2024 Digital Health Annual Innovation White Paper: The Era of 'Hundred Medical Large Models' and Record-Breaking Funding Round

Digital Health is widely recognized as a process that leverages a suite of emerging digital technologies—including artificial intelligence, mobile internet, the Internet of Things (IoT), virtual reality, and health information technology—delivered via software platforms and driven by data. By empowering and optimizing the entire core healthcare workflow, it transforms the health system from a provider-centric model into a patient-centric digital health ecosystem, thereby enhancing the capabilities and experiences of patients, healthcare providers, and healthcare system administrators.

Driven by the Fourth Industrial Revolution, led by information and communications technology, big data, and artificial intelligence, digital healthcare is rapidly advancing the medical and health sector. This revolutionary progress is swiftly transforming the industry, as technologies such as artificial intelligence (including large language models), the Internet of Things, virtual reality, blockchain, digital diagnostics and therapeutics, telemedicine, and consumer-oriented mobile health applications have moved from concept to reality, bringing convenience to all stakeholders in the healthcare ecosystem.

Even the most skeptical critics of digital health cannot deny its immense value over longer historical cycles. This explains why, despite an unfavorable macroeconomic environment over the past year, the digital health sector has continued to surge forward and evolve rapidly. As long-term observers of the digital health industry, VCBeat and VBInsight feel a profound responsibility to document and organize this evolution. Therefore, we have once again embarked on this endeavor to produce the “2024 Annual White Paper on Digital Health Innovation,” recording the joys and sorrows of digital health from an outsider’s perspective.

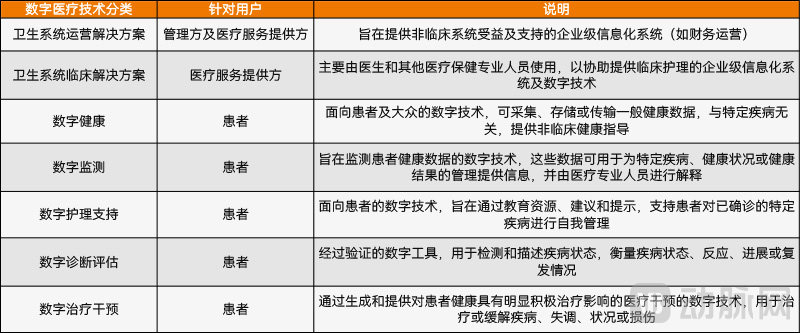

Digital healthcare is a relatively broad concept. We have adopted previous research methodologies to define the scope of our study as follows: operational solutions for healthcare systems, clinical solutions for healthcare providers, and five types of patient-oriented digital health technologies, namely digital health, digital monitoring, digital care support, digital diagnostic assessment, and digital therapeutic interventions.

Definition and Scope of Digital Health in This White Paper

Primary market conditions have always served as one of the bellwethers for the overall industry trend. VBInsight, using the period from December 2023 to October 2024 as its analysis window and conducting incomplete statistics on investment and financing data, identified 74 valid domestic digital health-related investment and financing events involving 73 Chinese digital health companies.

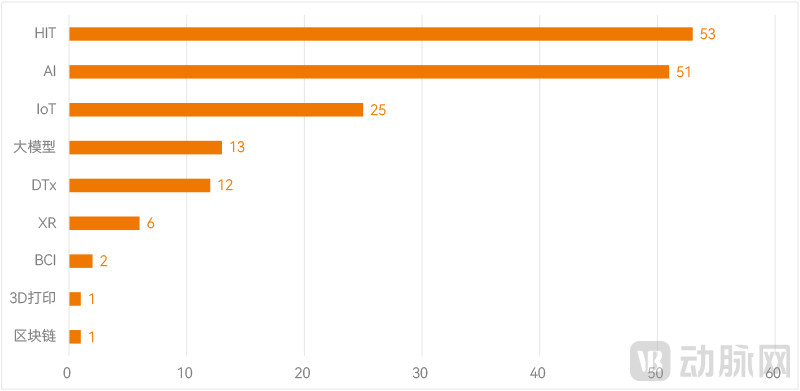

Although the number of financing events was lower than in the same period of 2023, the total cumulative funding amount increased. Notably, Baichuan Intelligence’s RMB 5 billion financing round completed in July 2024 set a recent record for single-round fundraising in the digital health sector. Additionally, 51 financing events involved companies whose core businesses include artificial intelligence (AI), with 13 of these specifically related to large language models (LLMs). These figures underscore the significant momentum and high level of interest in AI, particularly LLMs, throughout 2024.

