2024 Annual Innovation White Paper on Medical Devices and Supply Chain: Accelerated Industry Consolidation and Three Strategic Pathways to Breakthrough

In 2024, the medical device industry faced widespread pressure, yet it also harbored new development opportunities. This year marked a critical period of market validation for the sector. Amidst delays in tendering and procurement of medical equipment, the normalization of volume-based procurement (VBP), and macroeconomic challenges, industry growth encountered significant headwinds. VBInsight has observed three notable shifts within the industry:First, the drivers of industry growth are undergoing a transition. Profit margins for mature products are being squeezed, necessitating more refined operational management by enterprises. Meanwhile, market penetration of differentiated innovative products is rising, as companies actively seek entry into high-growth segments. Enterprises offering multi-tiered, comprehensive solutions are better positioned to adapt to market changes.Second, the trend of industry consolidation is intensifying. In 2024, innovative medical device companies faced heightened survival pressures, prompting many to explore strategic transformations. The pace of mergers and acquisitions within the sector has also accelerated.Third, from a payment perspective, cost containment within medical insurance has become an overarching trend. The normalized implementation of centralized procurement has emerged as a critical factor determining corporate survival.

To gain a deeper understanding of the development trajectory of China’s medical device industry, this report reviews the sector’s progress in 2024 and outlines trends for 2025 from multiple perspectives, including the macro market environment, access reforms, segment evolution, investment and financing trends, and global expansion efforts. Overall, the innovative medical device sector represents a long-term, high-potential arena; only with sustained patience can companies reap the fruits of growth.

In 2024, the overall growth of innovative medical devices in China faced pressure, but long-term growth momentum remains robust.China’s innovative medical device industry is facing multiple challenges, including anti-corruption campaigns in the healthcare sector, the expansion of centralized procurement, delays in bidding processes, and cost-containment measures under medical insurance schemes, all of which have dampened overall growth momentum. However, in the long run, China’s medical device industry continues to be driven by three core forces. First, the accelerating trend of population aging has led to growing demand for long-term medical care. Second, state investment in the healthcare sector continues to increase, resulting in a steady rise in the number of healthcare institutions. Finally, technological innovation has injected new vitality into industry development. As a manifestation of new quality productive forces in the healthcare sector, medical science and technology innovation is not only a key factor driving economic development but also an important engine promoting high-quality industry growth. Therefore, although industry growth may experience short-term fluctuations, these three drivers will sustain strong growth potential for the medical device industry in the long term.

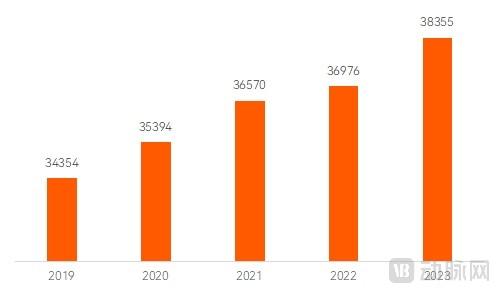

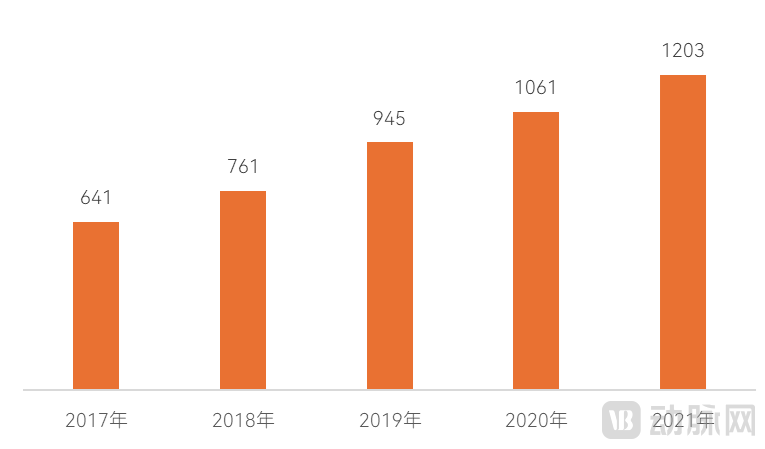

Number of Hospitals in China (2019–2023) (Unit: Number of Hospitals)

Data Source: 2019–2023 Statistical Bulletin on Health and Medical Care

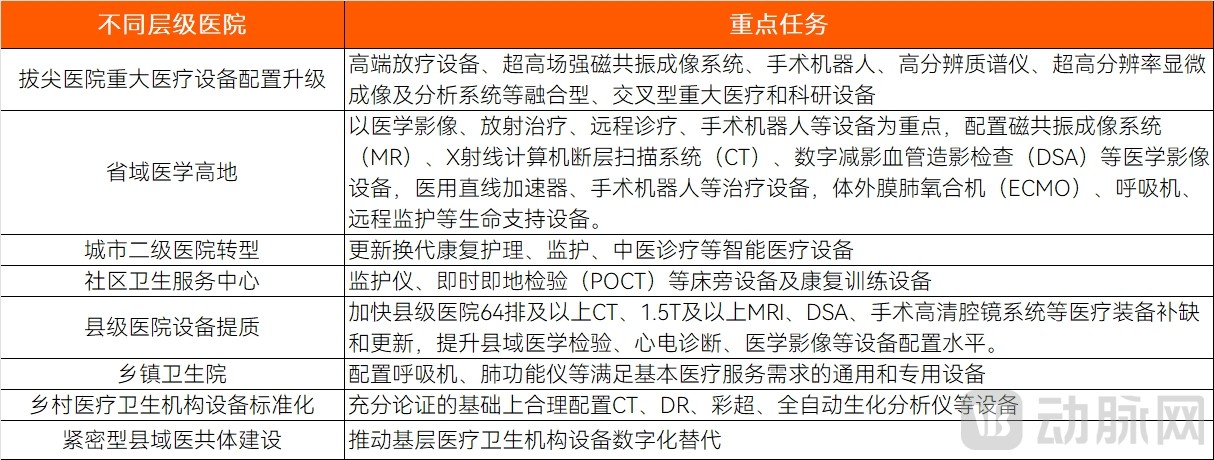

The upgrade and replacement of medical equipment are expected to drive growth in 2025, with the CNY 10 trillion debt resolution policy providing financial support.Policies introduced at the end of 2024 to support local governments in mitigating debt risks, by increasing debt quotas to address implicit debts, will free up more fiscal resources for localities to promote development and safeguard public welfare. This is expected to lead to a market recovery in 2025, a trend already reflected in the bidding data from the fourth quarter of 2024. Statistical data from Zhongcheng Medical Devices shows that since November, there has been a significant increase in the value of equipment renewal bidding projects.

Key Work Plan for Medical Device Iteration

Data Source: Work Plan of Anhui Province for Promoting the Iterative Upgrading of Equipment in the Health Sector

