2024 Annual Innovation White Paper on Medical Services: Thriving Specialties Amid Industry Winter

The industry continues to advance amid turbulence. This is a snapshot of the current healthcare services sector.

In 2024, the primary and secondary markets in the healthcare services sector continued to experience the “cooling” trend observed in 2023. Nevertheless, we are pleased to note that within the same year, companies operating in segments such as traditional Chinese medicine (TCM), oncology, and rehabilitation reported robust revenue growth; Ping An Good Doctor, a leading player in internet healthcare, achieved profitability for the first time; and the growth rate of health insurance premiums accelerated significantly.

As 2024 draws to a close, VBInsight, as a companion and witness in the healthcare sector, has compiled the "2024 Annual White Paper on Innovation in Healthcare Services." Through data consolidation, investor interviews, and other methods, this report aims to present a comprehensive overview of the development of the healthcare services industry in 2024 and its future trajectory from multiple perspectives, including data analysis and industrial innovation, for industry reference.

Service Data: Continuous Expansion of Healthcare Service Scale, with Accelerated Improvements in Supply and Efficiency

In 2024, China's medical services industry returned to a stable growth trajectory, with diversified service supply and improvements in quality and efficiency driving multidimensional growth across diagnostic and treatment services, pharmaceutical services, and other areas.

In 2024, China saw significant improvements in the total volume and efficiency of services provided by medical institutions. As of the end of November, five provinces/municipalities had released healthcare service data for certain periods in 2024, revealing a growth trend in healthcare service supply across different regions.

Healthcare Service Statistics for Selected Provinces/Municipalities in 2024, Source: Official Websites of Provincial/Municipal Health Commissions

Nationwide, the total volume of medical services has also seen significant growth. Data released by the National Health Commission shows that from January to April 2024, the total number of outpatient and emergency visits at healthcare institutions across China reached 2.5 billion, a year-on-year increase of 15.9%. During the same period, the total number of hospital discharges nationwide amounted to 107.945 million, representing a year-on-year increase of 11.2%.

The expansion of outpatient service capacity is attributable, on one hand, to the provision of diversified care options by offline medical institutions, such as midday and evening clinics, and on the other hand, to the optimization of healthcare processes through initiatives like “pre-consultation” services and “one-stop” service centers. In the online sphere, as of September 12, 2024, the number of internet hospitals across China had reached 3,340. Internet-based healthcare has become a vital component for users accessing medical services.

Private hospitals continue to maintain a development trajectory in service volume that is in sync with public hospitals, with standout performance in sectors such as traditional Chinese medicine (TCM), oncology, and rehabilitation.

Policy Data: Strictly Control Medical Services and Strengthen the Quality of Primary Healthcare

Since 2024, the National Health Commission, the National Healthcare Security Administration, and other relevant departments have jointly issued nearly 200 policy documents related to medical services. These policies focus on raising new requirements and providing new guidance for the high-quality development of medical services, particularly in areas such as improving service quality and implementing Version 2.0 of the DRG/DIP payment system.

In terms of enhancing medical service capabilities, multiple normative documents on capacity building across various healthcare service areas have been issued, focusing on “medical quality and safety” and “deepening the reform of the pharmaceutical and healthcare system.”

In the realm of anti-corruption in healthcare, the Work Plan for Large-Scale Hospital Inspections (2023–2026) was released to the public at the end of 2023, with a focus on inspecting medical corruption. Various regions have since followed suit by formulating corresponding policies.

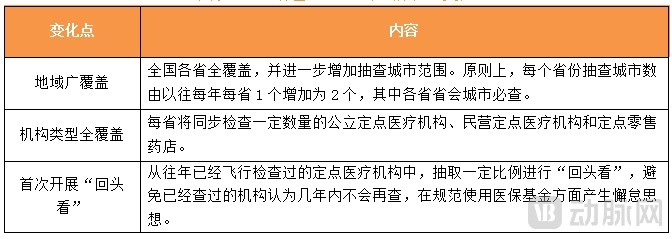

In terms of medical insurance, unannounced inspections of the medical insurance fund have become a major theme throughout the year. In April 2024, the National Healthcare Security Administration and other departments issued the "Work Plan for Unannounced Inspections of Medical Security Funds in 2024," focusing on inspecting the use and management of medical insurance funds, as well as the establishment and implementation of relevant internal control systems during the period from January 1, 2022, to December 31, 2023.