Comparison of China's Digital Health Primary Market in 2024 vs. the Same Period in 2023

Nevertheless, the commercialization of large language models remains in its early stages, with more than half of all financing events occurring at the angel or Series A rounds. The future trajectory of healthcare-specific large language models will still need to withstand scrutiny from various stakeholders.

Classification of Financing in China's Digital Health Industry by Technology

Affected by various factors, the path to public listing for domestic digital health companies in 2024 was not smooth. Two companies were listed on the NEEQ (National Equities Exchange and Quotations), and another one went public on NASDAQ. However, four companies have already reached Series D or even Series E funding this year, and may enter the secondary market in the future.

In terms of policy, according to incomplete statistics, China’s central government issued more than 40 key policies closely related to digital healthcare in 2024. These policies have provided significant impetus to the development of the digital healthcare industry.

In terms of regulatory approval, the digital health sector has maintained its recent rapid momentum. Taking AI-based medical devices as an example, a total of 41 such devices received Class III medical device registration certificates in China during the study period. Although this figure is lower than the 47 approvals recorded in the same period last year, the gap is narrow, marking the second consecutive year with more than 40 approvals.

As of the study period, a total of 162 AI-based medical devices have obtained Class III certification in China. Among them, four companies each had more than 10 AI-based medical devices approved for Class III certification, accounting for nearly 30% of the total approvals. Furthermore, three of the AI-based medical devices approved in 2024 were granted approval through the expedited review pathway for innovative medical devices, highlighting the innovativeness of China’s AI-based medical device sector.

The digital therapeutics sector has also maintained a high growth rate. According to incomplete statistics, 40 software medical devices that meet the widely accepted definition of digital therapeutics were approved in 2024, reaching a new high in recent years. As of 2024, a total of 128 “digital therapeutics” products have received regulatory approval and obtained medical device certifications. Nevertheless, the current product landscape for “digital therapeutics” in China is highly concentrated, with the vast majority focused on cognitive impairment and ophthalmology, resulting in significant homogenization.

Furthermore, according to incomplete statistics from the High-End Medical Device Institute’s Data Center, as of the third quarter of 2024, four products categorized as “medical software” had entered the expedited approval process for Class II innovative medical devices across various provinces, with two from Shanghai and two from Jiangsu. Meanwhile, two products that had previously entered this expedited approval pathway ultimately received approval as Class II innovative medical devices within the year. One of these features artificial intelligence capabilities, while the other is a typical VR-based digital therapeutic. These represent the current primary directions of innovation in digital healthcare.

The progress made in digital health in 2024 was breathtaking. In particular, the rapid transition of large language model (LLM) technology from concept to practical implementation, covering various healthcare application scenarios, stands out as a major highlight of digital health in 2024. Furthermore, the maturation and advancement of digital technologies such as extended reality (XR) have enabled their increasing deployment across a growing number of use cases.

In 2024, large language models (LLMs) gradually transitioned from conceptual frameworks to practical implementation. According to incomplete statistics, there are now over one hundred LLMs applied in the healthcare sector, covering a wide range of scenarios and nearly all segments of digital health. “AI agents” (i.e., AI intelligent agents powered by LLM technology) have also become one of the most prominent keywords in the field of large models. Taking Tencent Health as an example, it has achieved large-scale deployment of its AI-powered intelligent pre-consultation system. This AI tool, which automatically summarizes pre-visit reports for attending physicians, has reached an accuracy rate of 87% in generating medical record summaries, with average monthly usage exceeding 20,000 instances.

JD Health, a giant in the internet healthcare sector, also launched its intelligent health assistant product, “Kangkang,” for pre-consultation scenarios this year. It can answer users’ health inquiries at any time and precisely and efficiently match them with medical service resources. In April last year, JD Health launched China’s first internet hospital specializing in dermatology, establishing one of the country’s first online medical service platforms dedicated to skin care. Leveraging the Jingyi Qianxun large language model, the AI-assisted diagnosis accuracy rate at JD Health’s Dermatology Internet Hospital exceeds 95%, and the paid conversion rate for patients using its specialized disease follow-up services has reached 20%.

In addition, the integration of large language models with IoT hardware for continuous monitoring of users’ physiological indicators has emerged as a prominent highlight in LLM applications in 2024, enabling more targeted personal health management and disease risk prediction.