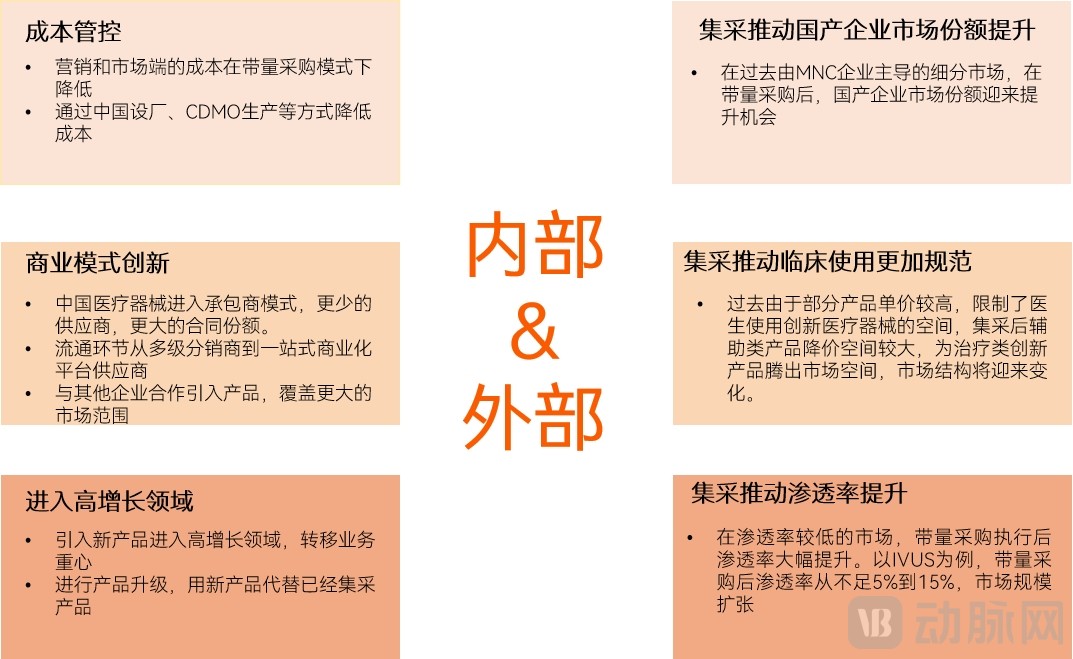

Cost Control + Entry into High-Growth Tracks: A Strategic Combination to Help Enterprises Mitigate the Impact of Volume-Based ProcurementReductionMitigating the Impact of Volume-Based Procurement on Performance Requires Two Key Strategic Initiatives. Internally, companies must reduce costs and enhance efficiency, with core measures including cost control and entry into high-growth sectors. Externally, they need to proactively respond to volume-based procurement by submitting precise bids and leveraging grouping advantages, thereby seizing opportunities such as increased market penetration, shifts in the clinical product mix, and expanded market share for domestic enterprises.

Key Strategies for Global Companies to Navigate the Impact of Volume-Based Procurement

Source: VBInsight

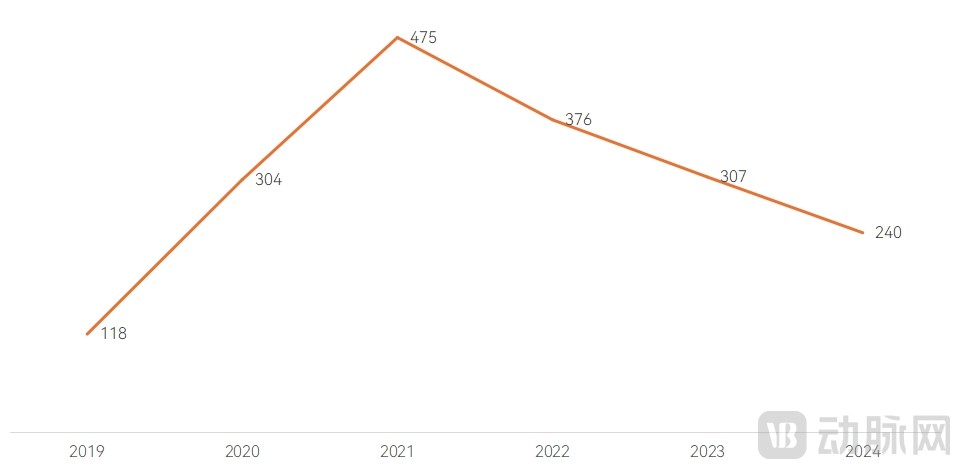

Investment and Financing Data: Investment and financing have entered a downward phase, while M&A data shows growth.In 2024, China’s healthcare investment sector maintained a cautious stance, with a decline in investment activities. In 2023, there were 307 financing deals in the innovative medical device sector; however, by October 2024, the number of publicly disclosed financing deals for innovative medical devices had dropped to 240, indicating that the overall financing environment has regressed to levels seen four years ago. The continued decline in financing for innovative medical devices is attributable to multiple factors, including obstacles in exit channels, sluggish valuations of medical device companies in the secondary market, and increased difficulties in fundraising.

2019–2024 Number of Private Equity Deals in Innovative Medical Devices (Unit: Cases)

Data Source: VBInsight, Haoyue Capital

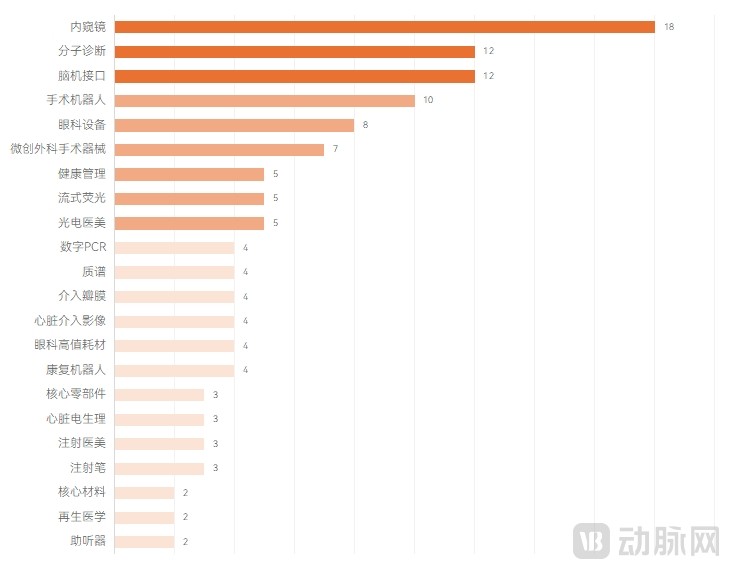

From an industry perspective, innovative medical devices are distributed across four major categories: medical equipment, high-value consumables, in vitro diagnostics, and the upstream supply chain.Among medical devices, endoscopes, surgical robots, brain-computer interfaces, and optoelectronic aesthetic medicine devices ranked high in the number of financing events. In the high-value consumables sector, cardiovascular, ophthalmology, aesthetic medicine, and minimally invasive surgery led in financing activity. Within in vitro diagnostics (IVD), frequent financing occurred in areas such as molecular diagnostic platforms (including digital PCR, early cancer screening, and sequencing services), gas-liquid phase and mass spectrometry instruments, metabolomics, proteomics, spatial omics clinical application developers and service providers, as well as upstream supply chains and flow fluorescence applications in immunology. Furthermore, the upstream supply chain segment has risen prominently, with several financing rounds secured for core components of imaging equipment, CDMOs, and key upstream materials. Notably, the surge in GLP-1 demand has driven heightened investment interest in upstream injection pen manufacturers.

Number of Financing Deals in Innovative Healthcare Subsectors in 2024 (Unit: Count)

Data Source: VBInsight

Recently, M&A activities in the medical device industry have shown an upward trend.The factors driving increased attention to mergers and acquisitions (M&A) in China’s medical device sector in 2024 primarily include: technological innovation, expanding market demand, accelerated industry consolidation, and supportive policy environments. In 2024, the secondary market for medical devices in China witnessed multiple M&A and consolidation transactions.including Mindray Medical's acquisition of Huitai Medical, and Sino Biopharmaceutical's acquisition of controlling interest in Haoubo, a company listed on the STAR Market.There are over 170 listed medical device companies in China, including more than 80 in vitro diagnostics (IVD) enterprises, indicating substantial room for mergers and acquisitions (M&A) and consolidation in the secondary market. Policymakers have repeatedly emphasized the importance of M&A and restructuring, introducing relevant policies to deepen market-oriented reforms in this area for listed companies. It is foreseeable that the domestic medical device secondary market will optimize resource allocation and stimulate market vitality through M&A and restructuring in the future.

Innovative Approval Data: Innovation Highlights Industry Resilience。Amid mounting pressure on industry development, innovation remains the most effective strategy to counteract intense market competition. In 2024, changes were also observed in the approval process for innovative medical devices in China. According to the latest data from the VCBeat Research Institute Data Center, as of December 16, 2024, a total of 66 products had successfully entered the national-level approval channel for innovative medical devices. In contrast, the total number of products that entered the national priority approval channel for medical devices in 2023 was 67.

Based on data from the past two years, the number of products from Chinese enterprises entering the National Medical Device Priority Review and Approval Channel has not shown significant growth. VBInsight analysis suggests that this phenomenon may stem from two factors: First, facing market pressures, domestic medical device companies have reduced their investment in innovative R&D; second, after several years of rapid development, many companies have completed product preparation and pipeline layout, and are now shifting their focus to achieving large-scale commercialization of their products. This indicates that, although the pace of innovation has slowed, companies are gradually transitioning from the R&D phase to the market promotion and application phase.

The medical device industry is characterized by its diverse market segments, each with its unique development trajectory and underlying logic. This chapter delves into the latest developments and future trends in the major subsectors of innovative medical devices in 2024, highlighting significant changes in technological innovation, market demand, and policy orientation.

