Medical Equipment Sector Enters Its Coldest Winter in a Decade Amid Slumping Sales and Procurement Delays

Medical device manufacturers have been having a tough time lately.

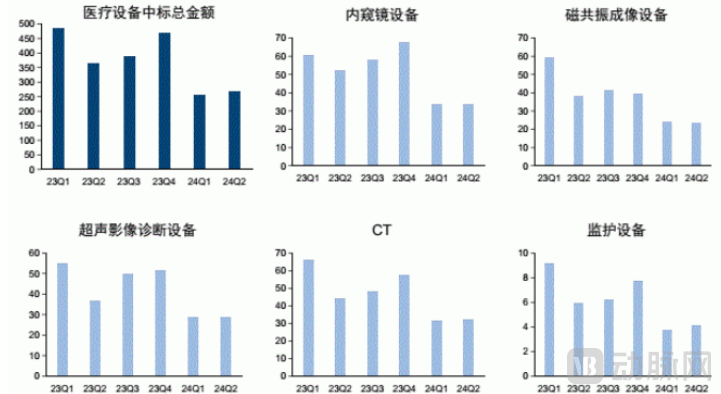

A research report by Guosen Securities shows that the total winning bid amount for medical equipment nationwide in the first half of 2024 was only RMB 52 billion, a year-on-year decline of 35%.

Among these, the situation is particularly severe for MRI, CT, ultrasound, endoscopy, and patient monitoring equipment, with winning bid amounts of RMB 6.5 billion, RMB 6.5 billion, RMB 6.0 billion, RMB 4.5 billion, and RMB 1.0 billion, respectively; corresponding year-on-year declines were -40%, -40%, -40%, -50%, and -50%, with sales volumes for each category nearly halved.

Winning Bid Amounts for Key Medical Equipment Categories (Q1 2023–Q2 2024) (Unit: RMB 100 million; Data Source: Guosen Securities)

The macroeconomic downturn has affected every company equally. Whether it is domestic leaders such as Mindray and United Imaging, or multinational giants GPS (GE Healthcare, Philips, and Siemens Healthineers), their performance over the past six months has been less than satisfactory.

Now That Winter Has Arrived, How Far Off Is the Turning Point for Medical Devices?

Behind the rapid tightening of the medical device market, the most obvious reason is the anti-corruption campaign in the pharmaceutical industry that began in mid-2023.

As the hardest-hit area in this campaign, illegal practices involving medical devices have emerged in endless succession. Many hospital administrators have profited by inflating expenses and accepting bribes. For instance, one hospital president overruled objections from other leadership members and purchased a linear accelerator with an import price of approximately RMB 15 million for RMB 35.2 million, pocketing around RMB 16 million in kickbacks.

“Customized” bidding is also a common form of corruption in hospitals. Some hospitals, under the guise of “technology” and “intelligence,” impose additional “customized” screening rules for bidding by ingeniously setting specific conditions such as “technical parameters.” In this way, a hospital president in Sichuan Province tailored bidding standards for a company, reducing the number of the hospital’s drug and consumable suppliers from over 200 to just seven with which he had direct interests, thereby evading regulatory oversight.

Following the launch of the “most stringent anti-corruption campaign in healthcare,” various corrupt practices have been investigated and dealt with, substantial public funds have been recovered, and prices for many medical devices have consequently declined.

Yet it was precisely during this period that many administrators not involved in corruption halted the procurement of various medical devices to mitigate risks. Since Q3 2023, healthcare institutions across China have exhibited varying degrees of “procurement hesitation,” which has become the primary driver behind the sharp decline in medical equipment purchases.

However, the causes of the market slump extend beyond this.

According to statistics from VCBeat Research Institute: although the overall sales revenue of imaging equipment maintained an upward trend in 2023, the total sales volume ultimately declined by nearly 10%. Even magnetic resonance imaging (MRI) systems, which had seen rising sales for decades, experienced their first-ever drop in sales volume during this period.

Upon closer examination, following the over-purchasing during the COVID-19 pandemic, mid-to-low-end imaging equipment, such as CT scanners with fewer than 64 slices and mobile digital radiography (DR) systems, has remained in a phase of digesting existing inventory. Furthermore, hospitals are currently prioritizing scientific research and precise diagnosis for neurological, cardiovascular, and cerebrovascular diseases, leading to a widespread preference for procuring high-end and ultra-high-end medical equipment. The approval process for such devices is lengthy, and when combined with delays in funding approvals caused by anti-corruption campaigns, this has resulted in a cyclical vacuum in demand.

Under the combined effect of multiple factors, medical device manufacturers are facing comprehensive pressure.

