China's Clear Aligner Industry Faces a 'Battle for Survival'

The once-booming invisible orthodontics industry is undergoing a major shakeout.

VCBeat recently learned from multiple frontline practitioners that several clear aligner companies are facing significant survival pressures, with some currently experiencing operational abnormalities or undergoing deregistration.

“In June 2021, Angelalign, the leading domestic clear aligner company in China, went public, with its stock price surging by as much as 183.24% on the first day of trading, highlighting the immense potential of the clear aligner market to numerous innovative enterprises and investment institutions,” Liu Ming (a pseudonym used at the interviewee’s request), Executive Director of a U.S. dollar fund, told VCBeat. “The rush of interest led to a short-term ‘capital’ boom in the industry.”

But as the tide recedes, the market reveals its jagged rocks like a menacing visage, forcing companies that previously relied primarily on financing for survival to confront the harsh reality.

According to feedback from multiple sources, many new enterprises, after securing financing, prioritize rapidly increasing their patient case volume as a core strategy to capture market share and boost valuations. Guided by this approach, mid-tier and lower-tier companies have primarily focused on the primary healthcare market—a segment where industry leaders have limited presence and which poses greater operational challenges. However, these strategies have driven up sales and marketing expenses for mid-tier and lower-tier enterprises, resulting in weak profitability and sluggish business expansion.

Consequently, in the face of sluggish consumer demand and declining venture capital activity, mid- to lower-tier invisible orthodontics companies that have yet to establish a profitable business model are facing an unprecedented survival crisis, as the industry enters a fierce “fight for survival.”

Invisible orthodontics has emerged as a major growth driver in the dental industry over the past decade, surging with remarkable momentum.

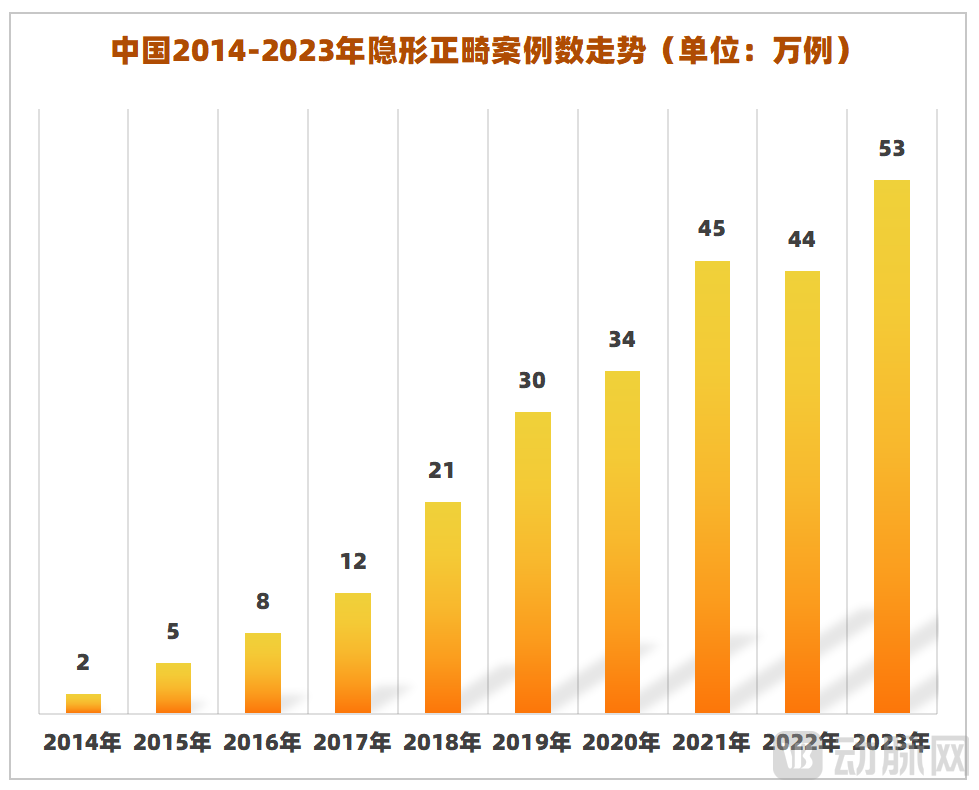

This can be glimpsed from the data. The “Annual Insights Report on China’s Clear Aligner Industry” shows that,In 2023, the number of clear aligner orthodontic cases in China was approximately 530,000, a significant increase from only 20,000 cases in 2014.

