How U.S. Biotech Firms Are Leveraging Chinese Innovation to Stage Remarkable Comebacks

Chinese biotech firms are not only a strategic reserve for multinational corporations (MNCs) but have also become a lifeline for overseas biotech companies.

As the number of domestic license-out transactions increases, the composition of the buyer pool has also shifted. In addition to multinational corporations (MNCs) that have drawn market attention, the proportion of overseas biotech companies has been rising year by year. According to data from Guosheng Securities, between 2019 and 2023, the share of MNCs among recipients in China’s business development (BD) deals increased from 14% to 36%, while the share of overseas biotech firms rose from 14% to 35%, making them a significant force in BD transactions that cannot be overlooked.

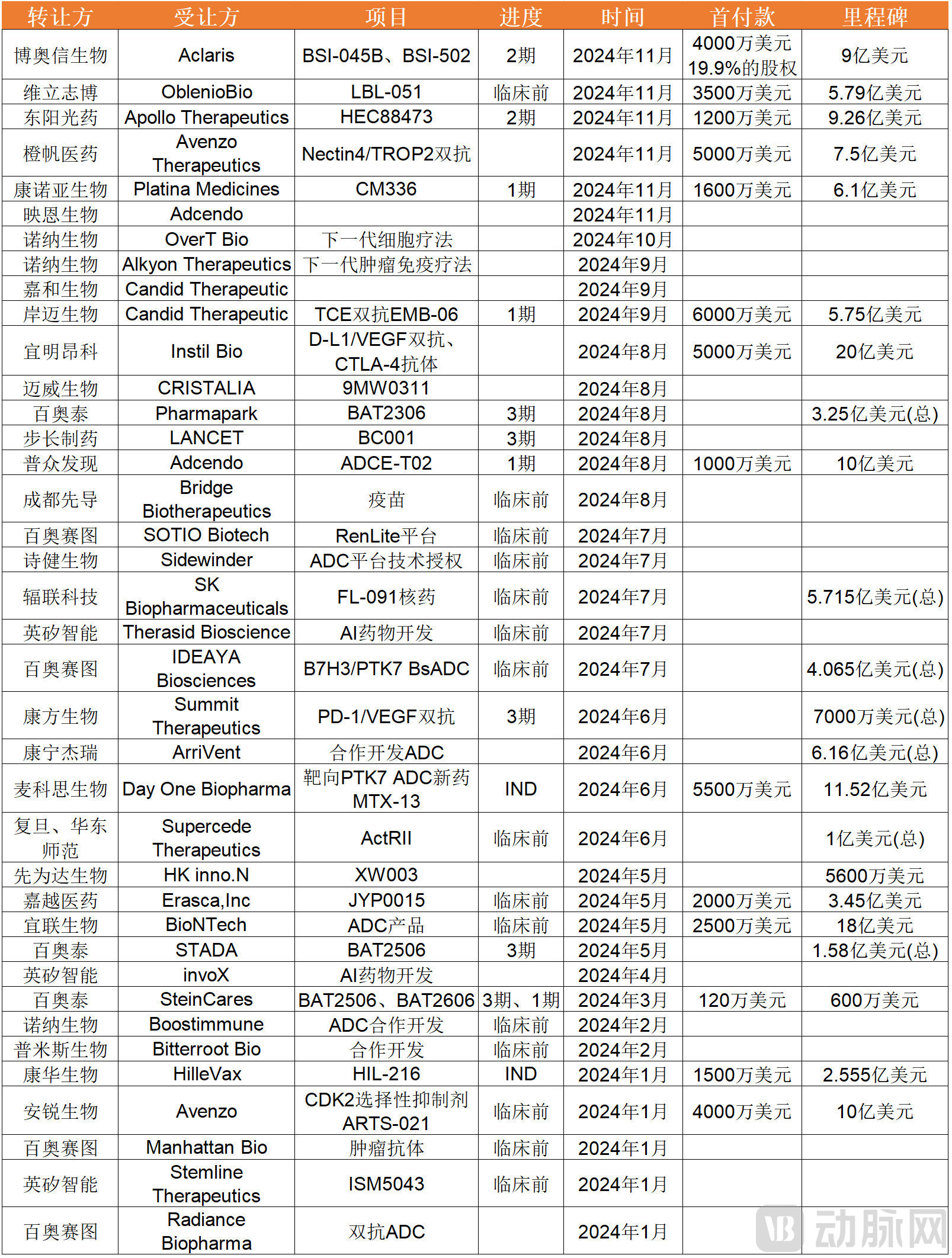

Selected BD Deals Involving Overseas Biotech Companies This Year, Based on Publicly Available Information

In terms of deal volume, overseas biotech companies have played a significant role in business development (BD) transactions this year. However, the transaction values are generally modest, and the selected pipelines are predominantly in early stages. Notably, some foreign biotech firms, themselves facing precarious operational conditions, have managed to turn the tide by licensing-in pipelines from Chinese biotech companies.

