2024 Report on the Laparoscopic Surgical Robotics Industry: From Monopoly to Coopetition, with Over 200% Growth in Installed Units

Leveraging their high precision and minimally invasive nature, laparoscopic surgical robots have become important adjunctive tools in the field of surgery. Previously, the Chinese market for laparoscopic surgical robots was monopolized by the da Vinci system. However, the prohibitive treatment costs associated with da Vinci, coupled with breakthroughs in laparoscopic robotic technology under China’s National High-Tech Research and Development Program (863 Program), have provided domestic enterprises with the impetus and opportunity to enter the market. Currently, several Chinese companies, including Weigao, MicroPort, and Kangduo, have successfully obtained marketing approval for their laparoscopic surgical robots from the National Medical Products Administration (NMPA).

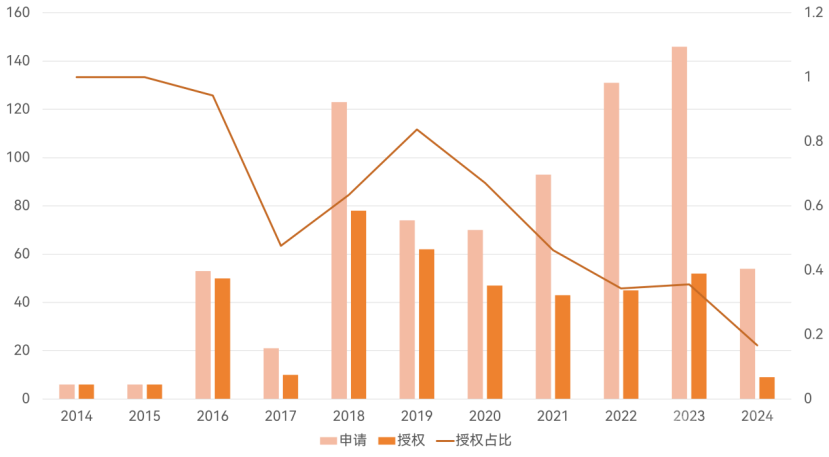

As patents and technical barriers have become the biggest obstacle to entering the field of laparoscopic surgical robots, whilePatents are the core means of building technical barriers and maintaining market competitiveness. The United States remains the most important country of origin for patents related to laparoscopic surgical robots, leading other countries and regions by a wide margin in terms of both patent application volume and the combined total of valid and pending patents. Data on Chinese patent applications shows that from 2014 to 2023, the number of patent applications increased by an order of magnitude, achieving rapid growth. Due to the high technical threshold for laparoscopic surgical robot technology and the substantial investment required for research and development, patent portfolio strategy has become a key factor for major companies in securing capital support and attracting investment. Furthermore, companies in this field must meet stringent medical device standards; through the accumulation and protection of patents, they can effectively demonstrate the compliance and advanced nature of their technologies.

Domestic Breakthroughs in Patent Barriers, Seizing Market Opportunities

Patent Application Trends for Laparoscopic Surgical Robots

Data Source: Patsnap, VBInsight

Patents related to the da Vinci Surgical System are primarily held by Intuitive Surgical. In terms of geographic patent layout, application targets are mainly concentrated in regional market hubs such as the United States, Europe, and China. To rapidly penetrate the market, Chinese enterprises should synchronize their patent strategies with market expansion efforts. Only by establishing comprehensive patent portfolios in core domestic and international markets at an early stage can companies effectively avoid constraints in technology development and market entry. Furthermore, as some of the early patents for the da Vinci Surgical System expire sequentially, this presents opportunities for technological innovation and improvement for domestic firms. However, when leveraging existing technologies, particular attention must be paid to potential infringement risks to ensure compliant research and development. Through strategic patent portfolio management, companies can not only enhance their market competitiveness but also reduce dependence on single markets or technologies, thereby building a more robust competitive advantage.

