Amid Surge in License-Out Deals, These Biotechs Prove License-In Can Succeed

Everest Medicines

Developer of Innovative Therapies

Zai Lab

Innovative Global Biopharmaceutical Company

The long-neglected license-in business model is reaching a turning point in its development.

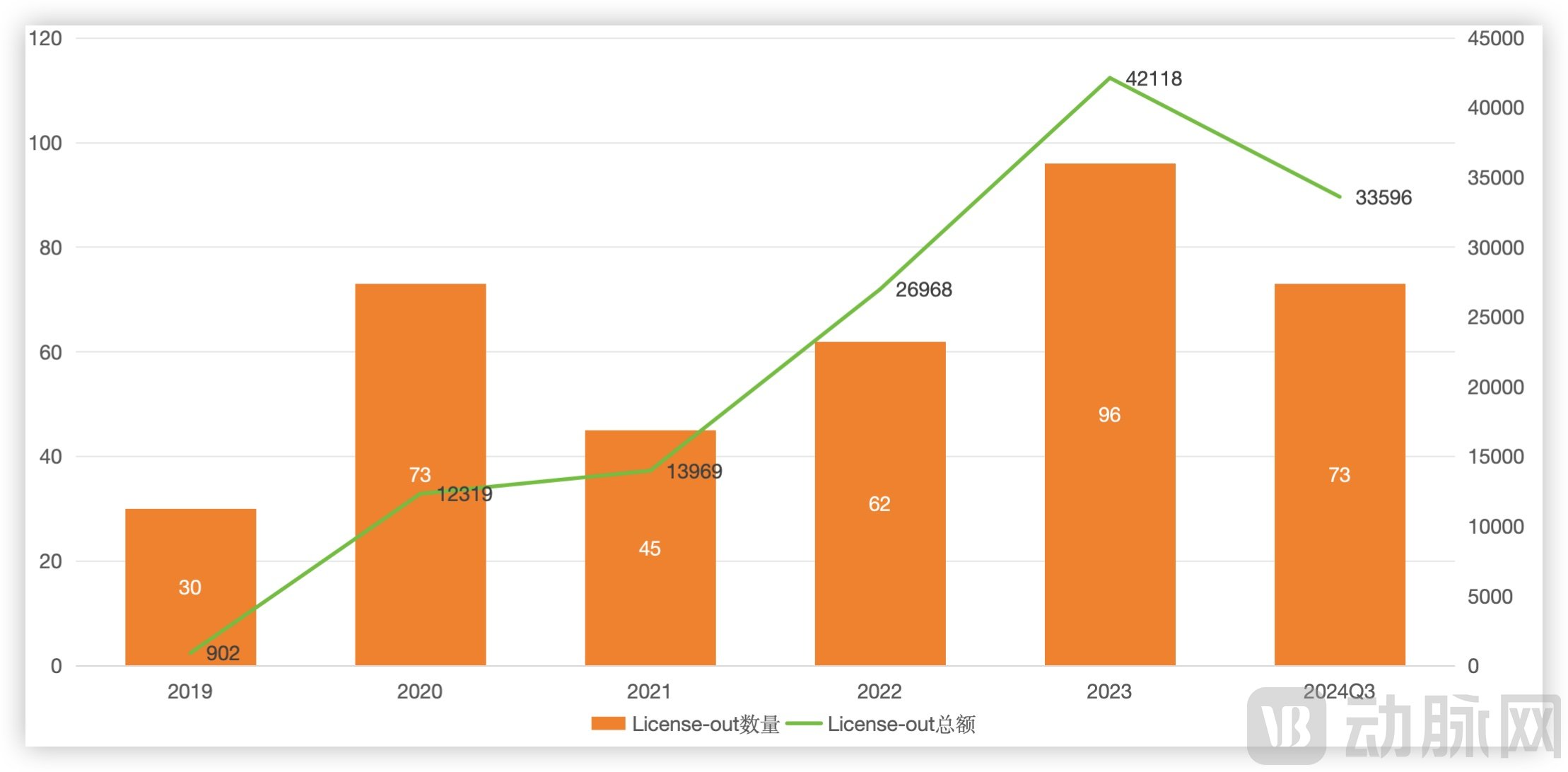

In recent years, under pressure to achieve profitability, an increasing number of biotech companies have chosen to license out their self-developed pipelines to secure upfront and milestone payments, thereby boosting cash flow to sustain business operations. Data on domestic license-out transactions in recent years also indicate that such deals among Chinese biotech firms have entered a phase characterized by simultaneous growth in both volume and value. In the first three quarters of this year, the number of out-licensing projects increased by 11 year-on-year, while the total disclosed transaction value surged by 100% compared to the same period last year.

License-out Deals by Chinese Pharmaceutical Companies in Recent Years (Unit: Million USD), Data Source: Guosheng Securities

More notably, amid the frequent emergence of out-licensing deals, the controversial license-in business model has also begun to prove viable, with several pharmaceutical companies championing this approach demonstrating its feasibility through their own tangible progress.

Profitability is an inescapable topic for biotech companies.

Whether through the commercial sales of self-developed products or by out-licensing their pipelines to secure upfront payments, biotech companies are striving to turn losses into profits. Amidst this effort, the license-in strategy appears increasingly marginalized, overshadowed by the successive waves of acclaim surrounding license-out deals.

Previously, the market harbored doubts about the license-in model. Although it enables companies to rapidly acquire pipelines and shorten R&D cycles, this path appeared more suitable for large pharmaceutical companies with higher risk tolerance, rather than biotech firms with weaker risk-bearing capabilities.

Now, biotech companies represented by Everest Medicines and Zai Lab are proving with their concrete actions that this path is viable.

