China's Innovative Biotech Targets a Ten-Million-Patient Blue Ocean with First-in-Class Nephrology Drug

The “cold bench” of chronic kidney disease in the pharmaceutical industry is poised to be warmed up by Chinese biotech firms.

Compared with hot sectors such as oncology and weight management, nephrology has been a relatively neglected area in drug development in recent years. However, multinational pharmaceutical companies, including Biogen, Vertex Pharmaceuticals, and Novartis, have recently engaged in a wave of mergers and acquisitions, with total transaction values exceeding $10 billion.

This shift stems from the FDA’s acceptance of surrogate endpoints in nephrology clinical trials, which has significantly lowered the barrier to entry for innovative drug development in this field and accelerated the R&D pace. Consequently, multinational corporations (MNCs) have naturally increased their investments, ushering in a golden era for the nephrology market over the next few years. Although IQVIA’s “White Paper on Chronic Kidney Disease in China” noted that drug development in this area progressed slowly over the past decade, several Chinese biotech companies had already strategically positioned themselves during this prolonged R&D winter, positioning them well to potentially deliver first-in-class (FIC) therapies.

The risk of chronic kidney disease (CKD) progressing to end-stage renal disease (ESRD) is extremely high in China, and the resulting socioeconomic burden is receiving increasing attention.

Following a new round of negotiations, budesonide delayed-release capsules have been successfully included in the latest 2024 National Reimbursement Drug List (NRDL). This inclusion was based on clinical data demonstrating that a 9-month treatment course can delay the progression of IgA nephropathy to dialysis or kidney transplantation by an estimated 12.8 years. This development not only reflects strong endorsement from the national healthcare security system for innovative therapies with favorable cost-effectiveness profiles but also underscores the growing market potential in the field of nephrology.

It is evident from the inclusion of budesonide that treatment regimens prioritizing early intervention, striving to preserve patients’ renal function, and delaying the progression to kidney failure have become the preferred choices for medical insurance coverage. Budesonide is the first and only etiologic therapy for IgA nephropathy to receive full approval from the U.S. Food and Drug Administration (FDA). It is also the first non-oncology drug designated as a breakthrough therapy by the National Medical Products Administration (NMPA).

In the “2024 KDIGO Clinical Practice Guideline for the Management of IgA Nephropathy and IgA Vasculitis (Public Review Draft),” budesonide is considered the only treatment proven to date to reduce levels of IgA and IgA immune complexes. In the field of IgA nephropathy treatment, budesonide has firmly established itself as a first-line cornerstone therapy.

Budesonide, with its innovative mechanism of action and superior efficacy, fills the gap in etiology-targeted therapy for IgA nephropathy. Coupled with volume expansion driven by medical insurance coverage, its commercial prospects are promising.

On the other hand, multinational corporations (MNCs) are also intensifying their efforts to compete in the kidney disease therapeutics market.

In May 2024, Biogen acquired HI-Bio for $1.8 billion, primarily targeting its core asset felzartamab for the treatment of IgA nephropathy. In April 2024, Vertex Pharmaceuticals announced the acquisition of Alpine Immune Sciences for $4.9 billion, thereby securing povetacicept, an investigational therapy for IgA nephropathy. Earlier in January, Novartis acquired Sinuano Therapeutics, a China-based company focused on kidney diseases and related treatments; this follows Novartis’ previous $3.5 billion acquisition of Chinook Therapeutics, which also specializes in therapies for IgA nephropathy.

The Window of Opportunity for the Kidney Disease Pipeline Has Arrived.

Currently, the therapeutic breakthroughs have only reached the field of IgA nephropathy. Although there are nearly 5 million patients with IgA nephropathy in China, other glomerular diseases—such as membranous nephropathy (approximately 2 million patients), minimal change disease (approximately 2 million patients), and focal segmental glomerulosclerosis (approximately 1 million patients)—also remain in a state of having no available treatments. In this vast blue-ocean market encompassing nearly 10 million patients, multinational corporations (MNCs) and domestic biotech companies are on an equal footing; whoever takes the lead will secure the first-mover advantage.

Membranous nephropathy has surpassed IgA nephropathy to become the primary glomerular disease with the fastest-growing incidence rate in China in recent years.