We will conduct a detailed segmentation of the innovative medical device industry, primarily dividing it into four core sectors: high-value consumables, medical equipment, in vitro diagnostics (IVD), and upstream supply chains and core components. Subsequently, we will provide an in-depth analysis of the major changes occurring within each sub-sector of these segments.

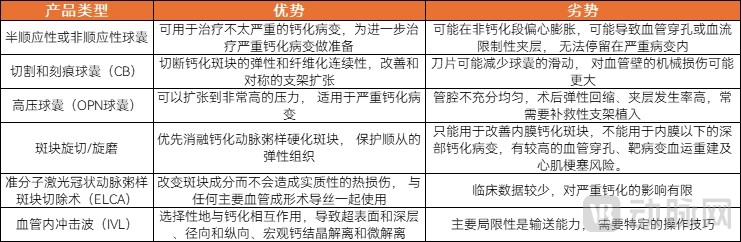

Centralized procurement for coronary interventions boosts the penetration rates of drug-coated balloons and intravascular lithotripsy systems.Changes in the coronary intervention industry are primarily reflected in two aspects: continuous improvement in penetration rates and increased utilization of innovative medical devices. Although the prices of coronary stents have declined rapidly following volume-based procurement (VBP), their usage has increased significantly, with a pronounced effect of domestic substitution. Furthermore, VBP has also driven higher penetration rates for innovative products such as drug-coated balloons (DCBs) and coronary intravascular lithotripsy (IVL) systems. For instance, the penetration rate of DCBs rose from less than 5% in 2020 to 18% in 2023. Since vascular preparation is required prior to DCB placement, the use of drug-coated balloons will drive growth in vascular preparation products.

Shockwave balloon catheters demonstrate favorable efficacy and enhanced safety in the management of moderate-to-severe calcified lesions.It is currently the only device capable of effectively treating deep vascular calcification. By precisely delivering acoustic pressure waves to the calcified lesions, it fractures or loosens intravascular calcified plaques, restores vascular elasticity, maintains unobstructed blood flow, and achieves coronary vessel remodeling. Compared with traditional calcification management techniques, the shockwave balloon catheter is not only effective for superficial calcification but also safely, efficiently, and precisely disrupts both superficial and deep calcium deposits, while minimizing damage to soft tissue and improving vascular compliance, thereby preparing the vessel for subsequent balloon angioplasty and stent implantation. Consequently, shockwave balloons have become a focal point of innovation in the field of percutaneous coronary intervention (PCI).

Characteristics of Treatment Modalities for Coronary Artery Calcification

Data source: Chinese Expert Consensus on the Diagnosis and Treatment of Coronary Artery Calcification (2021 Edition)

Shockwave Balloon Active Intervention is a high-barrier product, and domestic companies have achieved breakthroughs.Coronary Intravascular Lithotripsy Treatment System is classified as an active interventional medical device. Although passive interventional technologies have been developed for many years and reached a high level of maturity, domestic technical accumulation in active interventional products remains relatively weak compared to foreign counterparts, particularly concerning key technologies, components, and critical bottlenecks. Despite these high technical barriers, some Chinese enterprises have achieved breakthroughs. Intravascular lithotripsy devices from companies such as Saihe Medical, Blue Sail Medical, and Lepu Medical have been approved for market launch in China. Among them, Saihe Medical’s Coronary Intravascular Lithotripsy Treatment System delivers pulsed driving electrical energy to the lithotripsy catheter, enabling intermittent, 360-degree circumferential output of divergent, low-intensity shockwave energy. This mechanism fractures calcified plaques and improves vascular compliance. The system features an extremely short learning curve and is simple, safe, and easy to use.

Heart Failure and Cardiac Assist Devices: Inclusion of Artificial Hearts in National Health Insurance Brings Significant Benefits, with Over 1,000 Domestic ImplantationsAmong the various implantable artificial hearts marketed in China, based on the overall status of long-term LVAD implantation in China announced by Academician Hu Shengshou from Fuwai Hospital at the 2024 Chinese Biomedical Engineering Conference and Innovative Medical Summit, as well as the LVAD implantation data released in Fuwai Hospital’s 2023 Annual Development Summary Report, a total of 1,140 LVAD implantations using four models were performed in Chinese hospitals from June 2017 to August 2024. Core Medical’s left ventricular assist device, Corheart® 6, ranked first with 385 implantations. From January to August 2024, approximately 479 LVAD implantations (estimated) using four models were completed in Chinese hospitals, among which Corheart® 6 accounted for the highest volume with approximately 208 cases, representing about 43% of the total implantations.

Fully Maglev Integrated Biventricular Assist System Enters the Green Channel for Innovative Medical Devices.In clinical practice, left ventricular assist devices (LVADs) are not the ultimate or most comprehensive solution for end-stage heart failure. Up to 30% of patients with end-stage heart failure present with right-sided or biventricular failure, requiring right ventricular or biventricular mechanical circulatory support. Furthermore, the incidence of right heart failure following isolated LVAD implantation is as high as 30%, which significantly reduces long-term survival rates in LVAD recipients. While patients with biventricular failure require biventricular assistance, existing total artificial hearts (TAHs) are associated with high complication rates, large pump volumes, and low survival rates, failing to effectively address the challenges of biventricular failure.

Currently, no biventricular assist devices have been approved for market entry worldwide. Notably, in 2024, Core Medical’s fully magnetically levitated integrated biventricular assist system, DuoCor®, was admitted into the Green Channel for Innovative Medical Devices. It features the following key innovations: a single-system approach enabling integrated coordinated control and left-right ventricular balance; an integrated design with lightweight external equipment to improve patients’ quality of life; and a globally first-of-its-kind integrated biventricular design that further reduces weight and volume while better accommodating right-sided hemodynamics and physiological anatomy. DuoCor® holds promise for bringing new hope to patients with end-stage biventricular heart failure.

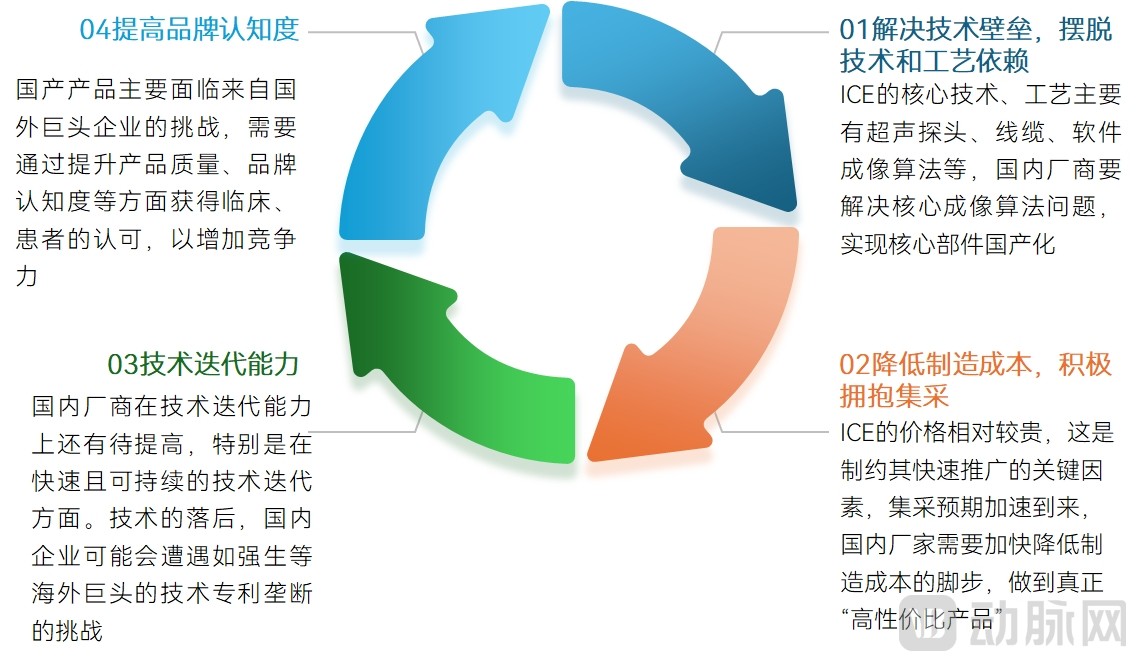

In China, the ICE market is expanding rapidly, characterized by its swift growth rate and broad range of applications.Intracardiac echocardiography (ICE) has been widely adopted to guide interventional therapies for structural heart disease and arrhythmias, as well as to monitor intraoperative complications. Its clinical applications include catheter ablation for atrial fibrillation, transseptal puncture, closure of atrial septal defects, left atrial appendage occlusion, and mitral valve repair. Currently, ICE is primarily used in the field of electrophysiology in China, with atrial fibrillation treatment being the dominant indication, followed by left atrial appendage occlusion. Compared with the United States, where ICE is utilized in over 90% of electrophysiology procedures, the penetration rate of ICE in China is only one-tenth that of developed countries, highlighting the significant growth potential of the Chinese ICE market.