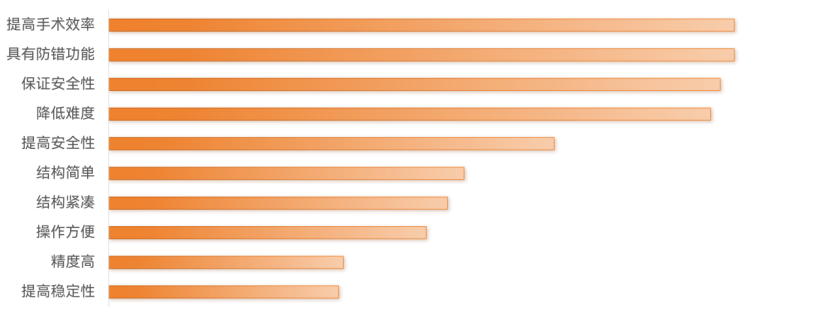

Safety Remains a Key Imperative in Patent Design

Problem Areas Addressed by Patents for Laparoscopic Surgical Robots

Data source: PatSnap, VBInsight

Statistical data indicate that error-proofing capabilities, improved surgical efficiency, and enhanced safety are key priorities in current patent designs in China. The industry places significant emphasis on ensuring patient safety during surgical procedures, particularly in high-risk environments, by leveraging technological means to minimize human operational errors and ensure smooth surgical execution. Meanwhile, improvements in efficiency contribute to higher operating room turnover rates, meeting the practical needs of healthcare institutions. Simplifying operations and reducing surgical complexity represent another major focus; patents related to “reducing difficulty” account for a substantial proportion, reflecting strong industry demand for streamlined surgical procedures and lower technical thresholds for surgeons. Through optimized design, surgical robots can not only alleviate the operational burden on surgeons but also facilitate broader adoption across more departments and surgical types. For the industry, this signifies a substantial increase in equipment penetration and clinical adaptability.

Chinese Manufacturers Officially Begin Their Pursuit of Da Vinci’s Commercialization Path

Surgical robots in China started late, but the competitive landscape is beginning to take shape. With the entry of numerous domestically produced laparoscopic surgical robots, the market is gradually shifting from the previous dominance of the da Vinci system to a more diversified competitive environment. According to incomplete statistics based on public bidding data from the China Government Procurement Network and other publicly available sources, the da Vinci surgical robot won bids for 36 units in China in 2023, while MicroPort won bids for 11 units, and Jingfeng and Kangduo each won bids for 5 units. In the first three quarters of 2024, the da Vinci system secured 28 bids, whereas domestic brands collectively won 31 bids. The declining share of da Vinci’s successful bids in China further confirms that its market share is being steadily eroded by domestic manufacturers.

Laparoscopic Surgical Robots Approved in China

Data sources: Center for Medical Device Evaluation, National Medical Products Administration; VBInsight

According to the bid award announcement for the centralized procurement of intracorporeal endoscopic surgical systems by the International Exchange and Cooperation Center of the National Health Commission in 2023, published on the China Government Procurement Network, laparoscopic surgical robot systems must be capable of meeting the endoscopic surgical needs of departments including urology, general surgery, obstetrics and gynecology, thoracic surgery, cardiac surgery, and pediatrics. Industry data indicates that among currently approved domestically produced laparoscopic surgical robots, MicroPort’s Toumai and Edge Medical’s Jingfeng are the closest competitors to the da Vinci system; however, they still exhibit limitations in departmental coverage. The Toumai robot is not yet approved for use in cardiac surgery, while the Jingfeng robot does not cover pediatrics or cardiac surgery. Weijing Medical’s four-arm laparoscopic surgical robot is on the verge of obtaining regulatory approval. Its registered indications currently cover urology, general surgery, and gynecology, with indications for thoracic surgery already undergoing expansion and supplementation. If domestically produced laparoscopic surgical robots can achieve breakthroughs in applicable departments and surgical types in the future, they may potentially achieve comprehensive substitution for the da Vinci surgical robot.