According to statistics from “Evolution of the Spectrum of Chronic Glomerular Diseases and Epidemiological Characteristics of Membranous Nephropathy,” the proportional composition of glomerular diseases, represented by IgA nephropathy and membranous nephropathy, has changed significantly over the past two decades. The proportion of membranous nephropathy increased from 5.5% in 2001–2006 to 22.5% in 2013–2018.

Over the past 11 years, membranous nephropathy has been increasing at an annual rate of 13%.

In North and Northeast China, the incidence of membranous nephropathy has surpassed that of IgA nephropathy, making it the most common primary glomerular disease. Relevant studies indicate that, without treatment, 14% of patients may progress to renal failure within 5 years, approximately 35% within 10 years, and 41% within 15 years.

According to data released at the 2024 Annual Academic Conference of the Nephrologist Branch of the Chinese Medical Doctor Association (CNA), in 2023, the proportion of primary glomerular diseases among hemodialysis patients in China (37.7%) exceeded the combined total of diabetic nephropathy (21.8%) and hypertensive nephropathy (12.4%).

This is closely related to the current lack of specific therapeutic agents for membranous nephropathy.

Currently, there are no drugs approved worldwide specifically for membranous nephropathy. Guidelines such as those from KDIGO recommend conservative supportive care aimed at alleviating clinical symptoms, including proteinuria, edema, and hypertension. For patients who do not respond to supportive therapy or who are at high risk of disease progression, immunosuppressive therapy—either as monotherapy or in combination—is employed. This includes traditional agents such as cyclophosphamide, prednisone, and other corticosteroids, as well as newer immunosuppressants like calcineurin inhibitors (cyclosporine and tacrolimus) and anti-CD20 monoclonal antibodies (e.g., rituximab).

These commonly used immunosuppressive agents are all being used off-label, with unsatisfactory safety and efficacy profiles; for instance, the cyclophosphamide plus corticosteroid regimen carries a risk of carcinogenesis, while calcineurin inhibitors are associated with high relapse rates.

This means that 2 million patients are left with no available treatment options.

New-generation drugs for membranous nephropathy have considerable room for development.

Key processes in the progression of membranous nephropathy, including antigen presentation and T-cell and B-cell activation, have become focal points for pharmaceutical R&D. Therapeutic targets within pathways such as CD20, CD38, BTK, BAFF, and the complement system are now under active investigation.

Currently, immunosuppressants represent the mainstream direction of research and development for membranous nephropathy. The efficacy of targeted CD20 monoclonal antibody therapy, exemplified by rituximab, has been confirmed; however, approximately 40% of patients do not respond to this treatment. Consequently, there are three primary pathways in the global clinical pipeline: First, next-generation anti-CD20 monoclonal antibodies with improved bioavailability achieved through humanization and glycosylation modifications are being developed to replace rituximab. Second, therapies targeting alternative immune mechanisms, such as CD38, APRIL/BAFF, and BTK, are being explored to benefit patients who are refractory to anti-CD20 monoclonal antibodies, thereby serving as an important complement to these agents. Third, complement therapy aims to manage renal injury through drugs targeting complement factors.