In the past, any Chinese pharmaceutical company could package a few pipelines licensed from the U.S. to secure financing or even pursue an IPO; now, the situation has reversed.

An increasing number of overseas biotech firms are staging a comeback by leveraging China’s innovative drug pipelines.

In late November, the share price of U.S.-listed biotech company Aclaris surged more than twofold, pushing its market capitalization above $300 million. Just over 20 days earlier, its market cap had been under $100 million, meaning it tripled in value within a month.

The catalyst for the stock price surge was Aclaris’s announcement on November 18, in which it acquired global rights (excluding China) to two antibody drugs from Bio-Thera Solutions: a TSLP monoclonal antibody and a TSLP/IL-4R bispecific antibody. According to the announcement, Aclaris is required to pay an upfront fee of $30 million, approximately 20% of its corporate equity, $10 million in reimbursement for R&D expenses, and up to approximately $900 million in milestone payments.

Aclaris’s development trajectory is a microcosm of many small overseas biotech companies.

Despite being in operation for over a decade, Aclaris Therapeutics experienced a significant setback in 2023 when its Phase 2b clinical trial of ATI-450, an oral MK2 inhibitor and core pipeline asset for the treatment of rheumatoid arthritis, failed to meet either its primary or any secondary endpoints. Following the announcement, the company’s stock price plummeted by 86% on the same day and continued to decline.

Although Aclaris has two other early-stage drug candidates, the market holds little expectation for them. As of the end of September this year, Aclaris held approximately $170 million in cash and treasury securities, with a projected annual loss of $50 million. This implies that Aclaris is staking its only remaining assets on Bio-Thera’s two monoclonal antibodies. This transaction not only triggered a significant rebound in Aclaris’s stock price but also completed an $80 million private placement, while ushering in new management, creating a sense that the company is back on track.

It is not the first time that U.S. biotech stocks have staged a comeback against the odds by leveraging Chinese assets.

Instil Bio was once a star biotech in the TIL field. However, following the failure of its core pipeline, its stock price plummeted from a high of over $20 to less than $1, leaving the company with a market capitalization of only $80 million by the end of 2023. According to its Q1 financial report this year, the company’s current assets stood at just $161 million. In July, to generate cash flow, Instil Bio leased one of its manufacturing facilities to AstraZeneca.

At a critical juncture, in August, Instil Bio announced the acquisition of global rights outside Greater China for a PD-L1/VEGF bispecific antibody and a CTLA-4 antibody from ImmuneOnco. The deal terms included a $50 million upfront payment (with $10 million paid initially), near-term milestones, total milestone payments not exceeding $2.1 billion, and single-digit to low double-digit sales royalties.

Subsequently, driven by breakthrough advances in the field of PD-1/VEGF bispecific antibodies, Instil Bio’s stock price surged from $12 at the time of pipeline acquisition to a high of $92, significantly alleviating the operational pressures facing this near-bankrupt company.

It is not only a driver of stock prices; while domestic biotech firms are shut out from IPOs, several overseas biotechs have successfully gone public by leveraging innovative drug pipelines from China, achieving a leap forward in their development trajectories.

In June this year, U.S. biotech company Alumis rang the opening bell on its IPO, raising nearly $300 million in one of the largest offerings in the U.S. biopharmaceutical sector this year. Notably, Alumis’s core pipeline asset, ESK-001, originates from the Chinese pharmaceutical company Haisco Pharmaceutical.

Summit, which previously licensed its pipeline from Akeso, and Arrivent, which licensed furmonertinib from Allist, have both staged remarkable turnarounds by leveraging Chinese assets. Of greater interest, however, is how these overseas biotech companies have precisely timed their moves and selected the right projects.

Unlike well-funded MNCs with ample room for error, overseas biotech firms prioritize precision in their product selection.

It can be seen that in BD transactions involving overseas biotech companies this year, most upfront payments are only in the tens of millions of dollars. However, for many cash-strapped overseas biotechs, this is already their last bargaining chip. Therefore, they have unique requirements in product selection, among which financing is a key objective.

For overseas biotech companies aiming to secure financing, the criteria for product selection are very clear: market acceptance.

