Pharmaceutical M&A Wave Surges: 29 Companies Already Acquired, Top Deal Exceeds $14 Billion

Recently, there has been a surge in the establishment of M&A funds.

According to incomplete statistics from VCBeat, in October 2024, a total of 33 listed companies disclosed announcements regarding the establishment of industrial (M&A) funds, with as many as seven focusing on the healthcare sector. In addition, central state-owned enterprises and state-owned capital entities are also intensifying their efforts, having already launched multiple M&A funds, including the Yizhuang Kangqiao Healthcare M&A Fund with a total size of RMB 3 billion, as well asThe First Pharmaceutical M&A Fund in Central and Western China—Chengdu Rongchuang Pioneer Equity Investment Fund。

This is certainly inseparable from policy-driven momentum. On September 24, the China Securities Regulatory Commission (CSRC) officially released the “Six Measures on Mergers and Acquisitions,” which resonates with the “Nine National Guidelines” issued in April this year. Both initiatives underscore strong support for the M&A market, encouraging and guiding absorption and integration across industrial chains. Therefore, it is foreseeable that M&A and restructuring activities in the capital market will continue to heat up, and the establishment of M&A funds will soon enter a period of explosive growth.

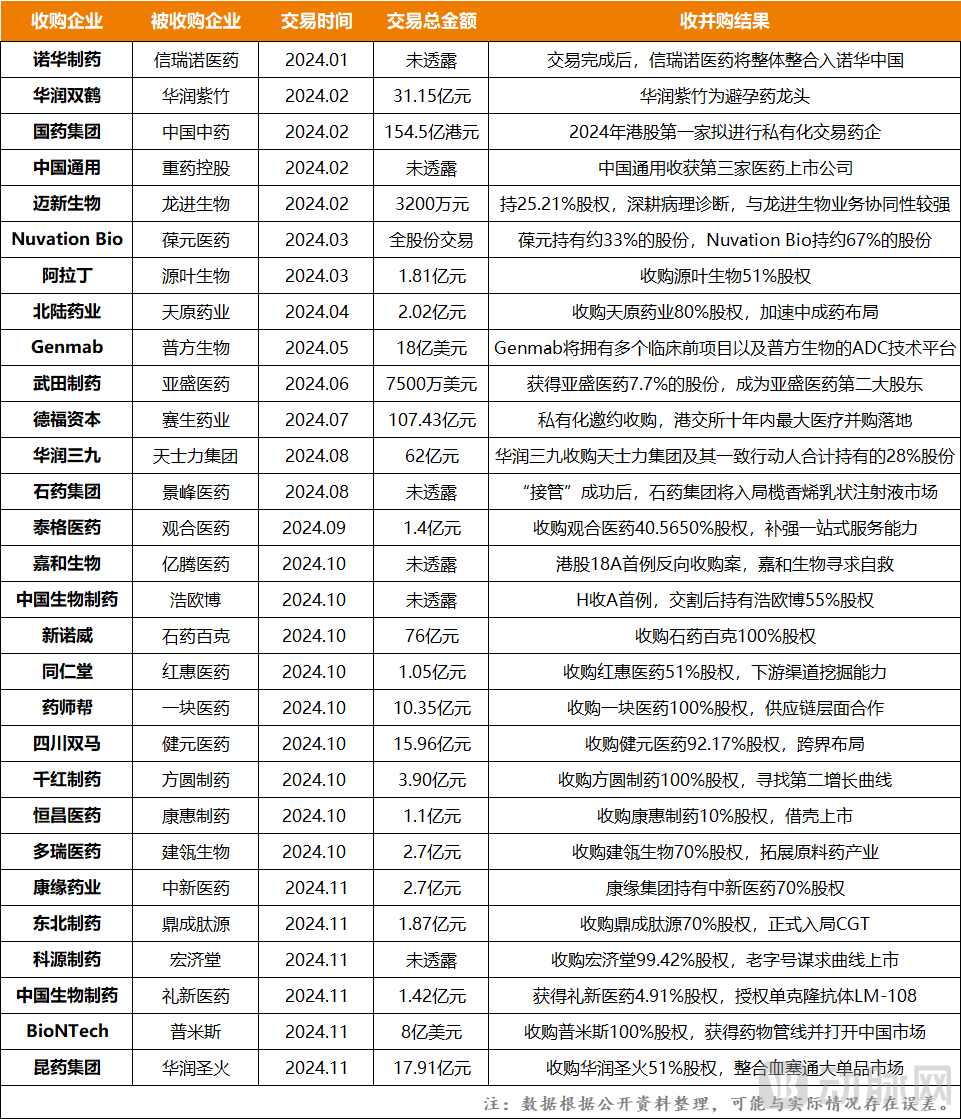

Figure 1. Selected M&A Transactions in China’s Pharmaceutical Sector Since 2024

Figure 1. Selected M&A Transactions in China’s Pharmaceutical Sector Since 2024