For instance, “SHANMU” combines its “Sense Series” fully automated biochemical analyzer—which is the most miniaturized globally and adheres to the same standards as hospital-grade automatic biochemical analyzers costing millions of yuan in terms of sensitivity, precision, and specificity—with personalized AI pathology models. By pre-collecting multi-dimensional personal data such as user height, weight, age, preferences, medical history, and current symptoms, and integrating these with quantitative results of molecules, proteins, and markers in each urine sample, the system enables tracking, early prediction, and auxiliary diagnosis for conditions including prediabetes, hyperuricemia, chronic nephritis, and female hormonal imbalances. As user data continues to accumulate, the “Sense Series” vertical pathology model of “SHANMU” will deepen its understanding of users’ health status, providing increasingly professional and precise health feedback. This paves the way for creating a true “family doctor” in the era of Artificial General Intelligence (AGI).

In addition to large language models, the application of artificial intelligence (AI) in medical imaging had already permeated the entire workflow of screening, diagnosis, treatment, and prevention by 2024. In terms of departmental adoption, AI for medical imaging is gradually expanding from radiology to a broader range of clinical departments. Taking pathology and electrocardiography (ECG) as examples, these areas also face challenges such as heavy workloads and a scarcity of relevant medical resources. Significant breakthroughs have been made in these fields in recent years through AI empowerment, which is poised to transform the operational logic of their applications in the future.

Tencent Health has partnered with Mindray Medical to jointly develop a fully automated cell morphology analyzer for complete blood count (CBC) testing (AI slide reader). Leveraging the core technologies of Tencent AI Lab and the comprehensive solutions of Tencent Cloud, this product incorporates AI algorithms to clearly reconstruct the three-dimensional structure and details of cells, achieving an AI-based slide reading accuracy rate of over 95%. The AI slide reader also significantly improves reading efficiency, reducing the average time physicians spend on slide interpretation from the original 25–30 minutes to under 30 seconds. As a benchmark for innovative integration of “healthcare + AI,” this product has broken the monopoly previously held by a single imported brand in the slide reader market, filled a domestic gap, and has been installed in more than 400 hospitals worldwide.

Whether in terms of approval data or breakthroughs in specific diseases and medical specialties, these achievements reflect the strong momentum of China’s medical artificial intelligence sector in recent years. This has also attracted an increasing number of multinational corporations to invest more heavily in local innovation, fostering mutual empowerment through ecosystem partnerships with domestic medical AI innovators.

Taking GE HealthCare as an example, since 2021, it has established three major innovation centers in Beijing, Wuxi, and Shanghai, respectively targeting the supply chain, imaging chain, and digital chain, based on local industrial layouts and its own resource advantages. Among them, the Shanghai Innovation Center is GE HealthCare’s first innovation platform in China focused on digital health, and it is the largest and most functionally comprehensive innovation entity among the three innovation centers. It focuses on innovation in digital health technologies and applications, creating a “smart brain” to empower GE HealthCare’s R&D in China. To date, the GE HealthCare Shanghai Innovation Center has collaborated with more than 50 partners from various sectors. In the field of artificial intelligence alone, it has introduced nearly 90 digital products/technologies for integrated innovation and clinical application, which will also accelerate the construction of a local medical innovation ecosystem and promote the “two-way integration” of digital technologies and clinical applications.

A clear trend is the surging enthusiasm among healthcare institutions for developing their own large language models (LLMs). This is hardly surprising, as healthcare providers have the deepest understanding of their specific operational needs. LLM vendors are also lowering the barriers to development by providing various technical tools and frameworks—effectively “teaching them to fish”—thereby empowering healthcare institutions to independently build and deploy LLM-based applications.

For instance, Yidu Tech has established a dual-middle-platform model comprising a “Data Middle Platform + AI Middle Platform,” enabling hospitals to independently develop intelligent applications according to their specific needs and thereby achieve secure, professional, and autonomous construction of smart hospitals. Taking Sun Yat-sen University Cancer Center as an example, the hospital leveraged the AI Middle Platform to independently build a large language model designed for personalized out-of-hospital services for nasopharyngeal carcinoma patients, achieving intelligent upgrades across multiple dimensions of its business systems, including scientific research, patient recruitment, and patient services. Moreover, the large language model developed through the collaboration between Yidu Tech and hospitals achieved notable success in the “Healthcare Big Data Track” of the “2nd National Digital Health Innovation Application Competition” organized by the National Health Commission.

In the field of healthcare informatization in 2024, IT application innovation (Xinchuang) has become an unavoidable topic. Since late 2023, the pace of Xinchuang adoption in the healthcare sector has accelerated sharply, driven not only by policy support but also by gradual breakthroughs in Xinchuang-related hardware and software technologies.

