Over 10,000 Yuan per Shot: Youth-Reviving PLLA Injections Spark a New Aesthetic Wealth Boom

Galderma

Developer of Dermatological Medical Solutions

“Rejuvenation Injection,” a product whose name evokes the promise of turning back the clock, is breathing new life into a long-established pharmaceutical company, pulling it out of years of losses.

Following the release of its third-quarter financial report, investors noted impressive performance from Jiangsu Wuzhong Pharmaceutical Development Co., Ltd., which was founded in 1993. From January to September 2024, the company’s medical aesthetics and life sciences business generated RMB 198 million in revenue, representing a year-on-year increase of more than 40-fold. Gross profit reached RMB 163 million, surging by over 60-fold year-on-year, while the segment successfully turned a profit after previous losses.

Behind the strong financial performance lies the outstanding achievement of the medical aesthetics business. In January this year, AestheFill, a collagen-stimulating injection under South Korea’s Regen Biotech (Lizhen) introduced by Jiangsu Wuzhong Pharmaceutical Development Co., Ltd., officially received approval from the National Medical Products Administration (NMPA) and was launched for sale in late April. It rapidly gained market traction, selling approximately 20,000 units within just two months (May–June) and generating a gross profit of RMB 66.4074 million.

This is not the first time that a collagen-stimulating injection product has become a bestseller in China.In 2021, AestheFill (Aiweilan), a poly-L-lactic acid-based collagen stimulator under Changchun Shengboma, and Ru Bai Angel, a similar product under Imeik, were successively approved for market launch, triggering a buying frenzy among medical aesthetic institutions. Notably, Ru Bai Angel achieved sales of 618,200 units that year (specific sales figures for AestheFill remain unknown as Changchun Shengboma was not yet publicly listed).

