic institutions to drive short-term transformation.

With the rise of the customization model, leading domestic hyaluronic acid enterprises have adopted a business strategy that runs original manufacturer brands alongside custom brands, while continuously launching new products.

Previously, Bloomage Biotech’s main hyaluronic acid injection brands were “Runbaiyan” and “Runzhi.” Among them, the core brand Runzhi has successively launched a matrix of products targeting different skin layer needs based on the concept of layered anti-aging, including Runzhi Natural, No. 2, No. 3, and No. 5, as well as a micro-cross-linked product—Runzhi Baby Needle—designed for skin rejuvenation and long-lasting solutions.

In July 2024, Bloomage Biotech’s composite sodium hyaluronate solution for injection was approved for market launch. It is indicated for intradermal injection to correct moderate to severe horizontal neck lines, marking the second hyaluronic acid-based injectable for neck wrinkles following Hi-Ti.

Haohai Biotech has previously launched its first-generation hyaluronic acid product, “Haiwei,” primarily positioned as an entry-level product for mass-market adoption; its second-generation hyaluronic acid product, “Jiaolan,” is targeted at the mid-to-high-end market, emphasizing “dynamic filling” capabilities; and its third-generation hyaluronic acid product, “Haimai,” features a linear, non-particulate structure, positioned in the high-end segment with a focus on “precise contouring.” Notably, in 2023, “Jiaolan” hyaluronic acid completed its registration change, expanding its indications to include “subcutaneous (or submucosal) injection into the vermilion body and vermilion border of the lips for lip augmentation to increase lip tissue volume.”

Also in July 2024, Haohai Biological Technology’s fourth-generation hyaluronic acid product, the organically cross-linked “Hai Mei Yue Bai,” received regulatory approval. It will form a product portfolio with the first three generations of hyaluronic acid products, featuring differentiated functionalities and pricing strategies.

From the perspective of medical device companies, hyaluronic acid has been partially substituted by various injectable regenerative material products launched in recent years, leading to a slowdown in its growth rate. Meanwhile, the number of hyaluronic acid products itself continues to increase, resulting in intense market saturation and competition.Upstream companies continue to maintain their market share through customized models, and shifting part of the brand operation pressure onto institutions is also a viable strategy.

Meanwhile, building on the years-long operation of their existing brands, enterprises must continuously develop next-generation products or expand indications to maintain technological competitiveness.

There is another key player in the domestic hyaluronic acid market: imported products. Clearly,Due to production area restrictions, imported products are virtually unable to participate in the customization model. Therefore, theoretically, imported products are the most directly impacted under this model.

As of November 2024, a total of 39 imported hyaluronic acid injection products from 17 companies have been approved in China. Major brands include Juvederm under Allergan, Restylane under Galderma, and Yvoire under LG.

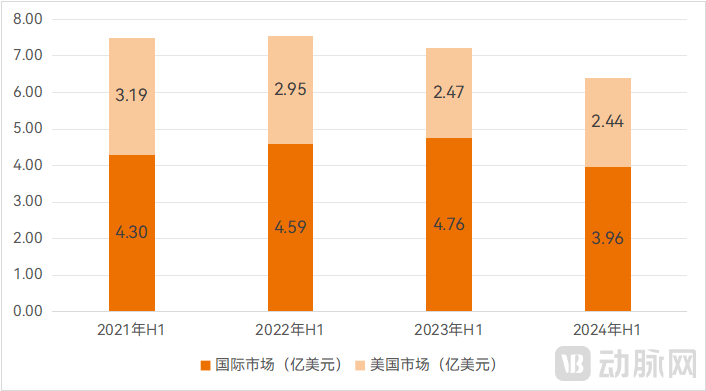

According to AbbVie’s (the parent company of Allergan) financial reports, Juvederm has experienced a significant decline in revenue in international markets since 2024.

Looking at Juvederm’s revenue performance in recent years, the U.S. market has been on a downward trend due to demand factors; meanwhile, international markets had been growing in previous years but declined to $396 million in the first half of 2024, representing a year-on-year decrease of 16.8% based on actual exchange rates. According to the latest financial data, this downward trend continued through the first three quarters ending September 2024.

Changes in Juvederm's Global Revenue, Data Source: AbbVie Financial Reports

China has long occupied a significant position in the global medical aesthetics market, and its vast population base means that shifts in the Chinese market will have a direct impact on the global performance of many multinational corporations. Although AbbVie attributed the decline in its 2024 international market revenue to “a decrease in consumer demand in international markets” in its financial report without specifying further reasons, it is difficult to argue that this is entirely unrelated to the prevalence of domestically customized products in China.

In this context, imported products are consolidating their market position through strategies such as more precise customer targeting and a greater emphasis on personalized treatment.

It is reported that in March 2024, Allergan launched the Juvederm “2024 Starry Sky Initiative.” This one-year program targets thousands of small and medium-sized medical aesthetic institutions across 26 provinces, municipalities, and autonomous regions in China. It focuses on exchange and empowerment in three key areas: physician training, institutional operations, and professional consulting, with the aim of enhancing their specialized, compliant, and high-quality service capabilities.