In late November, Denmark’s Adcendo announced the completion of a $135 million Series B financing round, driven by an antibody-drug conjugate (ADC) program licensed from China. Over the past three years, the total value of global ADC transactions has exceeded $10 billion. Amid this surge, Chinese pharmaceutical companies have rapidly advanced their ADC pipelines, leveraging their engineering advantages. Companies such as RemeGen, Kelun-Biotech, Baili Tianheng, Keymed Biosciences, Lepu Biopharma, and Hengrui Medicine have garnered significant attention with their respective ADC products. China’s ADC pipeline is increasingly attracting the attention of global capital.

In such circumstances, selecting ADC projects from China is naturally a reasonable choice, with some companies having come to the Chinese market more than once to “snap up” assets.

Avenzo Therapeutics entered into agreements with Arriya Biologics and OrangeSail Pharma in January and November 2024, respectively. What attracted them was the distinctiveness of the projects. For instance, OrangeSail Pharma’s bispecific antibody-drug conjugate (ADC) leverages the synergistic effect of two different targets to more precisely target tumor cells. Theoretically, this can further enhance the tumor selectivity and internalization rate of the drug, improve responses in patients with low target expression and tumor heterogeneity, and thereby expand the clinical application of ADC drugs. Arriya Biologics’ ARTS-021 has demonstrated high kinase selectivity, favorable pharmacokinetic properties, and potential best-in-class preclinical efficacy in preclinical studies.

Moreover, several highly promising projects have also become targets for their strategic investments.

As exemplified by Hengrui’s TSLP monoclonal antibody transaction, TSLP inhibition is currently the only biological approach with confirmed clinical benefits for patients with moderate-to-severe asthma. Globally, Tezepelumab, co-developed by AstraZeneca and Amgen (administered monthly), remains the only approved drug targeting this pathway. Currently, there are nearly 30 TSLP candidates in development worldwide, with major multinational corporations such as Sanofi, Johnson & Johnson, and Pfizer actively involved in this space. The prevailing R&D trend focuses on TSLP-targeting bispecific or trispecific antibodies. Hengrui’s TSLP monoclonal antibody is among the most advanced candidates in its class, and its ultra-long half-life, enabling twice-yearly dosing, represents a significant differentiator. Such a highly attractive asset naturally draws considerable attention.

It is not difficult to see that these product selection targets are all projects that lend themselves easily to “storytelling” in the capital markets. However, securing financing for Chinese pipelines is merely an appetizer; the main course lies in acting as a middleman to resell these Chinese pipelines.

It is no longer novel for Chinese biotech pipelines to be subject to price arbitrage.

Early this year, GSK’s announcement of its acquisition of Aiolos Bio for a $1 billion upfront payment plus $400 million in milestone payments topped industry headlines. The reason lies in the fact that Aiolos Bio’s core asset originated from Hengrui’s SHR-1905, which had been acquired just four months earlier with a $25 million upfront payment and total milestones of $1 billion. The dozens-fold price difference in merely over four months is undoubtedly astonishing.

Whether it is Aiolos Bio or Alumis, mentioned earlier, the successful monetization of their Chinese assets would not have been possible without the contributions of their founding teams.

Taking Aiolos Bio as an example, the two founders compiled a list of immune targets at the company’s inception, aiming to identify promising candidates for pipeline development. One of the founders, Khurem Farooq, previously served as Senior Vice President of Immunology and Ophthalmology at Roche. During his tenure as CEO of Gyroscope Therapeutics, he facilitated the company’s acquisition by Novartis.

Alumis CEO Martin Babler’s previous venture, Principia Biopharma, was ultimately acquired by Sanofi for $3.68 billion. Just one year later, Martin embarked on a new entrepreneurial journey by founding Alumis.

For these serial entrepreneurs, after selling off the core assets of their previous ventures, the quickest and most efficient way to replenish their war chests is to make another acquisition, with Chinese innovative drugs serving as their ideal target.

For investors behind them, it is more advisable to partner with teams that have already demonstrated their monetization capabilities than to back newcomers who favor high-risk innovation. Particularly in the current environment, possessing a proven track record of success and strong monetization ability is crucial for securing greater capital commitments from investment firms.

The CEO of the foreign venture capital firm Perceptive Advisors once stated that it is better to bet on a seasoned team, even at a cost of $400 million, than to spread investments across ten companies. This remark was made against the backdrop of Mirador Therapeutics, a startup, completing its $400 million Series A financing round in March of this year. At the time, Mirador had not disclosed its candidate pipeline; instead, it relied on the track record of its founders and management team, who had previously sold their last company to Merck for $10.8 billion.