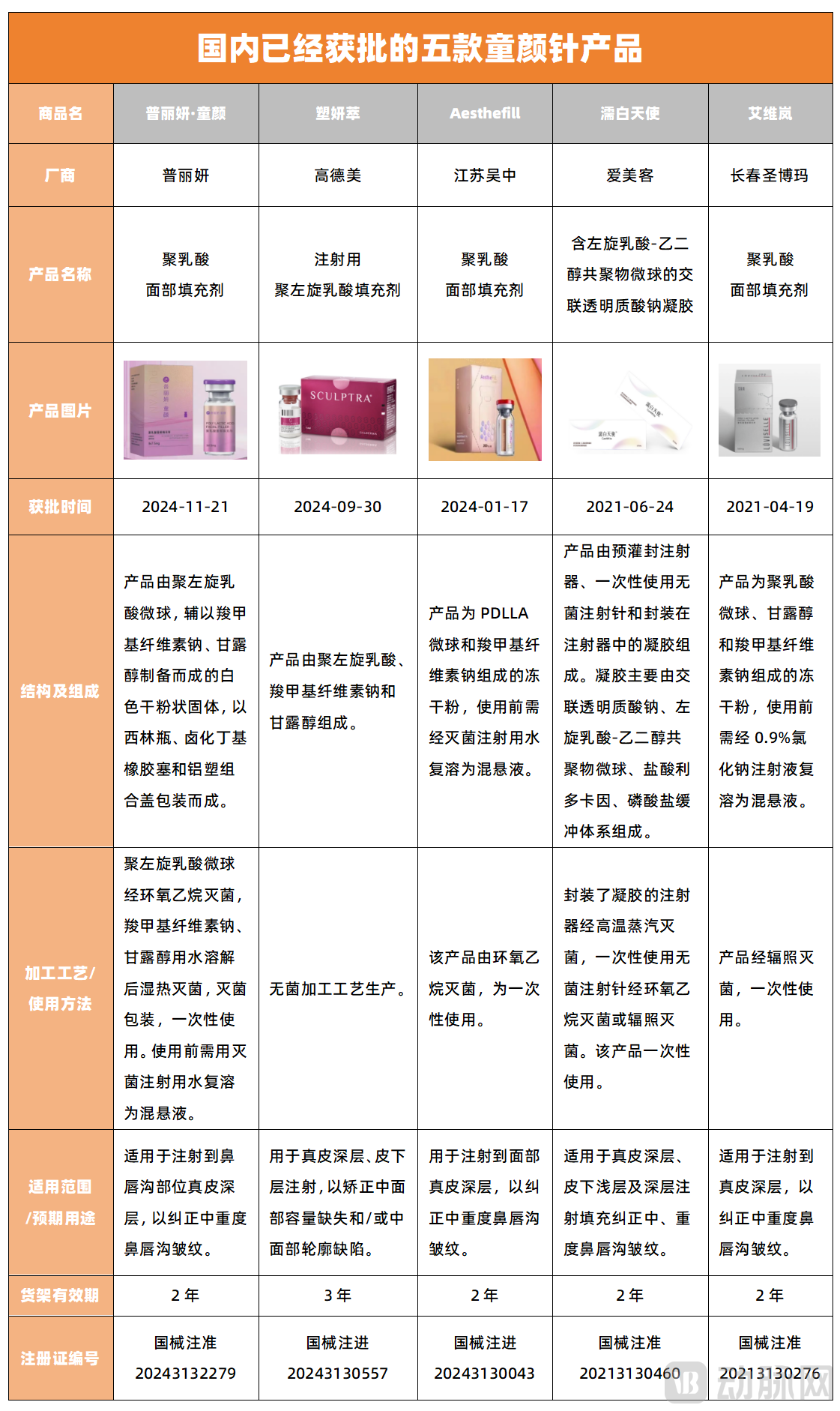

The immense potential for market growth has attracted numerous companies to enter the field, accelerating product development and regulatory approvals. So far this year alone, three poly-L-lactic acid (PLLA) biostimulatory injectables—commonly known as “baby face needles”—have received approval: Aisufei by Jiangsu Wuzhong Pharmaceutical Development Co., Ltd., Sculptra by Galderma, and Puliyan Baby Face by Puliyan (Nanjing) Medical Technology Co., Ltd.To date, five poly-L-lactic acid (PLLA) dermal fillers have been approved for market launch in China, creating a “five-way competition” landscape.

How will the competitive landscape of the poly-L-lactic acid (PLLA) filler market evolve as more players enter the fray? Where lie the new variables shaping the industry?

Although poly-L-lactic acid (PLLA) fillers were only approved in China in 2021, they are not new products in the medical aesthetics industry.

As early as 2004, Sculptra, under Galderma, received approval from the U.S. FDA for the correction of deep nasolabial folds and other wrinkles in patients with HIV; in 2009, the indications for Sculptra were further expanded to include aesthetic uses in healthy individuals, thereby unlocking the vast potential of biostimulatory injectables, often referred to as "youth-restoring injections," in the medical aesthetics industry.

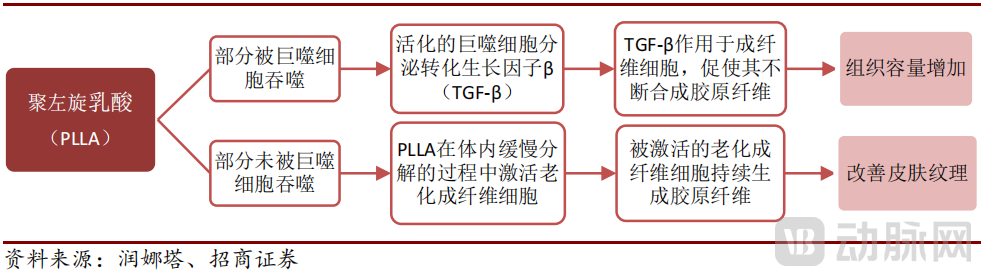

“As a synthetic medical-grade biodegradable macromolecular material,The core component of the "Baby Face Injection" is Poly-L-Lactic Acid (PLLA).“It typically integrates well with the human body and is absorbed by cells, thereby stimulating collagen regeneration in the skin and activating the dermis to achieve significant skin-tightening effects. This makes the skin appear more youthful and can also help slow down the aging process,” said an associate chief physician in the Department of Plastic Surgery at the outpatient clinic of a chain medical aesthetics institution, in an interview with VCBeat.

▲ Mechanism of Action of Poly-L-lactic Acid Image Source: China Merchants Securities

Driven by its favorable aesthetic outcomes, poly-L-lactic acid (PLLA) fillers, commonly known as “baby face injections,” have attracted a surge of interest among beauty enthusiasts. Prior to the domestic launch of approved products in China, many individuals even traveled abroad specifically to receive these treatments.

However, even though such products are now available on the Chinese market, the price of a single injection of Sculptra remains high.Currently, the average retail price for a single vial of poly-L-lactic acid (PLLA) dermal fillers, commonly known as "youth-restoring injections," exceeds RMB 10,000. As multiple vials are often required for certain treatment areas, the total cost ranges from RMB 40,000 to RMB 100,000, resulting in a high barrier to entry for consumers.

“Patients who typically visit outpatient clinics for injectable treatments are high-net-worth individuals aged 35 to 50, primarily seeking improvement in nasolabial folds and hollowing around the eye corners.” The associate chief physician of plastic surgery at the outpatient department of a chain medical aesthetics institution cautioned: “It is essential to receive Sculptra injections from qualified physicians at reputable medical aesthetics facilities. If product quality is substandard or administration is improper, excessive immune reactions at the injection site may occur, leading to granuloma formation. Additionally, patients should avoid premature contact between the injection sites and water to prevent infection and inflammation, which could impede local recovery.”

The ultra-high average transaction value and relatively high entry barriers have made poly-L-lactic acid (PLLA) fillers, commonly known as “baby face injections,” another blockbuster product in the medical aesthetics industry in recent years, raising high expectations that they will replicate the wealth-creation myth of hyaluronic acid.

According to data obtained by VCBeat from interviews, the domestic market size of PLLA-based biostimulatory fillers (calculated at ex-factory prices) was slightly over RMB 100 million in 2021, is projected to exceed RMB 3 billion in 2024, and is expected to reach a scale of RMB 10 billion within the next five years, reflecting a steep growth trajectory.

Amid rapid growth, three products were approved this year alone, creating a “five-way rivalry” in the market. Will this intensify internal competition?

“The industry is currently in a growth-phase market, and these products each have distinct differentiators, so significant competition has not yet emerged,” Wang Jun (a pseudonym used at the interviewee’s request), an investor at a state-backed investment firm, told VCBeat. “For instance, Imeik’s Rulan Angel is formulated as a liquid injectable that can be administered directly, with its differentiation lying in ease of use. Another example is the newly approved ‘youth-restoring’ injection under Puliyan, which leverages China’s leading technology in the preparation of poly-L-lactic acid (PLLA) injectable microspheres and microparticles, resulting in relatively longer-lasting regenerative effects.”

However, the “Big Five Rivalry” is not the end point of the market landscape.Faced with the lucrative incremental market, an increasing number of companies are flocking to the field of collagen-stimulating injections for facial rejuvenation.

According to incomplete statistics, among the “youth-restoring injections” currently under development in China, products from Sihuan Pharmaceutical, Lepu Medical, Shangli Biotechnology, and Huadong Medicine are expected to be launched between 2025 and 2026. Meanwhile, Hanggai Biotechnology’s Ruibo “youth-restoring injection” and Xihong Biotechnology’s “youth-restoring injection” are both in the registration application stage, while CMS Pharmaceuticals’ “youth-restoring injection” is in the clinical trial phase.

Once the PLLA-based “baby face” injection products from various companies receive regulatory approval, a fierce price war will be imminent. According to interviews conducted by VCBeat, the gross profit margin for these products generally exceeds 90%, which is rare among Class III medical devices. Industry experts widely agree that as competition intensifies, gross profit margins will decline to below 80%.

Furthermore, alongside this price competition, manufacturers are inevitably committed to enhancing product efficacy. In addition to modifying or functionalizing microspheres and developing materials with superior therapeutic outcomes, they are exploring optimizations in carrier components and the adoption of combination therapies. This trend will significantly boost the market penetration of collagen-stimulating injectables (commonly known as “Tongyan Zhen”).