Taking Everest Medicines, a representative domestic enterprise adopting the License-in model, as an example, it achieved a significant year-on-year revenue increase of 884% in 2023. In the first half of 2024, its total revenue reached RMB 302 million, marking a substantial quarter-on-quarter growth of 158% compared to the second half of 2023, while also achieving profitability at the commercialization level.

Specifically, Everest Medicines’ primary revenue stems from two products licensed from overseas: Yijia (eravacycline) and Nefecon. Yijia generated RMB 134 million in revenue in the first half of 2024, bringing its cumulative revenue to RMB 233 million since its commercial launch last July. Meanwhile, Nefecon achieved sales of RMB 167 million within just one month following its commercial launch in May this year. Since the announcement of its semi-annual results, Everest Medicines’ stock price has risen by more than 80% over the subsequent two months.

Zai Lab, another company focusing on the License-in model, has also reached a turning point toward profitability. In the first three quarters of 2024, Zai Lab achieved total revenue of $290 million, a year-on-year increase of 44.32%. From 2021 to 2023, Zai Lab’s losses continued to narrow, standing at -$700 million, -$440 million, and -$340 million, respectively. In the first three quarters of this year, the net loss was $175 million, a year-on-year decrease of 26.66%.

The improvement in corporate revenues has also been reflected in the secondary market. As of early November, the share price of Zai Lab’s H-shares exceeded HK$25, doubling from the HK$12 recorded in August of this year. In addition, Zenas BioPharma (Shanghai Zenas Biopharma), a multinational biotech company specializing in immunology and inflammation, successfully listed on the Nasdaq in September, raising approximately US$230 million. Its success is also underpinned by the license-in model.

From a market perspective, as these two companies reach an inflection point in their development, they have also dispelled doubts about the viability of the license-in model, thereby shifting market sentiment toward this approach. The question remains: what drove this change?