Amidst a highly favorable landscape, numerous emerging companies have been established, securing frequent rounds of financing in recent years and becoming an undeniable force in the field of clear aligner orthodontics.

However,Amid a surge in supply, market competition has intensified, placing performance pressure on some laggard firms and threatening their survival.

It turns out that, although clear aligners are priced at upwards of 20,000 yuan from the consumer end, representing a high-ticket business, butThe profitability of clear aligner orthodontics companies is not optimistic.

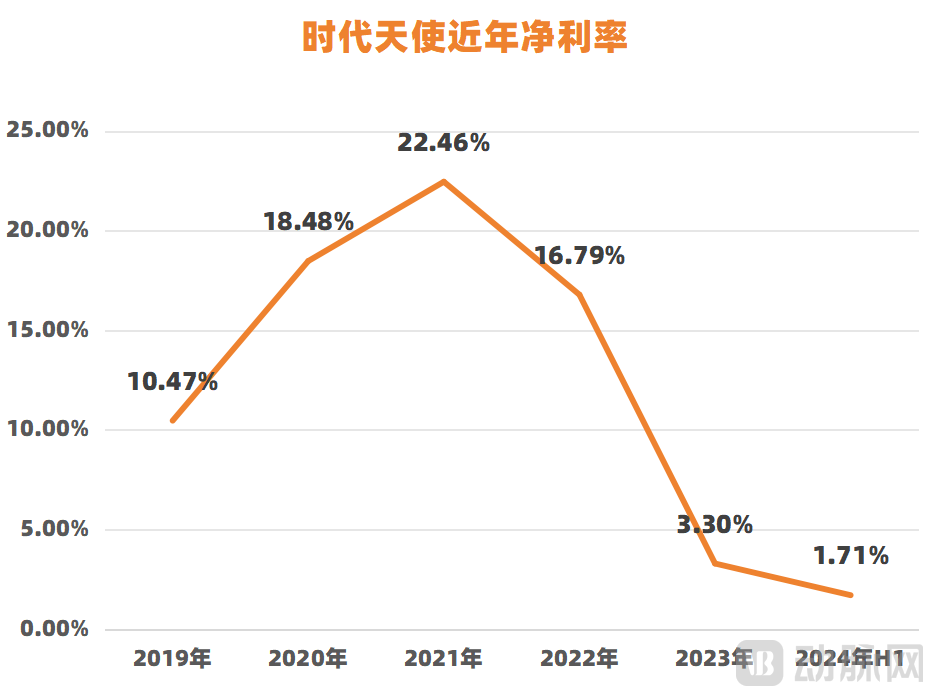

Taking Angelalign, the industry’s leading listed company, as an example, its net profit margin has continued to decline in recent years, dropping from 22.46% at the time of its IPO in 2021 to a historical low of 1.71% in the first half of 2024.

Overall, there are three underlying reasons.