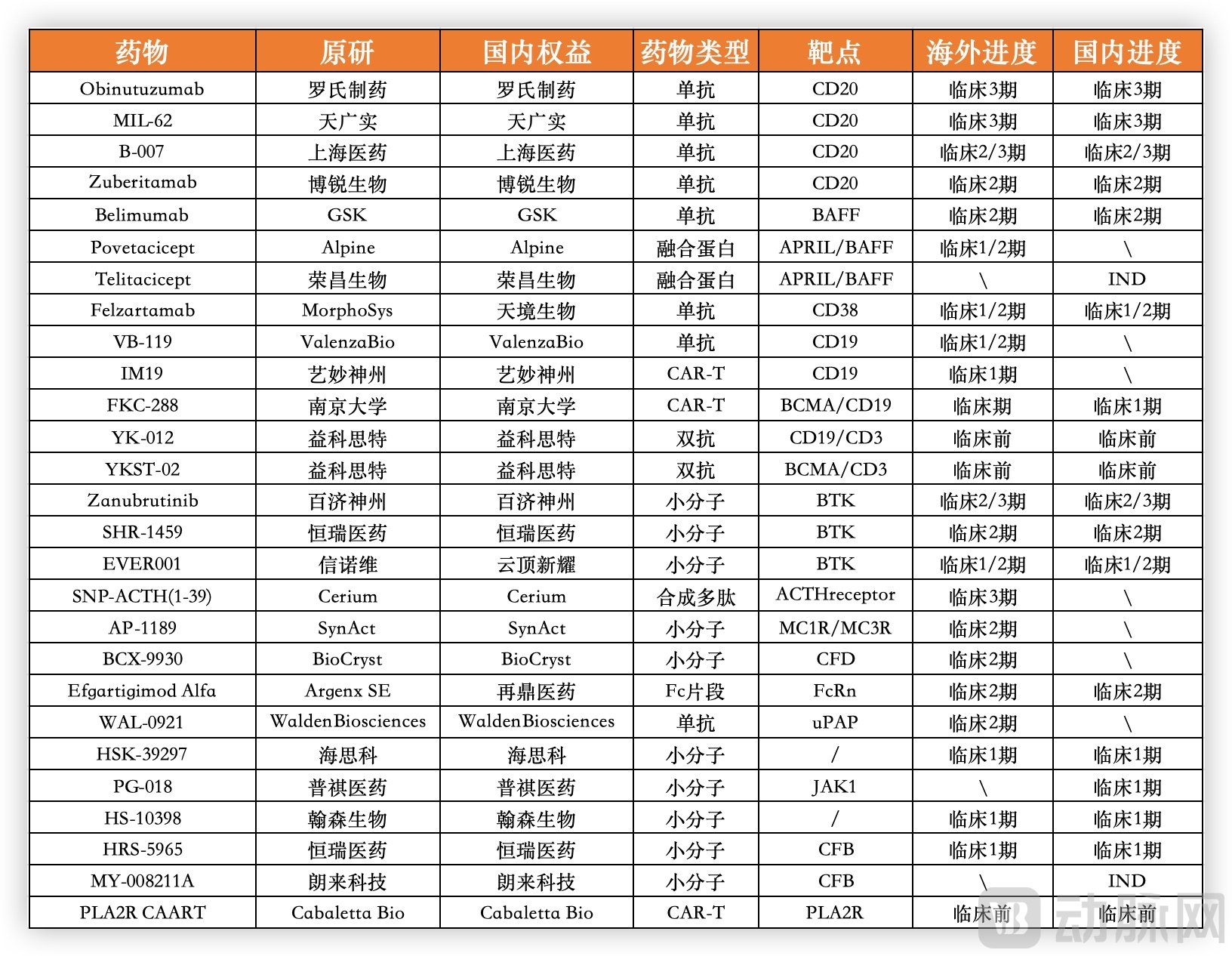

Global R&D Pipeline of Major Drugs for Primary Membranous Nephropathy; Data Sourced from Pharmaceutical Companies’ Official Websites and Great Wall Securities

Using rituximab as a benchmark, we can gauge the potential of the current pipeline. In the pivotal MENTOR trial of rituximab (NCT01180036), the rates of complete remission (CR) and partial remission (PR) of proteinuria at 6 and 12 months were 35% and 60%, respectively. Regarding safety, the incidence of adverse events (AEs) was 71%, while the incidence of grade ≥3 AEs and serious adverse events (SAEs) was 17%.

Roche’s obinutuzumab, a second-generation anti-CD20 monoclonal antibody, primarily exerts its therapeutic effect by targeting the CD20 protein on the surface of B lymphocytes, thereby eliminating B cells implicated in the pathogenesis of membranous nephropathy. Clinical data have demonstrated complete remission (CR) and partial remission (PR) rates for proteinuria of 75% at 6 months and 90% at 12 months, along with a further reduced incidence of grade ≥3 adverse events (AEs).

MIL62, a CD20 monoclonal antibody developed by the Chinese company TianGuangShi, has also demonstrated promising potential in Phase 1/2 clinical trials. According to data presented by TianGuangShi Biologics at the 2024 Annual Academic Conference of the Chinese Society of Nephrology (CSN), the overall renal response rate (ORR) at 76 weeks in the MIL62 monotherapy group reached 71.7%. This outcome surpassed the historical data from the Rituximab MENTOR study at 18 and 12 months, indicating certain long-acting advantages. Furthermore, in the field of autoimmune diseases, MIL62 is being developed for multiple indications, including lupus nephritis, neuromyelitis optica spectrum disorders (NMOSD) in neuroimmunology, and systemic lupus erythematosus (SLE) in rheumatology and immunology. Currently, MIL62 is in the late stages of Phase 3 clinical development, with completion expected in 2025.

Beyond the traditional CD20 target, numerous other targets are under investigation, albeit with less-than-satisfactory efficacy.

For example, GSK’s BAFF monoclonal antibody belimumab showed in its Phase 2 clinical trial (NCT03949855) that, when combined with rituximab, it did not provide additional benefit compared to rituximab monotherapy; the proportions of complete remission (CR) and partial remission (PR) of proteinuria at 6 and 12 months were 23% and 67%, respectively.

Meanwhile, felzartamab, a CD38 monoclonal antibody acquired by Biogen through its acquisition of HI-Bio, showed in Phase 1/2 clinical trials that the partial remission (PR) rate for proteinuria at six months was only 13.3%, with no complete remissions (CR). As for other treatment regimens, such as tacrolimus combined with rituximab or corticosteroids plus cyclophosphamide, they fail to achieve an optimal balance between efficacy and safety.

Although aggressively exploiting the potential of the CD20 pathway along traditional lines may prove effective, true innovation currently appears to be emerging from BTK inhibitors.

In early December, Everest Medicines announced clinical data for its next-generation BTK inhibitor, EVER001, instantly emerging as a beacon of hope in the field of primary membranous nephropathy.

Previously, BTK inhibitors were commonly used for hematologic malignancy indications; however, their moment in the spotlight has emerged in the field of membranous nephropathy, where they even hold the potential to become first-in-class (FIC) or best-in-class (BIC) therapies.

BTK inhibitors target the B-cell signaling pathway, primarily functioning to inhibit B-cell maturation and proliferation and prevent their differentiation into plasma cells that produce autoantibodies, while also exerting broad regulatory effects on various other immune responses. This mechanism of action is fundamentally different from that of CD20 monoclonal antibody therapy, which works by depleting B cells.

Clinical Data on Drugs for Membranous Nephropathy (Non-Head-to-Head), Collected from Public Information

Based on clinical data, subjects in the two EVER001 cohorts completed treatment with dosing regimens of 100 mg once daily (QD) titrated to twice daily (BID) and 200 mg BID, respectively. In the low-dose group, 54.5% of patients achieved complete immunological response by Week 6, increasing to 90.9% by Week 28. In the high-dose group, 66.7% of patients achieved complete immunological response by Week 8, reaching 100% by Week 24.

Specifically, the baseline PLA2R autoantibody titer of patients in this clinical trial was 85.4 RU/mL, and serum albumin was 3.1 g/dL. Regarding the most important indicator of proteinuria improvement, the low-dose group exhibited a 78.3% reduction from baseline at Week 36. The proportions of subjects achieving complete remission (CR) and partial remission (PR) were 18.2% and 81.8%, respectively. The median time to proteinuria remission was 19.7 weeks, with no rebound in proteinuria observed during the subsequent follow-up period.

In the high-dose group, the partial remission (PR) rate reached 85.7% at Week 20, and a 73.8% reduction from baseline was observed at Week 24. Along with the decrease in 24-hour proteinuria, serum albumin levels increased by 33.6% in the low-dose group and 30.2% in the high-dose group at Weeks 36 and 24, respectively. The low-dose group returned to the normal range by Week 36, while the high-dose group approached the normal range by Week 24.

Regarding another key indicator, the reduction in anti-PLA2R autoantibodies, the low-dose group achieved a decrease of over 90% from baseline by Week 28, while the high-dose group also achieved a reduction of over 90% from baseline by Week 24. Meanwhile, the rate of complete immunological remission exceeded 90% in both groups, reaching 100% in the high-dose group. It is evident that the rate of anti-PLA2R reduction with EVER001 is comparable to that of Obinutuzumab and faster than that of Rituximab and other agents with different mechanisms of action.

In terms of safety, the incidence of adverse events (AEs) was 58%, with most being transient Grade 1 or 2 events, representing a significant improvement over the >70% AE incidence rate observed with rituximab. Meanwhile, typical clinically significant adverse events associated with BTK inhibitors, such as neutropenia, bleeding, and arrhythmias, were not observed—issues that had previously constrained the application of BTK inhibitors by multinational corporations (MNCs) such as Sanofi and Roche.