Changes in the 2024 Flight Inspections of the Medical Insurance Fund, Data Source: National Healthcare Security Administration

In the pharmaceutical sector, in November 2024, the National Medical Products Administration (NMPA) released the "Administrative Measures for Pharmaceutical Representatives (Draft for Comments)," aiming to curb unethical practices from a legislative perspective, further standardize the professional conduct of pharmaceutical representatives, and ensure the orderly and compliant implementation of academic promotion activities for pharmaceutical products.

Centralized procurement has further improved in quality and expanded in scope, with cochlear implants now included. By eliminating drug markups, implementing volume-based centralized procurement, and strengthening cost control, the reduction in prices of drugs and medical consumables has created conditions for adjusting medical service prices.

Regarding DRG/DIP, the National Healthcare Security Administration issued the "Version 2.0 Grouping Scheme for Diagnosis-Related Groups (DRG) and Big Data Diagnosis-Intervention Packet (DIP) Payment." Building on a closer alignment with clinical practice, the "grouping" framework emphasizes mechanisms for negotiated consultations and case-by-case review of exceptional cases.

Capital Data: Overall Investment Continues to Slow, Health Management Gains Popularity

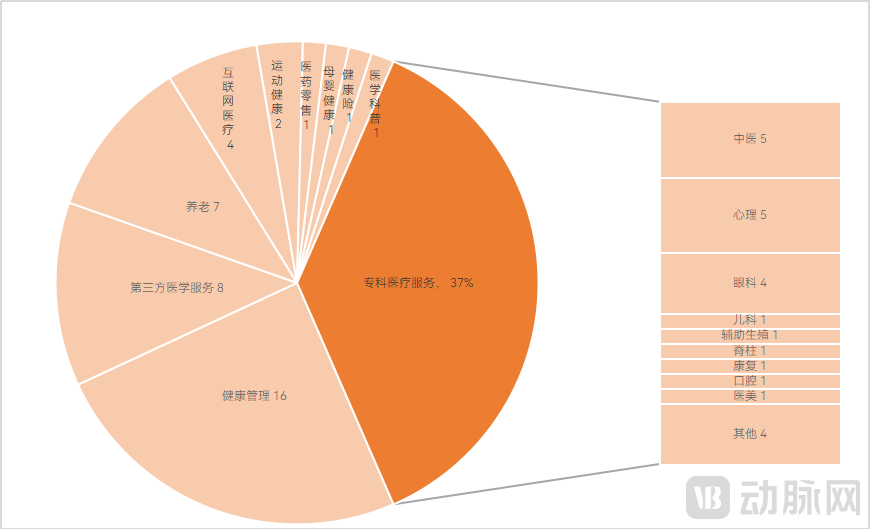

According to data compiled by VBInsight and Qichacha, a total of 65 financing deals were completed in the primary market for medical services by the end of November 2024, with a disclosed total financing amount of approximately RMB 2.946 billion. Compared with the 59 financing deals recorded in 2023, the number of transactions saw a slight increase, but the disclosed financing amount decreased compared to that of 2023.

From a segmented perspective, the health management sector accounted for the highest proportion of financing, with a total of 16 transactions. The traditional Chinese medicine (TCM) services sector also demonstrated notable performance.

Distribution of Primary Market Financing Events in Healthcare Services by Sub-sector; Data Source: VBInsight and Qichacha

Capital with “national team” backing was highly active in 2024. From an overall investment perspective, state-owned capital has focused its investments in the healthcare services sector on areas such as early disease diagnosis and health management.

“National Team” Funded Projects: Data sourced from VBInsight and Qichacha

Fourteen companies in the medical services sector filed prospectuses on the secondary market. Among them, Meizhong Jiahe, which provides oncology diagnosis and treatment services; Yimai Yangguang, which offers third-party medical imaging services; and Fangzhou Yunkang, which specializes in chronic disease management, successfully completed their IPOs and listed on the stock exchange. Differentiated advantages were a key factor in their successful listings.

Payment Data: Significant Growth in Health Insurance Premiums, Accelerated Integration of Public and Commercial Health Insurance Data

In 2024, the basic medical insurance fund continued to face significant challenges in cost containment, while commercial health insurance saw an acceleration in premium income growth. Meanwhile, the empowerment of commercial health insurance by the basic medical insurance system markedly accelerated in 2024.

China’s healthcare security sector continues to advance, with the medical insurance system being strengthened and yielding significant achievements. In terms of medicines covered by medical insurance, the combined effects of price reductions through negotiations and reimbursement are expected to reduce patients’ financial burden by more than RMB 50 billion in 2025. Regarding long-term care insurance (LTCI), as of November 2024, a total of 180 million people had enrolled in LTCI across 49 pilot cities nationwide, with over 2 million individuals having received LTCI benefits cumulatively. For direct settlement of cross-provincial medical expenses incurred outside one’s home province, this service benefited 170 million patient visits during the first three quarters of 2024. The scope of family members eligible for sharing funds from employees’ basic medical insurance personal accounts has been expanded beyond spouses, parents, and children to include other close relatives who are enrolled in medical insurance.

In terms of data application, 19 provinces, autonomous regions, and municipalities directly under the Central Government, including Hebei, Shanxi, Inner Mongolia, Chongqing, and Yunnan, have successively launched mini-programs for price comparison at designated pharmacies.

Methods for Public Price Comparison of Medical Insurance Drugs at Designated Pharmacies in Selected Provinces, Data Source: Official Website of the National Healthcare Security Administration

In the commercial health insurance sector, premium income reached RMB 873.9 billion from January to October 2024, representing an 8.46% year-on-year increase. This growth rate exceeded that of the same period in 2023, indicating a rebound trend. The integration of health management and health insurance continues to be explored.

From the national to the local level, the pace at which basic medical insurance is empowering commercial health insurance is accelerating. First, the first batch of compliant medical data has been listed for trading. In October 2024, China’s first batch of compliant and tradable data products from the national healthcare system were officially listed for trading at the Major Disease Data Industry Innovation Center of the Shanghai Data Exchange. Second, a “headquarters-to-headquarters” connection has been established for medical insurance information data. Third, the focus is gradually shifting from top-level design to operational implementation.

Bridging Resource Gaps: Why Are Traditional Chinese Medicine, Oncology, and Rehabilitation Sectors Surging?

In 2024, the sectors with particularly outstanding performance in private medical services were traditional Chinese medicine (TCM) services, oncology specialties, and rehabilitation.

Notably, the TCM services sector is exhibiting three major new trends. First, the strong market performance of TCM service providers in the secondary market has further stimulated investment and financing activities in the primary market. Of the 65 financing deals recorded by the end of November 2024, eight were related to TCM. Meanwhile, state-owned capital has gradually expanded from the traditional Chinese medicine (TCM) pharmaceutical sector into the TCM services sector. Second, expansion strategies among private TCM medical institutions are increasingly diverging. Tongrentang Medical and Elderly Care optimizes the allocation of medical resources through a tiered diagnosis and treatment system for TCM, delivering a customer-centric service experience. Gushengtang adopts a regional density strategy, focusing on areas with higher levels of economic development and stronger resident purchasing power for healthcare services. Third, the international expansion of TCM services is emerging as a significant new industry trend.