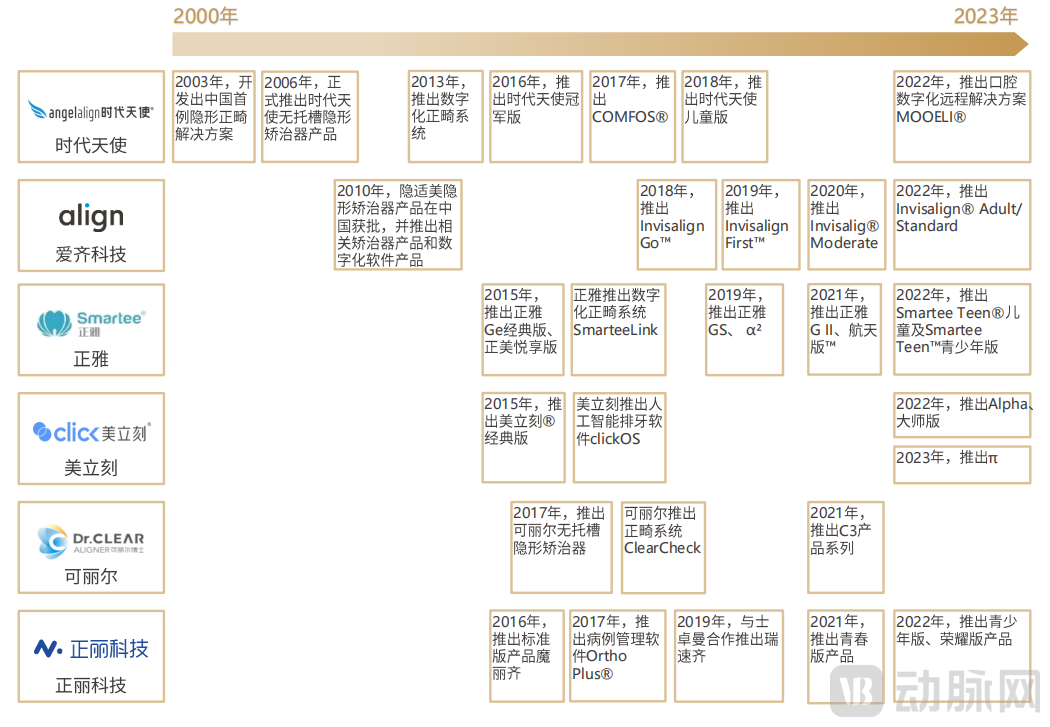

First,Intensifying Market Competition, a review of the National Medical Products Administration (NMPA) website reveals that, as of November 2024, more than 100 clear aligner products had been approved in China. New products are emerging continuously, whereas prior to 2021, the number of newly approved products each year was mostly in the single digits.

The Pace of New Product Launches by Major Clear Aligner Brands on the Market

Image source: “White Paper on China’s Invisible Orthodontics Industry”

Second, since 2022The Implementation of Centralized Procurement Has Reduced Product Profit MarginsFor example, in the centralized volume-based procurement of orthodontic brackets conducted in Shaanxi Province in October 2022, three products from Angelalign—Angelalign Teen, EAB II, and Angelalign Full—were selected at prices of RMB 12,600, RMB 6,300, and RMB 9,200, respectively, representing price reductions of approximately 23% to 30%.

Third, Angelalign’s expansion of its overseas business led to a significant increase in period expenses.

Excluding the third reason, the first two are common factors contributing to the decline in profitability within the clear aligner orthodontics industry.

If industry leaders with brand premiums and economies of scale are facing such difficulties, the challenges confronting smaller, less competitive firms are undoubtedly even greater.

Liu Ming told VCBeat that the average ex-factory price of clear aligner products from tier-three companies ranges from RMB 3,000 to RMB 4,500, which is significantly lower than the RMB 5,500 to RMB 7,500 average ex-factory price charged by market leaders, thereby imposing greater pressure on profitability.

With low profit margins per unit, many smaller players have adopted a “price-for-volume” strategy. Lower ex-factory prices often translate to lower end-user prices, presenting an opportunity for some dental clinics to capture entry-level invisible orthodontic treatments priced in the tens of thousands of yuan.