In other words, while it may appear on the surface that overseas biotech companies are profiting from arbitrage on Chinese-developed pipelines, the underlying driver is actually a shift in investment trends within foreign primary markets.

On the other hand, leveraging advantages in labor and operational costs, China’s drug development pipelines generally progress more rapidly. In the United States, employing a Ph.D.-level R&D researcher costs approximately $200,000, whereas in China, the cost may be only 30% of that amount or even lower. Furthermore, in many therapeutic areas, China has access to larger patient populations, facilitating clinical trial execution.

Moreover, over the past decade, China’s innovative drug sector has undergone a period of rapid development, with many biotech companies advancing multiple pipelines simultaneously. As the industry enters the current “winter” phase, companies are facing mounting pressure to achieve profitability. Rather than letting these pipelines languish internally, divesting them has become a strategic option to alleviate financial strain.

Under these circumstances, overseas biotech companies have begun acquiring Chinese drug pipelines at lower prices, securing U.S. market financing or designing clinical development plans that appeal to multinational corporations (MNCs) based on prevailing market conditions, thereby “packaging” these assets to command higher valuations.

China’s Innovative Drug Pipeline Is in High Demand: A Sign of Progress, Yet Also of Lagging Behind

As biotech companies shift their focus from becoming pharmaceutical giants to prioritizing business development (BD), the agile “small and beautiful” model—centered on a single pipeline as its core asset—is gaining traction and may well define the future trajectory of China’s biotech sector.

In the past, Chinese biotech companies favored developing multiple pipelines, whereas their U.S.-listed counterparts adopted the opposite strategy. Although they typically maintained around three pipelines, only one served as the core asset. These companies would go public after advancing this key pipeline to Phase I clinical trials, with market capitalizations generally ranging from $100 million to $300 million—roughly equivalent to the value of that core pipeline. As clinical development progressed or if the company attracted interest from multinational corporations (MNCs), institutional investors could seize the opportunity to exit.

Beyond scale, the rationale for project initiation also warrants consideration.

Taking recent transactions as an example, although LexinPharma’s most advanced asset is a Claudin18.2 ADC for gastrointestinal tumors, the project that truly garnered widespread attention is LM-299, which is still at the IND stage. This PD-1/VEGF bispecific antibody was acquired by Merck & Co. for an upfront payment of $588 million.