Compared with existing products and pipelines under development, EVER001, especially the high-dose group, is in a clearly leading position. For example, the current first-line recommended treatment regimen, rituximab, has CR and PR rates of 35% and 60% at 6 months and 12 months, respectively, which are far lower than the response rates of the two dose groups of EVER001 after 28 weeks. Even the second-generation CD20 monoclonal antibody obinutuzumab, which increased the CR and PR rates to 75% and 90% at 6 months and 12 months, respectively, still falls short of the data from the EVER001 high-dose group. The data for other pipelines targeting CaN, CD38, BAFF, and other targets are even lower.

Overall, EVER001 has demonstrated efficacy in reducing proteinuria and lowering anti-PLA2R autoantibody levels in clinical outcomes. It exhibits significant differentiated advantages over existing clinical treatment regimens and data reported from other investigational pipelines, highlighting its potential as a first-in-class (FIC) therapy in the blue-ocean market of membranous nephropathy.

Following oncology, autoimmune diseases have become the next arena of fierce competition among Chinese biotech firms, but blind overcrowding is not a viable strategy.

Although the domestic autoimmune disease sector has become intensely competitive, Chinese-made targeted therapies remain predominantly fast-follow products. Their target selection is relatively concentrated on popular targets with multiple indications, and their therapeutic areas are similarly focused. For instance, there are nearly 20 products targeting the popular IL-17 pathway that are either marketed or in clinical development. The same trend applies to targets such as JAK1, TYK2, and IL-4Rα. In diseases like atopic dermatitis, nearly 10 products have been launched or submitted for marketing approval, while more than 40 pipeline candidates are in late-stage clinical trials.

Indications such as membranous nephropathy, which have a large patient population, unmet clinical needs due to inadequate existing therapies, and limited corporate involvement, are undoubtedly attractive targets; however, few companies have made forward-looking strategic layouts in this area.

In addition to membranous nephropathy, EVER001 is being developed for minimal change disease (MCD) and focal segmental glomerulosclerosis (FSGS), as well as lupus nephritis (LN). The first two indications represent blue-ocean markets with patient populations in the millions and no currently approved therapies worldwide. Coupled with IgA nephropathy, which is covered by the budesonide enteric-coated capsules included in the National Reimbursement Drug List, Everest Medicines’ potential patient population in the nephrology field amounts to approximately 10 million. Notably, aside from IgA nephropathy, there are currently no approved therapies for the other indications.

Everest Medicines’ Portfolio in the Field of Nephrology, Source: Company Website

Coupled with the characteristics of an oral small-molecule drug, EVER001 offers advantages in safety and potential for combination therapy. Consequently, its clinical data release has attracted significant market attention. As previously mentioned, HI-Bio, Chinook, and Alpine secured high-value acquisitions by multinational corporations (MNCs) due to their core nephrology pipelines; similarly, expectations for EVER001’s business development (BD) prospects are rising accordingly.

Project initiation capabilities may become the core competitiveness of domestic biotech companies in the future.

Previously, drug development for kidney diseases was a niche field due to complex pathogenesis, long clinical trial cycles, and high evaluation thresholds. With the 2021 KDIGO guidelines recommending the reduction of proteinuria as a surrogate endpoint for assessing drug efficacy in slowing the progression of IgA nephropathy, the barrier to entry for drug development in the nephrology field is expected to decrease.

Under these circumstances, Everest Medicines has licensed EVER001 and secured global development rights for its use in the treatment of kidney diseases. Notably, when EVER001 was introduced in 2021 to target membranous nephropathy, among more than 20 BTK inhibitor pipelines under development in China, only Hengrui’s SHR-1459 covered this indication.

The chronic kidney disease market, serving tens of millions of patients, is merely the beginning. China’s innovative drug industry needs more Chinese biotech companies that can self-reinvent during their development and establish differentiated operational logic.

References:

"Evolution of the Spectrum of Chronic Glomerular Diseases and Epidemiological Characteristics of Membranous Nephropathy"

《Future landscape for the management of membranous nephropathy》

《Obinutuzumab versus rituximab for the treatment of refractory primary membranous nephropathy》