Efficiency Is the Foundation of Success or Failure

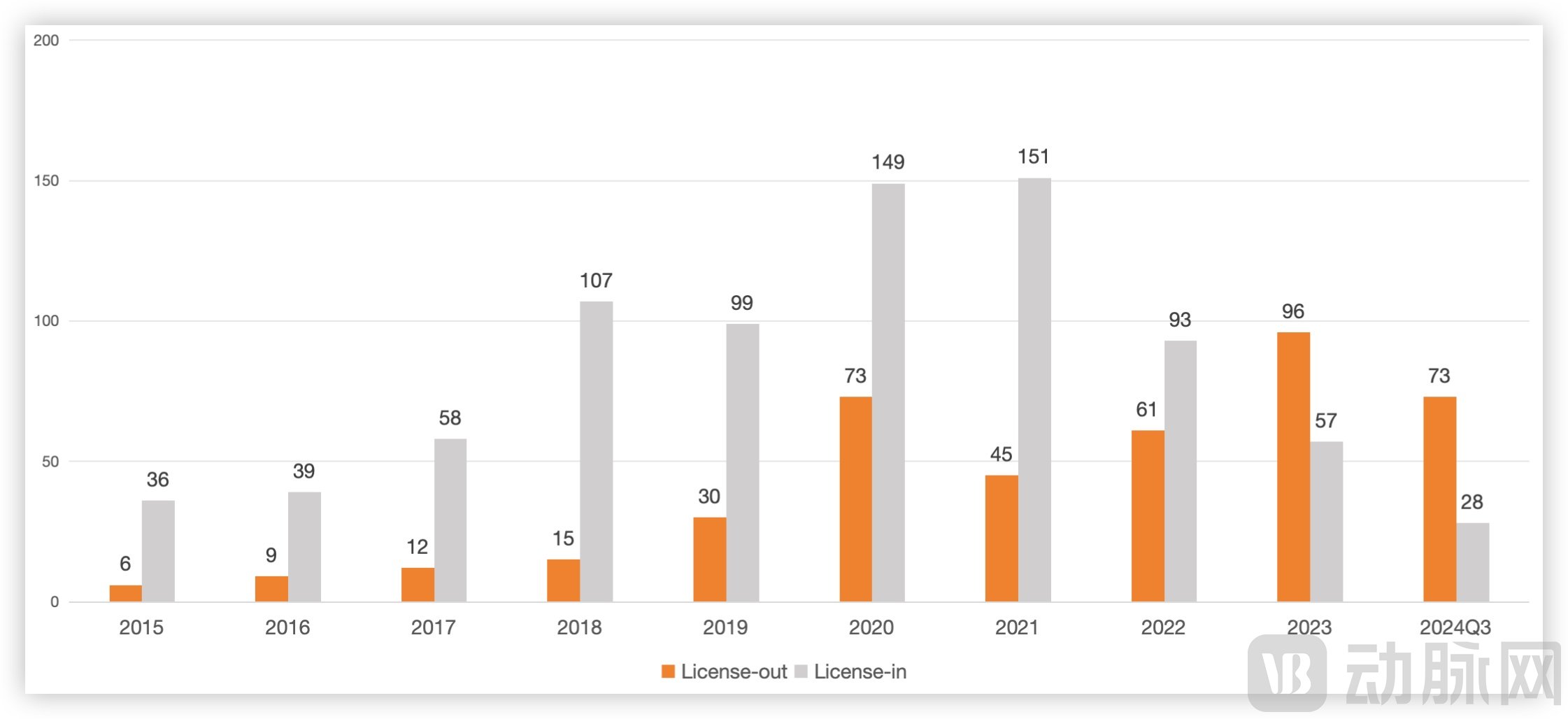

In recent years, business development (BD) strategies of domestic pharmaceutical companies have shifted from the License-in model to the License-out model. In addition to aligning with industry development trends, the inherent drawbacks of the License-in model have also hindered further corporate investment.

