Domestic Biotechs Circle the $6B Bcl-2 Blockbuster with Next-Gen Inhibitors

CHIATAI TIANQING

High-quality pharmaceuticals research, production, and sales provider

BeOne

Developer of Molecular Targeted and Immune Anti-Tumor Drugs

InnoCare

Innovative Drug Developer

Bcl-2 is undoubtedly one of the most prominent targets at present.

First, Ascentage Pharma’s marketing application for its core candidate, lisoclastib tablets (APG-2575), was officially accepted recently.Poised to Become China’s First Approved Bcl-2 Inhibitor. Similarly, with regulatory approvals underway, CHIATAI TIANQING has recently made significant moves. Its self-developed Bcl-2 inhibitor, TQB3909 tablets, has successively received approval for two clinical trials. Furthermore, at the recently concluded ESMO Annual Meeting, the company presented its Phase I clinical results for the first time, demonstrating an 88.9% response rate in patients with CLL/SLL and a generally manageable safety profile.

In addition, BeOne Medicines has entered the fray. In April this year, its next-generation Bcl-2 inhibitor, sonrotoclax (BGB-11417), formally launched a “head-to-head” challenge against venetoclax. Preliminary study results indicate that sonrotoclax demonstrates greater potency and target selectivity compared with venetoclax, and also holds the potential to overcome common mutations associated with venetoclax resistance. Furthermore, while venetoclax is currently approved in China only for the indication of acute myeloid leukemia (AML), sonrotoclax is undergoing four registrational trials, all of which have advanced to Phase II clinical studies, signaling an imminent market launch.

However, as it stands,Venetoclax from AbbVie remains the only approved Bcl-2 inhibitor globally., since its FDA approval in 2016, its sales reached $2.3 billion in 2023, with further growth potential ahead. It is reported that venetoclax is still in a rapid phase of market expansion.There are over 250 global clinical trials underway, with peak sales projected to reach $6 billion in 2026.。

Figure 1. Representative Domestic Bcl-2 Inhibitors and Their Development Progress

Figure 1. Representative Domestic Bcl-2 Inhibitors and Their Development Progress

Amidst the massive market impact, domestic players have long been stirring beneath the surface and are now launching a fierce offensive against venetoclax,In addition to Ascentage, BeOne Medicines, and CHIATAI TIANQING, InnoCare, Fosun Pharma, and Lupeng Pharmaceuticals have also joined the race to develop vikneral.。

After a 20-Year Wait, “One Company Dominates”

AbbVie’s Journey Across the “Bcl-2 Inhibitor” Tightrope Has Not Been Easy

Bcl-2 is a protein that inhibits apoptosis. First discovered in 1983, its high expression is responsible for the tenacious viability of tumor cells. Therefore, effective inhibition of Bcl-2 protein expression can induce apoptosis in tumor cells, thereby exerting anticancer effects.

However, this is not easy to achieve, primarily because the binding interface and binding pocket of the Bcl-2 protein are both relatively large, making it difficult to design small molecules capable of blocking the interaction. Furthermore, drug delivery challenges associated with the Bcl-2 target have further increased the difficulty of drug development. Consequently, numerous related studies ended in failure during the early period spanning nearly a decade.

It was not until 1996 that Stephen Fesik, then Director of Drug Discovery at Abbott, finally found a way to break the deadlock. By dividing the binding pocket into two fragments, he proposed that if small molecules could be identified to bind to each fragment respectively, they could then be linked together. Following this strategy, AbbVie (spun off from Abbott in 2013) dedicated itself to intensive research and development. Despite experiencing two failures along the way, the collaboration with Genentech, which joined the effort in 2007, ultimately led to the joint selection of ABT-199, a near-perfect compound, enabling its successful market launch.

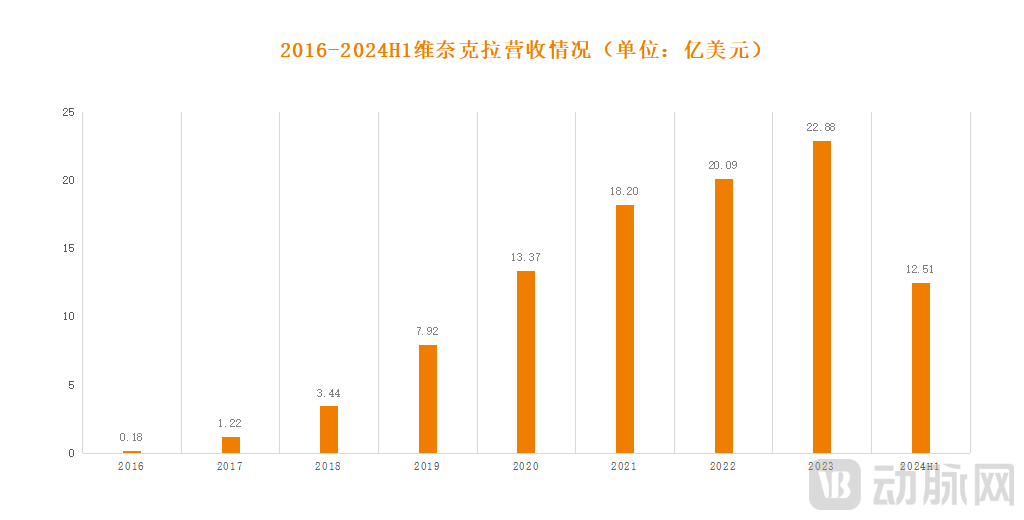

Figure 2. Venetoclax Revenue from 2016 to H1 2024 (Source: AbbVie Annual Report)

Figure 2. Venetoclax Revenue from 2016 to H1 2024 (Source: AbbVie Annual Report)

As the world’s first and only Bcl-2 inhibitor, venetoclax experienced rapid sales growth following its market launch.With $1.251 billion in revenue added in the first half of this year, Vicinay’s current total revenue has exceeded $10 billion., becoming AbbVie’s third blockbuster product after Humira and Imbruvica. However, unlike Humira and Imbruvica, which are currently facing growth bottlenecks, Venclexta remains in a phase of rapid ascent.

This is partly because it has a broad range of indications, including multiple hematologic malignancies such as CLL/SLL (chronic lymphocytic leukemia/small lymphocytic lymphoma) and AML (acute myeloid leukemia). These conditions generally have strong clinical demand and high unit prices, facilitating rapid sales volume growth. On the other hand, it faces limited market competition; as the world’s only Bcl-2 inhibitor, venetoclax currently maintains absolute market dominance.

However, venetoclax is not perfect.Issues of drug resistance and safety remain.。

It is reported that long-term administration of venetoclax may alter intracellular BCL-2 protein expression levels, leading to a significant reduction in its anticancer efficacy. Additionally, BCL-2 gene mutations may impair the binding between venetoclax and the BCL-2 protein, thereby diminishing drug effectiveness and causing a range of adverse effects, including gastrointestinal reactions, rash, neutropenia, thrombocytopenia, and peripheral hematomas.

To this end, venetoclax is currently administered using a weekly dose-escalation regimen. The recommended dosage is 20 mg once daily (QD) in Week 1, 50 mg QD in Week 2, 100 mg QD in Week 3, and 200 mg QD in Week 4, reaching 400 mg QD from Week 5 onwards until disease progression or intolerance occurs. Even so, severe tumor lysis syndrome (TLS) still occurs. From its approval in April 2016 to October 2021,The UK’s Yellow Card Scheme received a total of 28 suspected adverse drug reaction reports of tumor lysis syndrome (TLS) associated with venetoclax use, including seven fatal cases.。

This undoubtedly presents latecomers with an opportunity to overtake on the bend.

Domestic Brands Hit the Gas

Currently, China is far more active than overseas markets in targeting certain popular therapeutic targets, as evidenced by bispecific antibody-drug conjugates (BsADCs) and Bcl-2 inhibitors. According to the Insight database,There are currently 16 Bcl-2 inhibitors under development in China that have been approved for clinical trials, a number far exceeding that overseas.。

This intense enthusiasm stems not only from the substantial unmet clinical needs in hematologic malignancies but also, and importantly, from their strong potential for commercial realization—primarily referring to their attractiveness for business development (BD) partnerships with major pharmaceutical companies or for acquisition.

Taking APG-2575, the Bcl-2 inhibitor with the most advanced clinical progress in China, as an example, it holds significant potential for major business development (BD) deals. This is attributed to its efficacy and safety profile. Reportedly, when used in combination with the BTK inhibitor acalabrutinib for the treatment of patients with chronic lymphocytic leukemia/small lymphocytic lymphoma (CLL/SLL), the overall response rate (ORR) reached 100% in treatment-naïve patients and 97% in relapsed/refractory patients. Furthermore, APG-2575 demonstrated a more favorable safety profile, with lower incidences of tumor lysis syndrome (TLS) and neutropenia.

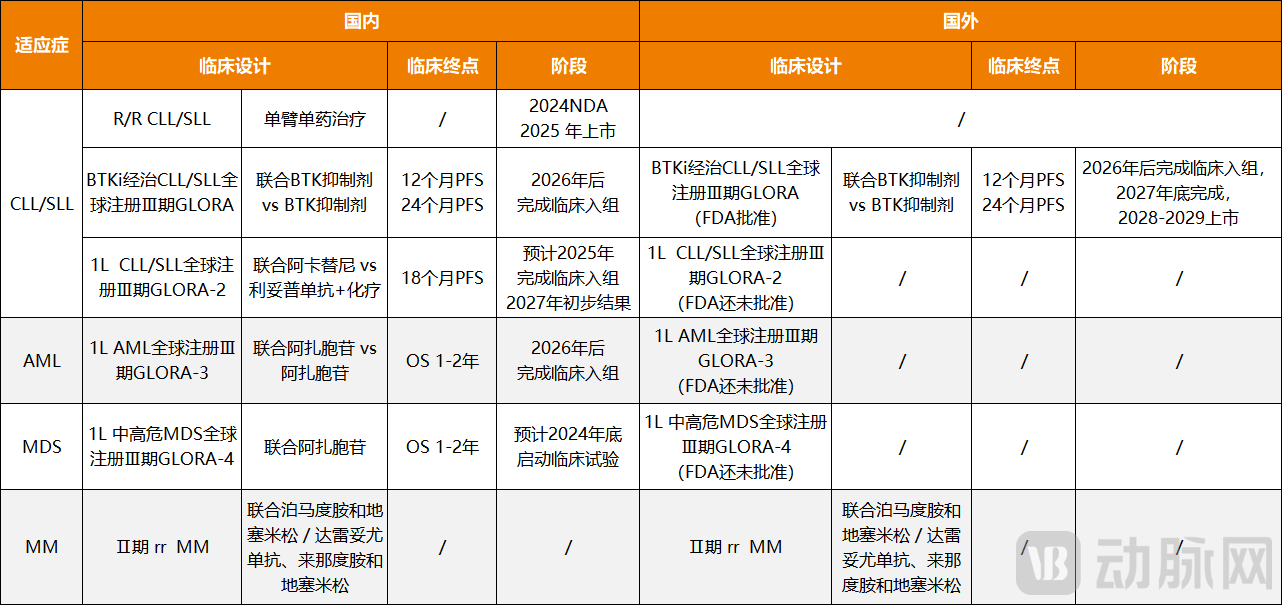

Figure 3. Indications and Clinical Progress of APG-2575 (Source: Haitong International Research Report)

Figure 3. Indications and Clinical Progress of APG-2575 (Source: Haitong International Research Report)

On the other hand, this is reflected in the indications; based on current clinical progress,APG-2575 is poised to capture all three major indications for hematologic malignancies—CLL/SLL, MM, and MDS—whereas venetoclax is currently approved in China only for CLL/SLL.In addition, four global Phase III registration trials of APG-2575 are progressing rapidly, with the expectation of submitting a New Drug Application (NDA) in the United States in 2026.

Certainly, APG-2575 is not the only asset with strong business development (BD) potential; BeOne Medicines’ sonrotoclax has also been gaining significant momentum recently. At the recently concluded ASH Annual Meeting, BeOne presented oral data from its Phase 1/1b study evaluating sonrotoclax in combination with zanubrutinib as first-line treatment for chronic lymphocytic leukemia (CLL). A total of 56 patients underwent response assessment, achieving an overall response rate (ORR) of 100%. Across all dose levels, the complete response (CR) rate increased over time, with a median time to CR of 10.1 months. In fact,Existing data on sonrotoclax are increasingly validating its potential to become the best-in-class Bcl-2 inhibitor in common indications such as CLL, AML, MM, WM, and MCL.。

It is worth noting that, in addition to Sonrotoclax, BeOne Medicines has another Bcl-2 inhibitor, BGB-21447. Although currently only in Phase I clinical trials, preclinical studies have shown that BGB-21447 exhibits greater potency and selectivity than Sonrotoclax, along with a longer half-life. This indicates that BeOne Medicines has established a “dual safeguard” strategy and is vigorously challenging Venetoclax’s dominant position.

In addition to Ascentage Pharma and BeOne Medicines, other domestically developed Bcl-2 inhibitors are rapidly advancing their clinical programs; most have now entered Phase II trials and all demonstrate the potential to become best-in-class therapies.

For exampleInnoCare's ICP-248, which can induce a longer duration of response and is expected to overcome the resistance issues associated with existing Bcl-2 inhibitors; for example,Lupeng Pharmaceuticals' LP-108, achieving an overall response rate (ORR) of 70% in patients with relapsed/refractory chronic lymphocytic leukemia/small lymphocytic lymphoma (R/R CLL/SLL) who had previously failed treatment with BTK inhibitors; furthermore, no tumor lysis syndrome (TLS) was observed under a rapid once-daily dose-escalation regimen; additionally,CHIATAI TIANQING's TQB3909, with a response rate of 88.9% in patients with CLL/SLL and 37.5% in patients with B-NHL, and an overall manageable safety profile; finally,Fosun Pharma's FCN-338, its Phase II clinical trials evaluating combination therapy with azacitidine or chemotherapy for the treatment of myeloid malignant hematologic diseases are underway, and several other clinical trials have also entered pivotal stages.

It is evident that domestic Bcl-2 inhibitors are currently accelerating toward approval, with the competitive pressure on venetoclax intensifying significantly. This signals that a major market showdown is inevitable; both the direct challenge to venetoclax and the subtle rivalry among domestic Bcl-2 inhibitors will soon unfold.

Ambition Does Not Stop Here

In terms of indications, Bcl-2 inhibitors are primarily used in hematologic malignancies. Due to their high incidence and aggressive nature, the market size for related drugs is substantial. According to data from Bizwit Research & Consulting LLP,The global market size of therapeutic drugs for hematologic malignancies reached $40 billion in 2024, with a projected CAGR of 6% during the forecast period from 2024 to 2029.。

Figure 4. Overview of the Six BTK Inhibitors Currently Approved and Marketed Worldwide

Figure 4. Overview of the Six BTK Inhibitors Currently Approved and Marketed Worldwide

It is reported that prior to the advent of targeted therapies, chemotherapy was the standard treatment for hematologic malignancies. The therapeutic landscape underwent a fundamental transformation in 2013 with the introduction of ibrutinib, the first Bruton’s tyrosine kinase (BTK) inhibitor. Subsequently, multiple BTK inhibitors, including AstraZeneca’s acalabrutinib and BeOne Medicines’ zanubrutinib, have received regulatory approval and entered the market. Offering superior efficacy and a more favorable safety profile, these agents have gradually replaced chemotherapy as the preferred treatment option for patients with hematologic malignancies.

However, BTK inhibitors still have limitations. According to industry insiders,Regardless of the BTK inhibitor used, the evolution and selection of subclones during continuous treatment are highly likely to lead to disease relapse and resistance to these drugs.. Therefore, there is an urgent need to identify a novel agent capable of addressing the “therapeutic blind spots” of BTK inhibitors, either as monotherapy or in combination. Fortunately, Bcl-2 inhibitors can fulfill this role.

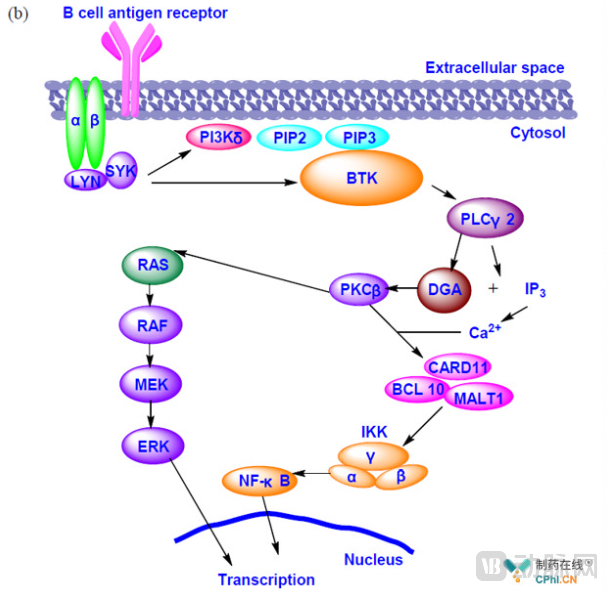

Figure 5. BTK signaling pathway (Image source: PharmaOnline)

Specifically, compared with monotherapy, the combination of Bcl-2 and BTK inhibitors offers greater advantages in enhancing efficacy and reducing drug resistance:BTK inhibitors can dislodge CLL cells from lymph nodes, allowing BCL-2 inhibitors to induce apoptosis of tumor cells in the circulation. This is akin to simultaneously “braking” tumor cell proliferation and “flooding the gas” for their apoptosis.。

It is precisely on this basis that this combination therapy is becoming the first-line standard for the long-term treatment of hematologic malignancies. It is reported that,Currently, only three companies are capable of independently completing combination therapies using their own drug portfolios: AbbVie, BeOne Medicines, and InnoCare., all three companies have their own BTK inhibitors and Bcl-2 inhibitors. Taking AbbVie as an example, it has made the most rapid progress by virtue of possessing the only approved Bcl-2 inhibitor on the market. This asset has enabled ibrutinib to achieve its first approved combination therapy: in August 2022, the European Commission approved the expansion of the indication for ibrutinib in combination with venetoclax as a first-line treatment for adult patients with chronic lymphocytic leukemia (CLL).

Following closely is BeOne Medicines, which is regarded as AbbVie’s most formidable competitor, thanks to zanubrutinib’s head-to-head victory over ibrutinib in 2022 and the superior efficacy of sonrotoclax compared with venetoclax. Lastly, InnoCare has just released clinical data on its BTK inhibitor orelabrutinib for the treatment of marginal zone lymphoma (MZL). Among the 12 enrolled patients, six completed the interim efficacy assessment, achieving an overall response rate (ORR) of 100%. Three patients completed combination therapy and entered the maintenance phase, maintaining an ORR of 100%.

Based on the data,AbbVie, BeOne Medicines, and InnoCare have formed a tripartite balance of power.So, how can pharmaceutical companies that do not yet have their own BTK inhibitors break through this impasse? The answer lies in finding strong partners suited to their specific needs.

Taking Ascentage Pharma as an example, although APG-2575 is the Bcl-2 inhibitor with the most advanced development progress in China, the company remains at a disadvantage in the competition for hematologic malignancies due to its lack of a BTK inhibitor. This is because the competitors for APG-2575 are not Bcl-2 inhibitor monotherapies, but rather combination regimens of BTK inhibitors and Bcl-2 inhibitors. To address this, Ascentage Pharma established a collaboration with AstraZeneca as early as June 2020, with both parties jointly exploring clinical trials of APG-2575 in combination with acalabrutinib. Currently, this trial has initiated a randomized Phase III confirmatory study this April.

However, many industry insiders believe that this is not the optimal choice for Ascentage Pharma. This is because pirtobrutinib, Eli Lilly’s third-generation BTK inhibitor, demonstrates superior efficacy. As the first and only non-covalent (reversible) BTK inhibitor approved by the FDA, it features significantly improved half-life and bioavailability, which could allow Ascentage’s APG-2575 to leverage greater synergistic benefits. Furthermore, given that Eli Lilly currently lacks a mature Bcl-2 inhibitor in its portfolio, the likelihood of collaboration between the two companies has increased substantially.

Of course, this all requires time to verify. But regardless,The combination of BTK inhibitors and Bcl-2 inhibitors will undoubtedly become the preferred treatment for hematologic malignancies in the future, sparking intense competition.. As the most potent adjunct, Bcl-2 inhibitors hold strategic significance that extends beyond revenue generation; they also help solidify a company’s position in the BTK inhibitor market. For instance, although AbbVie’s ibrutinib faced market headwinds, its combination with venetoclax revitalized its competitive edge, allowing the company to regain a favorable position in the competitive landscape.

This is undoubtedly a major trend, and who will emerge victorious in the future,It must achieve higher efficacy while maintaining consistent safety.. This “major battle” is about to begin. AbbVie currently holds a certain first-mover advantage, but domestic competitors represented by Ascentage Pharma and BeOne Medicines are in hot pursuit.

1. “Hunting the $6 Billion Blockbuster Drug” – Yaozhi.com;

2. “King of Hematologic Malignancies, Unsheathing the Sword” – Archimedes Biotech;

3. “The Strongest Adjuvant to BTK Inhibitors: Is Now the Right Time to Strike Gold with BCL-2 Inhibitors?” — Tong Xieyi.