According to research, by 2030, the total number of procedures in China for common ICE-guided interventions—including left atrial appendage closure (LAAC), patent foramen ovale (PFO) closure, and atrial septal defect/ventricular septal defect (ASD/VSD) closure—is projected to reach 700,000 cases. Furthermore, the volume of atrial fibrillation ablation procedures is expected to exceed 1 million cases, indicating substantial growth potential for the Chinese ICE market. In the future, electrophysiology procedures will remain the primary application area for ICE. Meanwhile, as ICE technology continues to advance, its importance and benefits in the treatment of structural heart disease will become increasingly prominent, leading to a gradual increase in its adoption rate in this field and further driving the sustained expansion of the ICE market.

Four Key Capabilities That ICE Enterprises Need to Strengthen

Data Source: VBInsight

Domestic innovative peripheral interventional products are being approved in rapid succession, with devices addressing complex lesions becoming a key strategic focus.Competition in the peripheral intervention market is relatively moderate, characterized by a wide variety of product types. Currently, domestic companies are in a critical “ramp-up” phase focused on refining and completing their product portfolios. In areas such as balloons, iliac vein stents, drug-coated balloons (DCBs), scoring balloons, and access devices, domestic companies have basically achieved comprehensive coverage of their product lines. As domestic companies deepen their involvement in the field of peripheral intervention, products designed to address complex peripheral lesions have become the focus of their next-stage strategic layout. Looking ahead, aspiration systems, intravascular lithotripsy (IVL) systems, and sirolimus-eluting DCBs will be key pipeline priorities for domestic companies in the coming years.

Among these, patients with lower extremity vascular calcification constitute the majority of those with peripheral vascular calcification. Peripheral calcified lesions are characterized by greater lesion length and higher degrees of stenosis. Additionally, the presence of non-stented segments in the lower extremity arteries leads to increased subsequent use of drug-coated balloons. Compared with coronary artery calcification, lower extremity vascular calcification features thicker calcific layers and a longer duration of calcified lesions.

Therefore, peripheral intravascular lithotripsy (IVL) balloon therapy is particularly suitable for the treatment of calcified lesions in lower extremity vessels. The primary demands for IVL in the peripheral vascular field focus on its ability to successfully cross occluded segments, achieve greater luminal gain, and reduce the need for bailout stenting. As IVL technology is still in its early stages within the peripheral domain, with current annual procedure volumes numbering in the thousands, significant growth in procedure volume is anticipated as more products receive regulatory approval.

Leading domestic IVL companies, such as Saihe Medical, have obtained approval for their peripheral intravascular lithotripsy systems. This system delivers pulsed electrical energy to emit divergent, low-intensity shockwave energy outward in a 360-degree circumferential and intermittent manner, without causing damage to the luminal intima or normal vascular tissue. It features excellent human-machine interaction, pressure resistance, and procedural efficiency.

Under the influence of centralized procurement policies, competition in the peripheral intervention market has intensified, and companies with comprehensive product portfolios or innovative products are more likely to gain a competitive edge.Against the backdrop of normalized volume-based procurement (VBP), the market size for single-product categories has been significantly compressed, ushering in a period of industry consolidation. A comprehensive product portfolio and integrated solutions are particularly critical for market expansion. As widely recognized within the industry, under the impact of VBP, only enterprises with complete product lines can effectively penetrate the market and lead shifts in the competitive landscape. Furthermore, amid normalized VBP, competition among homogeneous products has intensified, leading to continuous erosion of profit margins. However, the price reduction of ancillary products has created greater payment capacity for the promotion of innovative products. In this market environment, breakthrough and differentiated innovative products are more likely to gain a competitive edge.

For instance, Zhongtian Medical’s rapid development in the field of peripheral interventions is primarily attributed to its innovative products and differentiated advantages. Its SWAM technology, an innovative separator-assisted peripheral thrombectomy system, enables more efficient clot removal; its fully controllable ciliated coils for peripheral embolization achieve more precise and controllable embolic effects; and its carotid artery stent features an innovative single-layer microporous hybrid braided design, making it the first domestically produced product approved through the “Green Channel.”

Domestic neurointerventional companies are entering a period of profitability, and capturing market share in large central hospitals has become the key to their development.In 2024, several industry leaders achieved breakthroughs in commercialization, officially entering the profitability stage. To sustain profitability, companies must drive revenue growth through innovative and differentiated products, while enhancing profit margins by controlling costs and improving operational efficiency. Additionally, seizing opportunities arising from centralized volume-based procurement (VBP) is crucial for achieving leapfrog growth in revenue. For instance, Zhongtian Medical reached break-even in 2024 and completed a new round of financing, primarily attributable to its strong comprehensive capabilities. Its AIS one-stop innovative solution has cumulatively served over 50,000 patients in China, and its Zhongtian Tianxun® distal access catheter won the bid in Group A of the Beijing-Tianjin-Hebei “3+N” centralized VBP program.

Ophthalmic Equipment Market Grows Against the Trend, with Significantly Improved Recognition of Domestically Produced Products.Despite the impact of delays in domestic tendering and bidding processes in 2024, which led to a reduction in procurement activities by public hospitals, terminal demand in the ophthalmology sector has continued to grow steadily. This growth is driven by three key factors: ① The increase in the number of specialized ophthalmology outpatient clinics, coupled with strong demand from private hospitals, has continuously upgraded the need for diagnostic equipment in ophthalmology outpatient settings. ② Demand for ophthalmic equipment is multi-tiered, with continuous product upgrades sustaining market growth. This includes the evolution from fundus cameras to Optical Coherence Tomography (OCT) systems, from conventional fundus cameras to ultra-widefield confocal scanning laser ophthalmoscopes, and from second- and third-generation OCT products to swept-source OCT. ③ The substitution of high-end imported ophthalmic equipment with domestically produced alternatives.

In the past, the high technical barriers associated with high-end ophthalmic equipment resulted in a market dominated by a few imported brands. However, thanks to the relentless efforts of domestic enterprises in accumulating technological expertise and achieving breakthroughs, end-users’ perceptions of Chinese-made high-end ophthalmic equipment are shifting positively. This has led to increased market recognition for domestic brands, further driving market prosperity.

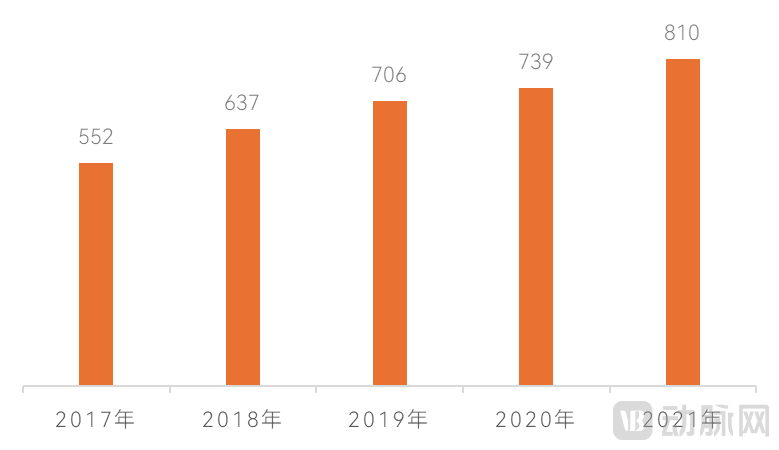

Number of Domestic Ophthalmic Specialty Hospitals in China, 2017–2021 (Unit: Number of Hospitals)

Data Source: China Health Statistical Yearbook

Domestic OCT Brands Establish Competitive Advantages Through Technological Iteration.In the OCT sector, the market share of domestic enterprises has surpassed that of imported brands. The key to this overtaking lies in the rapid iteration of OCT technology, which has provided Chinese companies with an opportunity to leapfrog their competitors. The OCT technological roadmap has consistently undergone high-speed updates and generational shifts. Meanwhile, imported brands face higher costs for technological transformation and slower transition speeds, creating opportunities for domestic enterprises adopting the latest technological pathways to surpass them. Consequently, it has become increasingly feasible for domestically produced OCT products utilizing swept-source OCT (SS-OCT) technology to outperform imported counterparts in terms of performance.