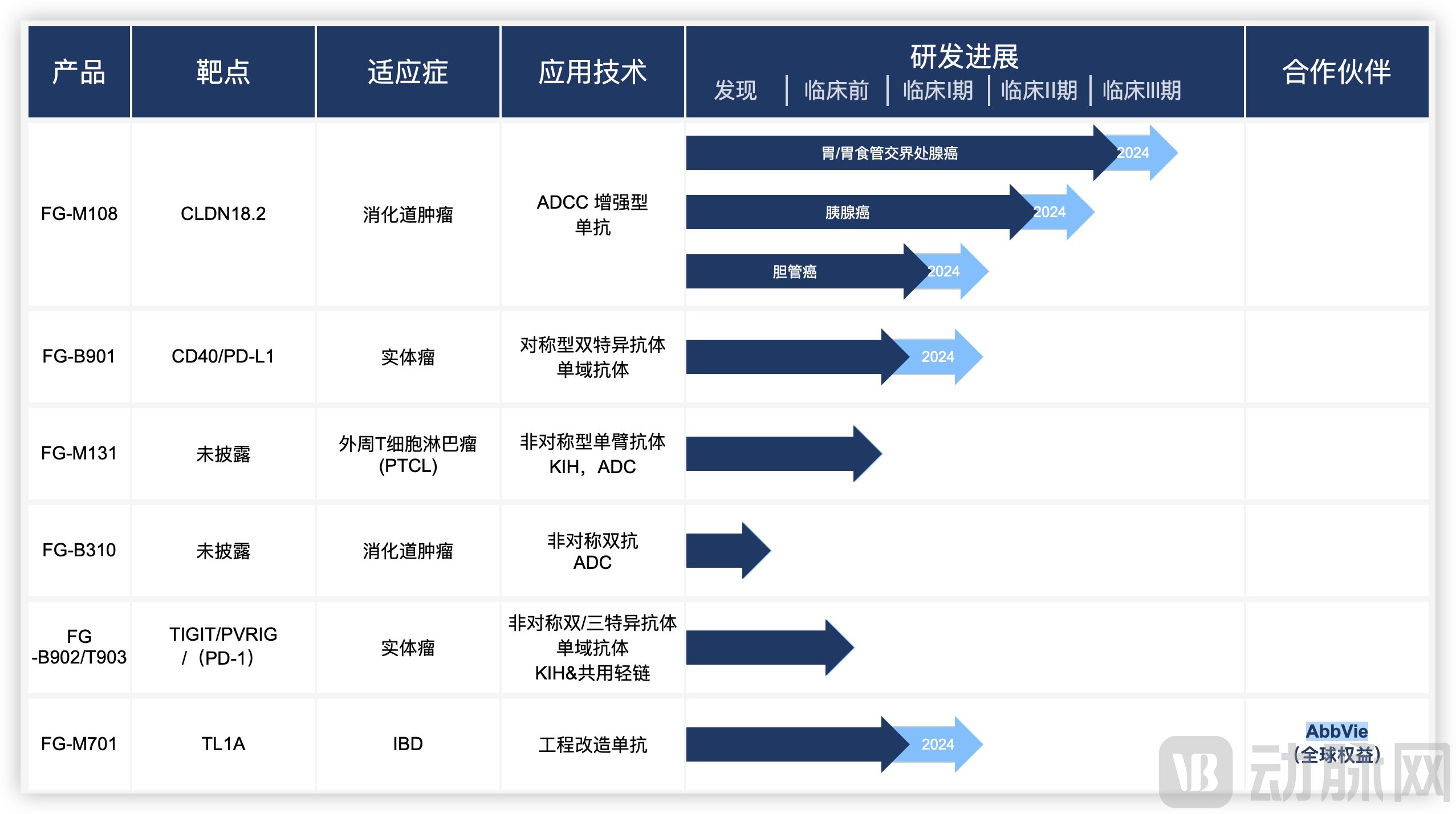

Mingji Biologics’ Product Pipeline, Source: Company Official Website

Mingji Biopharma is another case in point. Its core pipeline candidate, FG-M108, indicated for gastrointestinal tumors, has advanced to Phase III clinical trials. Meanwhile, a preclinical asset targeting TL1A was licensed to AbbVie for global rights, with an upfront payment of $150 million and milestone payments totaling $1.56 billion.

Coupled with Aiolos’s earlier divestment of Hengrui’s TSLP monoclonal antibody to GSK, the most notable characteristic of these pipelines is their alignment with the needs of multinational corporations (MNCs). Some of these needs are explicit, prompting MNCs to make direct acquisitions; others are implicit, with overseas biotech companies “packaging” their assets before selling them to MNCs. For Chinese biotech firms, the question arises: can they bypass intermediaries and engage directly?

As the saying goes, “respect the ‘middlemen,’ understand the ‘middlemen,’ and become the ‘middlemen’”; Chinese biotech companies have already begun to explore this path.

Some early-stage Chinese biotech companies aspire to emulate overseas small biotechs by securing direct financing or listing abroad; however, given the current landscape, the likelihood of success is extremely low. Meanwhile, more mature biotech firms often possess extensive pipelines that complicate valuation, making them less viable as primary entities for transactions. In this context, the emergence of NewCos offers a viable solution.

In essence, NewCo is akin to making a whole batch of dumplings just for a saucer of vinegar. The emergence of this model reflects current industry demands, but it is by no means a panacea.

NewCo’s core asset—its drug pipeline—remains subject to the same MNC-aligned standards, regardless of whether NewCo is ultimately acquired by a multinational corporation (MNC) or lists on the U.S. stock market. In other words, pipelines that can secure a deal for NewCo are highly likely to be suitable for business development (BD) out-licensing; conversely, assets that cannot be BD-ed out are unlikely to be valued by NewCo in the first place.

For domestic biotech companies, especially those that have reached a certain scale, NewCo serves as an ideal window to the world. Through NewCo, they can learn from overseas operational experiences, including pipeline “packaging”—that is, designing clinical development plans aligned with MNC preferences—as well as navigating subsequent M&A negotiations or IPOs, and building talent pipelines. When these companies eventually expand globally, such experience will help them avoid many pitfalls.

For early-stage biotech startups, the “small but beautiful” development model prevalent in the U.S. biotech sector may be an optimal choice at present. By focusing on high-potential pipelines, accelerating development to achieve timely monetization, and then embarking on new ventures, founders can craft a narrative of seasoned entrepreneurs capable of repeated commercial success within China’s current biotech landscape. Only through more deals akin to Gracell Biotechnologies’ acquisition by AstraZeneca can Chinese biotech companies transition from being perceived merely as “arsenals” for global pharmaceutical firms to becoming protagonists on the global stage.