In fact, small and medium-sized medical aesthetic institutions also find it difficult to participate in the customized model. Due to limited patient flow and even lower treatment volumes for individual products, these institutions have weak bargaining power. In the short term, they will continue to rely primarily on products from original equipment manufacturers (OEMs).

Furthermore, following the approval of Restylane Defyne in 2023 as the first hyaluronic acid product in China with indications for the mandibular region, another hyaluronic acid product utilizing OBT gel technology, Restylane Contour, was launched in the Chinese market in 2024. This new product can be combined with other products in the Restylane portfolio, employing precise dosing to individually address needs such as mid-face lifting and volumization.

Regardless, imported products remain a significant component of the hyaluronic acid market, offering consumers more time-tested options. On major online medical aesthetics platforms, imported brands continue to top the best-seller lists and are heavily promoted by many medical aesthetics institutions; however, they must respond flexibly to changes in the domestic market.

Admittedly, the customization model has empowered medical aesthetic institutions with pricing autonomy and higher profit margins. Domestic manufacturers are also motivated to participate in this model, given that original factory brands can coexist with customized products. Imported brands, after further refining their target customer segments, can still maintain their market position.

It seems harmonious, but is that really the case?

In the past, price wars were primarily fought among medical aesthetic institutions. Now, however, a price war involving both these institutions and upstream device manufacturers is quietly emerging, with its direct manifestation being the chaos in the pricing systems for customized products. According to industry insiders,Multiple customized products have exhibited high brand premiums, in some cases far exceeding the prices of original manufacturer brands, with the costs ultimately borne by consumers.

Price Comparison of Select Custom-Branded Hyaluronic Acid Fillers and Original Manufacturer Brands (For General Reference Only; Prices for the Same Brand May Vary by City). Source: Publicly Available Corporate Information, SoYoung App

VCBeat has compiled pricing information for certain customized products based on data from online medical aesthetics platforms, product registration records, and publicly available corporate information. Taking the two hyaluronic acid products listed in the table above as examples (each corresponding to a distinct registration number), different specifications of the same product have been customized under several brands, and even identical specifications have been marketed under different brand names. Notably, for the same specification, the price of a customized brand may be several thousand yuan higher than that of the original manufacturer’s brand.

Aesthetic medicine institutions have another consideration. “Everyone is currently engaged in a price war; when that becomes unsustainable, they turn to customization,”Customized products are sold exclusively, preventing consumers from directly comparing prices with other institutions; strong recommendations from medical aesthetics consultants can significantly influence consumer decision-making.“A doctor who previously worked at a large chain medical aesthetics institution told VCBeat.”In reality, most consumers lack professional knowledge in areas such as medical device registration and indication inquiries. This widespread information asymmetry has become one of the conditions enabling aesthetic medicine institutions to vigorously promote customized products.

Furthermore, when launching products, most medical aesthetic institutions release them under the guise of “new products” labeled as customized, exclusively supplied, or specially researched. However, a review of publicly available data on the approval years of registration certificates for multiple products reveals that most were initially approved between 2016 and 2020. At the time these products were launched by medical aesthetic institutions, there were virtually no new indications added to their registration certificates.

As previously mentioned, leading hyaluronic acid companies continue to actively innovate. For these enterprises, customized products can be considered the “old” in this equation. Although these products have been on the market for an extended period and their safety and efficacy have been extensively validated—indeed a key advantage—does repackaging them as “new wine in old bottles” and marketing them to consumers at premium prices truly constitute “innovation”? When consumers have access to more comprehensive information, will they still pay solely for the label of “customization”? The answer is most likely no.

Let’s review the various stakeholders involved in the customized model one final time: Aesthetic medicine clinics stand to profit; domestic hyaluronic acid companies, leveraging their technological resources, assume dual roles as both brand owners and manufacturers; and multinational corporations can achieve synergistic development with more precisely targeted customer segments. Amidst this fierce competition, a “win-win” scenario may appear feasible for industry players. However, consumers are the inevitable losers: they bear higher costs yet, apart from gaining emotional satisfaction, do not necessarily obtain more product information or better treatment outcomes.

Consumers are the ultimate payers; if products are not designed with consumer benefit in mind, then customized products currently driven by the pursuit of pricing power may ultimately fail on price.Many medical aesthetics practitioners interviewed by VCBeat have noted that consumers are becoming increasingly rational, with a growing proportion of highly educated individuals who place greater emphasis on product mechanisms and quality, as well as physicians’ technical expertise. Furthermore, regardless of the timing, product pricing should be positively correlated with the advancement and irreplaceability of the underlying technology, as well as its efficacy in addressing actual needs. Therefore, developing customized products is not unfeasible; rather, it requires leveraging technical expertise and insights into customer needs from the service side to inform product R&D, thereby creating truly proprietary products that live up to their name.