China's Radiology AI Industry Faces Revenue Model Restructuring After National Healthcare Security Administration Bans Separate AI Diagnostic Fees

On November 20, the National Healthcare Security Administration released the “Guidelines for Establishing Price Items for Radiological Examination Services (Trial),” which not only integrated and standardized existing radiological examination items but also defined the business model for imaging AI.

The policy interpretation article states: “Artificial intelligence technology plays a certain role in assisting diagnosis or improving efficiency in clinical practice, but it cannot yet replace physician diagnosis. In the absence of independent medical service outputs and with the quality utility of assisted diagnosis being difficult to determine,”After collecting fees for the corresponding diagnostic tests, it is inappropriate to charge patients additional fees solely for AI-assisted diagnosis.

In this regard, to support the clinical application of AI-assisted diagnosis while preventing additional financial burden on patients, the project initiation guidelines uniformly arrange an “AI-assisted diagnosis” add-on item under the main category of radiological examinations. In other words, where hospitals utilize artificial intelligence for assisted diagnosis,Apply the same pricing level as the primary item, without duplicate billing.”

Simply put,The National Healthcare Security Administration supports the widespread clinical application of AI-based imaging, but prohibits hospitals from passing on the costs associated with AI utilization to patients.

Amid the new policies, practitioners in the AI medical imaging sector have mixed feelings. On the positive side, the National Healthcare Security Administration has officially recognized AI’s contributions to clinical practice and raised awareness among relevant stakeholders about its use. However, concerns remain: given that the introduction of AI does not generate direct revenue for hospitals, will the newly issued guidelines be sufficient to sustain the revenue growth of the AI medical imaging industry?

In the early stages of AI development in medical imaging, startups charted a course for medical AI, aiming to secure market access, pricing approval, and inclusion in national health insurance coverage one by one.Form an independent medical device product, ultimately achieving case-based payment for patients and creating a closed-loop solution implemented in hospitals.

Such business models have precedents; for instance, Digital Diagnostics in the United States charges $55 per analysis for diabetic retinopathy (2022 data, same below), and Viz.AI charges $1,040 per test for large vessel occlusion detection. These examples have long served as a compass for domestic medical imaging AI companies.

Following this path, companies such as Keya Medical and Airdoc have begun to extensively promote price approval and inclusion in medical insurance coverage after obtaining Class III medical device certificates for their products. Over the past few years, related products have successfully been included in the provincial price catalogs of more than ten provinces and municipalities, theoretically making out-of-pocket payment by patients possible. However, they have encountered challenges in the more critical area of basic medical insurance reimbursement, having been included in the coverage scope only in a very limited number of regions, far from achieving scale.

The reasons for the failure of this pathway are multifaceted. Over the past few years, hospitals, pricing structures, and payment models have been jointly promoted by enterprises, governments, and regulatory agencies; however, overall efforts have lacked sufficient proactivity.

On one hand, the large-scale price approval and payment model validation in medical insurance inclusion both require companies to invest significant human and material resources. However, the outcomes do not guarantee that products will achieve substantial commercial success, thereby limiting the pace of advancement.

On the other hand, market access for pricing and reimbursement are akin to public goods, creating a scenario where early investors bear the costs while others free-ride. Consequently, companies that pioneer related research tend to conceal interim findings, which restricts the overall pace of industry advancement and often leads to redundant research on single products.

Today, the introduction of new policies has undoubtedly shattered the dream of medical imaging AI, as a standalone product, to secure case-based reimbursement under medical insurance. The sustainable business models common to pharmaceuticals and medical devices may never materialize in the field of medical imaging AI.

Although the new policy has eliminated a theoretically significant pathway for commercial monetization, it has not significantly undermined the profitability of medical imaging AI companies; rather, it has charted a clear course for their long-term development.