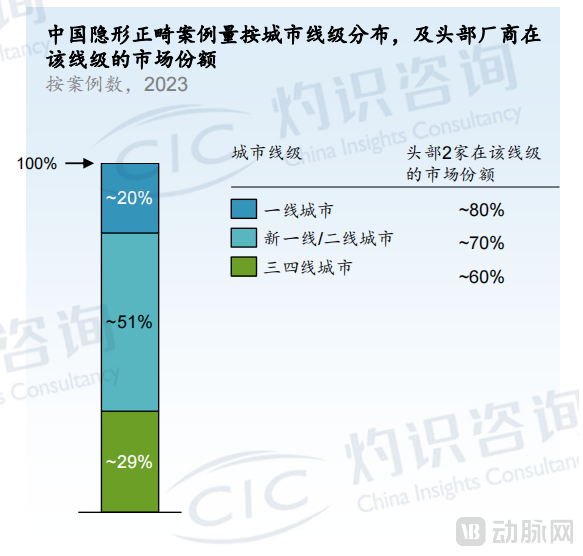

However, the challenge lies in the fact that Invisalign and Angelalign, as early entrants, have already secured the majority of dental institutions and market share in economically developed regions. According to the "Annual Insights Report on China's Clear Aligner Industry" released by Frost & Sullivan, Invisalign and Angelalign hold an 80% market share in first-tier cities, making it difficult for latecomers to enter the market in a short period.

Image Source: CIC Consulting's "Annual Insights Report on China's Clear Aligner Industry"

Therefore,The prevailing strategy among trailing companies is to “encircle the cities from the countryside,” i.e., first capture grassroots markets where penetration rates of leading enterprises remain low, then rapidly increase case volumes through pricing advantages to boost corporate valuations, and gradually scale up after securing successive rounds of financing.

However, the grassroots market, represented by third- and fourth-tier cities and county-level regions, faces numerous challenges. On one hand, compared with first-tier cities, dentists in these grassroots areas have relatively less clinical experience and rely heavily on manufacturers’ medical service support; on the other hand, the grassroots market is highly fragmented, resulting in higher customer acquisition costs.

In the early stages backed by capital, emerging clear aligner companies could disregard the break-even point and engage in aggressive market expansion through high sales expenditures. According to multi-source information gathered by VCBeat, several of these emerging enterprises achieved more than a tenfold increase in case volumes over the two-year period from 2022 to 2023.

However, as “ammunition” grows scarce and capital cools, the high-sales-expense model is becoming unsustainable for enterprises, with some companies incurring annual losses of tens of millions of yuan.

“A harsher reality is that even after the faucet of liquidity (financing) has been tightened, water continues to flow from the outlet.“Liu Ming stated, ‘Clear aligner therapy is not simply a business of buying and selling clear aligners; at its core, it is a “product + service” business.’”

This lies in the fact that, in addition to requiring dentist involvement during the pre-consultation and consultation phases,After orthodontic treatment, patients also require extensive dental involvement in the maintenance of their previous cases.From a clinical perspective, 4–6 years is generally the critical threshold for the recurrence of oral health issues. After orthodontic treatment is completed, relapse may occur within this 4–6 year period, manifesting as conditions such as “braces face,” tooth loss, or reversed protrusion, thereby necessitating further dental care.

Some invisible orthodontic brands under financial pressure show limited enthusiasm in managing cases that require maintenance or restarts. This has led dentists who previously opted for products from smaller, less-established manufacturers to become increasingly cautious about these brands, making market expansion more challenging.

In a vicious cycle, unprofitable fringe companies are beginning to be cleared out.

“Various phenomena emerging in the industry, such as business contraction, corporate deregistration, operational abnormalities, and equity disputes, are all symptomatic; fundamentally, these emerging brands have failed to establish self-sustaining revenue-generating capabilities,” stated Liu Ming.

As can be seen from the preceding discussion, late entrants in the clear aligner market have consistently incurred high sales expenses in their market expansion efforts due to a lack of brand strength.

Is there a possibility of bypassing dentists (B2D) and going directly to consumers (B2C)? This approach would not only save on sales costs associated with acquiring dentists but also rapidly capture consumer mindshare and expand brand influence.