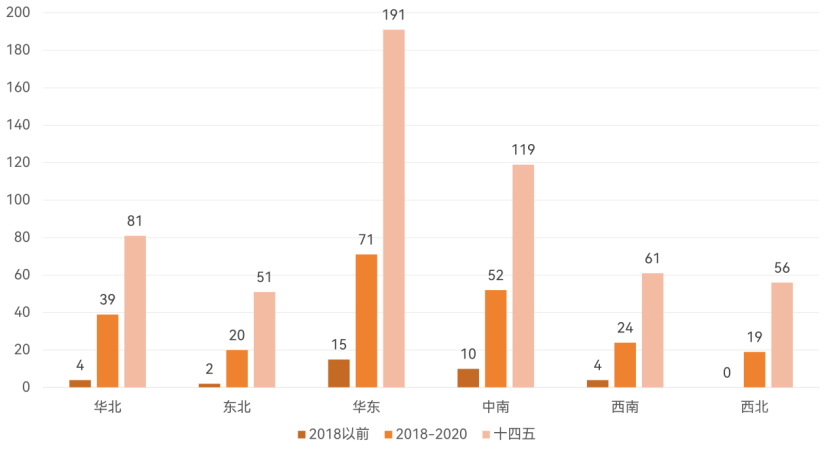

Trend Toward Relaxation of Configuration Certificate Regulation

On June 29, 2023, the National Health Commission released the "14th Five-Year Plan for the Allocation of Large-Scale Medical Equipment," which plans to allocate 3,645 units of large-scale medical equipment nationwide, including 117 Class A devices and 3,528 Class B devices. Since laparoscopic surgical robots were reclassified from Class A to Class B in 2018, the planned number of allocation permits has increased significantly, with 225 and 559 additional units approved during the 2018–2020 period and under the 14th Five-Year Plan, respectively. As the management of allocation permits is gradually relaxed, the installed base of laparoscopic surgical robots is expected to continue growing.

Domestic Endoscopic Robot Quota Planning

Data sources: National Health Commission, VBInsight

To date, over 240 configuration licenses for surgical robots have been issued across China’s provinces (autonomous regions and municipalities directly under the central government), further unleashing market demand. During the 14th Five-Year Plan period, the number of newly added large-scale medical devices has seen significant growth compared to the existing installed base, with laparoscopic endoscopic surgical systems surging by 215%. In terms of average annual installations, laparoscopic endoscopic surgical systems increased by 49.1% compared to the 13th Five-Year Plan period. In recent years, as domestic manufacturers rapidly rise in the high-end market, Chinese brands are poised to capture a larger share of new installations, gradually achieving import substitution for high-end medical equipment.

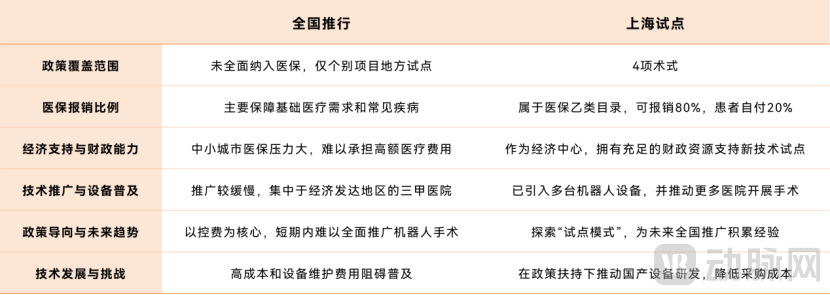

The Tug-of-War Between High Costs and Medical Insurance Funds: Full Coverage Under National Health Insurance Will Take Time

In recent years, facing rising medical costs and increasing pressure from an aging population, China’s healthcare security system has made cost containment a core objective of health insurance fund management. Health insurance policies tend to adopt a conservative stance toward the broad inclusion of high-cost, cutting-edge medical devices. The system prioritizes coverage for common diseases, frequently occurring conditions, and basic medical services. As a premium medical service, robotic surgery requires extensive cost-effectiveness validation over a prolonged period before it can be gradually accepted. Even in Shanghai, where certain procedures using laparoscopic surgical robots have been included in the health insurance scheme, this remains largely a localized pilot initiative aimed at exploring the feasibility of integrating such technologies into the national health insurance framework.

Comparison of Policy Implementation: China vs. Shanghai

Data Source: VBInsight

As China’s economic and healthcare hub, Shanghai benefits from robust fiscal support and abundant medical resources. However, this pilot model does not imply that similar conditions exist nationwide. There are significant disparities across China in terms of economic development, the adequacy of medical insurance funds, and the distribution of medical resources. Many small and medium-sized cities, as well as less developed regions, face greater pressure to maintain the balance between revenue and expenditure in their medical insurance funds. With laparoscopic surgical robots costing tens of millions of yuan, plus daily operational expenses such as maintenance and consumables, surgical costs are further elevated. Consequently, comprehensive coverage of such high-cost medical equipment is difficult to achieve in the short term.

The comprehensive inclusion of laparoscopic surgical robots in the medical insurance system is not merely an economic issue, but a multifaceted challenge involving technology assessment, policy decision-making, and the socioeconomic environment. Reimbursement approval for new medical devices typically requires substantial clinical data support and cost-effectiveness analysis. Furthermore, nationwide adoption necessitates coordination between central and local government policies. Although Shanghai has taken a leading role in this field, transitioning from localized breakthroughs to national widespread use will still require considerable time and navigate complex approval processes. This situation may change as domestic production of these technologies advances, equipment costs decrease, and more clinical data accumulate.