For instance, Intalight’s Saiwei Ruyi Whole-Eye OCT has ushered in a new era of “whole-eye OCT.” Nearly 500 units have been deployed in ophthalmic hospitals across China, with over 120 installed in national or provincial benchmark hospitals. Moreover, it is already in use at more than 30 top-tier overseas hospitals and eye care institutions in the United States, Europe, South America, and the Asia-Pacific region, achieving peak international adoption upon market entry. The Ruyi 150 model offers a single-scan coverage of up to 150°, pushing the boundaries of OCT angiography (OCTA) imaging range. Launched in 2024, the Ruyi Whole-Eye Biometer incorporates proprietary second-generation visualization swept-source biometry technology, increasing axial length detection rates from 94% to over 99%. It enables wide-field fundus imaging up to 9 mm and full corneal topography, and can be integrated with anterior segment OCT.

Domestic Companies Achieve Breakthrough in Fundus Camera Market Share.As capital market attention and investment in the ophthalmic equipment sector continue to increase, the number of participants in China’s high-end ophthalmic equipment market has grown significantly, accompanied by a substantial rise in the number of certified fundus cameras. The fundus camera segment particularly tests companies’ long-term R&D capabilities. The annual newly added procurement volume for ultra-widefield laser cameras (including angiography and photography models) is approximately 600 units, with a growth rate maintained between 15% and 20%. Ultra-widefield laser technology is gradually becoming the mainstream technology for fundus cameras, and it is projected that by 2028, ultra-widefield laser fundus cameras will completely replace traditional products.

According to publicly accessible bid-winning data from Chinese public hospitals, in 2023, the Optos Daytona (P200T) model accounted for the highest proportion of total sales revenue, reaching 38%; the Zeiss CLARUS 500 model ranked second, with a sales revenue market share of 26.8%, and MicroClear Medical ranked third, with a sales revenue market share of 24.9%. This ranking was updated in 2024. According to statistics from Bidi Bidding Network, among brands with higher market shares in fundus camera sales revenue from January to June 2024, MicroClear Medical, as the top-ranked Chinese-made brand, placed second overall. Its fundus laser cameras have been installed in nearly 500 hospitals, achieving coverage of key ophthalmology hospitals across China with multiple installations completed. In some hospitals, its winning bid prices exceeded those of similar imported products, and its products have already reached more than 40 countries and regions worldwide.

Domestic ophthalmic equipment is advancing from replacing imported products to leading industry development.22024 witnessed the breakthrough launch of multiple high-end domestically produced ophthalmic devices, which broke through the limitations of traditional products. For instance, MicroClear Medical’s SKY Whole-Eye Imaging Platform integrates technologies such as confocal laser scanning and SS-OCT. It combines fundus planar imaging—including ultra-widefield laser color photography, angiography, and autofluorescence—with ultra-wide and ultra-deep tomographic imaging of both the anterior and posterior segments. The platform enables real-time, multi-modal display on a single screen and features intelligent annotation for assisted analysis as well as stepless optical zoom. This one-stop examination approach enhances diagnostic efficiency and improves the experience for both physicians and patients, making diagnosis more efficient, comprehensive, and precise.

In 2024, the domestic endoscopy market was impacted by the rectification of the healthcare industry and medical equipment renewal programs, leading to continued delays in tendering and procurement activities.In the rigid endoscopy sector, image quality and product functionality are the core drivers of market competition. In terms of market landscape, foreign companies dominate the domestic market by leveraging their first-mover advantages and superior product performance. Among them, Karl Storz and Olympus occupy the first tier, while Stryker and Richard Wolf follow closely in the second tier. Meanwhile, the market share of Chinese enterprises has grown significantly, with key competitors including Mindray Medical, OptoMedic, Sonoscape, Shenda Endoscope, Tiansong Medical, New Optical Dimension, Kangji Medical, and Tuoge Medical. Notably, in the field of fluorescence endoscopy, the installed base of domestically produced equipment has exceeded half of the market. In the flexible endoscopy market, maneuverability and image quality have become critical factors for competition. Currently, foreign companies still hold a substantial market share, while the market penetration of Chinese enterprises remains relatively low. The main players in the domestic flexible endoscopy segment include Aohua Endoscopy and Sonoscape, which are poised to enhance the competitiveness of Chinese-made flexible endoscopes in the future.

Providing end-to-end solutions in the field of endoscopy has become a core competency.For instance, Hisense Medical provides full-chain solutions in the field of endoscopy, addressing core pain points commonly associated with domestically produced endoscopes, such as product stability and performance degradation after prolonged use. The high performance and stability of its endoscopes have reached an industry-leading level. Its intelligent navigation 4K fluorescence endoscopy system is equipped with an intelligent navigation system, an integrated smart teaching system, and an AI algorithm optimization system. It offers a comprehensive workflow solution covering preoperative planning, intraoperative precise navigation, live surgical demonstrations, remote surgical guidance, and postoperative outcome evaluation. This significantly improves surgical success rates and meets the needs of clinical diagnosis and treatment, academic research, and medical education.

The disposable endoscope market continues to grow, with strong overseas performance.With the rapid advancement of CMOS image sensor chip technology, particularly the achievement of self-sufficiency and controllability in domestically produced chips, the endoscopy industry has been presented with significant opportunities for robust growth. Single-use electronic endoscopes have emerged as an optimal strategic choice for Chinese medical endoscope manufacturers to catch up with and surpass leading global enterprises, thereby achieving leapfrog development. There is substantial demand for these devices in clinical departments with critical infection prevention requirements, such as pulmonology, gastroenterology, and gynecology. Furthermore, China’s mature endoscopy supply chain establishes a strong industrial foundation for the global expansion of single-use endoscopes. Currently, China’s export volume of single-use endoscopes stands at 250,000–300,000 units, indicating considerable room for further growth. In the first three quarters of 2024, China’s endoscope exports experienced significant growth, underscoring the vast potential of the overseas market for Chinese endoscope manufacturers.

Among the numerous disposable endoscope manufacturers in China, key competitive advantages that enable companies to stand out in a fiercely competitive market include large-scale mass production capabilities, comprehensive product portfolios across all clinical departments, superior image quality, advanced image processing technologies, and high device operability. Overall, technological prowess and large-scale commercialization capabilities are the critical success factors for disposable endoscope enterprises.

For instance, RayPai Medical’s comprehensive global layout across multiple departments and product lines, coupled with innovative technologies in medical optics, image processing, software, and algorithms, has positioned it at the forefront of competition. Its advanced medical imaging algorithms enable next-generation host systems to deliver ultra-high-definition imagery, while intelligent computer-aided diagnosis and treatment technologies enhance lesion detection rates and improve physicians’ workflow efficiency. Currently, the company’s single-use endoscope products—including pyeloscopes, cystoscopes, cholangioscopes, hysteroscopes, and gastrointestinal endoscopes—have obtained more than 100 approvals from regulatory bodies such as China’s NMPA, the EU’s CE, and the US FDA. Its products and services reach over 50 countries and regions across North America, Europe, the Middle East, Southeast Asia, South America, and Africa, serving more than 2,600 hospitals worldwide.