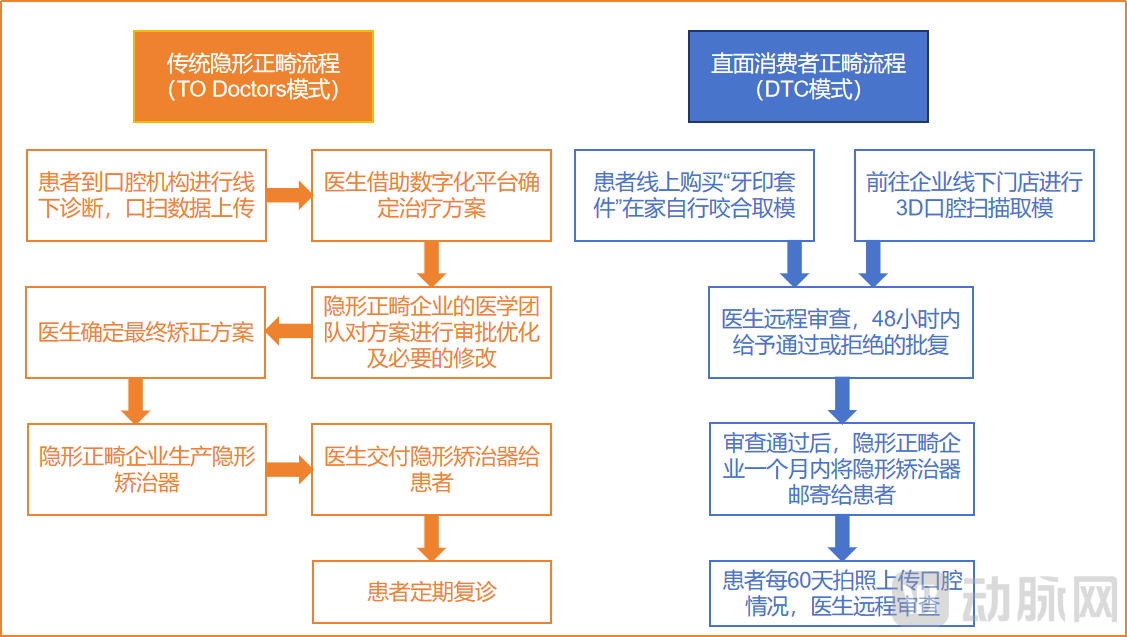

There are indeed companies that have adopted this approach—such businesses are generally referred to as DTC (Direct To Customer). Representative international players include SDC (Smile Direct Club) and Meijiegao, while Chinese counterparts include Smile Formula and xixilab.

In detail, in the traditional clear aligner orthodontic process, patients must visit a dental institution to have their dental impressions taken by professional dentists. AndUnder the DTC model, patients can choose between two impression-taking methods: one is to purchase a “dental impression kit” online and take bite impressions at home, then mail the dental molds back to the company; the other is to visit the company’s affiliated offline stores for 3D intraoral scanning to obtain the relevant modeling data.

Differences Between the TO Doctors Model and the DTC Model Process | Graphic by VCBeat

How Significant Is the Price Gap Between the To-Doctors and DTC Models? Taking U.S. data from 2020 as an example, the end-user price for clear aligners under the To-Doctors model ranged approximately from $5,000 to $8,000, whereas the DTC model, by eliminating the need for in-person diagnosis, cost less than $2,000, representing a price reduction of over 60%.

It is worth noting that the DTC model has also broken down geographical barriers in second- and third-tier cities. In the United States, 40% of counties lack access to relevant dental specialists; however, through online ordering services and a network of 300 offline stores, patients can easily obtain orthodontic care.

The significant price disparity and convenient services have propelled the DTC model to rapid prominence. Founded in 2014, DTC industry leader SDC went public successfully in 2019 after just five years, at which time its market capitalization reached $8.9 billion (approximately RMB 63.8 billion).

Since then, some domestic companies began to adopt this model, reaching a peak between 2021 and 2022.

However, the short-term growth has sparked significant controversy: bypassing physicians can easily expose patients to numerous potential harms.“If the direct-to-consumer model is applied to simple cases, it should not pose significant problems. However, it is prone to causing various issues in complex cases, such as alveolar bone dehiscence. Improper self-correction can easily lead to irreversible consequences. For example, if a building is constructed off-alignment, it can be demolished and rebuilt; however, teeth cannot be extracted and re-straightened.” Zhu Xianchun, Director of the Orthodontics Department at Jilin University Stomatological Hospital and a member of the Chinese Society of Orthodontics, previously told VCBeat that orthodontic treatment requires careful management by experienced clinicians to ensure optimal therapeutic outcomes.

Moreover, as Class II medical devices, clear aligners are subject to strict regulation under national laws and regulations. Consequently, for a considerable period, compliance requirements have essentially necessitated that clear aligner orthodontic companies collaborate with medical institutions. After all, each patient’s oral health status is unique; a suitable treatment plan can only be selected following a dentist’s examination and diagnosis. Furthermore, after patients begin wearing the aligners, they are required to attend regular follow-up visits at hospitals or clinics.

For the aforementioned reasons, some clear aligner companies facing scrutiny have swiftly issued statements declaring that they will not adopt the DTC model. Meanwhile, companies that continue to pursue the DTC model have encountered significant resistance in scaling up their market presence.

A landmark moment occurred in September 2023, when industry leader SDC officially declared bankruptcy, causing sentiment toward the DTC model to plummet to rock bottom within the sector and inflicting significant setbacks on Chinese companies.

Actually,From an industry perspective, clear aligner companies are not selling products but rather services.: Orthodontics is a highly specialized medical field. Patients first place their trust in the dentist, and it is this trust that leads them to choose the clear aligner brands recommended by their dentist.

Therefore, major companies invest significant effort and capital in providing educational training for dentists and building information systems, with the core objective of enhancing dentists’ efficiency and stickiness.

It can be said that doctors and clear aligner companies are mutually dependent and interdependent. Therefore, the “To Doctors” model will remain the mainstream business model in the industry for a considerable period of time.

During the years of rapid expansion in the clear aligner industry, market entrants have proven through “blood and tears” that building genuine product strength is the key to a company’s long-term, stable development.

“Since Class II medical devices are relatively easy to certify, many people believe that the barrier to entry in the clear aligner industry is not high. However, unlike other medical devices, clear aligners require a very high degree of customization,” said Liu Ming. “ThereforeIt is easy to manufacture clear aligners, but challenging to produce high-quality ones. Excellence entails capabilities in medical design, surface treatment processes, and large-scale delivery.”

From this perspective, technology serves as a critical foundation for products. A review of the development trajectories of industry leaders such as Invisalign, Angelalign, and Smartee clearly reveals their relentless accumulation of technological expertise. In contrast, smaller players lacking such technical depth often struggle to match the quality control standards of market leaders, resulting in a significantly compromised patient experience.

Taking large-scale mass production as an example,As there are no off-the-shelf production lines available for purchase upstream, the challenge in the clear aligner industry lies not only in companies’ ability to manufacture clear aligners, but more critically in their need to independently develop and build the production lines required for manufacturing these aligners.

“When applying for Class II medical device registration certificates, companies typically rely on manual processes. This approach is feasible for small-scale commercialization after certification. However, as production volumes increase and delivery timelines tighten, numerous issues arise. Therefore, a digitalized production line for clear aligners represents the first critical hurdle that determines whether a company can emerge as an industry leader,” said a senior industry expert.

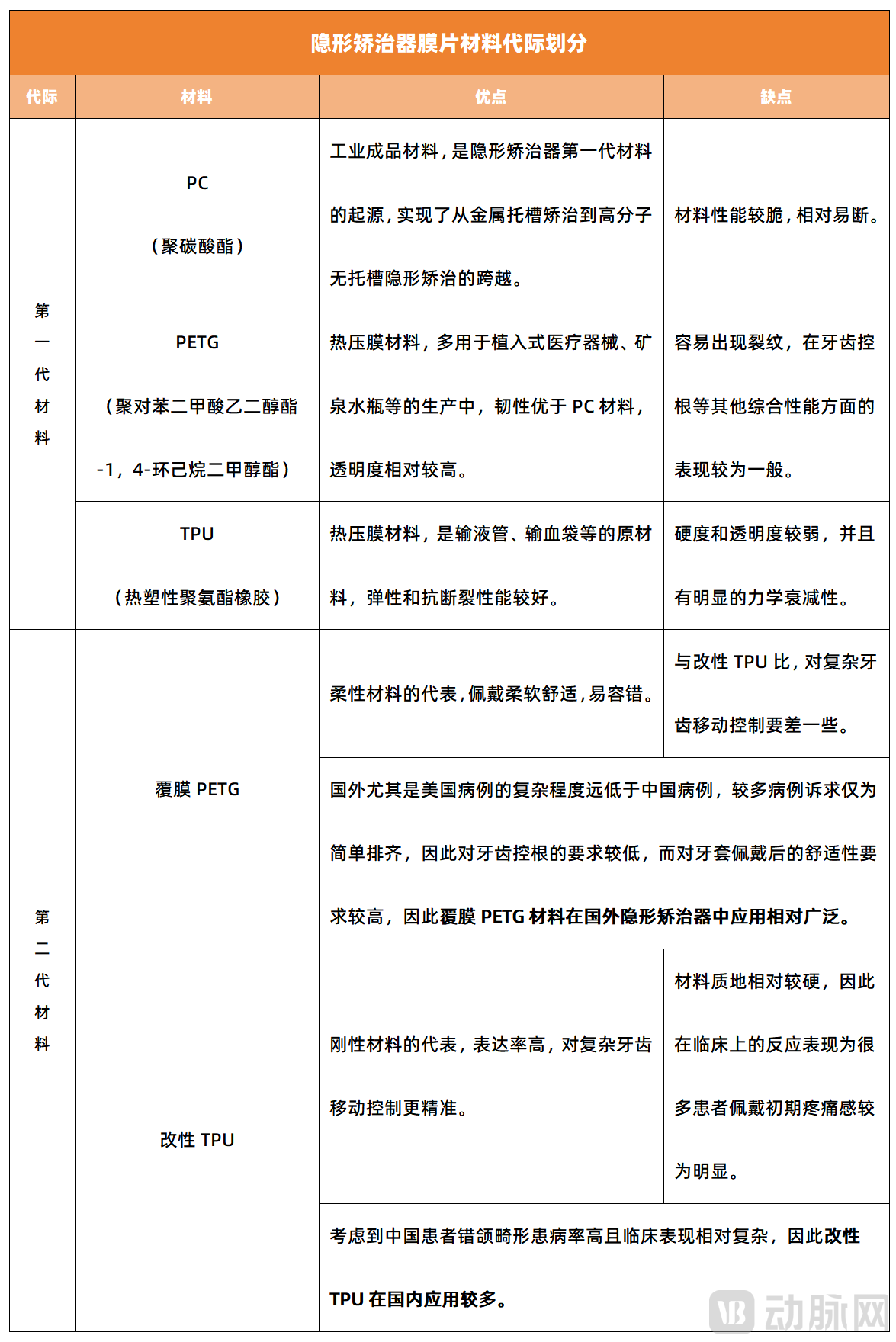

Material innovation is also a critical component. In the field of clear aligner orthodontics, clear aligners rely heavily on sheet materials.——The quality of aligner sheet materials directly impacts the treatment efficacy of clear aligners. Consequently, manufacturers place significant emphasis on the research and development of these materials. Currently, clear aligner materials are categorized into first-generation and second-generation types. First-generation materials include polycarbonate (PC), polyethylene terephthalate glycol (PETG), and thermoplastic polyurethane (TPU), all of which are standard industrial-grade materials. Second-generation materials represent improvements upon the first generation, including coated PETG and modified TPU. At present, leading companies have already adopted these second-generation improved materials.

Data source: Qila Technology; Graphic by VCBeat

Additionally,Whether sufficient service support and logistical backing can be provided to orthodontists is another core factor in building the product strength of clear aligner systems.As previously mentioned, clear aligner orthodontics is not merely a diagnostic and treatment process; it also encompasses preliminary patient acquisition and consultation, intermediate cephalometric analysis and treatment planning, as well as post-treatment services.