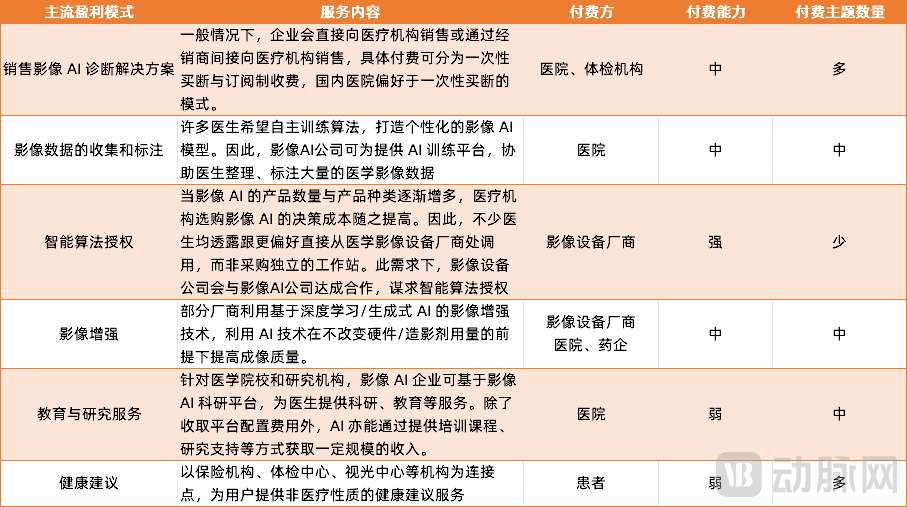

Let us first discuss the impact of policies. At present, the revenue of medical imaging AI companies is minimally related to health insurance reimbursement. These companies primarily rely on tendering processes to sell their imaging AI solutions to hospitals, either through outright purchase or Software-as-a-Service (SaaS) models. Furthermore, medical imaging has long been a significant source of academic publications; many hospitals and physicians are eager to collaborate with AI enterprises to enhance both the quantity and quality of their scientific research outputs.

Furthermore, collaborating with imaging equipment manufacturers and paying them directly is also an important revenue stream for medical AI companies. This represents a win-win partnership. Imaging equipment companies can rapidly gain access to a wide range of applications through intelligent algorithm licensing, effectively enhancing the competitiveness of their products. Hospitals also prefer to invoke algorithms directly from the platforms provided by imaging equipment manufacturers, thereby boosting the revenue of medical AI companies. In the early years, United Imaging Group specifically established United Imaging Intelligence to tackle imaging challenges across various clinical scenarios, and it has since become one of the largest and most comprehensive medical AI companies in terms of product portfolio. Subsequently, multinational corporations (MNCs) such as GE Healthcare and Philips Healthcare have also extensively built AI ecosystems in China, attracting a large number of high-quality partners.

Leveraging these diversified strategies, imaging AI companies have successfully deployed their solutions in a large number of hospitals without medical insurance reimbursement support, generating hundreds of millions in revenue.

Major Revenue Sources for Medical Imaging AI Companies

Revisiting Policy Guidance for Imaging AI. The article mentions “supporting the clinical application of AI-assisted diagnosis,” which serves as an affirmation of the clinical use of artificial intelligence. In practice, some hospitals in China have already established separate billing items for imaging AI services. After utilizing imaging AI for assisted diagnosis, hospitals can allocate a portion of the revenue as performance-based compensation to remunerate imaging AI providers for their services.

For instance, Shandong Province has undertaken significant innovative work in the design of AI service pricing. Some hospitals utilize AI for early-stage cancer screening via CT scans; while the official price standard is RMB 340 per anatomical site, this fee includes RMB 50 for AI-assisted screening and diagnostic services, which are not covered by medical insurance.

However, it is also important to note that AI imaging companies are unlikely to realize the benefits of the new policies in the short term. Currently, only a small number of hospitals have adopted performance-based payment models for AI, and the range of covered examination items remains quite limited. Therefore, the transition from small-scale pilots to large-scale implementation may take several years, necessitating more refined policies to facilitate the establishment of a new payment system.