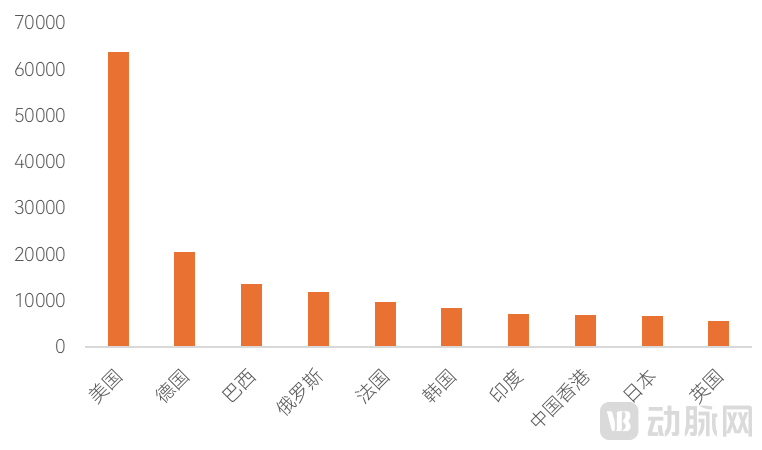

Top 10 Countries for China's Endoscope Exports and Export Values from January to October 2024 (Unit: 10,000 Yuan)

Data Source: China Customs

Procurement demand at public general hospitals remains weak, while rehabilitation specialty hospitals and private hospitals exhibit stronger growth momentum.In the rehabilitation equipment market, public general hospitals, due to their large numbers, continue to dominate the majority of the market. However, constrained by limited bed capacity and a generally low level of specialization in rehabilitation care, coupled with the overall slowdown in domestic medical equipment tendering processes in 2024, demand for rehabilitation equipment in public general hospitals exhibited weakness in 2024. Meanwhile, specialized rehabilitation hospitals and private hospitals have demonstrated strong growth momentum for intelligent rehabilitation equipment. Specialized rehabilitation hospitals account for substantial procurement volumes, while private rehabilitation hospitals, as an emerging market segment, are experiencing rapid growth.

Number of Rehabilitation Specialty Hospitals in China, 2019–2021 (Unit: Facilities)

Data Source: China Health Statistics Yearbook

The rehabilitation market is upgrading toward specialization.As China’s rehabilitation equipment industry continues to advance, hospitals have developed a deeper understanding of rehabilitation devices, driving demand toward greater specialization. This trend is reflected not only in the need for rehabilitation equipment but also in the ongoing subspecialization of rehabilitation medicine itself, which now encompasses multiple specialized fields such as cognitive rehabilitation, neurological rehabilitation, orthopedic rehabilitation, cardiopulmonary rehabilitation, and cardiac rehabilitation.

At the product level, domestic rehabilitation medical devices are moving toward specialization and intelligence. The intelligence level of rehabilitation robots is improving. Currently, rehabilitation robots on the market are mainly fixed or semi-fixed, which have certain limitations in autonomy and flexibility, and cannot provide personalized feedback based on the specific conditions of patients. Exoskeleton rehabilitation robots, as tools to assist patients in standing and walking, have functions such as gait correction, enhanced assistance, and motion compensation.

Exoskeleton robots have been developing in China for some time and are gradually transitioning from automation to intelligence. Intelligent exoskeleton robots need to accurately identify and predict human movement intentions, assist patients in walking through precise mechanical feedback, and improve interactivity and engagement, enabling personalized, immersive training that enhances patient compliance. In addition to technological iterations, many companies have diversified their product portfolios, expanding from lower limbs to ankles, upper limbs, hands, and bedside applications, while also extending their target demographics to include children.

For instance, AngelTech, which focuses on neurological rehabilitation, addresses motor dysfunction in hemiplegic patients by developing “intelligent, active, personalized, systematic, and precise” smart rehabilitation medical devices through an innovative AI-plus-rehabilitation approach. These devices meet the intelligent rehabilitation training needs of joints such as the shoulder, elbow, wrist, hip, knee, ankle, and hand, gradually forming an intelligent solution centered on neurological rehabilitation, featuring musculoskeletal rehabilitation, and extending to early bedside rehabilitation and geriatric rehabilitation. The clinical application of these products not only provides patients with more effective rehabilitation treatment but also alleviates the repetitive and strenuous physical workload of rehabilitation therapists, thereby effectively improving departmental operational efficiency.

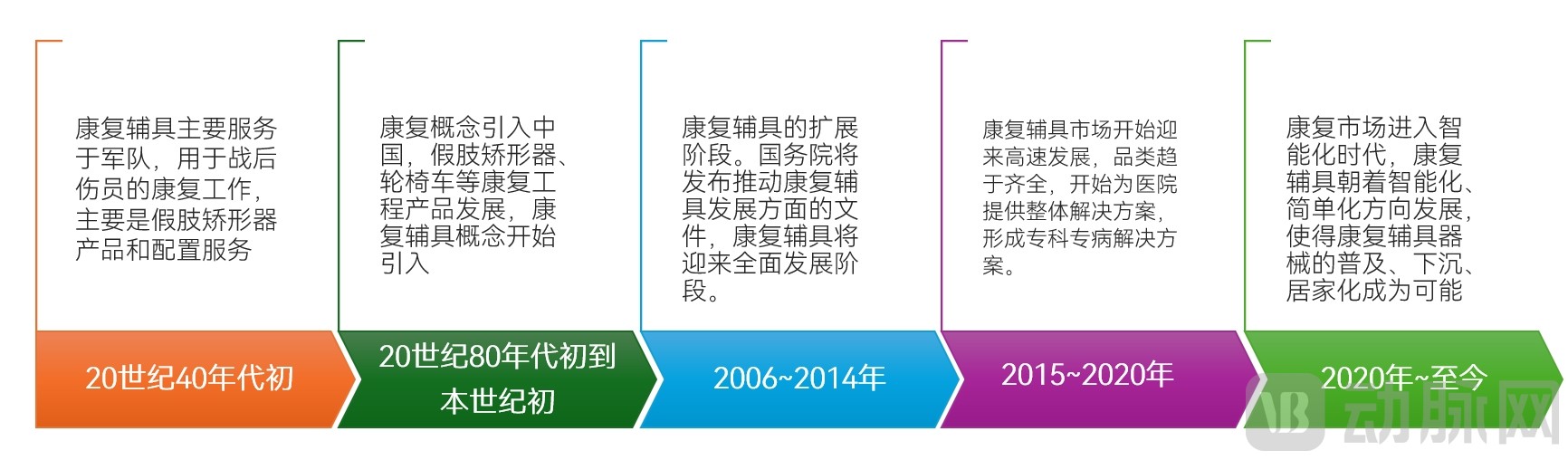

Development History of the Domestic Rehabilitation Assistive Devices Market

Data Source: VBInsight

Treatment and life support equipment includes anesthesia machines, cardiopulmonary resuscitation devices, external defibrillators, ventilators, patient monitors, ECMO systems, and other products. The localization process for most of these products has been relatively rapid, with the proportion of domestically produced equipment in tender procurements for cardiopulmonary resuscitation devices, external defibrillators, ventilators, anesthesia machines, and pulse oximeters exceeding 50%. However, certain high-end medical devices for extracorporeal circulation still rely on imports, including ECMO systems and organ perfusion systems.

Taking the organ perfusion system as an example, such systems are employed to maintain organ preservation during transportation. China currently ranks second globally in the volume of human organ transplantation surgeries, a field that imposes stringent requirements on the transport process. The two most commonly used organ preservation methods in current clinical practice are static cold storage (SCS) and machine perfusion (MP). To address the increasingly severe shortage of donor organs, a significant number of marginal donor organs have been utilized in clinical settings, thereby placing higher demands on traditional organ preservation technologies.

Mechanical perfusion preservation not only enhances the efficacy of organ preservation and extends the permissible preservation time, but also provides a platform for organ quality assessment and injury repair, making it the primary direction of development in the field of organ preservation. On August 26, 2024, Paragonix Technologies, a company specializing in organ preservation and transport, announced its agreement to be acquired by Getinge for $477 million (approximately RMB 3.4 billion). This significant merger and acquisition highlights the market potential of extracorporeal circulation devices for organ transplantation.

In machine perfusion (MP) technology, normothermic machine perfusion (NMP) is a technique performed under normothermic conditions. The perfusate typically consists of red blood cells or hemoglobin solutions, which provide adequate oxygen and metabolic substrates to maintain normal aerobic metabolism of the organ, thereby effectively preventing ischemic injury and preserving organ function. Furthermore, NMP allows for real-time assessment of organ quality during perfusion and enables active repair of organ damage, thus reducing the rate of organ discard.

Characteristics of Organ Preservation Methods

Source: VBInsight

In this cutting-edge field, domestic enterprises are becoming the main force of innovation, leveraging cutting-edge technologies and design innovations aligned with clinical needs to transform existing NMP products. For instance, Qinghan Medical has introduced five major innovative designs for its NMP system: ① An integrated trolley and panoramic operating table design that meets the demands of various clinical scenarios, including patient transport and surgery; ② A dual-pump high-precision perfusion system featuring a pulsatile centrifugal pump to enhance microvascular perfusion, alongside a constant-flow centrifugal pump to stabilize blood pressure; ③ Proprietary development of a full range of oxygenators, including a specialized low-prime oxygenator designed specifically for liver NMP perfusion; ④ Real-time display of hemodynamic parameters, blood gas indices, and donor liver metabolites; ⑤ Embedded intelligent algorithms for temperature control and oxygen supply systems, creating an optimal biomimetic environment to support the survival and repair of ex vivo liver organs.