Separation of Technical Services and Consumables: Transparent Pricing Leads the Way in New Medical Standards

Currently, most regions in China allow autonomous pricing for surgical robot procedures, with no unified fee structure established. The majority of hospitals continue to adopt a billing model for laparoscopic surgical robots that combines “laparoscopic surgery fees + equipment and accessory charges,” effectively bundling the costs of devices, consumables, and services into a single package. Markups vary by region; in economically developed areas such as Beijing, Shanghai, and Guangzhou, an additional RMB 30,000 to 40,000 is typically charged on top of the standard fees for conventional laparoscopic surgery.

Laparoscopic Procedure Fees in Select Regions

Data sources: Local healthcare security administrations, interviews and surveys, VBInsight

At the national level, there are no clear regulations on the use of medical consumables, nor have corresponding guidelines been issued. There is a lack of unified standards for the quantity, types, and upper and lower limits of costs for consumables used in various surgeries. This not only leads to a certain degree of arbitrariness in the use of surgical consumables by hospitals but also creates hidden risks for cost opacity. Furthermore, there is no consensus within the industry on whether the current charging model is reasonable, and this uncertainty has hindered the further adoption of laparoscopic surgical robots.

The fee structure that separates technical services from consumables more accurately reflects their independent values by itemizing the costs of technical services and equipment/consumables. Under this model, patients pay separately for the technical service fees and consumable costs associated with robotic surgery, thereby avoiding the lack of transparency often caused by bundled pricing. This approach not only provides hospitals with a clearer basis for rational surgical cost management but also enables both physicians and patients to better understand the source and purpose of each charge. Presenting the values of equipment, consumables, and services independently facilitates more reasonable evaluation of cost structures by hospitals and regulatory authorities.

In the long run, the separation of technical service fees and consumable costs may become the prevailing trend in pricing models for the surgical robotics sector. As policies are progressively refined, specific guidelines on consumable usage may be introduced to help hospitals conduct robotic surgeries in a more standardized manner. Meanwhile, this unbundled pricing structure will contribute to building a fairer, more transparent, and efficient healthcare system, fostering healthy competition among various stakeholders within the industry.

Precision Admissions at Benchmark Hospitals: Creating a Demonstration and Promotion Effect

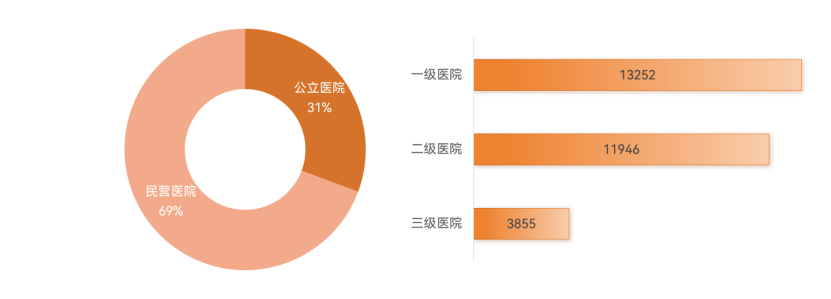

According to the "Statistical Bulletin on the Development of China's Health and Health Services in 2023," health resources in China have continued to grow steadily, with the number of hospitals showing a stable increase. By the end of 2023, the total number of hospitals nationwide reached 38,355, an increase of 1,379 from the previous year. Among these, there were 11,772 public hospitals and 26,583 private hospitals. In terms of classification by level, there were 3,855 tertiary hospitals nationwide, including 1,795 Class A tertiary hospitals.

China’s Medical and Health Institutions in 2023

Data source: Statistical Bulletin on the Development of China’s Health and Healthcare Services in 2023, VBInsight

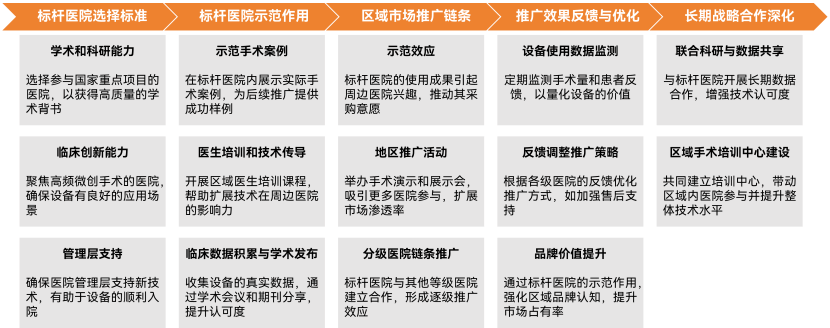

The growth in the number of tertiary hospitals has provided an ideal platform for the widespread adoption of laparoscopic surgical robots. Manufacturers of laparoscopic surgical robots should prioritize partnerships with Grade 3A hospitals or regional leading hospitals that boast high academic standards and abundant medical resources. These institutions possess strong academic influence and clinical innovation capabilities, enabling them to drive technology promotion in regional markets through demonstration effects. When selecting benchmark hospitals, it is also essential to evaluate their management models and receptiveness to innovation, including whether they participate in national key R&D programs or multicenter clinical trials. Hospitals whose management supports technological innovation and has a solid foundation for external collaboration will facilitate smoother market access for robotic systems.

Flowchart for Benchmark Hospital Selection and Regional Promotion

Source: VBInsight

The hospital adoption and promotion of laparoscopic surgical robots require precise selection of benchmark medical centers, in-depth needs assessment of high-potential departments, and multi-dimensional medical promotion strategies. This involves selecting tertiary Grade A hospitals with strong academic and clinical capabilities as benchmarks, identifying departmental pain points, and developing flexible collaboration models. Ultimately, by creating demonstrative case studies and establishing long-term partnership mechanisms, companies can achieve a win-win outcome in both market expansion and academic influence, thereby driving the widespread adoption and application of laparoscopic surgical robots across more medical fields.

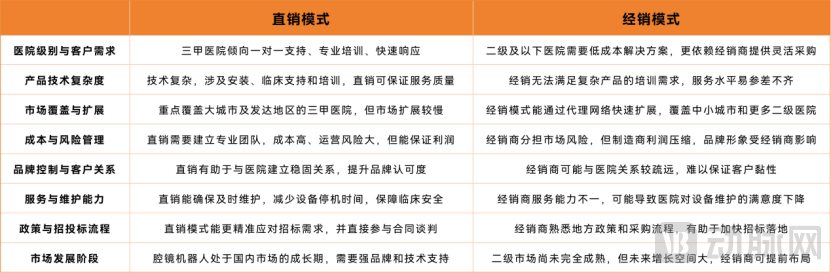

Dual-Engine Sales Channels: Building a Synergistic Direct and Distribution System Is More Advantageous

Laparoscopic surgical robots primarily serve major surgeries, with their customer base concentrated in Grade 3A hospitals and key provincial and municipal hospitals, which have extremely high requirements for technical support and maintenance services. Meanwhile, as the national tiered diagnosis and treatment policy advances, demand from secondary hospitals and those at lower levels will gradually be released. However, constrained by resources and equipment budgets, these hospitals tend to prefer cost-effective solutions with flexible service options when purchasing equipment. At the same time, regulatory oversight of the medical device market is becoming increasingly stringent, and some regions are implementing provincial-level centralized procurement, further complicating the selection of sales models.

Analysis of the Applicability of Direct Sales and Distribution Models

Source: VBInsight

In light of the above table, it is more reasonable for endoscopic surgical robot manufacturers to adopt a hybrid model combining direct sales and distribution in the domestic market. Manufacturers can employ a direct sales model in major cities and tertiary hospitals to ensure service quality and brand recognition. In small and medium-sized cities and secondary hospitals, they can leverage distributors to rapidly expand market reach, reduce operational costs, and capitalize on opportunities in lower-tier markets. This hybrid model strikes a balance between brand value and market coverage, helping manufacturers gain a proactive position in the competitive domestic healthcare market while providing greater flexibility and competitive advantages for long-term corporate development.

Currently, the technological pathways for domestically produced surgical robots are complex, with diverse product forms. This diversity facilitates differentiated competition and helps the industry avoid the pitfalls of price wars. In the future, centralized volume-based procurement policies will become a significant factor influencing the market, potentially compressing profit margins and requiring manufacturers to strike a balance between direct sales and distribution channels. Meanwhile, as the secondary hospital market matures, the role of distributor networks will become increasingly important. Furthermore, the responsiveness of after-sales service and the timeliness of equipment maintenance will be key determinants of a manufacturer’s ability to establish a foothold in the market. Regardless of the business model adopted, high-level after-sales support is essential for ensuring equipment operation and customer satisfaction.