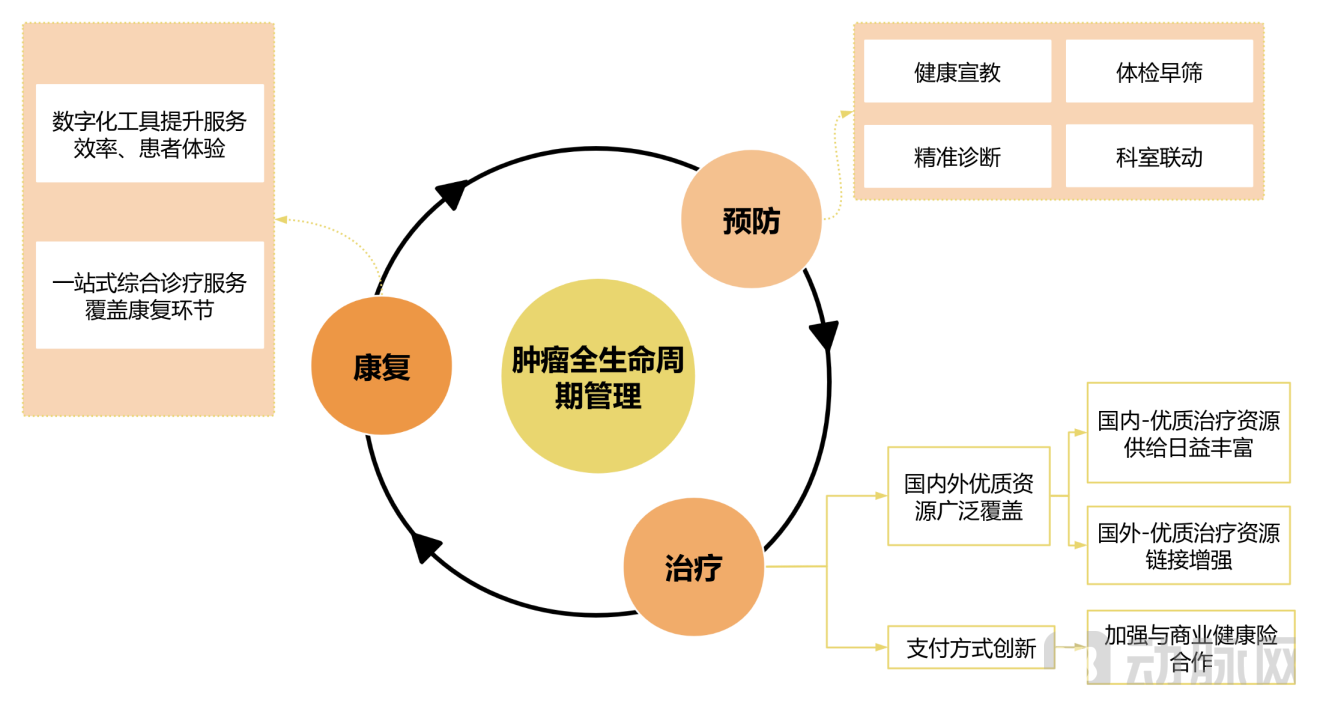

In the field of specialized oncology services, private cancer healthcare providers are increasingly pursuing public listings. Following the IPO of Meizhong Jiahe, key enterprises focusing on oncology medical services, such as Baize Medical Group and Lu Daopei Healthcare Group, have successively filed for initial public offerings. Meanwhile, private oncology institutions are steadily implementing various innovative initiatives, including expanding coverage of medical resources, improving treatment modalities, and integrating with commercial health insurance.

Private Medical Institutions Explore Full-Lifecycle Cancer Management, Chart by VBInsight

For example, high-quality overseas oncology care resources are entering China through cross-border medical services. Leveraging its network of over 1,100 medical institutions and more than 3,100 medical experts in Japan, Xikang Wanjia provides online remote consultations and oncology treatment services in Japan for middle- and high-net-worth individuals in China. It also introduces authoritative Japanese expert resources and healthcare service models into China, fostering academic exchanges and even joint discipline development between medical institutions and teams in both countries, thereby delivering higher-quality medical services to patients.

In the field of rehabilitation, demand continues to grow amid the aging trend. There are significant differences in rehabilitation needs among various population groups, creating new opportunities in specialized segments of rehabilitative medicine. Examples include cognitive impairment rehabilitation for the elderly and rehabilitation for female pelvic floor dysfunction. Furthermore, the industry saw innovations in 2024 addressing challenges such as the insufficient supply of rehabilitation resources and the standardization of rehabilitation service delivery.

For example, Jianjia Medical, as a chain rehabilitation group, has provided proven solutions for the establishment of rehabilitation hospitals, ensuring the continuous delivery of high-quality rehabilitation medical services. By promoting the tiered development of rehabilitation disciplines, it delivers premium services to patients. To address certain patient needs that cannot be met by in-hospital medical services alone, Jianjia Medical has innovatively proposed an integrated whole-course rehabilitation model and appointed “Rehabilitation Stewards” as case managers for patients. Based on the requirements of the rehabilitation journey and outcomes, these stewards integrate both medical and non-medical resources needed throughout the rehabilitation process, thereby achieving the goals of whole-course management, end-to-end service, and comprehensive setting-based rehabilitation for patients.

Consumer Spending Under Pressure, Intensified Competition Among Institutions: How Can Ophthalmology and Dentistry Innovate for Development?

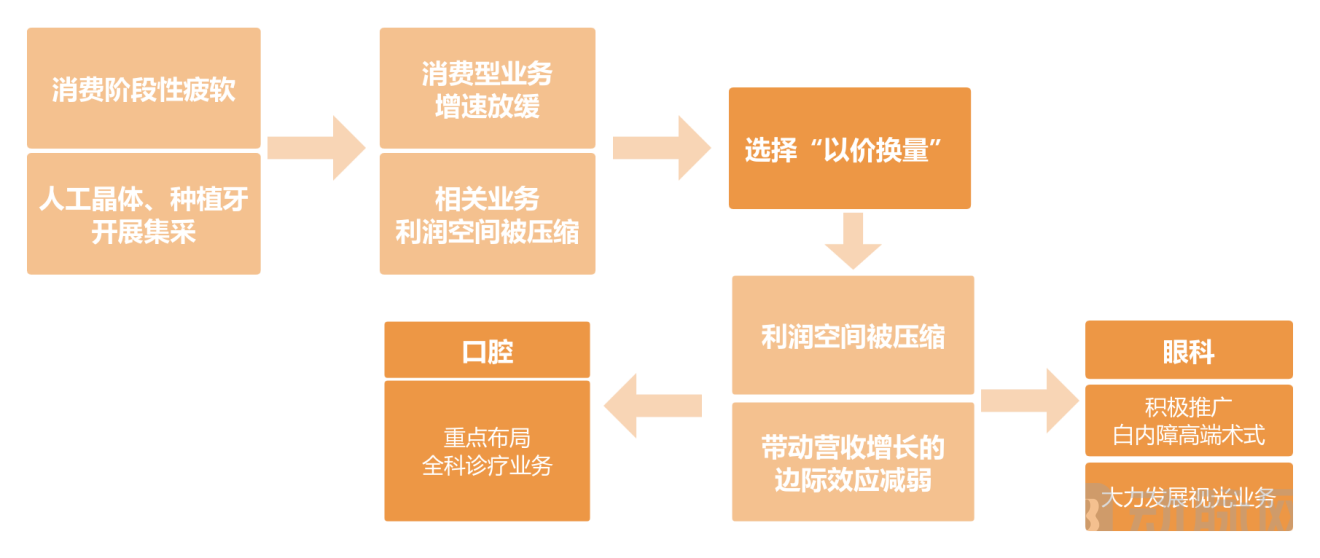

In 2024, private dental and ophthalmic medical service providers faced significant performance pressure due to the combined effects of centralized volume-based procurement (VBP) and temporary weakness in consumer demand. Seizing the opportunity presented by VBP, these institutions reignited price wars, posing challenges to their long-term, sustainable development.

Private Eye and Dental Medical Institutions Adjust Their Businesses; Chart Compiled by VBInsight

In response to businesses within the scope of centralized volume-based procurement (VBP), such as cataract services involving intraocular lenses and dental implant services involving dental implants, private ophthalmic and stomatological medical institutions have adopted a common primary strategy: “trading price for volume.” However, this approach has led to a decline in average revenue per user (ARPU), and its marginal effect on driving revenue growth is diminishing. In addition to “trading price for volume,” private ophthalmic and stomatological medical institutions have begun to actively adjust their business structures, employing slightly different strategic adjustments.

Business adjustments in private ophthalmic medical institutions primarily encompass two aspects: first, actively promoting multifocal intraocular lenses and advanced surgical techniques to meet patients’ diverse medical needs and enhance profit margins; second, capitalizing on new policy developments and market trends by prioritizing the expansion of optometry services. In contrast, business adjustments in private dental institutions are mainly evolving toward “providing users with full-lifecycle oral health,” with active deployment of general dental practice services.