In 2024, China’s in vitro diagnostics (IVD) industry faced significant challenges. Influenced by the COVID-19 pandemic, domestic companies substantially expanded production capacity, resulting in excess supply that outstripped market absorption and intensifying price competition. Meanwhile, domestic reagent consumption in 2024 was affected by sluggish non-essential medical demand and the implementation of Diagnosis-Related Groups (DRG). Furthermore, changes in the regulatory environment in 2024 also exerted pressure on the industry.

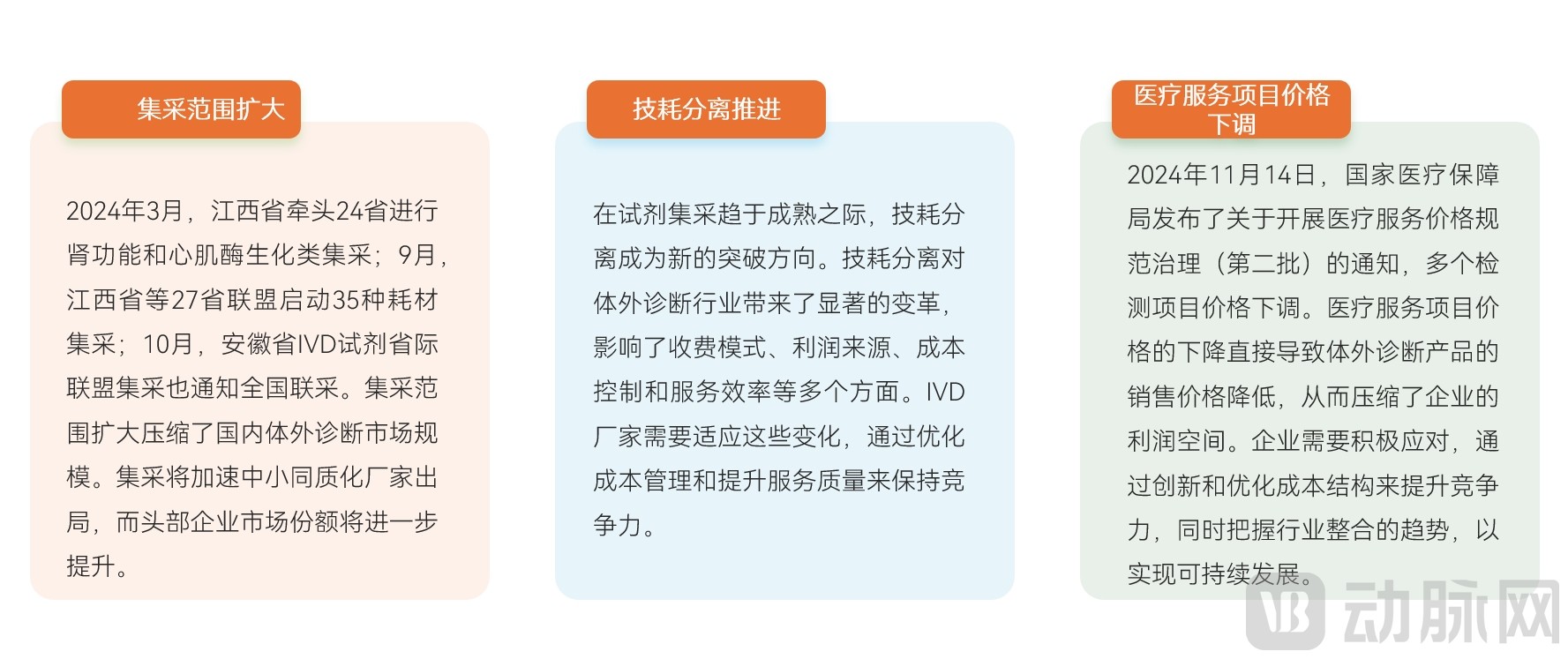

Major Policy Directions Impacting the In Vitro Diagnostics Industry in 2024

Source: VBInsight

The application of flow cytometry-based fluorescence in immunodiagnostics has garnered significant attention, particularly for enterprises that possess both upstream reagent technologies and the capability to industrialize instrument platforms.There are multiple reasons why this technology has garnered attention: ① Advantage of multiplexed detection: Flow fluorescence technology provides an efficient solution for simultaneous multi-analyte detection, enhancing testing efficiency and enabling high-throughput screening, which constitutes its most significant advantage. ② Breakthrough in full automation: The development of automated flow fluorescence systems addresses efficiency challenges, enabling unattended operation and providing strong support for large-scale clinical application. ③ Cost advantage in reagent testing: Compared with traditional chemiluminescence assays, consumable costs are significantly reduced, aligning better with the trend of centralized procurement in China’s in vitro diagnostics (IVD) industry. ④ Broad application scenarios: Flow fluorescence technology is primarily applied to the detection of cytokines, autoimmune diseases, tumors, and infectious diseases—fields characterized by a large patient base, long-term treatment regimens, and continuous testing demand. Furthermore, this technology holds potential for expansion into emerging markets such as the detection of Alzheimer’s disease biomarkers.

Meanwhile, flow cytometry-based fluorescence diagnostics has encountered several challenges in clinical applications. The primary challenge stems from the payment side: with the advancement of DRG/DIP payment reforms, cost-control requirements have become increasingly stringent. Particularly in the fields of autoantibody and allergen testing, traditional multi-analyte panel testing models urgently need to be adjusted within the DRG/DIP payment framework. This necessitates a more flexible and open testing platform to align with policy and market demands. Secondly, domestic enterprises need to invest in market education to enhance clinical recognition and expand the volume of clinical applications.

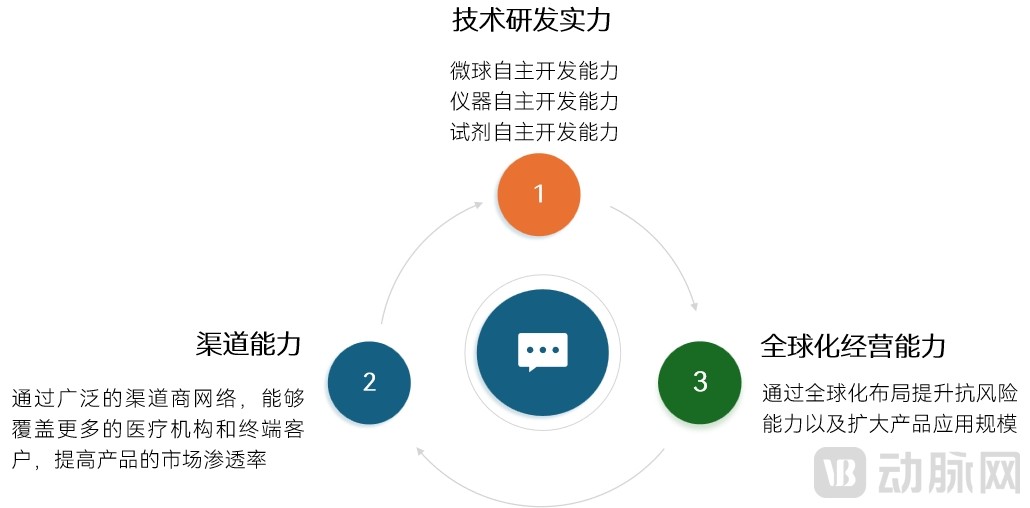

Opportunities and Challenges Coexist in the Field of Flow Cytometry Fluorescence Diagnostics: Leading Enterprises Must Possess Three Core CapabilitiesThe field of flow cytometry fluorescence diagnostics presents both opportunities and challenges. Leading enterprises must possess three core capabilities. First, strong R&D capabilities form the foundation. Companies need to master key technologies such as microsphere encoding, multiplex reagent development, optical detection, and software algorithms. This helps build core product competitiveness and expand market application potential. Second, channel capability is crucial. The commercialization of in vitro diagnostic (IVD) products relies on precise market positioning and robust channel marketing to achieve significant sales volume. Third, global expansion capability is key to broadening the application scope of flow cytometry fluorescence products and mitigating risks associated with fluctuations in any single market. This requires developing instruments and reagents tailored to the characteristics of overseas markets. Competition among enterprises has shifted from a focus on individual technologies to a contest of comprehensive strength. Going global has become a new arena for competition, where accumulated channel resources, business models, and high-quality products have emerged as critical competitive factors.