For instance, Yidu Tech and Ascend AI have jointly launched an integrated training and inference appliance that meets the data security and privacy protection requirements of private deployment. This solution not only complies with Xinchuang (Information Technology Application Innovation) standards but also satisfies computing power demands. These technological breakthroughs have enabled Xinchuang initiatives to move beyond the transformation of non-core business systems, achieving “genuine replacement and actual usage” in core clinical diagnosis and treatment systems. Furthermore, several benchmark hospitals have successively completed various stages of Xinchuang substitution for their core systems, setting a demonstrative example for medical institutions across China.

In 2024, the “Data Element × Healthcare” initiative also made progress. In January of this year, the Three-Year Action Plan for “Data Element ×” (2024–2026) was officially released, setting forth the goal of implementing the “Data Element ×” initiative across 12 key sectors, including healthcare. The plan highlights the strategy of “promoting application through competitions,” aiming to pilot and gradually mature essential components—such as co-governance mechanisms, management rules, hierarchical classification, technical standards, and professional teams—through these competitions, thereby establishing the basic framework of a public service system for “Data Element × Healthcare.” Numerous outstanding projects have emerged from these competitions, providing valuable references for the further development of “Data Element × Healthcare.”

Take Yidu Cloud, a subsidiary of Yidu Tech, as an example. It achieved remarkable results in the “Data Element ×” Competition held in multiple regions: its project, the “Chaoyang District Medical and Health Big Data Platform,” jointly developed with the Health Commission of Chaoyang District, Beijing, and its collaborative project with Xiangya Hospital of Central South University, the “Open Platform for Smart Medical Research Capabilities Based on Data Elements,” won the Second Prize in the Medical and Health Track in the Beijing and Hunan divisional competitions, respectively.

Moreover, by year-end, the first batch of compliant and tradable data products from medical institutions across China was listed, culminating in the first data transaction conducted by a public hospital in 2024. This achievement set a new benchmark for the compliant application of healthcare data nationwide and laid the foundation for breakthroughs in the “Data Element × Healthcare” sector in the following year.

Digital therapeutics, which garnered significant attention in the past two years, have cooled down considerably in recent times. However, from the perspective of Gartner’s Hype Cycle for Emerging Technologies, the deflation of this “bubble” may actually facilitate deeper industry consolidation and accumulation, given that digital therapeutics is an emerging field integrating various digital technologies and sectors. The key lies in identifying appropriate scenarios for innovative applications, where the advantages of digital therapeutics can be fully demonstrated, thereby delivering genuine value to both physicians and patients.

JD Health, an internet healthcare giant, emphasized the close integration of its dermatology digital therapeutic—approved last year—with online medical scenarios. By intelligently processing and dynamically tracking dermatological examination images, it assists physicians in accurately assessing patients’ conditions and promptly adjusting treatment plans. Leveraging the capabilities of the Jingyi Qianxun large language model, it has achieved a diagnostic accuracy rate of 95% for nearly 100 skin diseases and a treatment plan consistency rate exceeding 80%.

The above is an excerpt of the main content of the report. Below are the outstanding innovation cases of the year. Scan the QR code on the poster to access the full report.

Report Table of Contents

CHAPTER 1. Changes in the Digital Healthcare Industry in 2024

1.1. Definition and Development of Digital Health as Studied in the White Paper

1.2. Primary Market Capital Data

1.3. NEEQ Listing, IPO, and M&A

1.4. Policy Data: Digital Healthcare Receives High-Level Attention, with Policies Driving Integration Across All Aspects

1.5. Approval Data: AI Medical Devices See Significant Growth, While Digital Therapeutics Maintain Steady Growth Rate

CHAPTER 2. Six Key Questions on Digital Health in 2024

2.1. What practical changes have the successive deployments of large language models brought to healthcare?

2.2. As Imaging AI Matures, What New Breakthroughs Are Still Possible?

2.3. The Centralized Implementation of Medical IT Innovation: Can It Drive New Growth in Healthcare Informatics?

2.4. Will MXR Spark a Revolutionary Innovation in Healthcare Scenarios?

2.5. Did Data Elements × Medical Healthcare Achieve a Breakthrough in 2024?

2.6. Can Digital Therapeutics Reverse the Trend by Delivering Value in Application Scenarios?

CHAPTER 3. Interpretation of Digital Healthcare Innovation Cases in 2024

3.1. Tencent Health—Leading the Implementation of Large Medical Models

3.2. Yidu Tech—“AI Middle Platform” Empowers Hospitals to Enter the Era of Large Language Models

3.3. GE Healthcare—Building an “Accelerated Runway” for Digital Innovation in China’s Medical Equipment Industry

3.4. JD Health—Enhancing Large Model Scenario Expansion Based on Actual Needs in Real-World Settings

3.5. Shanmu: The Ideal Form of the “Family Doctor” Gateway in the AGI Era