Therefore, if companies can provide physicians with a comprehensive suite of treatment support services, enabling them to focus wholeheartedly on patient care, this will serve as an effective competitive advantage in physician acquisition. Based on this rationale,Numerous enterprises have established medical affairs departments.However, according to VCBeat, the medical departments of leading invisible orthodontics companies mostly have in-house teams of hundreds of people, while smaller players at the lower end of the market tend to rely more on outsourced physicians. This approach often results in inadequate follow-up services and a lack of continuity.

Of course, as China’s clear aligner industry enters a period of intense consolidation, market participants should avoid excessive anxiety. Instead, they must focus on building genuine product competitiveness while seizing the opportunities presented by this industry wave.

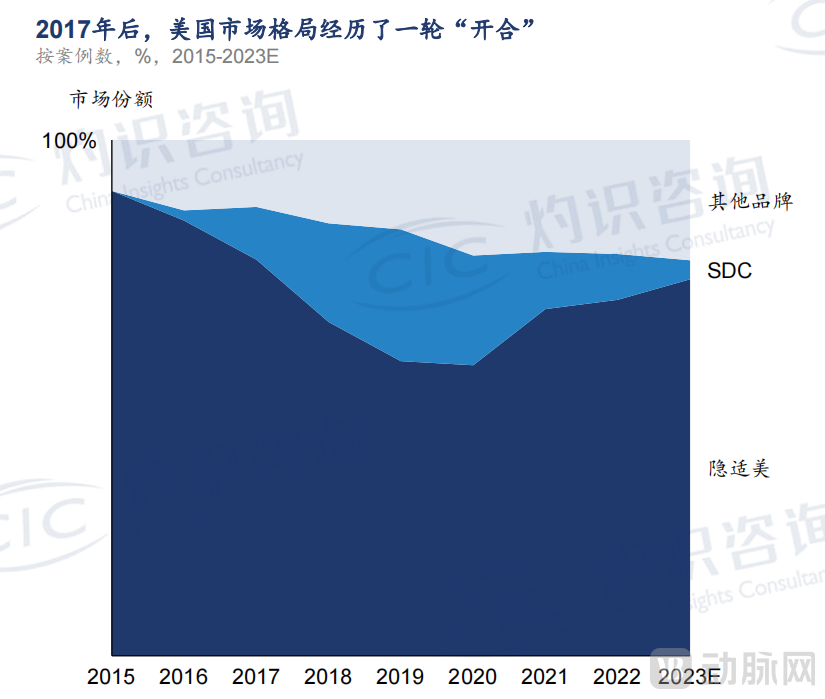

It should be noted that,In the United States, the clear aligner industry has also traversed a path of “oligopoly—fierce competition among numerous players—rising market concentration.”: After the expiration of Invisalign’s key patents in October 2017, small clear aligner companies in the United States became increasingly active, with their combined market share reaching as high as 40%. However, their market share has since declined, projected to drop to around 25% by 2023, indicating a continuous rise in industry concentration.

Image Source: CIC Consulting's "Annual Insights Report on China's Clear Aligner Industry"

Meanwhile, a detail that may be easily overlooked is that,In the first half of 2024, Align Technology, the parent company of Invisalign, surpassed Dentsply Sirona, Straumann, and Envista with revenues of $2.025 billion, becoming the top revenue-generating company in the global dental consumables sector for the first time and demonstrating the tremendous growth potential of clear aligners as a blockbuster product.

Therefore, industry growth will not cease. Globally, the annual volume of orthodontic cases is approximately 21 million, of which 5 million are clear aligner cases, resulting in a clear aligner penetration rate of 23.8%, indicating significant room for further growth.

Such a vast market will not be monopolized by a handful of companies; every enterprise that commits itself to the sector and pursues continuous innovation has the potential to succeed.

A rising tide lifts all boats. As laggard firms continue to exit the market, the competitive landscape of the clear aligner industry is stabilizing. Chinese clear aligner brands that sustain growth and persevere through challenges will inevitably benefit from this trend, gradually becoming key players and innovators in the global oral care industry.