Adjustments to the business architecture are also driving changes in expansion models. A community-based, small-scale expansion model is best suited for optometry and comprehensive dental services. This is because stores located near communities reduce patients’ travel time, and given their relatively fixed service radius and customer base, community stores are better positioned to provide in-depth services to residents, thereby enhancing customer stickiness and achieving the goal of delivering lifelong eye and oral health care to customers.

Taking Beitong Pediatric Ophthalmology as an example, the company has expanded its network to 10 directly operated clinics in Shanghai through a community-based strategy, and has strengthened patient engagement by offering customized and diversified diagnostic and treatment services via a membership-based service system. Among these 10 clinics, nine have already achieved profitability, with single-clinic revenue for new locations recording over 100% growth in 2024.

In addition to becoming more community-based and smaller in scale, private dental clinics have continued their expansion into lower-tier markets. In 2024, the number of dental institutions saw significant growth in several less economically developed provinces, such as Guizhou, Gansu, and Jiangxi. In contrast, in China’s most economically advanced regions, such as Beijing and Shanghai, the number of dental institutions either declined or experienced slowed growth. This indicates that “lower-tier markets” have become a key destination for the expansion of dental institutions.

Profitability Has Become the Core Mission: Is Internet Healthcare No Longer Relying on “Blood Transfusions”?

Two landmark events in the internet healthcare industry in 2024 signal its continued progress amid turbulence: first, the acquisition of Haodf Online; and second, the growth in the number of profitable companies.

In 2024, Ping An Health achieved profitability for the first time by implementing its managed care strategy and strengthening the construction of two core hubs: family doctors and elderly care stewards. The net profit for the first half of the year reached RMB 60.629 million. In June 2024, the Ping An Family Doctor brand underwent an upgrade. Its newly released “11312” one-stop proactive health management service system includes a 5A-standard service pathway guided by the Chinese Society of General Practice of the Chinese Medical Association and certified/coached by AGPAL, the designated certification body appointed by the Royal Australian College of General Practitioners (RACGP). It also features three sets of proactive health management service plans tailored for sub-healthy populations, individuals with chronic diseases, and patients with acute illnesses. This framework establishes a standardized operational system for efficient collaboration among medical services, pharmaceuticals, and health management, providing target customer groups with worry-free, time-saving, and cost-effective health and disease management services.

The online pharmaceutical e-commerce market (including B2B, B2C, O2O, and other models) continues to expand. The pharmaceutical e-commerce sector is undergoing two major adjustments: first, online channels are gradually becoming a key distribution channel for prescription drugs, further improving service accessibility; second, the gradual refinement of online medical insurance settlement policies and the expansion of their scope are further driving online medication purchases, thereby enhancing the convenience of pharmaceutical services.

The Closed-Loop Service of Internet Healthcare: Medical Testing, Pharmaceuticals, and Nursing Care — Chart Compiled by VBInsight

Meanwhile, the internet healthcare industry is not content with the “medical consultation + pharmaceuticals” service model and continues to deepen its involvement across multiple stages—pre-consultation, during consultation, and post-consultation—to better meet patients’ diverse service needs. On one hand, large internet healthcare platforms are strengthening their pre- and intra-consultation “disease detection” services, which have historically been lacking in internet healthcare. On the other hand, these platforms are further expanding their post-consultation “disease care” services.

For example, during the peak season for respiratory diseases in the autumn and winter of 2023, JD Health launched the “JD Daojia Rapid Testing” service. After users book the service online, dedicated riders will visit their homes to collect samples. Following the instructions provided, users complete the oral and nasal swab sampling themselves and hand the samples to the dedicated riders, who then deliver them to offline testing laboratories. Test reports are typically issued within three hours and automatically uploaded to the JD App. By integrating with its existing ecosystem, the “JD Daojia Rapid Testing” service has established a closed-loop offering encompassing medical consultation, testing, diagnosis, and pharmaceutical services. In September 2024, JD Health further introduced the “Nurse-at-Home” service, enabling users to access professional medical care without leaving their homes.

Health Insurance Growth Rebounds: Has the Bonus Period for “Insuring Individuals with Pre-existing Conditions” Arrived?