“As one of the product categories in the market, ‘Tongyanzhen’ (collagen-stimulating injectables for facial rejuvenation) has secured its own market position; however, prices will undergo a repricing process as the competitive landscape continues to mature. Therefore,”Should there be future breakthroughs in expanding current indications and injection dosages, market share and pricing could offer greater upside potential.“Zhang Ming (a pseudonym, at the interviewee’s request), an institutional investor focused on consumer healthcare, stated, ‘For example, Lanluma, recently acquired overseas by Huadong Medicine, is a product that breaks through the existing indications for pediatric facial rejuvenation injections.’”

It is foreseeable that, as domestic competitors continue to emerge, the cost-effectiveness of poly-L-lactic acid (PLLA) fillers will continue to improve, and their indications will expand.

In addition to the intensifying internal competition among products driven by an increasing number of companies investing in PLLA-based biostimulatory fillers, are other mainstream supplemental injectable treatments on the market—such as skin boosters and CaHA-based biostimulatory fillers—considered competitors to PLLA-based fillers?

“Skin boosters and Sculptra belong to different product categories; as Sculptra is a regenerative material, it does not, in principle, compete with skin boosters,” said Zhang Ming, an institutional investor specializing in consumer healthcare. “Ellansé and Sculptra are both regenerative injectables used in medical aesthetics. They share the same mechanism of action—stimulating autologous collagen regeneration through inert materials—and undergo mid-to-long-term degradation. Administered via deep injection with comparable efficacy, they serve as strong potential competitors to each other.”

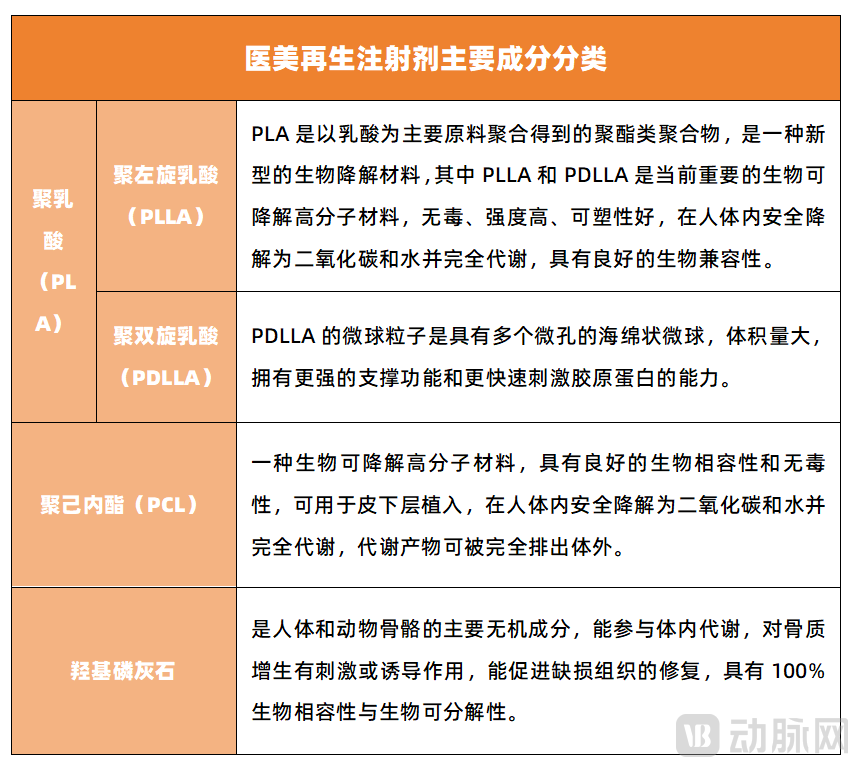

Based on the composition of currently marketed mainstream regenerative aesthetic injectables worldwide, they can be categorized into three types: polylactic acid (PLA), polycaprolactone (PCL), and calcium hydroxyapatite., while others are injectable products with hydroxyapatite as the main ingredient. Among them, those with PLA as the core component are generally referred to as "Baby Face Needle," whereas those with PCL as the core component are known as "Girl Needle."

▲Source: LeadLeo Research Institute

Similar to the “Baby Face Needle,” the first approved “Girl’s Needle” in China was introduced in 2021: Ellansé, an imported medical device under AQTIS Medical, distributed and sold in China by Sinocare Aesthetics, a wholly-owned subsidiary of Huadong Medicine. In August this year, the “Girl’s Needle” product from Shandong Guyuchun received approval, marking the second such product approved in China and the first domestically produced “Girl’s Needle” to gain regulatory clearance.

From the perspective of the current industry landscape,Regenerative medical aesthetic injectables currently constitute a growth market, with each product presenting its own market opportunities., and given that there are some differences in the therapeutic applications of Sculptra (commonly known as “Baby Face Needle”) and Ellansé (commonly known as “Girl Needle”), direct competition between the two will not be particularly pronounced for the time being, provided that the price differential is not substantial.

Taking Ellansé, distributed by Huadong Medicine, as an example, the product has experienced rapid sales growth since its launch in mainland China in August 2021. Its annual sales surpassed RMB 450 million within the first year of launch, and exceeded RMB 1 billion in 2023, making China the largest market for Ellansé.

Therefore, in the short to medium term, it remains difficult to determine which product performs better in the market—Sculptra or Ellansé—as both will jointly benefit from the growth dividends of regenerative aesthetic injectables.

Interestingly, the rise of regenerative aesthetic injectables has collectively eroded the market share of premium hyaluronic acid products.According to the STAR Market Daily, sales of Juvederm’s Voluma and Volite product lines have been impacted by regenerative medical aesthetic injectables. Moreover, among domestic hyaluronic acid products launched in the past two years, those priced above RMB 7,000 have barely made any splash in the market.

In response, many industry experts have stated that the primary challenge with regenerative aesthetic injectables, such as Sculptra and Ellansé, is their high cost. However, as related technologies undergo iterative optimization, the functionalities of these regenerative products may come to largely encompass the key advantages of hyaluronic acid fillers. This positions them to potentially capture a significant share of the market currently dominated by traditional dermal fillers, thereby becoming mainstream injectable anti-aging solutions.

However, in terms of absolute market size, the share of collagen-stimulating injections (commonly known as “Tongyan Zhen”) within the global market for injectable aesthetic treatments remains relatively small. In 2020, it accounted for only 1.14% of the global injectable aesthetic treatment market (data sourced from the SoYoung Medical Aesthetics Industry White Paper), and it is unlikely to compete with hyaluronic acid fillers in the short to medium term.

Behind this trend, on one hand, the relatively lower price of hyaluronic acid makes it more accessible to the general public; on the other hand, consumer education has been conducted over a longer period, and distribution channels are more mature.

Nevertheless, the substantial market growth opportunities have prompted companies to rush into the field. Currently, Sihuan Pharmaceutical and Yicheng Biologics, among others, have established their presence in the "Girl Needle" segment. Specifically, Sihuan Pharmaceutical’s second-generation "Girl Needle" is at the stage of registration application, while Yicheng Biologics’ second-generation product is in the clinical trial phase for registration. Coupled with the previously mentioned landscape of "Baby Face Needle" deployments, no fewer than 20 companies have now entered the domestic regenerative aesthetic injectables market.

“Currently, regenerative medical aesthetic injectable products are almost exclusively focused on skin tightening and anti-aging, resulting in relatively limited efficacy, lower efficiency in collagen stimulation, and shorter duration of contouring effects, soIf manufacturers fail to achieve further breakthroughs in efficacy and functionality, thereby creating more significant points of differentiation, market competition will become extremely intense.“Zhang Ming, an institutional investor focused on consumer healthcare, stated.”

Therefore, in the face of the upcoming market competition for regenerative medical aesthetic injectables, no participant can afford to be complacent. Only by delivering superior products can one secure a share of the market.

Following a discussion of the internal competition (a rapid increase in the number of companies laying out terminal products for collagen stimulators, with multiple products nearing approval) and external competition (potential competition from Ellansé and direct competition from high-end hyaluronic acid fillers) facing collagen stimulators, there is one sector that shows a positive correlation with the rapid growth of terminal collagen stimulator products.

These are the cornerstone of medical aesthetic products—raw materials.

As is well known, whenever a product becomes a blockbuster in the market, the upstream raw material supply chain associated with it also takes off. For instance, the strong sales of hyaluronic acid-based end products have expanded the market for companies involved in hyaluronic acid raw materials, supporting the growth of listed enterprises such as Bloomage Biotechnology, a major player in the hyaluronic acid raw material sector.

Moreover, the raw material sector for hyaluronic acid has formed an industrial cluster, with Chinese enterprises emerging as significant beneficiaries. According to the "China Hyaluronic Acid Industry Market Research Report" published by Frost & Sullivan, China’s total sales volume of hyaluronic acid raw materials accounts for approximately 80% of the global total, meaning that the raw materials for eight out of every ten hyaluronic acid products originate from China. Among these, the top five companies by sales volume—Bloomage Biotechnology, Focus Biotech, Fufeng Group, Dongchen Biotech, and Anhua Biotech—collectively hold a global market share of up to 75%.

Looking at the broader landscape of collagen-stimulating injectables, the sustained market enthusiasm for end-user products has triggered an explosive growth in the market for their raw material—medical-grade polylactic acid.

However, unlike the hyaluronic acid raw material market, which is crowded with competitors, only two companies worldwide currently hold complete regulatory approvals for the production of medical-grade polylactic acid (PLA) raw materials: one is Purac, a company based in the Netherlands, and the other is Changchun Shengboma, a Chinese enterprise.

This means that currently, only these two companies are capable of producing medical-grade polylactic acid (PLA) raw materials, while other manufacturers of "youth restoration injection" finished products basically need to procure their raw materials externally.

As a domestic entrant in the field of medical-grade polylactic acid (PLA) raw materials, Changchun Sinobioma relies on technical support from the Changchun Institute of Applied Chemistry, Chinese Academy of Sciences. It is reported that Changchun Sinobioma was established under the leadership of Academician Chen Xuesi’s team at the Chinese Academy of Sciences. The company currently offers more than 30 models of medical-grade PLA products and has built GMP-compliant production lines capable of large-scale, multi-model manufacturing of medical-grade polylactic acid-based polymer materials, with an annual production capacity of 10 tons.

Given the limited number of competitors in the medical-grade polylactic acid (PLA) raw material market, is it possible that end-product manufacturers will also enter this field?

Regarding this issue, some industry experts have stated that the preparation and mass production of medical-grade polylactic acid (PLA) raw materials involve significant technical barriers. Taking the preparation of poly(L-lactic acid) (PLLA) as an example, this material is highly sensitive to moisture, exhibits unstable performance, and is prone to degradation, making it difficult to achieve mass production with both high purity and high yield. Therefore, when selecting PLA raw materials for pharmaceutical applications, key parameters such as purity, residual monomer (lactic acid) content, and residual solvent levels must be closely monitored. Meeting these stringent specifications is no easy task.

Other industry experts, however, believe that the barriers to entry for medical-grade polylactic acid (PLA) raw materials are not particularly high. The primary reason some manufacturers previously refrained from entering this sector was the relatively small overall market demand. For end-product companies with in-house raw material production capabilities, establishing their own production lines without achieving global third-party supply would be economically inefficient in terms of cost control.

Currently, the market for medical-grade polylactic acid raw materials is already seeing undercurrents of change.: In this field, companies such as Jinkun Biology and Lixin Science have established their presence, leading to uncertainties in the industry landscape.

Facing future competition, Wang Jun, an investor at the aforementioned state-owned investment institution, believes: “The efficacy of product regeneration hinges critically on material selection and manufacturing processes. By thoroughly understanding intrinsic material properties, solidifying clinical data, and continuously optimizing technical processes, companies can significantly facilitate the expansion into new indications and the development of new products, thereby securing a competitive advantage for the future.”

Furthermore, it is an industry consensus that leveraging optimized combinations of various raw materials to enhance the functionality of existing products in alignment with market demands, as well as developing diverse product portfolios, is key to establishing a company’s core competitive barriers.

Meanwhile, at both the raw material and finished product levels, iterative process improvements have driven continuous declines in raw material and product prices, serving as a critical strategy for capturing market share.

After all, who can resist a product that is safe and effective, affordably priced, and capable of restoring a youthful appearance?