2015–2024 Q3: Number of License-in/out Projects by Chinese Pharmaceutical Companies (Data Source: Guosheng Securities)

Although the license-in model allows pharmaceutical companies to bypass the risks associated with the drug discovery phase, thereby reducing overall R&D complexity, rapidly enriching their product pipelines, and shortening time-to-market, challenges related to cost, clinical development, subsequent returns, and sustained competitiveness remain urgent issues that need to be addressed.

For pharmaceutical companies pursuing a license-in strategy, efficiency is the top priority; only by focusing on core business activities and achieving high execution efficiency can they successfully break through.

Take Everest Medicines as an example. In 2022, the company returned to Gilead Sciences the exclusive rights for the development and commercialization of Trodelvy (sacituzumab govitecan)—its only product approved for marketing in China for less than three months—in Greater China, South Korea, and select Southeast Asian countries. Although the transaction yielded $300 million, it sparked controversy in the secondary market, with the company’s stock price plunging more than 90% from its peak.

The rationale behind this decision was Everest Medicines’ desire to avoid the hyper-competitive oncology sector and instead focus its product portfolio on nephrology, anti-infectives, and autoimmune diseases—therapeutic areas with substantial market potential sufficient to drive the company’s revenue. Subsequent developments have validated that this strategic retrenchment was a sound choice; without such business focus, a turnaround in performance would not have been possible.

However, efficiency alone is not enough. Niraparib, introduced by Zai Lab in 2018, was successfully launched by the end of that year, demonstrating remarkable efficiency. Moreover, an increasing number of drugs have since received approval. Yet, the anticipated blockbuster drug has failed to materialize. This indicates that factors beyond efficiency are also required.

Differentiation Is the Foundation of Competitive Strength

Only products with differentiated advantages can achieve a smooth commercialization path.

In 2023, Everest Medicines’ Yijia (eravacycline) and Nefecon were approved in July and November, respectively. Eravacycline, the world’s first fluorocycline-class novel antibiotic, was licensed by Everest Medicines from Tetraphase in 2018 and had previously been approved in the United States, the European Union, the United Kingdom, Singapore, and other regions for the treatment of complicated intra-abdominal infections (cIAI). Nefecon is the only disease-modifying therapy available in China for the treatment of primary IgA nephropathy in adults, obtained through an exclusive licensing agreement between Everest Medicines and Calliditas.

Yijia has received positive reviews since its market launch and has been included in multiple clinical guidelines and expert consensuses, such as the 2023 Chinese “Guidelines for Diagnosis, Treatment, Prevention, and Control of Carbapenem-Resistant Organism (CRO) Infections.” Leveraging its status as the world’s first etiology-targeted therapy for IgA nephropathy, Nefecon has been incorporated into the “KDIGO 2024 Clinical Practice Guideline for the Management of IgA Nephropathy and IgA Vasculitis (Public Review Draft)” by Kidney Disease: Improving Global Outcomes (KDIGO).

Zai Lab’s inflection point in development has also been driven by the emergence of differentiated products.

Taking Vyvgart, approved in 2023, as an example, it generated $10 million in revenue within four months of launch. Its revenue reached $36.4 million in the first half of 2024, prompting Zai Lab to raise its 2024 sales guidance from $70 million to $80 million.

Vyvgart was acquired by Zai Lab from Argenx in 2021 for an upfront payment and milestone payments totaling $175 million. In the first three quarters of this year, Argenx generated $1.449 billion in revenue from Vyvgart, including $573 million in Q3 2024, representing a 74% year-over-year increase.

Vyvgart alleviates various pathogenic IgG-mediated autoimmune diseases by blocking the binding of FcRn to IgG, thereby inhibiting IgG recycling. It was approved by the FDA in 2021 for the treatment of anti-acetylcholine receptor (AChR) antibody-positive generalized myasthenia gravis (gMG) in adults.

Although the annual global incidence of myasthenia gravis (MG) is not high, the cumulative patient population exceeds 700,000 due to its chronic nature. Previously, there were no highly effective targeted therapies for MG; treatment primarily relied on non-targeted agents such as glucocorticoids and immunosuppressants, which had limitations in terms of long-term disease control and safety.

On the other hand, with the launch of innovative drugs for myasthenia gravis, market demand is surging. According to Frost & Sullivan data, the global market for myasthenia gravis therapeutics is projected to grow from $1.26 billion in 2020 to $3.048 billion in 2025, representing a compound annual growth rate (CAGR) of 19.3%.

More importantly, Vyvgart’s potential extends far beyond its current scope. Argenx aims to expand its indications to 15 conditions and has sequentially initiated clinical trials, while Zai Lab is closely following suit. This strategic progress is a key reason why the market holds a favorable outlook on its prospects.

Both Yijia and Vyvgart have demonstrated that product differentiation is a critical foundation for successful commercialization, while the ability to identify differentiated products constitutes the core competency of license-in strategies.

Product Selection Capability Is the Fulcrum

For License-in deals, selecting the right asset is important, but timing the selection is equally critical.

Whether it is Yijia and Nefecon, as essential therapies that fill market gaps, driving corporate performance growth, or Vyvgart, which has avoided the fiercely competitive areas of oncology and chronic diseases dominated by multinational corporations (MNCs) by pursuing source innovation and targeting differentiated indications, the rationale behind these choices reflects their deep insight into the License-in model.

The development of innovative drugs is a perilous journey fraught with risk; a failure at any stage can nullify all prior efforts.

Everest Medicines adopts a selection strategy grounded in commercial prospects and clinical insights. It evaluates whether a therapeutic area presents significant unmet clinical needs, particularly the urgency of patient demand, while also considering the future competitive landscape, physicians’ treatment preferences, and product accessibility. Once these factors yield relatively definitive answers, the company leverages clinical insights to identify suitable products under development.

More importantly, the judgment was made more than five years ahead of the market.

Judging from the results, Everest Medicines’ product selection capability is undoubtedly commendable. Whether it is Icariin or Nefecon, or even the abandoned sacituzumab govitecan, none of these would have generated hundreds of millions of dollars in cash to help the company navigate the challenging period prior to new product launches if they lacked market prospects.

Looking back at the projects licensed by Zai Lab, although they cover areas such as oncology, infectious diseases, central nervous system disorders, and autoimmune diseases—lacking the focused approach of Everest Medicines—their collaboration partners were subsequently acquired by multinational corporations (MNCs).

For instance, in 2016, Zai Lab licensed niraparib from Tesaro, which was subsequently acquired by GSK for $5.1 billion in 2018. Similar scenarios have unfolded with other partners, including Five Prime, Turning Point Therapeutics, Mirati, and Karuna.

Zai Lab’s Major License-in Projects in Recent Years, Compiled from Public Information

The acquisition by multinational corporations (MNCs) undoubtedly serves as an endorsement of the prospects for the projects introduced by Zai Lab, further attesting to its drug selection capabilities.

On the other hand, their product selection logic can also be discerned from their corporate product pipelines.

Taking Everest Medicines as an example, its key strategic focus areas include kidney diseases, infectious diseases, autoimmune disorders, and mRNA platforms, with significant arrangements made according to commercialization stages.

Everest Medicines’ Product Pipeline, Image Source: Corporate Official Website

Cefepime-taniborbactam and etrasimod, the successors to Yijia, are both in Phase 3 clinical trials. Cefepime-taniborbactam is a β-lactam/β-lactamase inhibitor (BL/BLI) antibacterial agent indicated for the treatment of serious bacterial infections caused by multidrug-resistant Gram-negative bacteria. Its New Drug Application (NDA) has been accepted by the U.S. FDA for priority review and has also been included in the priority review list in China.

Etrasimod received FDA NDA approval in October 2023 for the treatment of adult patients with moderately to severely active ulcerative colitis (UC). Meanwhile, the induction phase of the Phase 3 multicenter clinical study of etrasimod for UC in Asia also achieved positive top-line results, with subsequent studies being accelerated. The next-stage candidates, zetomipzomib and EVER001, are also under active development.

Of course, as the License-in model gradually proves viable, both Everest Medicines and Zai Lab are also embarking on the development of self-developed drugs, with the expectation of establishing an advanced dual-engine model driven by “in-house R&D + external collaborations” in the future.

While Everest Medicines has set a high benchmark, the delisting of LianTuo Bio serves as a cautionary tale; several challenges must still be addressed for the license-in model to achieve sustainable success.

If Everest Medicines and Zai Lab experienced numerous setbacks during their development, then the growth of Zenas BioPharma serves as a typical case study of the license-in model.

Zenas is a multinational (U.S.-China) biopharmaceutical company focused on immunology and inflammation. Shanghai Zenas BioPharma Co., Ltd. was established in 2021. Its founder and Executive Chairman, Lonnie Moulder, serves as a director at companies such as Zai Lab and Trevena, and previously founded Tesaro, which was acquired by GSK for $5.1 billion.

Currently, Zenas’ core product is obexelimab, a drug licensed from Xencor. Notably, obexelimab had previously been licensed by Xencor to Amgen, but was later returned by Amgen. After acquiring the rights to obexelimab, Zenas actively advanced its clinical development and announced robust Phase 2 clinical data in 2023.

The promising data attracted the attention of Bristol Myers Squibb, leading both parties to sign an agreement for the development and commercialization of obexelimab for the treatment of autoimmune diseases in Japan, South Korea, Singapore, Australia, and other regions. Zenas will receive a $50 million upfront payment, an equity investment from Bristol Myers Squibb, and potential milestone payments totaling $149.5 million. In addition to obexelimab, Zenas has four in-licensed drug pipelines, also primarily indicated for immune and inflammatory diseases.

Driven by the smooth advancement of its pipeline and the efforts of its management team, Zenas completed three rounds of financing within three years of its establishment, raising approximately $359 million, and listed on the Nasdaq this September with an IPO size of $225 million.

Looking at Zenas’ development trajectory, several questions are worth considering.

First, BD capabilities include the ability to raise capital for business development purposes. Essentially, the License-in model represents competition on the supply side of innovative drug intellectual property (IP). The core competitiveness of participating pharmaceutical companies lies in whether they have sufficient cash flow, as only adequate cash flow can sustain their operations.

Next is clinical advancement capability. Unlike multinational corporations (MNCs), which have sufficient room for error, license-in deals for biotech companies can be viewed as a form of venture capital investment. After acquiring drug intellectual property (IP) with capital support, the key issue is whether rapid clinical advancement can be achieved to enhance pipeline value. This is particularly critical for Chinese pharmaceutical companies: when introducing drugs from high-priced overseas markets into the domestic market, where payment capacity is relatively weaker, failure to advance quickly will trap them in a vicious cycle.

The final stage is commercialization. Multinational corporations (MNCs) possess established, top-tier sales teams that can rapidly penetrate the market upon drug approval. In contrast, biotech companies typically license in products first and then build their commercialization teams. However, this approach often leads to a mismatch between the sales network and the number of drugs; maintaining a nationwide sales network to promote only a few products results in uncontrollable costs. Consequently, companies like Zai Lab have launched contract sales organization (CSO) businesses, aiming to dilute marketing team costs by distributing other companies’ products.

Of course, the license-in model is closely tied to the broader market environment. When market valuations are low, the license-in model offers greater cost-effectiveness, making it easier to acquire promising pipelines at a lower cost. Conversely, when market valuations are high, license-in may be less cost-effective than in-house R&D. For startups, license-in can accelerate product development; however, relying solely on this approach will inevitably lead to growth bottlenecks. After more than a decade of development, China’s innovative drug industry has entered a phase of value realization. At this juncture, the license-in model serves as an important complement, broadening the path for innovation in China’s pharmaceutical sector.