From population coverage and benefit levels to product operations and sales scenarios, and further to the integration with industrial resources in healthcare, pharmaceuticals, and health management, innovation in commercial health insurance accelerated in 2024, permeating every aspect of product development and operations.

In terms of population coverage, driven by factors such as clear policy preferences and strong market demand, major insurance companies continued to explore commercial health insurance coverage for three categories of “special populations” in 2024: individuals with pre-existing conditions, the elderly, and children.

The further expansion of population coverage and the enhanced protection for special groups depend on the improvement of insurers' digital intelligence capabilities and deeper integration with industrial resources in healthcare, pharmaceuticals, and health management.

In 2024, innovations in the digitalization and intelligence of health insurance primarily encompassed two areas: the accelerated sharing of medical insurance data and the practical implementation of large language models (LLMs). In 2024, the pace at which medical insurance data was shared with commercial insurers significantly increased. This accelerated sharing of healthcare-related data is expected to help insurers overcome challenges in innovating health insurance products, particularly those designed for special populations. Meanwhile, the practical application of LLMs holds theoretical promise for enhancing insurers’ actuarial capabilities, strengthening underwriting and claims risk control, improving claims processing efficiency, and enabling precision marketing.

Based on the implementation of large language models in health insurance in 2024, intelligent claims processing and intelligent marketing have emerged as the most mature application scenarios. In the future, with further opening and sharing of medical insurance data, and the expanded application of digital intelligence capabilities such as AI and large language models, health insurance products will see enhanced capabilities in product design, pricing, operations, and marketing.

Furthermore, the deep integration of “medical care + pharmaceuticals + insurance” has also been a major objective in the development of health insurance in recent years. In 2024, both the breadth of resource integration and the depth of collaboration saw significant improvements.

By integrating innovative logic analysis with corporate practical initiatives, this white paper has selected the Top Ten Outstanding Innovation Cases of the Year. VBInsight provides detailed interpretations of selected cases in subsequent chapters.(The above is an excerpt from the main content of the white paper. To obtain the full report, please scan the QR code in the image below.)

The following is the report table of contents:

Chapter 1: Analysis of Healthcare Service Data in 2024

1.1 Service Data: The scale of medical services continues to expand, with accelerated improvements in supply and efficiency

1.2 Policy Data: Strictly Control Medical Services and Strengthen the Quality of Primary Healthcare Services

1.3 Capital Data: Overall Investment Continues to Slow, Health Management Gains Popularity

1.4 Payment Data: Significant Growth in Health Insurance Premiums, Accelerated Interoperability Between Public and Commercial Medical Insurance Data

Chapter 2: Four Key Questions on Healthcare Services in 2024

2.1 Supplementing Shortcomings in Resources: Why Have Traditional Chinese Medicine, Oncology, and Rehabilitation Sectors Surged?

2.2 Consumer Spending Under Pressure, Intensified Competition Among Institutions: How Can Ophthalmology and Dentistry Innovate?

2.3 Profitability Has Become the Core Mission: Is Internet Healthcare No Longer Relying on “Cash Infusions”?

2.4 Health Insurance Growth Rebounds: Has the Bonus Period for "Pre-existing Condition" Insurance Arrived?

Chapter 3 Interpretation of Innovative Cases in Medical Services in 2024

3.1 JD Health: Further Expansion of Internet Healthcare, Building a One-Stop Closed-Loop Service for “Medical Consultation, Testing, Diagnosis, and Pharmacy”

3.2 Jianjia Medical: “Multi-Site in One City” Chain Service Layout, Accelerating the Supply of Continuous Rehabilitation Medical Services

3.3 Ping An Health: Healthcare Services Undergo Another “Iteration,” Proactive Health Management Sets New Service Standards

3.4 Beitong Pediatric Ophthalmology: Deepening Expertise in the Field of Children and Adolescent Eye Care, with a Regional Chain Model Leading New Breakthroughs in Outpatient Services

3.5 Xi Kang Wan Jia: Providing One-Stop Cross-Border Services and Building a Bridge for Medical Communication Between China and Japan

Appendix Table 1: Details of Financing in the Medical Services Sector in 2024

Appendix 2: Key Policies in the Medical Services Sector in 2024