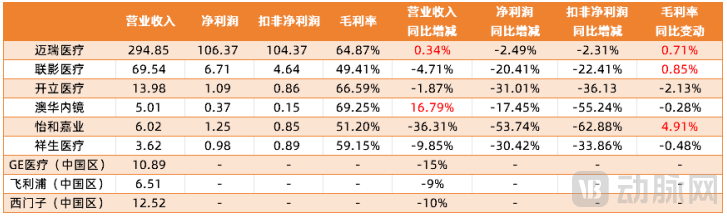

A statistical analysis of six Chinese medical device companies of varying sizes revealed that, in the first three quarters of 2024, only Mindray Medical and Aohua Endoscopy recorded revenue growth, while the remaining enterprises experienced declines to varying degrees. Even the “GPS” trio struggled to gain traction in the Chinese market, with their revenue scale decreasing by nearly 10%.

In terms of net profit, Mindray Medical experienced a significant decline in profits from its medical equipment business. Fortunately, slight growth in its non-medical equipment segment helped limit the year-on-year decrease in net profit to single digits. In contrast, other companies saw double-digit declines, with some experiencing drops exceeding 50%.

Q3 2024 Operational Data of Listed Medical Device Companies

(Domestic enterprises: CNY 100 million; multinational enterprises: EUR 100 million; data source: VCBeat)

The pressures faced by publicly listed companies can also be transmitted to startups. The capital-intensive nature of medical equipment places significant strain on these companies’ cash flows. With fundraising remaining difficult in both primary and secondary markets and operating revenues under pressure, 2024 has been an exceptionally challenging year for them.

Despite the sudden surge in pressure, China’s medical device market has not truly suffered “fundamental damage.”

An analysis from a market perspective reveals three primary factors. First, “procurement hesitation” has not eliminated hospital demand but merely deferred it, ensuring that there will always be opportunities for its release. As of 2024, the equipment configuration rate in China’s 2,062 county-level hospitals remained low, with the configuration rates for 29 types of medical equipment falling below 30%, indicating a significant gap.

Second, the effect of excess equipment procurement during the pandemic has gradually diminished over time. Meanwhile, the installed base of mid-to-high-end medical devices in China remains far below that of developed countries, indicating unmet demand. Under the confluence of these two factors, demand for medical devices across low-, mid-, and high-end categories will continue to be fully released in the medium term.

Third, many CT, MR, DSA, and PET scanners in hospitals have exceeded their service life at present, necessitating the phase-out of expired, non-functional, and obsolete equipment and the procurement of new, higher-quality devices.

In other words, the procurement pressure brought about by anti-corruption efforts is ultimately temporary, and the overall market size has not suffered significant negative impact. In the long run, hospitals still have substantial unmet demand for medical equipment, particularly for high-end devices.

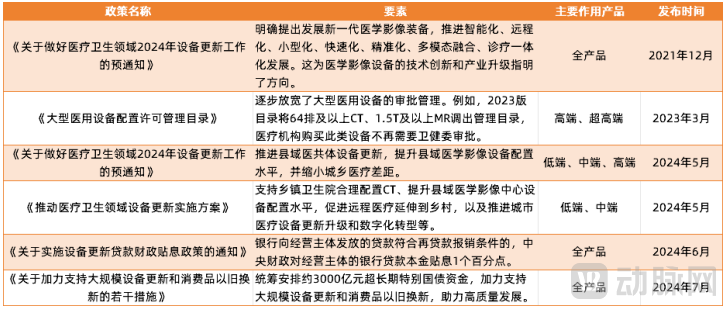

Turning to the policy dimension, national support for the medical device market over the past two years has been characterized by its high frequency, multi-dimensionality, and comprehensiveness.

In March last year, the National Health Commission rarely updated the “Catalog for the Administration of Licensing for the Allocation of Large-Scale Medical Equipment”: The 2023 deregulation of medical device allocation permits allowed any medical institution to directly purchase medical equipment not listed in the catalog, without the need to apply for filing with provincial or municipal authorities. This enabled some secondary and tertiary hospitals, which had previously been unable to meet their demand for mid-to-high-end medical equipment due to allocation permit restrictions, to initiate new procurement after the policy’s release, substantially expanding the fundamental base of the medical equipment market.

In May this year, the National Development and Reform Commission successively issued the Preliminary Notice on Doing a Good Job in Equipment Renewal in the Medical and Health Field in 2024 and the Implementation Plan for Promoting Equipment Renewal in the Medical and Health Field, transforming the passive renewal of medical equipment in county-level centers and tertiary hospitals into active renewal. This shift not only improves healthcare quality but also revitalizes the medical equipment market.

In July, the National Development and Reform Commission (NDRC) and the Ministry of Finance released the "Several Measures to Strengthen Support for Large-Scale Equipment Renewal and Consumer Goods Trade-In," which directly provides funding to hospitals. Guosen Securities estimates that of the RMB 300 billion in ultra-long special treasury bonds mentioned in the policy, approximately 7%–9% will be allocated to the healthcare sector (estimated based on the proportion of special bonds for medical and health care within China’s annual issuance of special-purpose bonds), amounting to RMB 21–27 billion. Assuming that treasury bond funds account for 50% of total investment, the total scale of medical equipment renewal is expected to reach RMB 42–54 billion.

Policies Related to Medical Devices in Recent Years (Source: VCBeat)

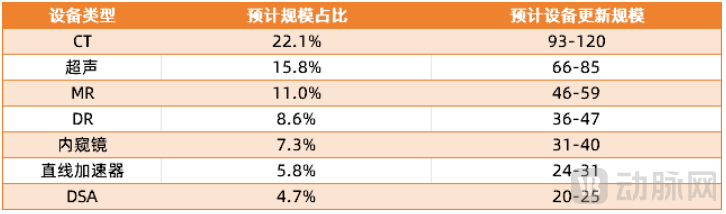

As of July 24, the equipment renewal projects announced by various provinces involved an investment amount exceeding RMB 20 billion. The top five types of equipment in terms of projected total investment were CT scanners, ultrasound systems, MRI scanners, digital radiography (DR) systems, and endoscopes, accounting for 22.1%, 15.8%, 11.0%, 8.6%, and 7.3% respectively, with a combined share of over 60%.

Estimated Total Investment in Various Types of Equipment (Data Source: Guosen Securities)

Furthermore, county-level medical institutions are highly likely to be the primary focus of the initial wave of demand release. According to statistics from Yizhuang Shusheng, by the end of September, the amount for equipment upgrades in county-level medical communities that had entered the procurement intention stage accounted for approximately 22%, while the amount that had entered the bidding stage accounted for approximately 5.10%. In contrast, urban hospitals recorded a procurement intention rate of approximately 17.32% and a bidding progress rate of approximately 4.59%.

At present, the “trade-in” program for medical equipment, stimulated by CNY 300 billion in government bonds, is most likely to break through the widespread “procurement hesitation” among healthcare institutions in the short term. Meanwhile, the catalog for configuration permit management and policies related to equipment updates will further expand the overall capacity of the medical device market.

The timelines projected for the release of “trade-in” initiatives vary across institutions, yet the overall ranges remain similar.

According to Guosen Securities, the bidding and tendering demand for the first batch of equipment renewal projects is expected to materialize starting in Q3 and be gradually released in Q4; Zhang Qiang, Chairman of United Imaging Healthcare, also anticipates large-scale implementation from the fourth quarter of this year through the end of the first half of next year.

However, after Q3, regulatory authorities in many regions have intermittently extended the duration of anti-corruption campaigns in the healthcare sector, which may to some extent affect the timing of demand release.

So, what if the demand is not released as scheduled?

For large enterprises, addressing this issue is relatively straightforward. The demand suppressed by “procurement hesitation” will eventually be released; with fewer concerns about cash flow, they can continue to sustain their R&D efforts and prepare for the upcoming competition in the mid-to-high-end market.

In the first three quarters of 2024, the R&D investments of United Imaging Healthcare and Mindray Medical remained unaffected by external environmental factors, with figures consistent with previous periods. Taking United Imaging Healthcare as an example, the company continued to maintain high investment in the research and development of high-end and ultra-high-end medical equipment in 2024, while also striving to complete its product portfolio by addressing ultrasound, the only remaining gap.

Furthermore, they must make ample preparations to compete for the imminent market opportunities. Currently, GPS (GE Healthcare, Philips, and Siemens Healthineers) have clearly launched their respective “refresh” initiatives, offering corresponding preferential packages for the comprehensive upgrade of medical institutions’ equipment portfolios. In China, companies such as Mindray Medical and Neusoft Medical have disclosed their preparatory plans for county-level markets, but have not yet released specific details.

By contrast, for startups—especially those that are not yet profitable—the delay in demand release will have a more adverse impact, potentially leading to industry consolidation.

Capital-intensive medical equipment inherently places significant strain on the cash flow of such enterprises. With fundraising remaining exceptionally difficult in both primary and secondary markets, the sharp decline in revenue will inevitably further test the survival capabilities of startups.

Therefore, over the past few years, medical equipment manufacturers have made all-out efforts to develop high-end products, leveraging flagship offerings to build brand recognition and drive sales. However, at this juncture, startups may need to slow down, seek a new balance between R&D and sales, and persevere until the day when market demand is fully unleashed.

In this process, startups should pay particular attention to the county-level market. On one hand, county-level medical institutions seek a balance between equipment capabilities and price, and most companies’ products can meet the needs of these institutions; on the other hand, the rate of equipment configuration in county-level medical institutions is already insufficient, and there is a need to update previously purchased equipment, making it a market with significant potential.

Overall, there remains a gap between the overall technical capabilities of China’s medical device industry and those of leading global players. It is hoped that more enterprises will survive and thrive, master more streamlined core components, and develop a greater number of effective high-end medical equipment, thereby benefiting both domestic and international markets.