Biotech Turns to Consumer Health for Survival Amid Funding Winter

It seems that overnight, biotech companies, which once regarded new drug development as their core mission, have begun to flock into the consumer health sector.

WithXueji BioTaking it as an example, the company focuses on stem cell research but has recently launched two products: facial masks and serums.Youjia BioLikewise, it is dedicated to the development of innovative small nucleic acid siRNA drugs, but currently has multiple anti-hair loss products on the market, including hair growth serums and scalp repair solutions; in addition, there areKintor Pharmaceutical, with a focus on innovative oncology therapies; however, in July this year, its self-developed topical anti-hair-loss solution for androgenetic alopecia (AGA) was officially approved for market launch.

Beyond these emerging categories, Biotech currently has a substantial portfolio of mature products in the consumer health sector. For example,SanBioIts ergothioneine capsules saw a 6,000% year-on-year increase in sales during the first half of this year, ranking first on JD.com’s bestseller list for the “ergothioneine” category. Additionally, in August this year, Sanhai launched the world’s first ergothioneine eye wash, which achieved over RMB 2 million in gross merchandise value within just six hours of its launch, becoming one of the month’s newest blockbuster products.

In fact, this is merely the tip of the iceberg. There are many other best-selling products of this kind, and the hotter they sell, the more pronounced the sense of disconnection becomes. Whether it is skincare products dominated by facial masks, or daily consumer goods such as hair growth tonics and eye washes, it is difficult to associate them with biotech companies that have long focused on cutting-edge research. Even some biotech founders harbor a certain resistance to health consumer products, viewing them as lacking in technical sophistication and having extremely limited potential for market translation.

So, what exactly is the magic that is prompting an increasing number of biotech companies to set aside their “prejudices” and turn their attention to consumer health products? Answering this question is not difficult.The challenge lies in how Biotech companies can sustain their long-term growth logic after the transformation.?

Survival is an instinct

Survival pressures are indiscriminately confronting every biotech company.

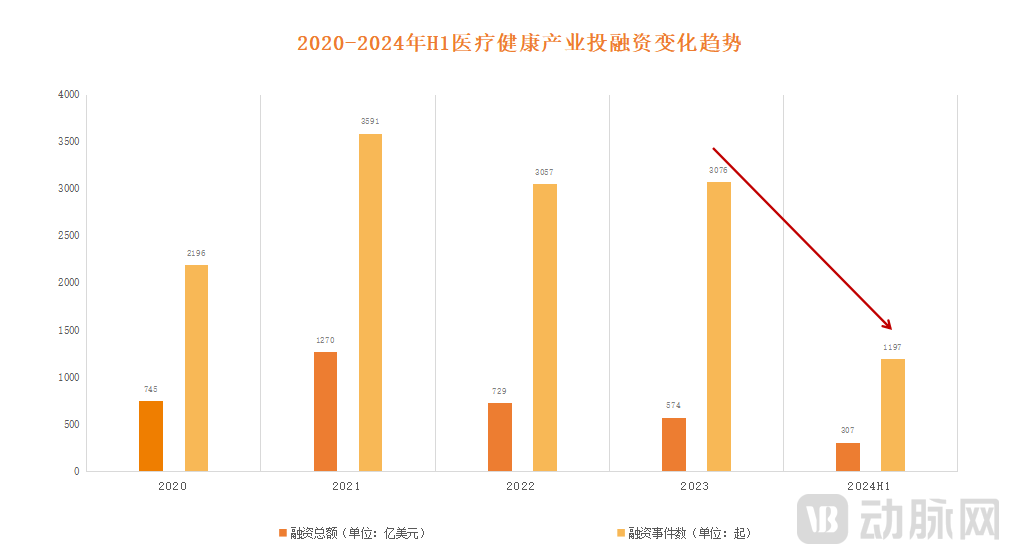

Figure 1. Trends in Investment and Financing in the Healthcare Industry from 2020 to H1 2024 (Data source: Artery Orange)

Figure 1. Trends in Investment and Financing in the Healthcare Industry from 2020 to H1 2024 (Data source: Artery Orange)

This trend has emerged against a complex backdrop of real-world factors. In addition to the inherent lack of monetization capabilities and high cost burdens faced by biotech companies themselves,The most critical variable is, in fact, the significant narrowing of current monetization channels.. Taking the primary market as an example, China’s healthcare sector completed 415 financing deals in the first half of 2024, with a total funding amount of approximately USD 4.8 billion, representing year-on-year declines of 32.3% and 12.2%, respectively. The secondary market was even more dismal; as of November 2024, the number of biotech companies that terminated their IPOs this year had exceeded 100.

Consequently, under a prolonged state of operational imbalance between revenue and expenditure, Biotech companies are facing increasingly tight cash flows. Based on the 2023 annual reports of companies listed under Chapter 18A of the Hong Kong Stock Exchange, assuming that R&D investment remains unchanged this year,Approximately 13 listed biotech companies will have insufficient cash reserves at year-end to sustain operations through the remainder of this year.. If this is the case for listed companies, the situation is even more severe for the large number of pre-IPO biotech firms, according to industry insiders,Currently, the actual development of approximately half of biotech companies has stalled or they have dissolved, with some firms laying off staff to the point that only the founders remain.。

Therefore, in order to survive,BD, NewCo, and M&A monetization trends are heating up.Taking business development (BD) as an example, according to statistics from PharmaCube, the total upfront payments received by Chinese innovative drug companies through BD deals amounted to RMB 26.764 billion in 2023, surpassing the total funds raised through initial public offerings (IPOs) for the first time and reaching nearly twice the latter figure. This momentum continued into 2024; according to incomplete statistics from Frost & Sullivan, there were 34 license-out transactions in China’s innovative drug sector in the first half of 2024, with the total upfront payments for the top 10 deals reaching USD 720 million, approaching the annual totals of the previous two years.

Figure 2. The 17 biotech companies that achieved profitability in H1 2024 (Data source: public information)

Figure 2. The 17 biotech companies that achieved profitability in H1 2024 (Data source: public information)

As business development (BD) activities have fully ramped up, many biotech companies have leveraged this opportunity to turn losses into profits. It is reported that among the 17 biotech firms that achieved profitability in the first half of this year, seven relied on revenue from BD partnerships, includingHutchmed, Kelun-Biotech, Ascentage Pharma, Harbour BioMed, and other representative enterprises.

However,Whether through business development (BD) or mergers and acquisitions, the focus is always on biotech companies with robust pipelines. For the vast majority of biotechs, however, monetization requires exploring alternative paths. From the perspective of the current market, pivoting toward the consumer health sector is undoubtedly a viable option.。

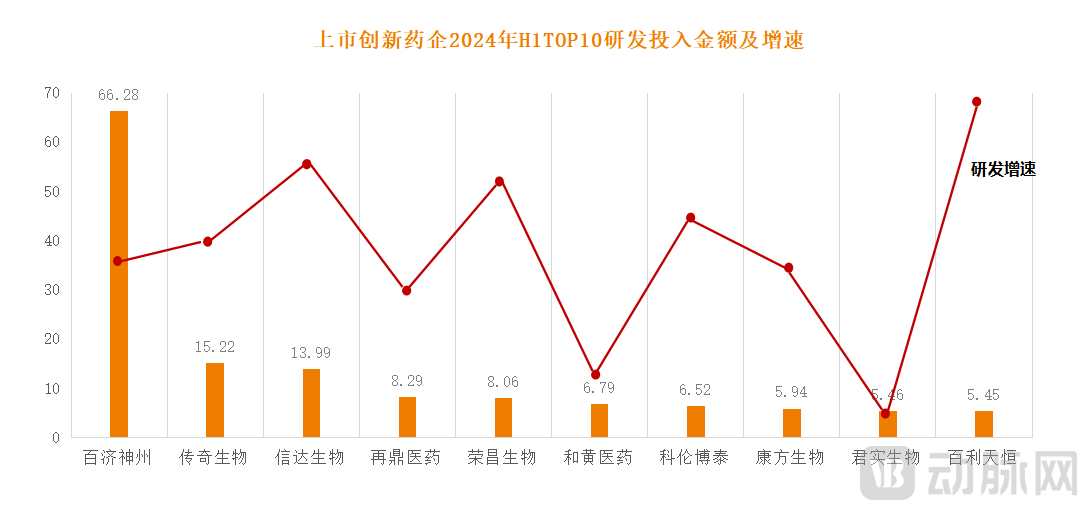

Figure 3. Top 10 R&D Expenditures and Growth Rates of Listed Innovative Pharmaceutical Companies in H1 2024 (Source: Public Information)

Figure 3. Top 10 R&D Expenditures and Growth Rates of Listed Innovative Pharmaceutical Companies in H1 2024 (Source: Public Information)

This is partly becauseConsumer health products generally undergo a relatively easier approval process with shorter cycles, thereby enabling faster monetization., enabling timely replenishment of cash flow for biotech companies. Taking skincare products as an example, the timeline from R&D to market launch is typically only 1–3 years, a stark contrast to innovative drugs, which often require more than a decade. Furthermore, consumer health products hold a distinct advantage in terms of R&D investment, generally accounting for just 1%–5% of a company’s annual revenue, whereas the proportion for innovative drugs approaches 30%. Therefore, for biotech companies eager to achieve rapid monetization, consumer health products—with their lower investment requirements and faster commercialization cycles—clearly offer greater “cost-effectiveness” in the current landscape.

On the other hand, from a demand-side perspective,Market demand in fields such as anti-aging and hair regrowth is currently expanding, accompanied by higher requirements for the safety and efficacy of related derivative products.. And all of this requires technical support from biotech companies, such asExosomes, Stem Cell DifferentiationCellular biology technologies can be widely applied in fields such as medical aesthetics, functional skincare, and health supplements; whereasPeptides, Carbohydrates, and Protein Engineering, and Small Nucleic Acidstechnologies such as these demonstrate strong applicability in the field of anti-aging; additionally, there has been considerable attention in recent years onSynthetic Biology, and it also holds significant application value in areas such as anti-aging and hair regrowth.

Fei Simin, a partner at Mingfeng Capital, which has long focused on investments in consumer healthcare, shared his insights on this matter. He stated, “This phenomenon has actually existed for a long time. The recent surge in semaglutide is an example of how the underlying biotech technology of GLP-1 has been extended into the consumer healthcare sector. Among the companies we have recently invested in or are currently evaluating, there are also cases where underlying technologies are being applied to the consumer healthcare field. Examples include using mRNA technology to produce collagen, employing peptide molecules to stimulate osteoblast generation for treating osteoporosis, and extending basic stem cell technologies into anti-aging applications.”

Therefore, taken together, the biotech industry’s collective pivot toward consumer health products is essentially an instinctive survival response amid a market winter. From another perspective, applying biotech innovations to consumer health sectors—including anti-aging, hair regrowth, and oral care—is also driving the transformation and upgrading of related products.

Same Direction, Different Paths

In fact, it is not new for pharmaceutical companies to develop consumer health products. For example, the well-known Pantene shampoo originated from Roche Pharmaceuticals. In later years, as Roche gradually shifted its focus to the two core areas of pharmaceuticals and diagnostics, it divested this business by selling it to Procter & Gamble. Another typical case is Sensodyne toothpaste, which was developed and manufactured by GlaxoSmithKline and remains in operation today.

Looking at the domestic market, there are also representative cases, with Yunnan Baiyao being the most well-known. It currently boasts a wide range of blockbuster products, including toothpaste, adhesive bandages, and aerosol sprays. Influenced by this trend, many traditional pharmaceutical companies have accelerated their transformation into consumer health products over the past decade, such asHuadong Medicine, Fosun Pharma, Jiangsu Wuzhong, CMS Pharmaceuticaletc. It has already achieved significant results in areas such as anti-aging, skin whitening, and repair, and has also generated strong cash flow.

Turning to the present, biotech companies are also venturing into the consumer health sector, with a significant increase in products that have already received approval or are currently under review. So, how does the transformation of biotech firms differ from that of “deep-pocketed” big pharmaceutical companies?

This is mainly reflected in three aspects,The first aspect lies in the different market entry strategies: large pharmaceutical companies primarily rely on mergers and acquisitions, whereas biotech firms tend to engage directly in development and operations.. This is not difficult to understand. For large pharmaceutical companies, the shift toward consumer health is primarily aimed at exploring new growth curves. Coupled with their substantial cash reserves, acquiring and merging mature products not only reduces risk but also accelerates monetization. Although biotech firms also aim to convert assets into cash flow, financial constraints often force them to cut costs and devote more resources to strategically positioning themselves in the consumer health sector.

Take Kintor Pharmaceutical as an example. In November 2023, due to setbacks in the development of its core pipeline asset—a small-molecule androgen receptor antagonist—and insufficient funding to conduct Phase III clinical trials, the company chose to suspend its original pipeline. It also recovered some previously invested assets, discontinued non-core projects, and concentrated its cash flow to prioritize its layout in cosmetics and hair loss products. By July this year, its cosmetics business, represented by the brand KOSHINE, had gradually been launched.

The second difference lies in their areas of focus: large pharmaceutical companies tend to prioritize currently popular products, whereas biotech firms mainly engage in “secondary development” within the consumer health sector, leveraging their core technologies.. In short, biotech companies are extending their core technologies or experimental findings from established serious medical scenarios to consumer healthcare scenarios.

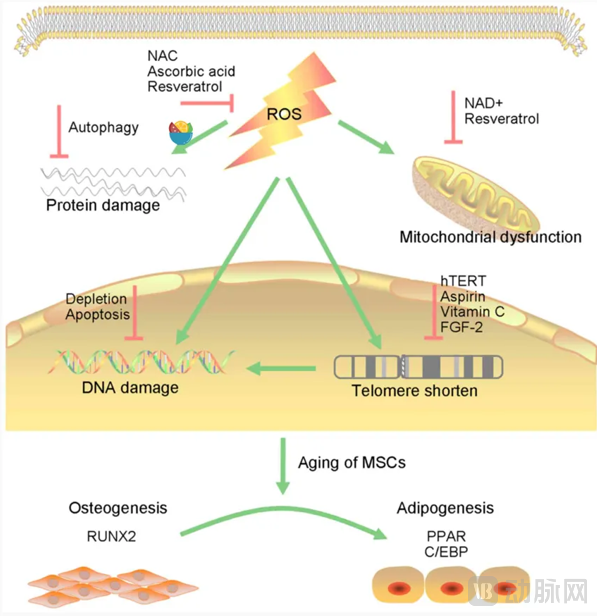

Figure 4. Mechanism of stem cell technology in anti-aging (Image source: public literature)

Taking small nucleic acids as an example, their development was originally focused on therapeutics for tumors, cardiovascular diseases, and other conditions. However, they also hold application value in the field of anti-aging. By targeting aging-related genes in the skin and regulating collagen production and metabolism, small nucleic acids can enhance skin elasticity and reduce wrinkle formation. Similarly, stem cells are primarily used in the treatment of neurological and autoimmune diseases due to their immunomodulatory functions. Yet, stem cells also possess differentiation potential, enabling them to differentiate into various types of skin cells, which promotes skin cell regeneration and thereby enhances the skin’s self-repair capacity. In addition, other biomolecules such as peptides and exosomes also find application scenarios in the consumer health sector.

The third aspect lies in the differences in promotional models. Large pharmaceutical companies can leverage their brand influence, as well as existing channels and resources, to rapidly deploy in the market and gain a first-mover advantage. In contrast, most biotech startups start from scratch, adopting more grounded and proactive promotional strategies.。

Taking Jinsan Biology as an example, its rise to the top position in the ergothioneine category within three years is attributed not only to the significant price reduction achieved through synthetic biology technology but also, importantly, to its unique market promotion strategies. It is reported that to penetrate the consumer market, Jinsan engaged industry veterans and implemented comprehensive promotional campaigns across platforms such as Douyin, Xiaohongshu (Little Red Book), and Zhihu. By leveraging diverse formats—including educational articles, short videos, and influencer recommendations (“zhongcao”)—the company rapidly built brand equity while simultaneously facilitating related transactions.

It is evident that although large pharmaceutical companies and biotech firms share the same ultimate goal in transitioning to the consumer health sector, their distinct starting conditions inevitably lead to markedly different paths and strategic choices.

Long-Termism After Transformation

The metric for a successful transformation is the ability to establish a firm foothold in new markets; by analogy, in the biotech sector, this means itsCan Consumer Health Be a Long-Term Business?Especially against the backdrop of sluggish overall industry growth and intensifying competition, how should biotech companies founded by outsiders respond?

In response, a senior expert provided an answer and outlined two typical characteristics:First, it must maintain technological leadership and contribute to cost reduction and efficiency improvement; second, it must take the lead in establishing a brand image of cutting-edge technology on the operational front.。

Let’s start with the first point: technology. As is well known, the greatest advantage of biotech lies in its R&D capabilities, which can also be effectively applied in the consumer health sector. By integrating innovative technologies, it is possible to address the technical pain points of existing products and thereby deliver higher-performance consumer health products. In short,Biotech Companies Must Remain Technology-Driven During Their Transformation。

In fact, leveraging technological advantages to create differentiated products has always been key to sustaining long-term market competitiveness. Taking the medical aesthetics sector as an example, Fei Simin, Partner at Mingfeng Capital, stated, “It is highly promising to extend current biotech biomaterial technologies into the medical aesthetics field. These biotechnologies can enable greater functional expansion of existing medical aesthetic materials, such as enhancing their structural properties and facilitating better drug-device combination through encapsulation and delivery systems. For instance, applying pharmaceutical-grade raw materials like PDRN to subcutaneous injections in consumer-oriented medical aesthetics, thereby achieving drug-device combinations, represents another valuable opportunity.”

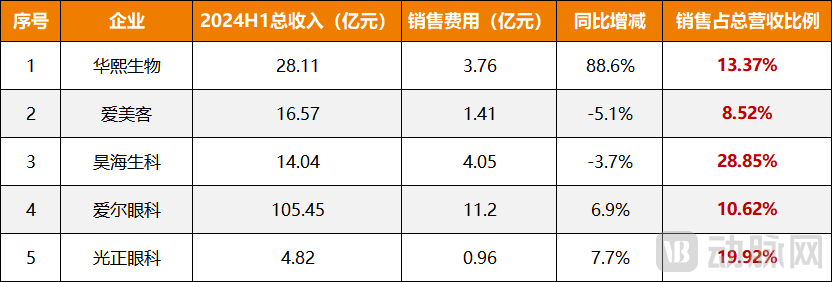

Figure 5. Sales Expenses and Their Proportion for Selected Consumer Healthcare Companies (Source: Public Information)

Figure 5. Sales Expenses and Their Proportion for Selected Consumer Healthcare Companies (Source: Public Information)

Having discussed technology, let us turn to the second point: promotion. Unlike the growth logic of innovative drugs, where exceptional clinical performance can generate hundreds of millions in revenue even before regulatory approval for market launch, consumer health products do not share this characteristic. Their monetization typically requires sustained marketing efforts, which happens to be the area where biotech companies are least proficient. Nevertheless, promotion is critically important. An analysis of annual reports from major consumer healthcare companies reveals that marketing expenditures generally account for 30% to over 40% of their total spending.

Thus, a question is growing increasingly prominent: How exactly should biotech companies approach marketing? By synthesizing multiple success stories and expert perspectives,VCBeat believes that it must have a robust content system capable of clearly articulating the stories of how biotech innovations are implemented in health consumer scenarios.Specifically, this entails possessing the ability to communicate with and persuade industry stakeholders, channel partners, and consumers over the long term.

In this regard, a seasoned investor remarked, “Although the health consumption industry is rapidly entering the technology era, marketing remains critically important at present. Taking a skincare product as an example, the cost of its active ingredients typically accounts for less than 10%, with the majority of expenditures directed toward customer acquisition. Therefore, for biotech companies, it is particularly crucial to establish a robust content system in their marketing efforts to facilitate effective communication with ‘lay’ professionals.”

From the perspective of Fei Simin, a partner at Mingfeng Capital, in addition to technology and market considerations, specific product design and the management of safety during frequent use—particularly in scenarios where such use is not strictly necessary—are also critical logical frameworks that biotech companies must address during their transformation.

However, these challenges cannot be formed overnight. Of course, this is not a problem unique to biotech companies, but rather a collective dilemma currently faced by the entire consumer health sector. Nevertheless, one increasingly undeniable fact remains:Biotech is slowly pivoting, beginning to walk on “two legs” with innovative drugs and consumer health products.。

And such a change is particularly commendable in the midst of a market winter.

1. “How Should We Navigate the Transition from Serious Medicine to Consumer-Friendly Healthcare?” — Tong Xieyi;

2. “The Mid-Term Dilemma of Biotech: Cash Flow Bottoms Out, Awaiting Angel Investors” — DeepBlue View;

3. “2024: Consumer Healthcare Faces Tough Times” – Amino Observation