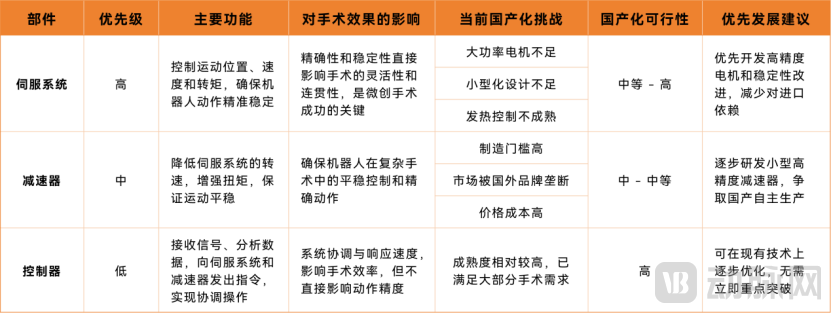

Heavy reliance on imports for the three core components, with weak domestic production capabilities

As the core power unit of surgical robots, servo systems are applied to the robot's motion joints. Their function is to precisely control the position, speed, and torque of movement based on command signals, ensuring the precision and coherence of robotic actions. Their performance directly impacts the flexibility and stability of robots in performing complex minimally invasive surgeries. Currently, high-end servo motors in the international market are predominantly monopolized by foreign brands, such as Japan’s Panasonic, Germany’s Siemens, Switzerland’s Maxon Motor, and the United States’ Kollmorgen. These brands have established a leading advantage through long-term accumulation in technological research and development and product performance.

Surgical robots rely on servo motors for power; however, the high rotational speeds of these motors are often unsuitable for surgical applications. Therefore, reducers are required to decrease speed and increase torque. A reducer must be paired with each motor’s output to ensure smooth robotic motion and precise control. Surgical robots primarily employ two types of high-precision reducers: RV reducers and harmonic drives. Characterized by their compact structure, high power transmission capacity, low noise, and smooth operation, these reducers are critical components enabling complex robotic movements. Nevertheless, the manufacturing threshold for precision reducers is extremely high, and the technology has long been monopolized by developed countries such as those in Europe, the United States, and Japan. Approximately 75% of the global precision reducer market is dominated by Japan’s Nabtesco and Harmonic Drive. This market monopoly weakens the bargaining power of surgical robot manufacturers in the reducer segment, while reliance on imported products exacerbates cost pressures and supply chain risks for domestically produced robots.

In contrast, the controller serves as the “brain” of a surgical robot, responsible for receiving signals, analyzing data, and transmitting motion commands to various components to achieve precise, multi-axis synchronized coordination. Since the controller’s performance directly impacts the robotic system’s response speed and execution efficiency, most surgical robot manufacturers opt to develop customized control systems in-house. In this domain, the gap between Chinese manufacturers and international brands is relatively small, with domestically developed controllers already meeting the requirements of most surgical robots.

Component Prioritization and Feasibility Analysis of Domestic Substitution

Source: VBInsight

Rapidly Respond to Physicians’ Needs and Enable Personalized Consumables Manufacturing

Domestic endoscopic surgical robots hold significant advantages over overseas competitors in the manufacturing of personalized consumables. First, domestic robots are better aligned with the local medical environment, enabling their R&D teams to rapidly identify and respond to the practical needs of clinicians. Benefiting from in-depth collaborations with physicians at Grade A tertiary hospitals, domestic manufacturers can fully incorporate clinical feedback to quickly customize consumables tailored to specific surgical requirements. In complex procedures within urology, general surgery, and other specialties, domestic systems allow for more flexible adjustments based on surgeons’ specific preferences regarding consumable attributes, such as the flexibility of forceps, the precision of shears, and instrument dimensions. This close integration of medicine and engineering facilitates the rapid implementation and efficient iteration of personalized consumables during R&D and production, thereby significantly enhancing instrument applicability and surgical outcomes.

Secondly, domestically produced robots possess significant local advantages in their supply and production chains. These Chinese-made robots not only circumvent the high costs and long lead times associated with imported consumables but also leverage the local manufacturing base to achieve localized production of consumables. This approach helps control costs and further shortens the cycle from design to production, thereby providing more efficient services to clinicians. Furthermore, by leveraging digital design and intelligent manufacturing technologies, domestically produced robots can directly translate physicians’ requirements into production standards, bridging the gap between research and development and clinical practice. This enables the rapid fulfillment of both quality and quantity demands for personalized consumables.

Guided by the profound understanding that “surgical preferences vary among operators, and different procedures entail distinct requirements,” TuoDao Medical established an in-house product team composed of senior medical professionals at an early stage. Throughout the product development process, this team works closely with engineers—from product planning and technical feasibility studies to product definition and design validation—ensuring that R&D resources are tightly aligned with clinical value to deliver products that better meet clinical needs. Meanwhile, TuoDao Medical actively engages in medical-engineering collaborations with major hospitals. Through its “Robot X Laboratory,” a comprehensive incubator for medical-engineering achievements, the company identifies and realizes clinical experts’ innovative concepts for robotic technologies and devices, rapidly validates them in clinical settings, and transforms insights into innovative medical devices. Thanks to continuous interaction and collaboration with local physicians, Chinese-made robots are achieving faster innovation in personalized consumables and offering more reasonable pricing. This positions them to further narrow the gap with the da Vinci Surgical System in the future, bringing more competitive, localized products to the Chinese healthcare market.

Avoiding European and American Barriers, Focusing on Differentiated Penetration

As of September 30, 2024, the total installed base of the da Vinci Surgical System reached 9,539 units. The da Vinci system has long maintained a dominant position in European and American markets, particularly in the United States and Europe, where this robotic device has become standard equipment in many top-tier hospitals. This advantage is reflected not only in its market share but also in its deep integration into surgical workflows, high familiarity among surgeons, a robust technical support network, and strong trust from patients, physicians, and hospitals. Leveraging its technological maturity and extensive clinical data, da Vinci has established significant brand recognition and loyalty. For Chinese companies seeking to enter the European and American markets, breaking through this brand barrier requires not only offering substantial cost advantages or performance breakthroughs but also building comparable trust through costly marketing, training, and equipment maintenance efforts—a challenge that is exceptionally difficult to overcome in the short term.

Medical regulatory agencies in Europe and the United States enforce stringent requirements and complex processes to ensure the safety and efficacy of medical devices. For instance, entering the U.S. market requires FDA approval, while the European market mandates CE certification. Both pathways involve lengthy timelines and demand substantial volumes of high-standard clinical trial data. Having undergone multiple rounds of clinical validation and accumulated extensive data on safety and efficacy, the da Vinci Surgical System has established a high level of market trust. Chinese companies would need to invest significant resources and time to meet these same standards, making it difficult to gain rapid market recognition in the highly competitive environments of Europe and the United States. Furthermore, given da Vinci’s extensive patent portfolio and technological barriers, Chinese manufacturers of laparoscopic surgical robots may face potential intellectual property disputes when entering these markets.

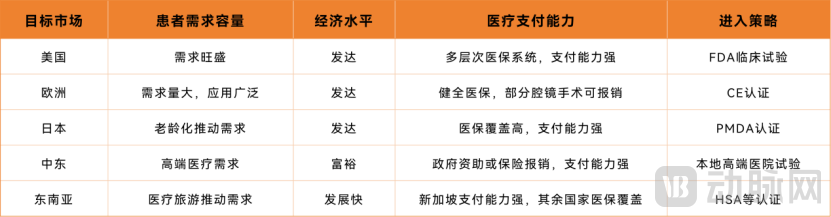

Scan and Analysis of Target Overseas Markets

Data source: VBInsight

The global expansion of laparoscopic surgical robots should adopt differentiated strategies based on market payment capacity and demand volume. In terms of marketing, developed countries prioritize brand effect and physician training, leveraging brand endorsement to expand market share; in emerging markets, such as the Middle East and Southeast Asia, market penetration can be enhanced through flexible approaches including medical tourism, leasing models, and government collaborations.

The Rise of Southeast Asia: Pioneering a New Blue Ocean in High-End Healthcare

Overall, the outlook for Chinese laparoscopic surgical robot manufacturers in European and American markets is less than ideal. While da Vinci’s home-field advantage is certainly a significant factor, more critical challenges include high market entry barriers, strong brand loyalty, demanding after-sales maintenance requirements, and substantial technical barriers. Therefore, given their limited resources, Chinese companies should prioritize entering more welcoming emerging markets (such as Southeast Asia) to accumulate experience and clinical data. By gradually achieving technological and brand maturity, they can then expand into European and American markets, thereby reducing the risks and costs associated with direct entry into developed markets.

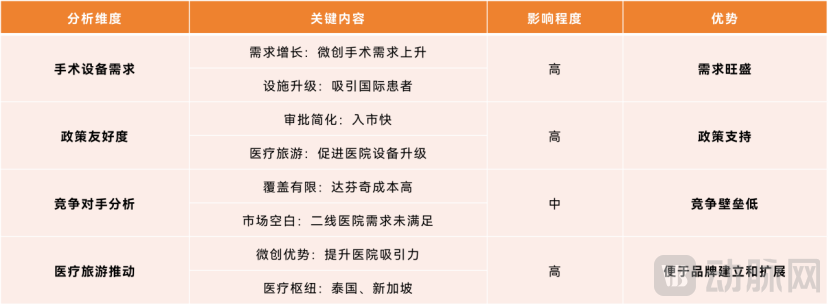

Table of Key Factors for Market Entry Strategy in Southeast Asia

Data Source: VBInsight

Countries such as Singapore and Thailand, serving as regional medical tourism hubs through initiatives like Singapore’s “Healthcare Excellence” program and Thailand’s “Medical Paradise” project, attract millions of international patients annually with relatively lower medical costs, high-quality services, and superior medical infrastructure. This has prompted nations within the region to actively invest in upgrading their healthcare facilities to cater to high-end patient segments. Such an environment provides a stable demand base for laparoscopic surgical robots, particularly as the advantages of robotic systems in minimally invasive surgery meet the expectations of international patients for premium healthcare services.

In certain Southeast Asian countries, economic development has been relatively rapid. Singapore, in particular, boasts comprehensive health insurance coverage and a high proportion of healthcare expenditure, resulting in strong patient payment capacity. In emerging markets such as Thailand and Malaysia, health insurance coverage is gradually increasing. Although local payment capacity is relatively weaker, hospitals are still able to bear the costs of using medical robotic devices with the support of international medical insurance. Compared to the high entry barriers in developed regions such as Europe and the United States, market access in Southeast Asia is relatively lenient. Certifications from Singapore’s Health Sciences Authority (HSA) and Malaysia’s Medical Device Authority (MDA) can serve as reference models for Chinese laparoscopic surgical robots seeking entry into other Southeast Asian countries. This approach enables market access with lower clinical trial and registration costs, shortens product launch cycles, and leverages Singapore’s regional influence to rapidly expand into other Southeast Asian markets.

Furthermore, Singapore and Thailand are at the forefront of Southeast Asia in terms of medical technology innovation and equipment adoption. Leveraging its status as a regional healthcare hub and robust scientific research capabilities, Singapore maintains an open attitude toward high-end medical devices. By collaborating with leading hospitals in Singapore, Chinese laparoscopic surgical robots can obtain high-quality clinical data support and authoritative certifications, thereby facilitating further penetration into neighboring markets in Southeast Asia. Thailand, on the other hand, boasts a mature medical tourism industry chain. If Chinese laparoscopic surgical robots are introduced there through leasing models or partnerships with large medical tourism companies, they can reach a substantial number of international patients, rapidly enhancing brand visibility.

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1 Clinical Value: Addressing the Pain Points of Minimally Invasive Procedures, Further Refining the Precision Blade

1.1 Pain Point Analysis: Surging Demand for Surgical Procedures, with Equal Emphasis on Precision and Safety

1.2 Future Directions: Optimization of Performance, Intelligence, and Ergonomics

Chapter 2 Market Status: Technological Innovation and Evolution, Patent Strategy Solidifies the Foundation

2.1 The Evolutionary Path: Technology-Driven Advancement in Intelligent Minimally Invasive Procedures

2.2 Patent Strategy: Laying the Groundwork for the Future and Seizing First-Mover Technological Advantage

2.3 Market Status: From Monopoly to Co-opetition, Reshaping the Market Landscape

2.4 TuoDao Medical: Leveraging Technological “Intelligence” to Enhance Medical “Treatment”

Chapter 3: Commercial Exploration: Paving the Way with Medical Insurance Pilots, Breaking Through in Commercial Implementation

3.1 Geographic Breakthrough: Medical Insurance Pilots Propel Endoscopic Robotic Surgery into Blue Ocean Markets

3.2 Commercial Offensive: From Price Wars to Market Win-Win, Multi-Level Business Strategies

Chapter 4 Expansion Strategy: Tackling the Challenge of Autonomous Control and Seeking a New Landscape for Domestic Substitution

4.1 Hospital Admission Strategy: Seizing the Expansion Trend of Grade A Tertiary Hospitals and Coordinating Marketing Channel Layout

4.2 Path to Breakthrough: Core Component Challenges Require Time; Cultivating Differentiated Advantages for Domestic Products

4.3 Global Expansion Strategy: Prioritize Southeast Asian Markets to Avoid High Barriers in Europe and the United States

Please scan the QR code to add the assistant and obtain the full report. If you have already added the assistant, please proactively reach out for assistance.

Special Acknowledgments (listed in order of research interviews):

Chief Physician of the Department of Urology, Shanghai General Hospital Affiliated to Shanghai Jiao Tong University; Obstetrician and Gynecologist at the General Hospital of the PLA Rocket Force; Deputy Director of the Department of General Surgery at the 306th Hospital of the Chinese People's Liberation Army; Dr. Cheng Min, Founder and Chairman of Tuodao Medical; Mr. Zhou Guanshan, Deputy General Manager of Weijing Medical