Prior to this, mergers and acquisitions (M&A) and consolidation in the pharmaceutical sector had already been gaining momentum beneath the surface. Since the beginning of this year, the volume of integration and restructuring among pharmaceutical companies has surged, giving rise to several historic deals, including"First H-to-A Case"、"HKEX's Largest Healthcare M&A Deal in a Decade"、"First Reverse Takeover Case under Chapter 18A of the Hong Kong Stock Exchange"etc. Meanwhile, M&A rumors have been rampant; for instance, Legend Biotech was reported to have received a takeover offer exceeding $10 billion. Additionally, Sanofi has also been cited as engaging in board-level discussions regarding the high-priced acquisition of Chinese biotech targets.

All signs point to one conclusion:The Wave of M&A in the Pharmaceutical Industry Has Quietly Arrived。

Why Are the Tides Surging?

In December 2023, AstraZeneca announced the acquisition of Gracell Biotechnologies for a total consideration of $1.2 billion,This is the first time an MNC has acquired a Chinese biotech company as a whole.. Since then, a major wave of mergers and acquisitions in China’s biotech sector has officially taken off, with multiple high-profile M&A deals occurring in succession, includingXinnuowei Pharma Acquires CSPC Baike for RMB 7.6 Billion、Genmab Bets $1.8 Billion on Pufeng Biologics, and recentBioNTech Announces Acquisition of Promab Biotechnologies for $950 Million。

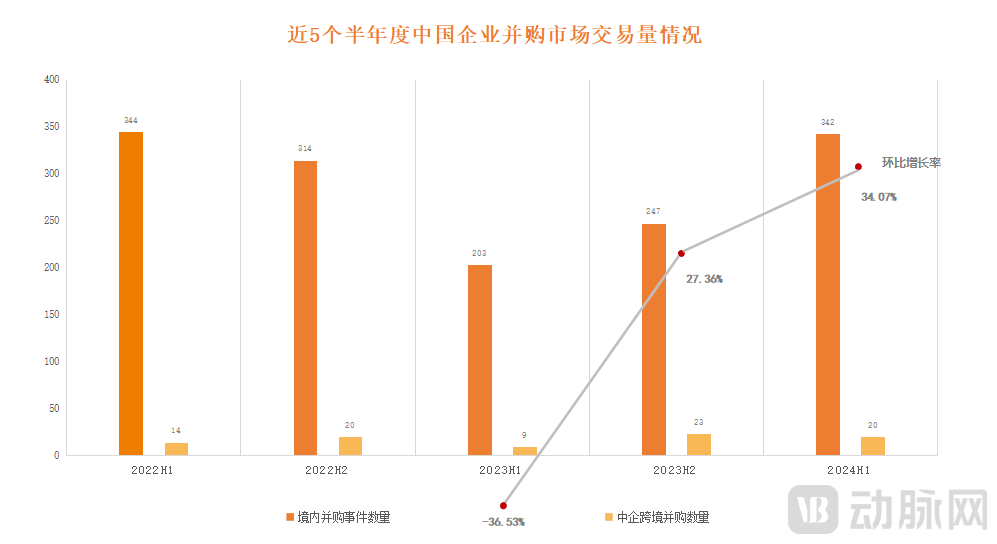

Figure 2. Transaction Volume in the Chinese M&A Market Over the Past Five Semi-Annual Periods (Source: IT Juzi)

Figure 2. Transaction Volume in the Chinese M&A Market Over the Past Five Semi-Annual Periods (Source: IT Juzi)

In fact, this is only the tip of the iceberg; there are many more deals hidden beneath the surface or currently under negotiation. According to data from Wind, as of November 9, 183 listed companies had issued announcements related to major restructuring events this year.Of these, 112 companies emerged after the release of the “Six M&A Measures” policy on September 24., among which as many as 30 are directly related to biomedicine, including Sino Biopharmaceutical, Tigermed, Northeast Pharmaceutical, and Keyuan Pharmaceutical, with a total transaction amount exceeding RMB 10 billion.

This is undoubtedly a rare scene in the history of China’s pharmaceutical industry. Especially amid the current market winter, frequent transactions and substantial capital flows have prompted industry professionals to raise a critical question:Why Has the M&A Wave Emerged Now, and Why Is It So Intense?

This requires a multi-dimensional perspective.First is the target company, i.e., the “seller,” whose immediate need in an M&A transaction is simply to survive.. Affected by the capital winter and the continued tightening of IPO channels, the entire pharmaceutical industry has been seeking more diversified exit paths over the past two years. As time has passed and the market has continuously validated this trend, mergers and acquisitions (M&A) have gained widespread recognition within the industry and are now considered the optimal exit channel at present.

In this regard, a senior industry insider stated, “Although an initial public offering (IPO) remains a form of exit that maximizes returns, with changes in the capital market and increasing complexity within the industry,As it becomes increasingly difficult for many pharmaceutical companies to go public, and with mounting pressure from limited partners (LPs), mergers and acquisitions are gradually becoming an imperative option.. On the other hand, in the process of continuous trial and error,Many pharmaceutical companies are gradually realizing that relying solely on their own technological innovation and market expansion capabilities makes it difficult to advance at the current stage, whereas mergers and acquisitions may enable them to experience a resurgence.。”

Taking *ST Jingfeng as an example, the company had recorded losses for five consecutive years prior to its acquisition. In 2023, its stock was flagged with a delisting risk warning due to negative net assets at the end of the reporting period. The turning point came in August this year. After being formally taken over by CSPC Pharmaceutical Group, *ST Jingfeng hit the daily price limit up 44 times within 52 trading days, emerging as the top-performing stock across both the Shanghai and Shenzhen exchanges in the second half of the year. Its upward momentum even surpassed that of Shenzhen Huaqiang, which had been leading the market rally.

Having discussed the "seller,"Next, let us focus on the “buyer,” i.e., the acquirer, whose core rationale for spending is to “scale up and strengthen its market position.”. Through observation, VCBeat has found that the following keywords generally appear in the current wave of M&A news, including“Expand the [Product/Therapeutic Area] Pipeline,” “Strengthen Capabilities in the [Specific Field],” and “Identify a Second Growth Curve”Wait, their motives are obvious: they hope to expand market share or fill gaps in their own business through acquisitions, thereby achieving a broader industrial layout.

In fact, amid the current complex landscape, although acquirers are predominantly large pharmaceutical companies, they too face survival pressures, such asPatent cliffs, competition in R&D efficiency and market expansion, and the exploration and strategic positioning in incremental marketsWait. Take the “patent cliff,” a major concern for large pharmaceutical companies, as an example. According to BOCOM International, sales of originator drugs drop by more than 60% in the second year after generic or biosimilar competitors enter the market. This undoubtedly represents a substantial loss, which may be mitigated through mergers and acquisitions.

Taking Takeda’s equity investment in Ascentage Pharma as an example, the olverembatinib it acquired can not only succeed its own product ponatinib, whose patent is set to expire in 2026, but also compete with Novartis’ blockbuster drug asciminib in the future. In addition, Genmab, after its high-priced acquisition of ProteoGenix, obtained a next-generation ADC candidate portfolio—including three clinical-stage pipelines and multiple preclinical pipelines—that serves as a timely complement to its existing assets.

In addition to the survival needs of both parties involved in the transactions, the inherent renewal and iteration of the pharmaceutical industry are also major drivers behind the current wave of mergers and acquisitions. Commenting on this, a senior industry expert stated, “Historical experience continues to demonstrate that when an economy undergoes industrial structural adjustment, the confluence of a major technological revolution and key institutional reforms in the capital market will inevitably trigger a large-scale wave of mergers and acquisitions., and the current pharmaceutical sector is precisely at this inflection point of transformationTherefore, mergers and acquisitions (M&A) can not only clear out companies with weak competitiveness but also adjust and restore the valuations of listed pharmaceutical companies, serving as a practical tool for rapidly achieving industrial scale and intensive development.

Three Waves of M&A: Stepping into Different Rivers

In fact, the current wave is not the first M&A surge in China’s pharmaceutical industry; looking back, there were two previous waves, one of which occurred around the year 2000.This phase is a period of rapid expansion, so mergers and acquisitions occur more frequently among peers.. Taking the establishment of CSPC Pharmaceutical Group as an example, it was formed through a strategic alliance among Hebei Pharmaceutical Group, Shijiazhuang No. 1 Pharmaceutical Group, and Shijiazhuang Second Pharmaceutical Enterprise Group.

The second wave of mergers and acquisitions occurred around 2018,During this period, the industry theme has shifted toward transformation and upgrading; consequently, the primary objectives of mergers and acquisitions have been to acquire new technologies or expand into new business sectors.. For instance, M&A serves as a key mechanism for traditional pharmaceutical companies to realize their transition toward innovative drugs; additionally, cross-sector entries into the pharmaceutical industry through M&A by companies in real estate, home appliances, internet, and food sectors were also concentrated during this period. According to incomplete statistics, there were 140 M&A transactions in China’s pharmaceutical and healthcare sector in the first half of 2018, with a total transaction value approaching RMB 66 billion.

The third wave, which is the current one, began in 2023 and has seen a significant surge this year. As with the previous two waves, the essence of this round of M&A remains growth, albeit with many subtle changes.

First, from the perspective of the acquiree, the target assets have gradually shifted from traditional Chinese medicines, generic drugs, and active pharmaceutical ingredients (APIs) to innovative drugs, with stringent screening criteria primarily focusing on clean, high-quality small-cap pharmaceutical companies.In this regard, a senior investor remarked, “Although current M&A policies have been liberalized, this does not mean that all biotech companies are qualified to sit at the negotiation table. High-quality acquisition targets are still subject to stringent criteria: they must possess either advanced technological advantages, a unique business model, or sound financial performance. Even if profits are modest, they should at least avoid substantial monetary losses.”

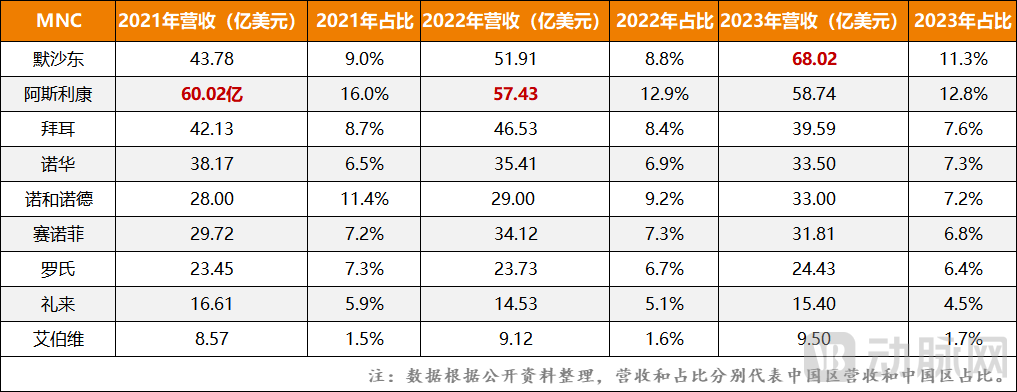

The second change stems from acquirers, with an increasing number of multinational corporations (MNCs) emerging as the primary drivers of M&A activity and aggressively acquiring Chinese innovative drug assets.. It is reported that since AstraZeneca completed its first acquisition, multiple multinational corporations (MNCs) have joined the wave of acquiring Chinese innovative drugs, including Novartis, Takeda, Merck & Co., and Sanofi, all of which have made substantial investments. This trend is primarily driven by two factors:On one hand, some innovative Chinese drugs now possess the strength to directly compete with global cutting-edge technologies and command high market value; on the other hand, multinational corporations (MNCs) can leverage acquisitions to enter the Chinese market, thereby unlocking greater profit potential.。

Figure 3. Changes in Revenue and Proportion of MNCs in China from 2021 to 2023 (Data Source: IT Juzi)

Figure 3. Changes in Revenue and Proportion of MNCs in China from 2021 to 2023 (Data Source: IT Juzi)

Meanwhile,For MNCs, now is also the best time to acquire high-quality Chinese biotech firms at low prices.This is because, impacted by tighter IPO regulations and a capital winter, most domestic biotech companies are currently facing certain cash flow pressures, leading to a relatively strong demand for M&A. Consequently, making slight concessions on price has become a common choice to facilitate deal closures.

The final change is reflected in the forms of mergers and acquisitions, with innovative concepts such as “backdoor listing,” “leveraging external platforms for global expansion,” and “Newco” emerging one after another.First, let’s discuss backdoor listings, taking the merger between GeneHarbor Biopharmaceuticals and Yiteng Medicine—the first reverse takeover under Chapter 18A of the Hong Kong Stock Exchange—as an example. As a leading Contract Sales Organization (CSO) in China, Yiteng Medicine had made multiple unsuccessful attempts to go public in recent years, whereas GeneHarbor Biopharmaceuticals had already listed on the Hong Kong Stock Exchange in 2020. Therefore, upon completion of the transaction, Yiteng Medicine was able to achieve its listing ambition by using GeneHarbor as a shell company. Meanwhile, GeneHarbor, serving as the “shell,” could leverage Yiteng Medicine’s commercialization and R&D capabilities to escape its loss-making predicament.

Next is the “borrowing a ship to go to sea” strategy. Over the past year or two, Chinese pharmaceutical companies have been actively seeking overseas expansion, and mergers and acquisitions (M&A) have provided them with a new pathway. For instance, Hutchmed has leveraged Takeda’s market expertise and distribution channels to achieve strong overseas sales of its innovative drug, fruquintinib. In the first half of this year alone, fruquintinib generated $130.5 million in revenue, equivalent to its total annual sales in the Chinese market in 2023. This is just the beginning. Based on market forecasts for fruquintinib, its peak annual overseas sales are expected to exceed $1.5 billion, suggesting that Hutchmed is well-positioned for continued effortless success in the future.

Finally, we turn to “NewCo.” Typically, a NewCo is established through capital-driven initiatives, wherein pharmaceutical companies spin off their pipelines and license them to the NewCo in exchange for equity stakes and funding. The ultimate exit strategy usually involves selling the company at a premium to multinational corporations (MNCs) or pursuing an initial public offering (IPO). On September 9, Candid Therapeutics, a newly formed entity, acquired two NewCos jointly established by Chinese biotech firms through product licensing agreements: Vignette Bio, co-founded by Biocytogen and Foresite Capital; and TRC004, co-founded by Genor Biopharma, Two River, and Third Rock Ventures. Through these acquisitions, Candid secured rights to two bispecific antibody products from the two companies and completed a $370 million Series A financing round.

Therefore, it is not difficult to see that,The current wave of M&A differs from the previous two rounds, which were primarily driven by long-term benefits; this round places greater emphasis on monetization logic, aiming to achieve solid short-term financial returns through acquisitions and thereby alleviate challenges in product pipelines, market positioning, and relations with limited partners (LPs).。

"Water can carry a boat, but it can also capsize it."

It is foreseeable that the wave of mergers and acquisitions in the pharmaceutical industry will remain robust in the future, leading to more blockbuster deals. Some pharmaceutical companies can leverage this trend to stage a comeback, achieving innovation and disruption in their products and markets.

Figure 4. The Six Most Failed Pharmaceutical M&A Deals Valued at Over RMB 10 Billion in the Past Decade

This is a relatively ideal situation, but in reality,Mergers and acquisitions, as a type of transaction, still carry a certain failure rate., which also frequently occurs among major pharmaceutical companies. For instance, AbbVie acquired the oncology firm Stemcentrx in 2016 for a hefty $10.2 billion, aiming to reduce its reliance on Humira. However, shortly after the acquisition, Stemcentrx was plagued by bad news due to the failure of its new drug Rova-T, ultimately forcing AbbVie to withdraw from the venture and rendering the exorbitant M&A expenditure a total loss.

In fact, this is a relatively common M&A risk, primarily due to inadequate preliminary due diligence and insufficient foresight regarding industry shifts and the advancement of drug pipelines. Furthermore, in the context of China’s pharmaceutical sector,Due to the overall immaturity of the M&A environment, coupled with the limited international perspective and weak international capital operation capabilities of some Chinese pharmaceutical companies, they often find themselves in a passive position in M&A transactions.。

Take a specific case as an example. In January 2024, GlaxoSmithKline (GSK) announced an acquisition agreement with Aiolos Bio, successfully securing its core asset, AIO-001. In fact, this drug originated from China’s Hengrui Medicine. In August 2023, Hengrui licensed the drug to Aiolos Bio, and just six months later, Aiolos Bio was acquired by GSK. Within less than half a year, Hengrui Medicine effectively profited from the valuation arbitrage. Indeed, there are many similar cases, indicating that Chinese pharmaceutical companies still need to “catch up” in terms of merger and acquisition capabilities.

The final limitation lies in "desperate patients seeking any available medical help."In this regard, a senior industry expert commented, “Due to tighter capital conditions and cautious investment sentiment, many pharmaceutical companies currently have strong demands for mergers and acquisitions (M&A). Coupled with the ongoing M&A boom, opportunities for being acquired have increased significantly. This environment easily leads to ‘blind transactions,’ which, if problems arise, will not only fail to resolve immediate difficulties but also drag pharmaceutical companies deeper into trouble.”

Therefore, from an overall perspective, mergers and acquisitions (M&A), as an effective means of optimizing resource allocation and promoting industrial consolidation, play a positive role and are necessary for the overall development and maturation of China’s pharmaceutical industry. However, M&A involves thresholds and risks, necessitating caution. Particularly during the current surge in M&A activity, it is essential to maintain rationality and act decisively at the most opportune moment.

1"When Will the Wave of M&A Reach Biotech?" — Deep Blue View;

2. “One of the Strongest Main Themes Currently—Mergers and Acquisitions and Restructuring” — Securities Market;

3. “The Era of Mega M&A in Pharma Arrives: Multiple Epic Deals—Board the ‘Noah’s Ark’”—VBInsight