Flow Cytometry Fluorescence Enterprise Capability Landscape

Data Source: VBInsight

For instance, Human Intelligent Manufacturing has established long-term partnerships with multiple European IVD companies, forming a mutually binding cooperation model that achieves a win-win outcome for both products and distribution channels. Taking the German company HUMAN as an example, Human Intelligent Manufacturing acts as the agent for HUMAN’s products, responsible for market access, marketing, and after-sales services in the Chinese domestic market, while also conducting R&D and manufacturing for HUMAN. Leveraging its distribution resources in over 160 countries and its brand influence built over more than 50 years, HUMAN has successfully introduced Human Intelligent Manufacturing’s products to the international market. Currently, Human Intelligent Manufacturing’s POCT product line, HumaFIA, has successfully expanded overseas and is now marketed in dozens of countries across the Middle East, Latin America, Africa, and other regions. In addition, the company is laying out multiple other product lines, making its future global expansion prospects promising.

In recent years, despite the medical device industry facing a capital winter, the number of upstream and supply chain financing events has continued to rise, demonstrating the resilience of this sector.Against the backdrop of the rapid rise of China’s medical device industry chain and changes in the external environment, an increasing number of companies are seeking supply chain stability. The upstream core supply chain features low customer turnover and relatively stable operations, providing domestic upstream component manufacturers with predictable business prospects. This has created systematic development opportunities for Chinese upstream enterprises and signals significant potential for high-speed growth. Within the upstream segment of the medical device industry chain, financing has been concentrated in two major areas: first, the optimization and integration of the upstream supply chain; and second, the research, development, and innovation of core upstream components and materials. Progress in these two fields is crucial to enhancing the competitiveness of the entire medical device industry. In the past, imaging-related core components, such as CT X-ray tubes, received the most market attention; however, in 2024, several other core components have also garnered significant interest.

Domestic enterprises have made significant progress in the manufacturing of key components, successfully breaking the long-standing monopoly held by international companies.Taking magnetically levitated motors as an example, fully magnetically levitated motors serve as core components in critical medical devices such as left ventricular assist devices (LVADs) and extracorporeal membrane oxygenation (ECMO) systems. Meanwhile, in biopharmaceutical manufacturing, fully magnetically levitated stirrers help reduce shear stress risks in bioprocesses, thereby protecting bioactive substances. Furthermore, magnetically levitated motors play a significant role in semiconductor manufacturing. Previously, these critical components were monopolized by international companies, with key technological products such as magnetic levitation pumps even included on export control lists. Today, domestic enterprises in China have achieved technological breakthroughs in this field, filling the market gap.

For instance, Kaici Medical has developed a portfolio of products including a fully magnetically levitated implantable left ventricular assist device (LVAD), a fully magnetically levitated extracorporeal artificial heart, a fully magnetically levitated stirrer, and a fully magnetically levitated clean pump. The company’s latest-generation multi-degree-of-freedom fully magnetically levitated platform technology addresses issues inherent in other technical approaches, such as wear, heat generation, contamination, and blood damage. It achieves contact-free, frictionless, and heat-free operation with low shear stress, thereby maintaining excellent hemocompatibility. Furthermore, the company has achieved full in-house design capabilities for key components, including motor stators, rotors, sensors, and control systems. The motors used in its fully magnetically levitated intracorporeal and extracorporeal blood pumps effectively control product costs, making these therapies accessible to a broader patient population.

Domestic CDMOs are rapidly rising.Particularly in 2024, they have emerged as prominent players in several high-growth sectors, including endoscopy, minimally invasive surgery, in vitro diagnostics (IVD), laser medicine, and continuous glucose monitoring (CGM). Demand growth in the endoscopy sector has been especially significant; the development of single-use endoscopes has simplified product structures and reduced the complexity of cost control, thereby generating substantial demand for original equipment manufacturing (OEM) services. In the IVD field, the disparities between instrument and reagent production, coupled with the long cycles characteristic of R&D and manufacturing, have also spurred considerable demand for contract development and manufacturing organization (CDMO) services. These products typically feature complex structures, exhibit strong reliance on downstream distribution channels, and face stringent requirements for cost control and usage volume, further driving the growth in CDMO demand. By providing end-to-end services, domestic CDMO enterprises have lowered industry entry barriers, enabling Chinese companies to respond rapidly to market demands and accelerate product launches, thereby securing a competitive advantage in an intensely competitive market.

Development History of Domestic CDMOs

Data Source: VBInsight, Boston Consulting Group

Currently, most domestic CDMO companies are still at the stage of component processing, with relatively few able to provide end-to-end services from design to production. This situation indicates that there is significant room for growth for domestic CDMOs in offering comprehensive services, particularly in enhancing key capabilities such as R&D and design, clinical trials, regulatory submissions, and large-scale manufacturing. Nevertheless, some standout players have already emerged.

For instance, Dongmai Medical provides end-to-end services covering compliant design and development of medical devices, engineering translation, process transfer, inspection and validation, quality management systems, regulatory registration consulting, clinical services, small-scale trials, pilot-scale trials, and contract manufacturing for mass production. The company holds competitive advantages in the industrialization of medical-engineering integration, localization of imported devices, and intensive consolidation of existing enterprises. Leveraging high-quality industry-academia-research resources, it offers services such as technology introduction, production optimization, and regulatory submission, enabling rapid and cost-effective registration. Its production base is equipped with large-scale manufacturing equipment and high-precision testing instruments, capable of supporting multi-module, multi-disciplinary, and diverse medical device products to achieve large-scale production.

Based on the industry innovation logic analysis and corporate practice initiatives presented in this chapter, this white paper has selected the Top 20 Outstanding Innovation Cases of the Year, with detailed interpretations of select cases to be provided in subsequent chapters.

The above is an excerpt from the main content of the report. Scan the QR code to access the full version.

Table of Contents

Preface

CHAPTER 1: 2024 in Numbers

1.1 Macro Environment Undergoing Refinement, Industry Inflection Point Imminent

1.2 Volume-based procurement improves quality and expands coverage, moving beyond the impact of centralized procurement

1.3 Surgical Volume Continues to Grow, Driven by Strong Medical Demand

1.4 Investment and Financing Data: Investment and financing have entered a downturn phase, while M&A data shows growth

1.5 Overseas Expansion Data: Going Global Has Become an Imperative Path

1.6 Innovative Approval Data: Innovation Highlights Industrial Resilience

CHAPTER 2 Annual Industry Questions

2.1 High-Value Consumables

2.2 Medical Devices

2.3 In Vitro Diagnostics

2.4 Upstream Supply Chain and Core Components

CHAPTER 3 Interpretation of Innovation Cases in Medical Devices and Supply Chain

3.1 Kaici Medical—A Pioneer in Fully Magnetically Levitated Motor Technology

3.2 Angelai Technology—Intelligent Rehabilitation Medical Devices Focused on Brain Science Applications

3.3 Hisense Medical — Provider of Medical Imaging Equipment and Smart Healthcare Solutions

3.4 Core Medical Care – Providing Comprehensive Solutions for Heart Failure Patients Worldwide

3.5 Saihe Medical—A Provider and Pioneer of Active Interventional Diagnosis and Treatment Solutions for Pan-vascular Diseases in China

3.6 Zhongtian Medical – Providing a One-Stop Innovative Solution for Pan-Vascular Interventional Therapy in Clinical Practice

3.7 Dongmai Medical – Providing Full Lifecycle Solutions for Global Medical Device Products

3.8 Huaman Intelligent Manufacturing: Providing Comprehensive Diagnostic Solutions Centered on Flow Fluorescence Technology

3.9 Intalight: Meeting the Global Ophthalmology Community at the Pinnacle

3.10 MicroClear Medical: Ushering in an Era of Full-Eye, True-Synchronized Imaging, Leading a New Epoch in Ophthalmic Diagnosis and Treatment

3.11 Qinghan Medical — Providing Solutions for Microcirculation, Pulmonary Circulation, Systemic Circulation, and Circulatory Dynamics

3.12 Ruipai Medical—Providing Single-Use Endoscope Solutions for Minimally Invasive Diagnosis and Treatment

References: