Surge of Healthcare Companies Rushing to IPO on HKEX Amid Policy Shifts and A-Share Bottlenecks

Recently, IPO applications from healthcare companies on the Hong Kong Stock Exchange have entered a new surge: nine companies filed their prospectuses in November, marking the highest monthly total so far this year, while five more applied for listing in the first half of December.

Among them, HanSi AiTai, Dazhong Stomatology, Weilizhibo, Yinnuo Medicine, and HEC Pharm have submitted their initial listing applications to the Hong Kong Stock Exchange (HKEX); meanwhile, Xuanzhu Biopharma and Changfeng Pharma have turned to the HKEX after halting their attempts on the STAR Market.

With the A-share listing channel facing bottlenecks, the Hong Kong stock market has become the optimal choice for IPOs for many companies. Since 2024, ten healthcare companies have successfully listed on the Hong Kong Stock Exchange. So, is the path to the Hong Kong Stock Exchange really that smooth?

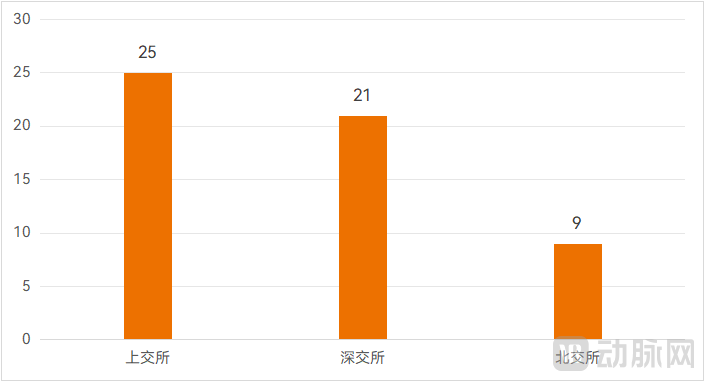

According to information disclosed on the HKEXnews website, as of December 15, 2024, a total of 47 healthcare companies had filed 61 prospectuses with the Hong Kong Stock Exchange (including refilings after previous lapses). Notably, the sector entered a surge period in the first half of November alone, during which 14 companies submitted their prospectuses.

Companies that have submitted prospectuses on the Hong Kong Stock Exchange since November 2024, Source: HKEXnews

Typically, driven by the timing of performance disclosures in prospectuses, small peaks in IPO application submissions often occur in June and December. However, the surge in 2024 was underpinned by new industry dynamics.

On the one hand, it is driven by policy guidance.

On April 19, 2024, the China Securities Regulatory Commission (CSRC) announced five measures to enhance cooperation between the mainland’s capital markets and Hong Kong. The measures stated that support would be provided for eligible leading enterprises from key industries in the mainland to list and raise capital in Hong Kong.

Additionally, 1On October 18, the Hong Kong Securities and Futures Commission (SFC) and the Hong Kong Stock Exchange (HKEX) jointly announced optimizations to the timeline for reviewing new listing applications. These enhancements cover two categories: listing applications that fully comply with regulatory requirements, and listing applications from eligible A-share companies seeking to list in Hong Kong.

Where the new listing application and related materials submitted by the applicant and its sponsor are fully compliant with relevant regulatory requirements and guidelines, the Securities and Futures Commission (SFC) and The Stock Exchange of Hong Kong Limited (HKEX) will maintain close communication to avoid duplicative inquiries. After issuing no more than two rounds of regulatory comments respectively, each party will assess and indicate whether there are any material regulatory concerns regarding the application.

Under the optimized approval process, applicants and their sponsors are expected to provide satisfactory responses to comments raised by regulatory authorities within a total of approximately 60 business days. Subject to obtaining approvals from the Listing Committee and other relevant departments or regulatory bodies, the application procedure is anticipated to be completed within the six-month validity period of the application.

For A-share companies submitting applications for listing on the Hong Kong Stock Exchange, if their expected market capitalization is at least HK$10 billion and it is confirmed, with support from legal opinions, that the company has complied in all material respects with laws and regulations related to its A-share listing during the two complete fiscal years preceding the submission of the new listing application, then the new listing application may be reviewed under an expedited approval timetable.

Under the fast-track approval timetable, if an eligible A-share listed company submits a fully compliant application, the Securities and Futures Commission of Hong Kong (SFC) and The Stock Exchange of Hong Kong Limited (HKEX) will each issue only one round of regulatory comments. In such cases, the respective regulatory assessments by the two regulators will be completed within no more than 30 business days.

The optimized approval process is undoubtedly highly attractive to enterprises.

On the other hand, the narrowing of IPO channels in China’s A-share market is forcing companies to seek alternative paths.

Since the China Securities Regulatory Commission (CSRC) announced a phased tightening of the IPO pace in August 2023, IPO access has become increasingly stringent, with a noticeable slowdown in the acceptance of IPO applications and listings committee reviews. This trend continued into 2024.

The most typical phenomenon is the emergence of large-scale “withdrawals of IPO applications.” According to incomplete statistics from VCBeat, since 2024, more than 50 healthcare-related companies listed on China’s three major stock exchanges have withdrawn their filing materials, resulting in the termination of their IPO reviews. These companies include star enterprises in the biopharmaceutical venture capital circle, which had received investments from multiple renowned institutions and extensively laid out innovative product R&D, as well as companies that have been operating for many years and have already achieved a certain scale of revenue.

Some companies had already reached the inquiry stage before withdrawing their applications; based on the acceptance dates, their queueing time was approximately one year. In individual cases, companies withdrew their applications even after waiting in the queue for nearly two years and being just one step away from listing.

Healthcare Companies Whose Reviews Were Terminated by the Three Major A-Share Exchanges in 2024 (as of December 16); Data Source: Official Websites of the Respective Exchanges

In the first half of 2024, after the termination of their listing reviews on the STAR Market, Xuanzhu Biopharma and Changfeng Pharma successively filed prospectuses with the Hong Kong Stock Exchange in November 2024.

In the current context, whether for companies still on the sidelines or those that have terminated their A-share listings, pivoting to the Hong Kong stock market, which has just introduced new policies, remains a viable option.

So, is the path to listing on the Hong Kong Stock Exchange an easy one?

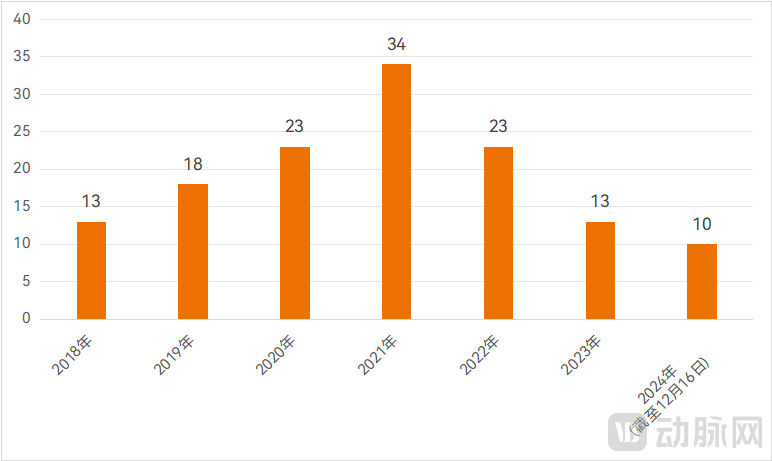

According to information disclosed on the HKEXnews website, a total of 10 healthcare companies have successfully listed on the Hong Kong Stock Exchange (HKEX) from 2024 to date. Although this figure falls far short of the peak levels seen in and around 2021, it represents a generally stable performance compared with 2023. Moreover, as Health Road and iFlytek Healthcare have recently passed the listing hearings, both companies may still manage to catch the last IPO train of 2024.

Listing of Healthcare Companies on the Hong Kong Stock Exchange Since 2018; Data Sources: HKEXnews, Ryan Capital

Healthcare Companies Listed on the HKEX Since 2024, Source: HKEXnews

Among the 10 companies that have gone public, most either generate no revenue from their core business or have yet to achieve profitability, a trend that remains largely consistent with the past.

Among the numerous companies in the IPO queue, some are able to complete their listings at a relatively faster pace.

Tongyuankang Pharmaceutical, Taimei Medical Technology, Huahao Zhongtian, and Jiuyuan Gene were among the companies that filed their prospectuses for the first time in 2024 and successfully went public within the same year.

Among them, as the 66th Chapter 18A company listed on the Hong Kong Stock Exchange (HKEX), Tongyuan Kang completed its initial public offering in less than seven months. In January 2024, Tongyuan Kang Pharmaceutical submitted its prospectus to the HKEX for the first time; after it lapsed, the company updated the prospectus in July 2024 and ultimately achieved a successful listing on August 20.

Depending on the specific characteristics of each company, leaders in niche segments and “first-of-their-kind” listings continue to be well received in the Hong Kong stock market. Companies such as Quanxin Biologics, Shenghe Biologics, Yimai Yangguang, XtalPi (renamed “XtalPi Holdings”), and Huahao Zhongtian have all listed on the Hong Kong Stock Exchange as the first publicly traded companies in their respective fields.

On March 20, Quanxin Biopharma, the “first IPO in Hong Kong’s autoimmune sector,” went public. According to Frost & Sullivan, as of March 2, 2024, Quanxin Biopharma was one of the pharmaceutical companies in China with the highest number of Investigational New Drug (IND) approvals in the fields of autoimmune and allergic diseases.

On May 24, Shenghe Biopharma, known as the “first antibody-cytokine stock,” held its initial public offering (IPO) on the Hong Kong Stock Exchange. As of its listing, Shenghe Biopharma had nine products in its development pipeline, six of which had entered clinical stages. These included three antibody-cytokine candidates filed for clinical trials in both China and the United States, all representing the fastest-moving antibody-cytokine therapies globally in clinical development for cancer patients.

On June 27, Yimai Yangguang, a third-party medical imaging service provider, listed on the Hong Kong Stock Exchange. As no company primarily engaged in third-party medical imaging services had previously gone public, Yimai Yangguang has become the “first stock in medical imaging services.”

On June 13, XtalPi Holdings, known as the “first AI-driven new drug stock,” was listed on the Hong Kong Stock Exchange. Addressing various challenges in new drug development, XtalPi integrates quantum physics, artificial intelligence, and robotics into solid-state R&D, delivering higher efficacy and precision within a shorter timeframe while reducing costs for developers.

On October 31, Huahao Zhongtian debuted as the first pharmaceutical synthetic biology company listed on the Hong Kong Stock Exchange. Since its establishment, Huahao Zhongtian has successfully developed three core technology platforms dedicated to the R&D of novel drugs based on microbial metabolites, and boasts one core commercialized product, Utidelone Injection, along with 19 projects in the pipeline.

Even if a company fails to become the “first IPO” in an emerging niche, it can still gain a competitive edge by pivoting promptly, capitalizing on market trends, and rising to the forefront.

Jiuyuan Gene is a typical example. Established in 1993, Jiuyuan Gene’s current business spans four major therapeutic areas: orthopedics, metabolic diseases, oncology, and hematology. The company has eight marketed products and ten products in development, with orthopedic products serving as its primary revenue source. However, Jiuyuan Gene has now emerged as a standout enterprise among the first tier of domestic GLP-1 drug manufacturers, positioning GLP-1 therapies as its new growth curve.

Notably, healthcare service providers remain a significant component of IPOs on the Hong Kong Stock Exchange. Meizhong Jiahe, Fangzhou Jianke, and Yimai Yangguang have successfully listed, demonstrating their value in enhancing the quality and efficiency of healthcare delivery systems within their respective niche sectors.

As one of the few private healthcare providers in China equipped with multiple proton therapy treatment rooms, USCC Health also possesses advanced capabilities in the research and application of oncology diagnosis and treatment technologies.

Third-party medical imaging services have been a key area of strong national support in recent years. Third-party medical imaging service providers, including Yimai Yangguang, have played a significant role in improving access to medical care, promoting the balanced distribution of healthcare resources, and enhancing the diagnostic imaging capabilities at the primary care level.

Furthermore, Fangzhou Jianke has established an online chronic disease management platform to provide users with professional, efficient, convenient, and accessible medical and chronic disease management services.

Healthcare services require heavy-asset, long-cycle investments, with extended payback periods. In this context, enterprises that have already achieved a certain revenue scale and demonstrate improving profitability will hold a significant advantage.

At the time of Meizhong Jiahe’s IPO, the company’s revenue continued to grow, with an annual income of RMB 472 million (the latest full year disclosed in the prospectus was 2022), and its losses gradually narrowed starting from 2021. From 2021 to 2023, Yimai Yangguang’s total revenue increased from RMB 592 million to RMB 929 million, achieving a turnaround from loss to profit in 2023. Fangzhou Jianke also demonstrated a strong revenue growth trend, rising from RMB 1.759 billion in 2021 to RMB 2.434 billion in 2023.

Overall, the Hong Kong Stock Exchange remains at least a safe and reliable option. It will take time for the effects of the new policies optimizing the approval process to become apparent, and whether the process will become smoother remains to be seen.

However, from another perspective, it is also important to recognize the various challenges associated with pursuing an IPO in Hong Kong.

In 2024, two healthcare companies passed the HKEX listing hearings in February and August, respectively, but have yet to go public. In fact, while both companies have demonstrated significant revenue growth, narrowing losses, and innovative value within their respective fields, they still face internal and external uncertainties.

Meanwhile, Hong Kong-listed stocks under Chapter 18A have entered a cooling-off period, with their financing function subject to further evaluation.

Since 2024, Quanxin Biopharma, Shenghe Biotech, and Tongyuankang Pharma have gone public under Chapter 18A of the Hong Kong Stock Exchange Listing Rules. Among them, Shenghe Biotech had an issuance market capitalization of just over HK$2.1 billion, making it the smallest biotech company by issuance market cap since the introduction of Chapter 18A in the Hong Kong stock market.

It is reported that since the implementation of Chapter 18A of the Listing Rules, a total of 66 biotechnology companies have successfully listed on the Hong Kong Stock Exchange under this framework. However, fundraising performance for many of these enterprises has been modest, with the share prices of multiple companies trading below their IPO issue prices; notably, the share prices of some companies have even fallen below HK$1, and two companies have market capitalizations of approximately HK$100 million.

For pre-revenue, for-profit biopharmaceutical companies, the primary purpose of going public is to fund ongoing research and development (R&D). For many Chapter 18A biopharmaceutical companies listed on the Hong Kong Stock Exchange, despite achieving this critical milestone, they face the dilemma of unfavorable financing conditions, making it difficult to advance subsequent R&D efforts.

Therefore, while the Hong Kong Stock Exchange (HKEX) represents a relatively stable listing option, various factors associated with an initial public offering (IPO) must be duly acknowledged. For both Chapter 18A companies and other healthcare enterprises, an IPO is merely one component of their financing strategy, serving as a complement to performance growth. In terms of operational performance, revenue streams can be generated through commercial product sales or business development (BD) transactions involving product pipelines.Regardless of how the external market environment changes, companies that possess both innovative R&D capabilities and commercialization prowess will always be more competitive.

References

Shanghai Securities News: Optimizing the IPO Process! Hong Kong Takes Action

PharmaDJ: HKEX Chapter 18A Welcomes the Smallest-Market-Cap Biotech IPO

Huayi Xin Capital Group: Analysis of the Current Status of HKEX Chapter 18A Companies