Furthermore, with the closure of the reimbursement pathway based on case-based payment for medical insurance, imaging AI companies have become increasingly reliant on hospitals and medical imaging equipment manufacturers as payers. Constrained by the intensified anti-corruption campaign in the healthcare sector, the total procurement value of medical equipment by hospitals in the first half of 2024 was nearly halved, with the winning bid amounts for magnetic resonance imaging (MRI) and computed tomography (CT) systems amounting to only 60% of those in the same period last year. Under these circumstances, the pressure faced by upstream imaging equipment manufacturers will be directly transmitted to midstream imaging AI companies, whose revenues will experience a certain degree of decline before the release of pent-up demand for equipment procurement.

At the end of the article published by the National Healthcare Security Administration, it was stated: “The inclusion of ‘AI-assisted diagnosis’ as an add-on item under the main category of radiological examinations in the Project Initiation Guidelines is intended toIt reflects the functional positioning of artificial intelligence technology in enhancing quality and efficiency, rather than increasing costs.”

This statement applies not only to imaging AI, but perhaps also to the various forms of artificial intelligence within the healthcare industry.

The “Notice on Regulating the Use and Pricing of Surgical Robot-Assisted Operating Systems” issued by the Hunan Provincial Healthcare Security Administration in 2022 standardized the forms and pricing of surgical robots through policy guidance, essentially aiming toOn the premise of ensuring reasonable medical insurance expenditures and reasonable patient out-of-pocket costsGuide the orderly development of relevant markets and prevent enterprises and hospitals from “innovating” billing items through mere software solutions.

The recent introduction of the “Guidelines for Establishing Price Items for Radiological Examinations (Trial)” serves a similar purpose. It defines the role of imaging AI, aiming to create incremental value for the entire healthcare system by helping hospitals improve quality and efficiency, thereby demonstrating its own worth.

An analysis of the two policies reveals that policymakers are less inclined to support companies in marketing AI as a standalone product or its primary selling point. Instead, they envision AI functioning akin to autonomous navigation in the automotive industry or quality control in industrial manufacturing—integrated as a component of devices or systems to enhance their overall value.

In practice, the so-called “leading medical imaging AI companies” have long shed the “imaging AI” label, developing highly intelligent hardware or systems and transforming into full-fledged medical device companies or healthcare IT firms.

Deepwise Medical has already achieved significant success in the field of medical IT. With the rise of large models, the company has focused on hospital data management, developing a multimodal data governance engine that covers the entire process of data acquisition, governance, and labeling, as well as a multimodal AI engine incorporating large language models, general-purpose imaging models, and multimodal large models. Furthermore, it offers various capability-opening models, including open access to full-lifecycle governance capabilities, customized data services, and multimodal AI modeling capabilities.

Furthermore, addressing the urgent need for data asset solutions in hospitals, Deepwise Medical also integrates AI into its offerings, providing intelligent products and services related to asset management for scenarios such as smart hospital administration, smart research, smart clinical practice, and AI innovation centers.

In the medical device sector, both Shukun Technology and Infervision are strategically expanding their presence. Leveraging AI, Shukun Technology has independently developed native ultrasound hardware systems, including the “Turing Brain” and “Turing AR,” which enable deep integration with intelligent algorithms. These solutions not only consolidate information from all organs during ultrasound examinations and provide real-time visualization of lesion characteristics, but also enhance physician workflow by eliminating the need for a “second screen” in clinical practice.

From Shukun Technology’s perspective, the synergistic integration of software and hardware not only redefines user experience but also serves as a key driver for AI to continuously push technological boundaries. In the future, every piece of hardware will transition from the industrial era into the AI era, with every step and every second of interaction between physicians and devices empowered by AI.

Infervision has entered the surgical robotics sector, deeply integrating imaging AI into its hardware. For instance, the company’s self-developed AI-guided robotic system, “Dragon’s Eye® Puncture Surgical Robot,” incorporates AI-driven intelligent technologies on top of magnetic navigation guidance. Empowered by intelligent algorithms, Infervision enables fully automated identification and reconstruction of tissue lesions, followed by automatic surgical path planning, puncture guidance, and post-ablation assessment, thereby effectively assisting physicians in performing percutaneous puncture procedures with greater accuracy and efficiency.

By this juncture, former AI imaging companies have all completed their self-driven value restructuring. The curtain fall on the old era corresponds to the dawn of a new age for AI enterprises.